Key Takeaways

- French Guiana applies metropolitan French corporate law directly, meaning all entity types — including the SA, SAS, SARL, SNC, and SCS — are governed by the Code de commerce with no separate territorial legal framework.

- Company registration in French Guiana is processed through the Greffe du Tribunal de Commerce in Cayenne and the Centre de Formalités des Entreprises (CFE), using the same procedures that apply across French territory.

- The SAS is the most frequently chosen structure among residents and foreign investors due to its flexible governance rules, while the SA is better suited to larger enterprises requiring formal board structures and capital market access.

- Individuals seeking a low-threshold entry point can register under the auto-entrepreneur micro-enterprise regime, which offers simplified tax reporting through the micro-fiscal system rather than standard corporate income tax obligations.

Introduction to Entity Types in French Guiana

French Guiana is an overseas territory of France located on the northeastern coast of South America, bordered by Brazil to the south and east and Suriname to the west. As an integral part of the French Republic, it falls under French law rather than operating as a separate legal jurisdiction — meaning business entity types French Guiana businesses can adopt are drawn directly from metropolitan French corporate law.

Company registration is handled through the Greffe du Tribunal de Commerce, the commercial court registry, with filings also processed via the Centre de Formalités des Entreprises (CFE). Businesses operating here are subject to French national taxation, including corporate income tax and VAT, with no separate territorial tax regime.

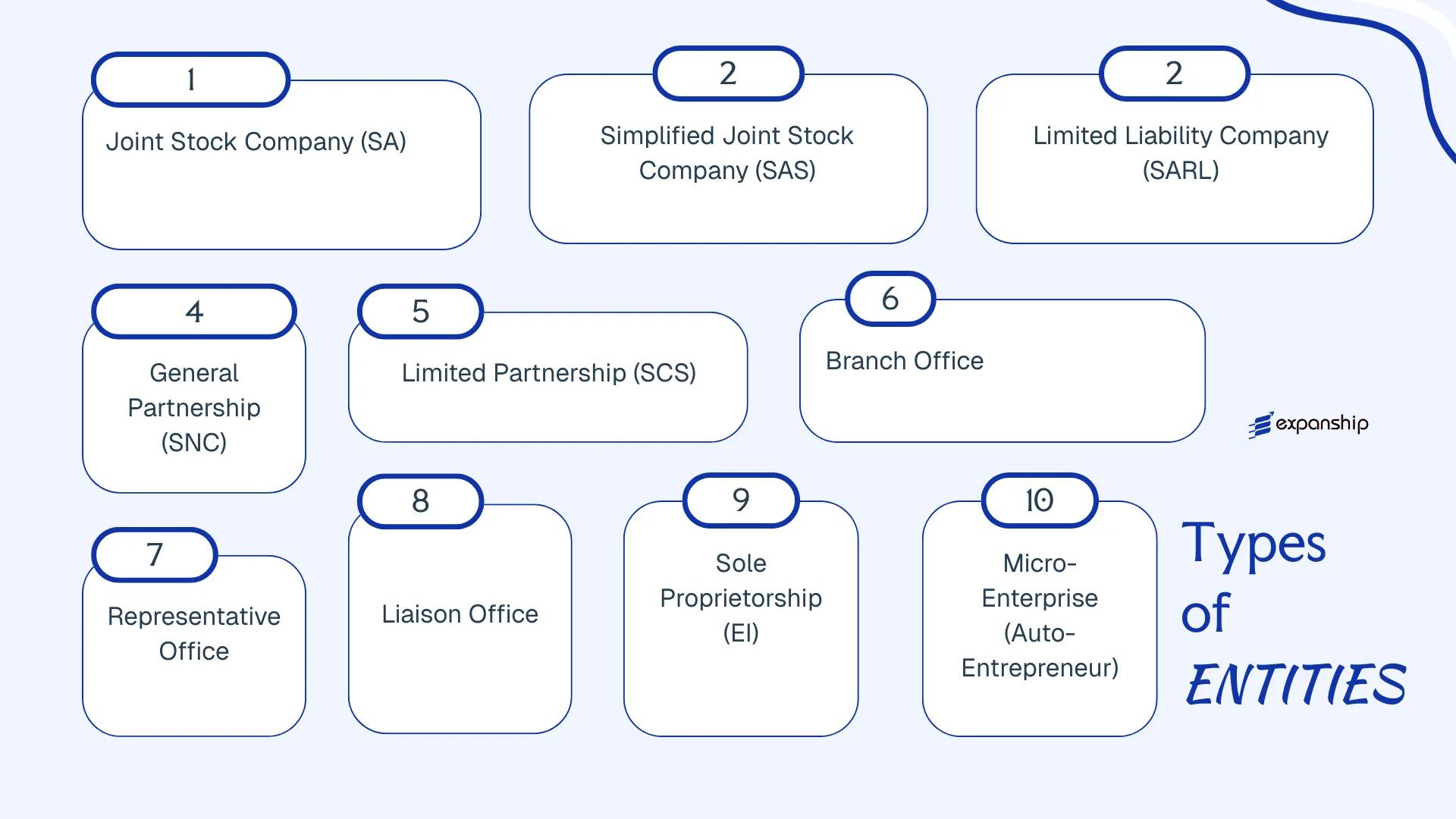

The legal structures available include the Société Anonyme (SA), Société par Actions Simplifiée (SAS), Société à Responsabilité Limitée (SARL), Société en Nom Collectif (SNC), Société en Commandite Simple (SCS), branch and representative offices for foreign firms, and the Entrepreneur Individuel (EI) along with the auto-entrepreneur micro-enterprise regime. Each structure carries distinct requirements around capital, liability, governance, and taxation that this article examines in detail.

An Overview of Business Structures in French Guiana

French Guiana operates under French commercial law, meaning the primary legislation governing corporate legal forms is the Code de commerce, supplemented by the Code civil and various implementing regulations applied at the departmental level. Several distinct entity types are available to investors and entrepreneurs, each structured for a different commercial purpose, scale of operation, or liability profile.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxation | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| SA | Joint Stock Company | Limited | Corporate tax | Permitted | 2 shareholders | Greffe du tribunal de commerce | Code de commerce |

| SAS | Simplified Joint Stock Company | Limited | Corporate tax | Permitted | 1 shareholder | Greffe du tribunal de commerce | Code de commerce |

| SARL | Limited Liability Company | Limited | Corporate tax / IR | Permitted | 1 associate | Greffe du tribunal de commerce | Code de commerce |

| SNC | General Partnership | Unlimited | IR (partners) | Permitted | 2 partners | Greffe du tribunal de commerce | Code de commerce |

| SCS | Limited Partnership | Mixed | IR (partners) | Permitted | 2 partners | Greffe du tribunal de commerce | Code de commerce |

| Branch Office | Foreign entity extension | Parent liable | Corporate tax | Permitted | N/A | Greffe du tribunal de commerce | Code de commerce |

| Representative Office | Non-trading presence | Parent liable | Generally exempt | Not permitted | N/A | Greffe du tribunal de commerce | Code de commerce |

| EI | Sole Proprietorship | Unlimited (separated assets) | IR | Permitted | 1 individual | CFE / Greffe | Code de commerce |

| Auto-Entrepreneur | Micro-enterprise regime | Limited (separated assets) | Flat levy / IR | Permitted | 1 individual | CFE / URSSAF | Code de commerce |

Each of these structures is examined in full in the sections below.

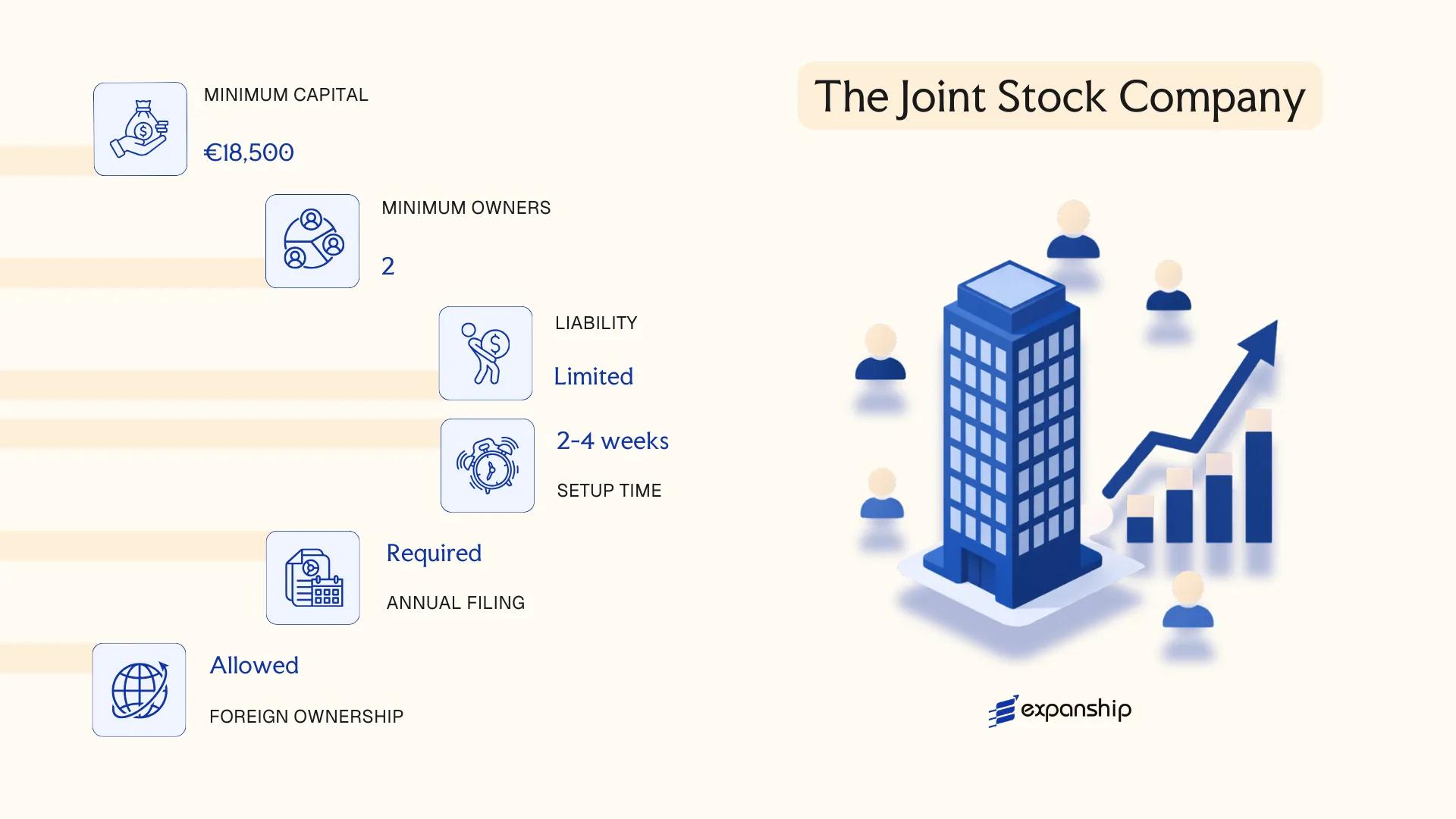

Société Anonyme (SA) — The Joint Stock Company

The Société Anonyme (SA) in French Guiana is governed by the French Commercial Code (Code de Commerce), specifically the provisions codified under Articles L225-1 through L225-270, which apply by virtue of French Guiana's status as an Overseas Department (Département d'Outre-Mer) of France. The entity carries full separate legal personality, meaning it exists independently of its shareholders.

Liability is limited to each shareholder's capital contribution. The SA structure accommodates both public and private capital-raising, making it the default form for larger enterprises, publicly traded companies, or ventures requiring institutional investment.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Société Anonyme (SA) | Separate legal personality; governed by French Commercial Code |

| Members | Shareholders (actionnaires); minimum 2 (non-public), minimum 7 (public) | No maximum; shares freely transferable unless restricted by statutes |

| Governance | Board of Directors (Conseil d'Administration) or Supervisory Board + Management Board; minimum 3 directors | Directors need not be residents of French Guiana |

| Local Presence | Registered office (siège social) required in French Guiana | No statutory requirement for a local resident director |

| Share Capital | Minimum EUR 37,000 (non-public); EUR 225,000 if shares offered to public | At least half must be paid up at incorporation; remainder within 5 years |

| Privacy | Shareholder identity disclosed in filings with the Greffe du Tribunal de Commerce | Beneficial ownership reported to the national Registre des bénéficiaires effectifs |

Focus Points

- Taxation: Subject to French corporate income tax (impôt sur les sociétés) at the standard rate of 25%; VAT applies at standard French rates; dividends paid to non-residents may attract withholding tax, though France's extensive tax treaty network can reduce or eliminate this.

- Annual Compliance: Statutory accounts must be filed annually with the Greffe; a statutory auditor (commissaire aux comptes) is mandatory regardless of size for the SA form.

- Economic Substance: As a French DOM, French Guiana does not impose separate substance requirements beyond standard French corporate law obligations.

- Conversion: An SA can be converted into an SAS or SARL by shareholder resolution, subject to compliance with capital and governance requirements of the target form.

- Restrictions: Certain regulated sectors (financial services, insurance) require prior authorisation from French supervisory authorities such as the Autorité de Contrôle Prudentiel et de Résolution (ACPR).

Closing

The SA suits capital-intensive businesses, joint ventures with multiple institutional investors, and entities anticipating a public listing. The mandatory auditor requirement and higher minimum capital threshold make it administratively heavier than simpler structures.

The SA is most appropriate for large enterprises, institutional joint ventures, or businesses planning to access public capital markets.

Company Incorporation in French Guiana

Incorporate your Société Anonyme or other entity type in French Guiana with end-to-end support from Expanship.

Société par Actions Simplifiée (SAS) — The Simplified Joint Stock Company

The Société par Actions Simplifiée SAS French Guiana operates under the same French Commercial Code that governs metropolitan France, given that French Guiana is an overseas department and region (département et région d'outre-mer) of France. Introduced into French law in 1994 and significantly liberalised by the Loi de modernisation de l'économie (LME) of 2008, the SAS carries full legal personality and offers shareholders limited liability capped at their capital contributions.

Its defining characteristic is contractual flexibility. The articles of association (statuts) govern most internal arrangements, including governance structure, share transfer conditions, and decision-making thresholds, giving founders considerable latitude that more rigid structures do not permit.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Société par Actions Simplifiée | Separate legal entity; limited liability |

| Members | Shareholders (actionnaires) | Minimum 1 (SASU if sole); no maximum |

| Management | President (Président) | At least one; can be an individual or legal entity; no nationality requirement |

| Local Presence | Registered office in French Guiana required | No statutory requirement for a local director |

| Share Capital | No statutory minimum | Capital must be stated in the statuts; denominated in euros |

| Privacy | Shareholders not listed in the public Registre du Commerce et des Sociétés (RCS) | Beneficial ownership disclosed to TRACFIN under anti-money laundering rules |

Focus Points

- Taxation: Subject to standard French corporate income tax (currently 25%), VAT under the French system with local adaptations (a reduced rate applies in French Guiana under the octroi de mer regime), and French withholding tax on dividends, interest, and royalties paid to non-residents; France's extensive double tax treaty network is accessible.

- Annual Compliance: Annual accounts must be filed with the greffe du tribunal de commerce; statutory audit (commissaire aux comptes) is mandatory once two of three legal thresholds are exceeded (balance sheet, turnover, headcount).

- Economic Substance: No separate substance test beyond standard French corporate law requirements; the registered office must be genuine.

- Conversion: An SAS can be converted into an SA or SARL by shareholder resolution, subject to the conditions set out in the French Commercial Code.

- Restrictions: SAS shares cannot be offered to the public or listed on a regulated stock exchange.

Sub-Types

Société par Actions Simplifiée Unipersonnelle (SASU)

The SASU is a single-shareholder variant of the SAS, governed by the same provisions of the French Commercial Code. It is commonly used for wholly-owned subsidiaries or by individual entrepreneurs who require corporate liability protection without a multi-shareholder structure.

Closing

The SAS is widely used for operating subsidiaries, joint ventures, and holding structures where shareholders require tailored governance arrangements and anticipate future investment rounds. Its key advantage is the degree of freedom granted to the statuts, but that same flexibility demands carefully drafted constitutional documents — poorly structured articles can create operational or legal ambiguity.

The SAS suits startups, foreign subsidiaries, and multi-investor ventures where bespoke governance and scalable share structures take priority over administrative simplicity.

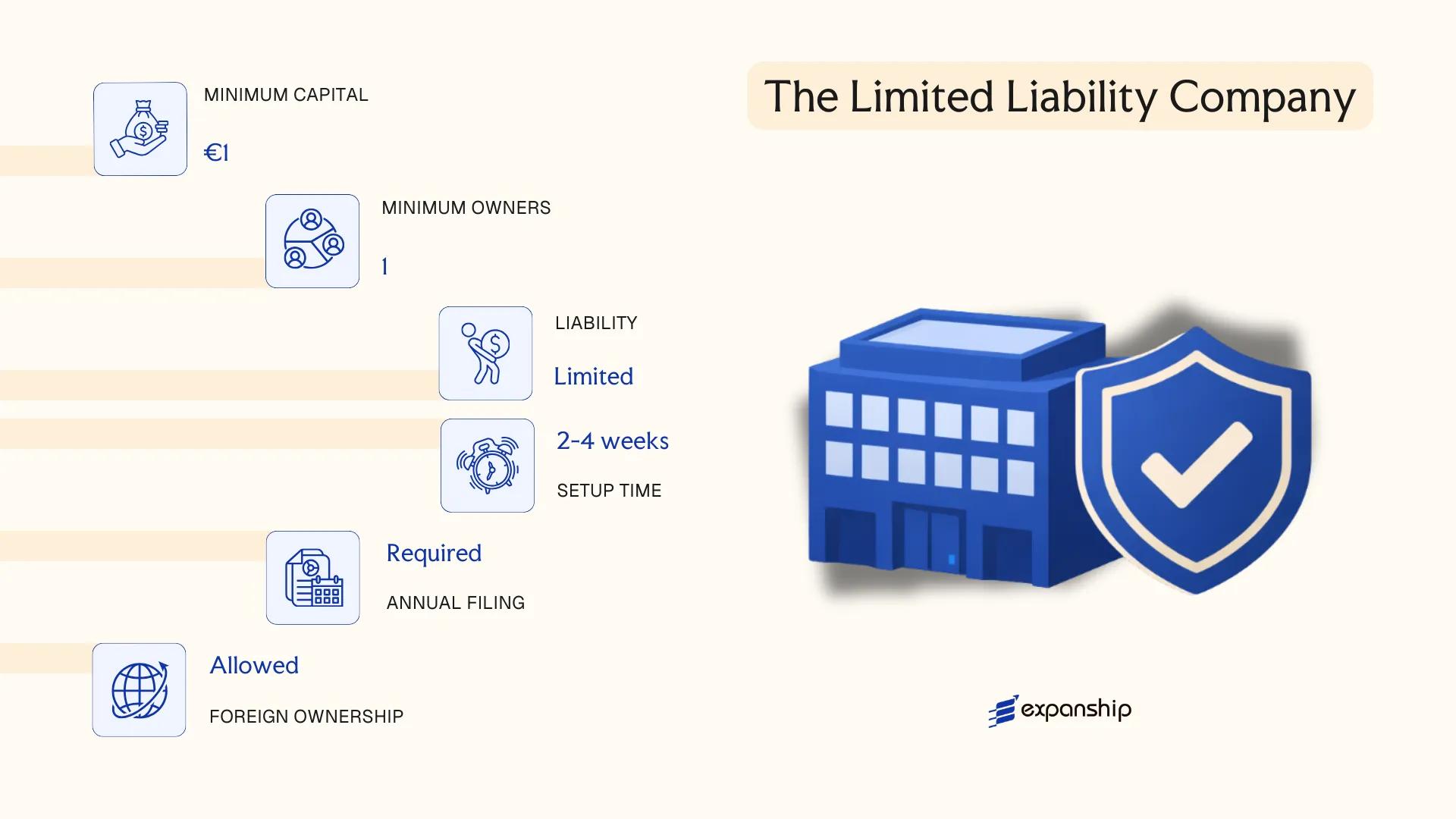

Société à Responsabilité Limitée (SARL) — The Limited Liability Company

The Société à Responsabilité Limitée SARL French Guiana operates under French commercial law, specifically the provisions of the Code de Commerce, which applies in full as an overseas department (département d'outre-mer) of France. As a hybrid entity, it combines limited liability protection with a more flexible management structure than a public company.

Each associé (member) is liable only to the extent of their capital contribution. The SARL holds a distinct legal personality separate from its members, allowing it to own assets, enter contracts, and bear obligations in its own name.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited liability company with separate legal personality | Governed by the French Code de Commerce |

| Members | 1 to 100 associés (shareholders) | Single-member variant is the EURL |

| Management | One or more gérants (managers) | Gérant may be a member or a third party |

| Local Presence | Registered office (siège social) required in French Guiana | No statutory requirement for a resident gérant |

| Share Capital | No statutory minimum since 2003; €1 is legally sufficient | Capital divided into parts sociales, not freely transferable |

| Privacy | Gérant identity disclosed in public register (RCS) | Beneficial ownership reported to the registre des bénéficiaires effectifs |

Focus Points

- Taxation: Subject to standard French corporate income tax (IS) at 25%; VAT applies under French rules; withholding tax on dividends distributed to non-residents is generally 30% unless reduced by an applicable tax treaty.

- Annual compliance: Mandatory filing of annual accounts with the Greffe du Tribunal de Commerce; statutory accounts must be approved by members within six months of the financial year-end.

- Transfer restrictions: Parts sociales require member approval for transfer to third parties; this restricts free exit.

- Conversion: A SARL may be converted into an SAS or SA by member vote, subject to Code de Commerce procedures.

- Treaty access: As an integral part of France, the entity benefits from France's extensive network of double taxation treaties.

Sub-Types

Entreprise Unipersonnelle à Responsabilité Limitée (EURL)

The EURL is a single-member SARL. The sole associé may also act as gérant, making it the standard structure for individual entrepreneurs who require limited liability without a multi-member arrangement.

Closing

The SARL suits small to medium-sized businesses, family-owned firms, and joint ventures where members want liability protection alongside control over share transfers. Its primary limitation is the restriction on transferring parts sociales, which reduces liquidity for investors seeking exit flexibility.

Small to medium enterprises and family businesses where ownership stability and limited liability take priority over capital market access.

Société en Nom Collectif (SNC) and Société en Commandite Simple (SCS) [General Partnership, Limited Partnership]

Both the Société en Nom Collectif and the Société en Commandite Simple are governed by French commercial law as extended to French Guiana under the principle of legislative assimilation — principally through the Code de Commerce. Each structure carries separate legal personality upon registration with the Greffe du Tribunal de Commerce.

The SNC is a general partnership in which all partners bear unlimited, joint and several liability for the firm's debts. The SCS introduces a two-tier membership structure: at least one general partner (commandité) retains unlimited liability, while one or more limited partners (commanditaires) are liable only up to their capital contribution.

Key Characteristics

| Requirement | SNC | SCS |

|---|---|---|

| Legal Form | General Partnership | Limited Partnership |

| Members | Partners (associés); minimum 2, no maximum | Min. 1 commandité (general) + 1 commanditaire (limited); no maximum |

| Liability | Unlimited, joint and several for all partners | Unlimited for commandités; limited to contribution for commanditaires |

| Minimum Capital | None required | None required |

| Registered Office | Must be maintained in France / French Guiana | Must be maintained in France / French Guiana |

| Privacy | Partners' names filed at the Greffe; publicly accessible | Same disclosure obligations; commanditaires listed in the statuts |

Focus Points

- Taxation: Both structures are fiscally transparent by default under the French tax regime; profits are taxed at the partner level rather than entity level, though partners may elect corporate tax (IS) in certain circumstances. Standard French VAT rules apply.

- Annual Compliance: Annual accounts must be filed with the Greffe du Tribunal de Commerce; failure to file may result in penalties under the Code de Commerce.

- Treaty Access: As an overseas territory under French sovereignty, French Guiana falls within France's tax treaty network, subject to entity-level qualification criteria.

- Transfer of Interests: In an SNC, transferring a partner's share requires unanimous consent of all partners, making ownership changes structurally rigid.

Closing Paragraph

Both structures suit closely held businesses where partners maintain direct operational control, with the SCS offering a useful vehicle for arrangements where passive capital contributors require liability protection. The unlimited liability exposure for general partners remains a significant structural constraint for most commercial applications.

The SNC and SCS are best suited for small, trust-based partnerships or family-held enterprises where the partners accept personal liability in exchange for simplified governance and tax transparency.

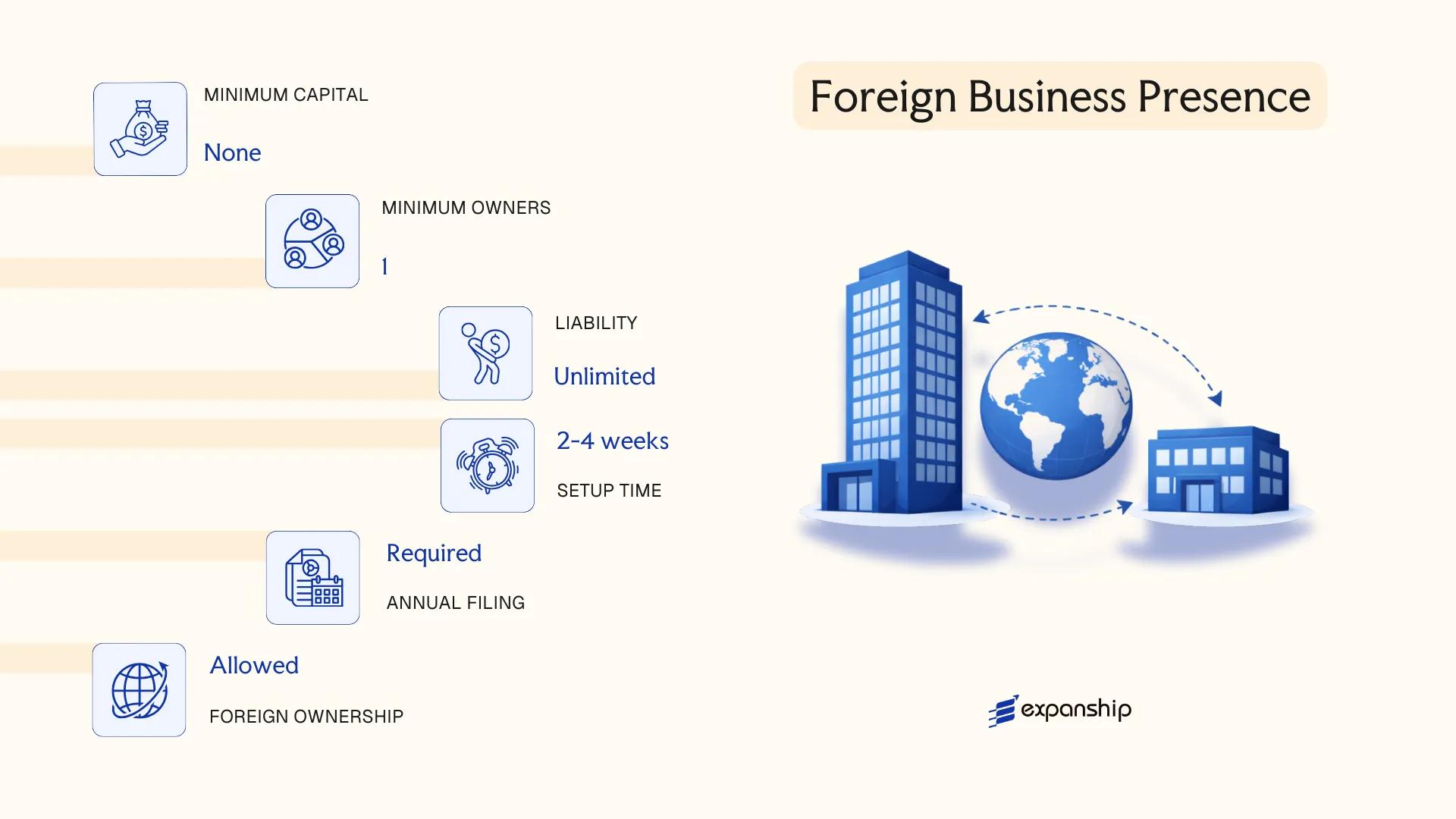

Foreign Business Presence in French Guiana [Branch Office, Representative Office, Liaison Office]

As an overseas territory of France, French Guiana falls under French commercial law, meaning a foreign company branch office in French Guiana is governed by the same legal framework as metropolitan France, primarily the Code de commerce. Foreign firms operating through a branch do not create a separate legal entity; the parent company retains full liability for all obligations incurred locally.

Registration is handled through the Greffe du Tribunal de Commerce (Commercial Court Registry) in Cayenne. A branch must be registered in the Registre du Commerce et des Sociétés (RCS) before commencing any commercial activity.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Branch / Representative / Liaison Office | Branch conducts commercial activity; liaison office is limited to non-commercial functions |

| Legal Personality | None | Parent company bears full legal and financial liability |

| Represented By | Permanent Representative (Représentant Permanent) | Must be appointed and registered with the RCS |

| Local Presence | Registered address in Cayenne required | Physical office address; PO boxes not accepted |

| Capital | No minimum capital required | Parent company's capital serves as financial backing |

| Privacy | Parent company details publicly disclosed via RCS filing | French commercial registry is publicly searchable |

Focus Points

- Taxation: The branch is subject to French corporate income tax (currently 25%) on profits attributable to French Guiana activities; VAT applies at standard French rates; withholding tax may apply on profit remittances to the foreign parent depending on applicable tax treaties.

- Economic Substance: The permanent representative must maintain genuine local operational activity; purely nominal presence risks reclassification by tax authorities.

- Annual Compliance: Annual accounts of the branch must be filed with the Greffe, and the parent company's accounts may also be required for disclosure.

- Treaty Access: France's extensive tax treaty network applies; eligibility depends on the parent company's residence jurisdiction and treaty terms.

- Restrictions: A liaison office is strictly limited to market research and promotional activities and cannot generate revenue or sign commercial contracts locally.

Sub-Types

Branch Office (Succursale)

A branch conducts full commercial operations in French Guiana under the parent company's name and legal identity. It can enter contracts, employ staff, and generate revenue, but all liabilities flow directly to the foreign parent.

Liaison Office (Bureau de Représentation)

A liaison office may only carry out preparatory or auxiliary activities such as market research or supplier coordination. It cannot invoice clients or conclude binding commercial agreements, making it suitable for firms assessing market entry before committing to a full commercial presence.

Closing Remarks

A branch structure suits foreign firms seeking direct commercial activity without the administrative burden of incorporating a new local entity, though the unlimited liability exposure of the parent company is a significant operational risk to account for before proceeding.

Foreign companies with an established parent entity seeking a cost-efficient commercial foothold, particularly those whose home jurisdiction has a tax treaty with France.

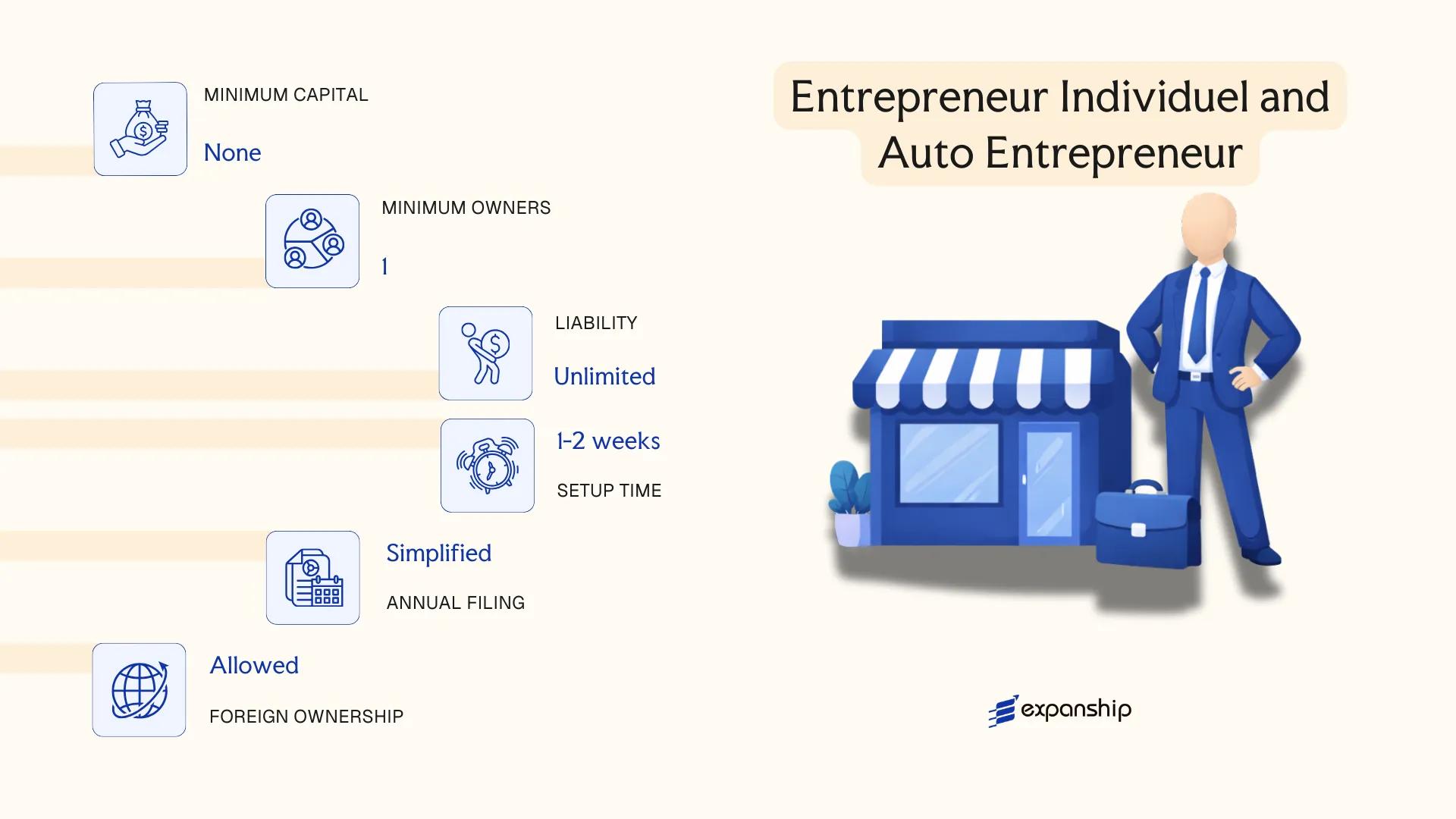

Entrepreneur Individuel (EI) and Auto-Entrepreneur [Sole Proprietorship, Micro-Enterprise]

As an overseas department of France, French Guiana applies French national law directly, meaning the Loi n° 2022-172 du 14 février 2022 governs the Entrepreneur Individuel status. This reform merged previously distinct sole trader statuses and introduced automatic asset separation, giving the EI a partial liability shield without requiring a separate legal entity.

The auto-entrepreneur micro-enterprise French Guiana regime operates as a simplified sub-status within the EI framework, subject to revenue thresholds set annually by French fiscal authorities. Registration for Entrepreneur Individuel French Guiana follows the standard French procedure through the Guichet unique platform managed by the Institut National de la Propriété Industrielle (INPI), which replaced the former Centre de Formalités des Entreprises (CFE) network in 2023.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole proprietorship with statutory asset separation | No separate legal personality; professional and personal estates are legally distinct since the 2022 reform |

| Proprietor | Single natural person only | The individual is both owner and operator; no shareholders or partners permitted |

| Capital | None required | No minimum capital; business is funded entirely by the proprietor |

| Local Presence | Declared business address in France or an overseas department | A domiciliation address in French Guiana suffices |

| Revenue Ceiling (Auto-Entrepreneur) | €77,700 (services) / €188,700 (commercial) for 2024 | Exceeding thresholds triggers automatic exit from the micro-enterprise regime |

| Privacy | Proprietor's identity is publicly registered | INPI register is publicly searchable |

Focus Points

- Taxation: Auto-entrepreneurs pay income tax under the versement libératoire flat-rate option (1%–2.2% on turnover depending on activity), or standard progressive income tax bands; standard EI is taxed on net profit at personal income tax rates; VAT exemption applies below the franchise en base threshold.

- Social Contributions: Calculated as a percentage of turnover under the micro-enterprise regime, with reduced rates available for new registrants under ACRE (Aide à la Création et à la Reprise d'une Entreprise).

- Annual Compliance: Monthly or quarterly turnover declarations to URSSAF; no statutory audit required; no annual accounts filing obligation for micro-enterprises.

- Conversion: An EI can be converted into a EURL or SASU without asset liquidation, enabling a structural upgrade if the business grows beyond micro-enterprise thresholds.

- Restrictions: The sole proprietor cannot bring in equity partners; access to double taxation treaties is through the individual's personal tax residency, not a corporate structure.

Sub-Types

Auto-Entrepreneur (Micro-Entreprise)

This status is available to EIs whose turnover remains below the annual fiscal thresholds. It applies a simplified flat-rate calculation for both social contributions and tax, eliminating the need for deductible expense accounting. It is primarily used for freelance, consulting, and small-scale commercial activities.

Recommendations

The EI and auto-entrepreneur regime suits low-overhead, single-operator activities where administrative simplicity outweighs the need for equity structuring. The primary advantage is the elimination of minimum capital requirements combined with the 2022 liability shield; the key drawback is the revenue ceiling that limits scalability under the micro-enterprise sub-status.

Freelancers, independent consultants, and sole traders testing a new market in French Guiana with minimal upfront commitment and no intention of raising external capital.

How to Choose the Right Entity Type in French Guiana

Choosing the right company structure in French Guiana directly affects your tax position, liability exposure, and long-term compliance obligations. The French commercial code — as applied in French Guiana through its status as an overseas department — governs these structures under the Code de commerce.

Why Your Entity Choice Matters

Selecting the wrong entity type produces concrete, correctable-but-costly outcomes:

- Registering as an auto-entrepreneur while conducting activity that exceeds the turnover thresholds set by the régime micro-entreprise results in automatic disqualification from that regime and potential retroactive tax reassessment.

- Choosing a structure without legal personality, such as an SNC, when operating in a regulated sector means the licensing authority may refuse registration entirely.

- Forming a SARL when your activity requires external investment rounds creates structural friction, since SARL share transfers to third parties require prior approval from existing associates under Article L223-14 of the Code de commerce.

- Selecting an EI when multiple parties need defined ownership stakes offers no mechanism for equity allocation, which can trigger disputes with no statutory resolution path.

Key Factors to Consider

- Business Activity: Active trading, asset holding, and regulated sectors each carry distinct capital and governance requirements under French commercial law.

- Ownership Structure: A single founder has different statutory obligations than a multi-party arrangement requiring a board or supervisory structure.

- Liability Exposure: Your tolerance for personal liability determines whether an unincorporated structure is acceptable or whether separate legal personality is necessary.

- Tax Regime Eligibility: Certain entities qualify for the impôt sur les sociétés while others are fiscally transparent, pushing income directly to associates.

- Substance Capacity: If you cannot maintain local management and decision-making, structures with lower administrative thresholds are more appropriate.

- Exit and Conversion: Not all French entities permit straightforward conversion; verify whether your chosen structure allows redomiciliation or statutory transformation before registering.

Compliance Services for Companies in French Guiana

Maintain good standing and meet ongoing statutory obligations for your French Guiana entity.

Conclusion

French Guiana operates under French commercial law, making it one of the few territories in South America where EU-standard corporate regulations apply directly. This company formation French Guiana guide has covered each recognized entity type available under the Code de commerce as applied in the territory.

The SAS remains the most commonly registered structure among both residents and foreign investors, valued for its flexible governance rules. The SA suits larger enterprises requiring a formal board structure and capital market access. A SARL fits closely held businesses with a defined ownership group, while the SNC and SCS are reserved for partners prepared to accept personal liability. For individuals, the auto-entrepreneur regime offers a low-threshold entry point with simplified tax reporting under the micro-fiscal system.

Regulatory alignment with metropolitan France continues to shape the business environment here, with compliance obligations tracking directly from Paris. Your chosen structure will be governed by the same Greffe du Tribunal de commerce procedures that apply across French territory.

How Expanship Can Assist You

As a dedicated corporate services provider French Guiana businesses and foreign investors rely on, Expanship guides you through the full incorporation process — from selecting between an SAS, SARL, or SA to filing with the Greffe du Tribunal de Commerce de Cayenne. Every step is handled with direct knowledge of French commercial law as it applies in this overseas department.

From document preparation to post-incorporation obligations, our team covers the practical work so your business can move forward.

- Constitutional document drafting and notarization

- Registered office and legal agent provision in French Guiana

- Filing and liaison with the Greffe du Tribunal de Commerce

- INSEE registration and SIREN/SIRET number coordination

- Ongoing compliance and annual obligations management

- Banking introduction assistance for newly incorporated entities

Reach out to Expanship French Guiana to discuss your incorporation requirements directly.

Frequently Asked Questions (FAQ)

The Société par Actions Simplifiée (SAS) is the most frequently formed structure. Its flexible governance rules and absence of a statutory minimum share capital make it accessible across a wide range of business sizes and sectors.

Both structures offer limited liability, but the SAS allows broader contractual freedom in drafting shareholder agreements, while the SARL operates under more prescriptive statutory rules governed by the Code de commerce. Tax treatment is broadly equivalent by default, though both can elect for income tax treatment under specific conditions. The SAS is generally preferred for multi-investor structures, whereas the SARL suits smaller, closely held businesses.

French law requires all commercial entities to register with the Registre du Commerce et des Sociétés (RCS), so full anonymity is not available. Beneficial ownership information is also subject to disclosure requirements under EU anti-money laundering directives as transposed into French law. Nominee arrangements do not eliminate disclosure obligations in this jurisdiction.

A single individual can form an SAS (as a SASU) or a SARL (as an EURL), and can register as an Entrepreneur Individuel. The Société en Nom Collectif and Société en Commandite Simple each require at least two partners by statutory definition, making sole formation impossible for those structures.

Non-residents and foreign nationals can form an SAS, SARL, or SA without holding French citizenship, provided they comply with registration requirements at the RCS and obtain any applicable professional authorizations. Certain regulated activities may require additional licensing regardless of nationality. Operating through a branch is also available for foreign companies already incorporated abroad.

Conversion between entity types is permitted under the Code de commerce, with the SARL-to-SAS conversion being the most frequently executed transformation. The process requires shareholder approval, updated statuts, and re-registration with the RCS. Not all conversions follow an identical procedural path, so the specific transformation sought determines the formalities involved.

The SA, SAS, SARL, SNC, and SCS all acquire separate legal personality upon registration with the RCS. The Entrepreneur Individuel, by contrast, does not create a distinct legal entity, though reforms introduced under the loi du 14 février 2022 established a statutory separation between personal and professional assets for sole traders.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.