Key Takeaways

- The International Business Company (IBC) is Grenada's primary vehicle for non-resident entrepreneurs seeking tax-exempt holding or trading arrangements under a territorial tax regime.

- Private companies limited by shares, registered under the Companies Act (Cap. 77) and overseen by the Grenada Companies and Intellectual Property Office, represent the most commonly formed business structure in the jurisdiction.

- Branch offices and representative offices allow foreign entities to establish a presence in Grenada without creating a separate legal person, distinguishing them structurally from locally incorporated entities.

- Grenada's regulatory framework distributes oversight between the Grenada Industrial Development Corporation (GIDC), the Registrar of Companies, and GARFIN, which supervises relevant licensed financial entities.

Introduction to Entity Types in Grenada

Grenada is a sovereign island nation in the southeastern Caribbean, situated northeast of Venezuela and southwest of Barbados, within the Windward Islands group. As an independent state and member of the Commonwealth, it maintains a legal framework rooted in English common law, which shapes how corporate entities are formed and governed.

Company registration falls under the jurisdiction of the Grenada Industrial Development Corporation (GIDC) and the Registrar of Companies, which operates under the Companies Act. International business activity is also subject to oversight by the Grenada Authority for the Regulation of Financial Institutions (GARFIN) for relevant licensed entities. The tax posture is broadly territorial, with certain structures — particularly those serving non-resident interests — benefiting from exemptions on foreign-source income.

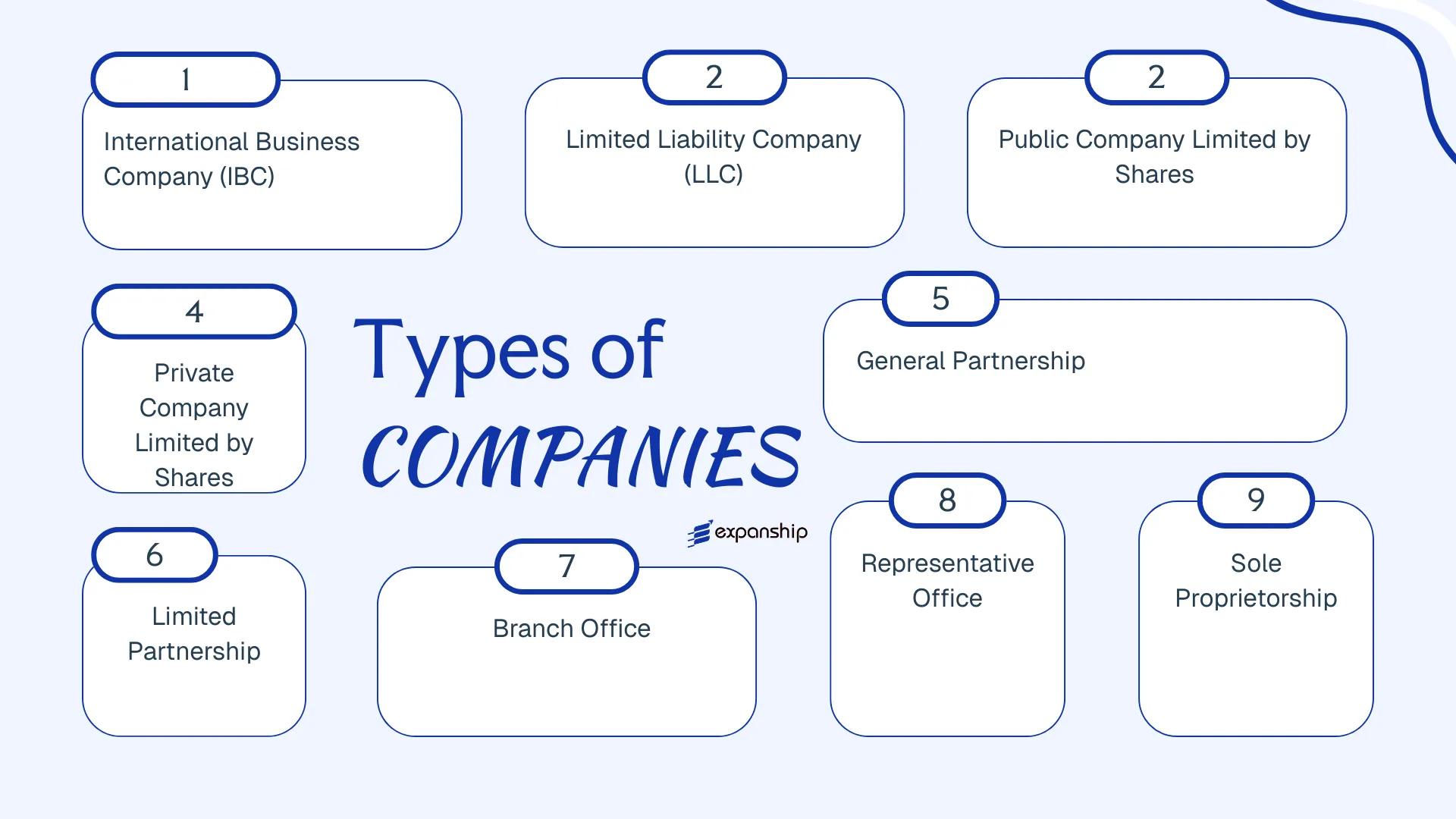

The types of business entities available in Grenada include:

- International Business Company (IBC)

- Limited Liability Company (LLC)

- Public Company Limited by Shares

- Private Company Limited by Shares

- General Partnership

- Limited Partnership

- Branch Office

- Representative Office

- Sole Proprietorship

Each structure carries distinct requirements around ownership, liability, governance, and applicable regulation. This article examines each entity type to help you determine which formation aligns with your operational and compliance objectives.

An Overview of Business Structures in Grenada

Grenada's company law framework provides several distinct entity types, each governed primarily by the Companies Act, Cap. 55 of the Laws of Grenada, alongside specific legislation such as the International Business Companies Act. Each structure carries different implications for liability, taxation, and permitted commercial activity.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| IBC | Corporate body | Limited | Exempt | Not permitted | 1 shareholder | Grenada Authority for the Regulation of Financial Institutions (GARFIN) | IBC Act |

| LLC | Hybrid entity | Limited | Taxable | Permitted | 1 member | Grenada Companies Registry | Companies Act |

| Public Company | Corporate body | Limited | Taxable | Permitted | 7 shareholders | Grenada Companies Registry | Companies Act |

| Private Company | Corporate body | Limited | Taxable | Permitted | 1 shareholder | Grenada Companies Registry | Companies Act |

| General Partnership | Unincorporated | Unlimited | Taxable | Permitted | 2 partners | Grenada Companies Registry | Partnership Act |

| Limited Partnership | Unincorporated | Mixed | Taxable | Permitted | 2 partners | Grenada Companies Registry | Partnership Act |

| Branch Office | Extension of foreign entity | Parent liable | Taxable | Permitted | N/A | Grenada Companies Registry | Companies Act |

| Representative Office | Non-trading presence | Parent liable | Generally exempt | Not permitted | N/A | Grenada Companies Registry | Companies Act |

| Sole Proprietorship | Unincorporated | Unlimited | Taxable | Permitted | 1 owner | Grenada Companies Registry | Business Names Act |

Each of these structures is examined in full in the sections below.

International Business Company (IBC) in Grenada

Governed by the International Business Companies Act (Cap. 117), the Grenada International Business Company IBC is a corporate structure designed primarily for cross-border commercial activity. The entity carries separate legal personality, meaning it can contract, hold assets, and incur liabilities in its own name, distinct from its shareholders.

Liability exposure is limited to each member's subscribed capital contribution. The structure draws on elements from both common law company frameworks and offshore corporate practice, making it adaptable for a range of international commercial purposes.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Corporation (separate legal entity) | Governed by the IBC Act, Cap. 117 |

| Members | Shareholders (min. 1, no maximum) | Corporate shareholders permitted; bearer shares are prohibited |

| Directors | Min. 1 director; no residency requirement | Corporate directors generally permitted |

| Local Presence | Registered Agent required; no physical office mandate | Registered Agent must be licensed in Grenada |

| Share Capital | No statutory minimum; denominated in any currency | Par value or no-par-value shares both permitted |

| Privacy | Beneficial ownership not on public register | Register maintained by Registered Agent |

Focus Points

- Taxation: IBCs are generally exempt from Grenadian corporate income tax, withholding tax, and stamp duty on income sourced outside the jurisdiction; VAT obligations do not typically apply to qualifying offshore activities.

- Economic Substance: IBCs conducting certain activities may be subject to economic substance requirements under CARICOM-aligned regulations; professional advice should confirm applicability.

- Annual Compliance: Annual renewal fees are payable to maintain good standing; financial statements are not required to be filed publicly.

- Treaty Access: Grenada's treaty network is limited, which may restrict the IBC's ability to claim double tax treaty benefits in counterparty jurisdictions.

- Restrictions: IBCs are prohibited from conducting business with Grenadian residents or owning real property within Grenada without specific authorisation.

Closing

IBC registration in Grenada suits international holding structures, IP ownership vehicles, and cross-border trading companies where income originates entirely outside the jurisdiction. The primary advantage is the tax exemption framework for non-resident income; the principal limitation is restricted treaty access, which can affect withholding tax exposure on certain cross-border payments.

Best suited for non-resident entrepreneurs and international businesses seeking a tax-neutral offshore vehicle for holding, trading, or IP management with minimal local administrative obligations.

Company Incorporation in Grenada

Register an IBC or other corporate structure in Grenada with end-to-end support from Expanship.

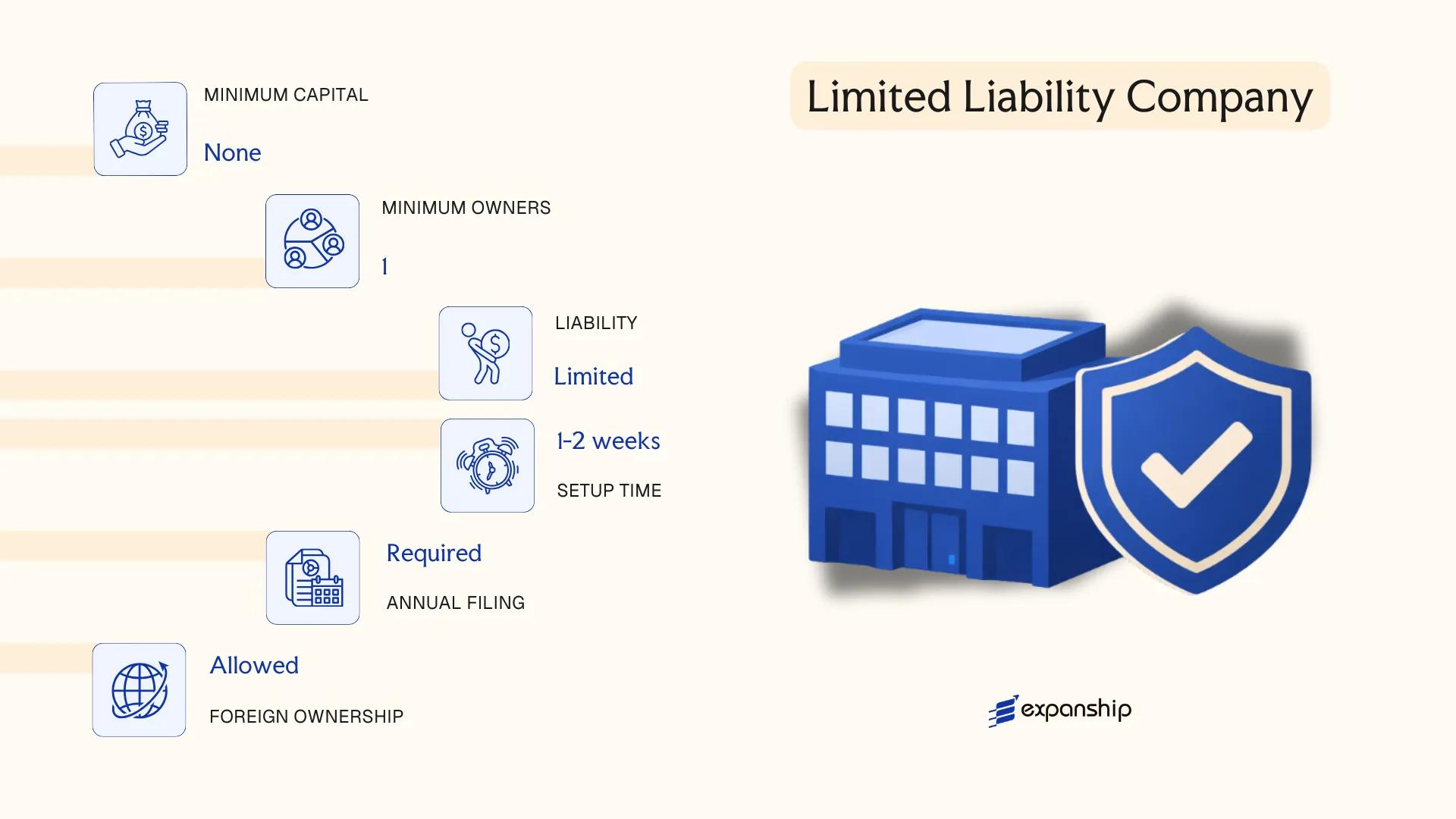

Limited Liability Company (LLC) in Grenada

Grenada LLC formation requirements are governed primarily by the Companies Act, Cap. 62 of the Laws of Grenada, which provides for the formation of companies with limited liability. An LLC in this jurisdiction carries separate legal personality, meaning the entity can own assets, enter contracts, and incur liabilities in its own name, distinct from its members.

Members' financial exposure is confined to their capital contribution, which is the defining characteristic of this structure. The hybrid nature of the LLC allows for flexible internal governance while maintaining the liability shield that makes it suitable for a range of commercial activities.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Company | Governed under the Companies Act, Cap. 62 |

| Members | Minimum 1 shareholder; no statutory maximum | Shareholders can be individuals or corporate entities |

| Management | Minimum 1 director; no statutory maximum | Directors need not be resident in Grenada |

| Local Presence | Registered agent and registered office required | Must be maintained at all times |

| Share Capital | No mandatory minimum; denominated in Eastern Caribbean Dollars (XCD) or foreign currency | Par value or no-par-value shares permitted |

| Privacy | Shareholder names are on public record at the Companies Registry | Director information is also publicly filed |

Focus Points

- Taxation: Subject to Grenada's corporate income tax at the standard rate; VAT may apply to trading activities; withholding tax applies to dividends, interest, and royalties paid to non-residents; stamp duty is assessed on certain instruments.

- Annual Compliance: Annual returns must be filed with the Grenada Companies Registry; financial records must be maintained in accordance with the Act.

- Economic Substance: Domestic LLCs conducting relevant activities may be subject to economic substance requirements under applicable regulations.

- Treaty Access: Grenada has a limited tax treaty network; treaty benefits are not broadly available to standard domestic LLCs.

- Conversion: The Act provides a mechanism for conversion to other corporate structures, subject to regulatory approval.

Closing Paragraph

The LLC structure is used for trading operations, holding arrangements, and service-based businesses where personal liability protection is a priority. A clear limitation is the public disclosure of shareholder and director information, which reduces confidentiality compared to certain offshore vehicles.

Best suited for entrepreneurs and small-to-medium businesses seeking a straightforward corporate structure with liability protection for domestic or regional commercial activities.

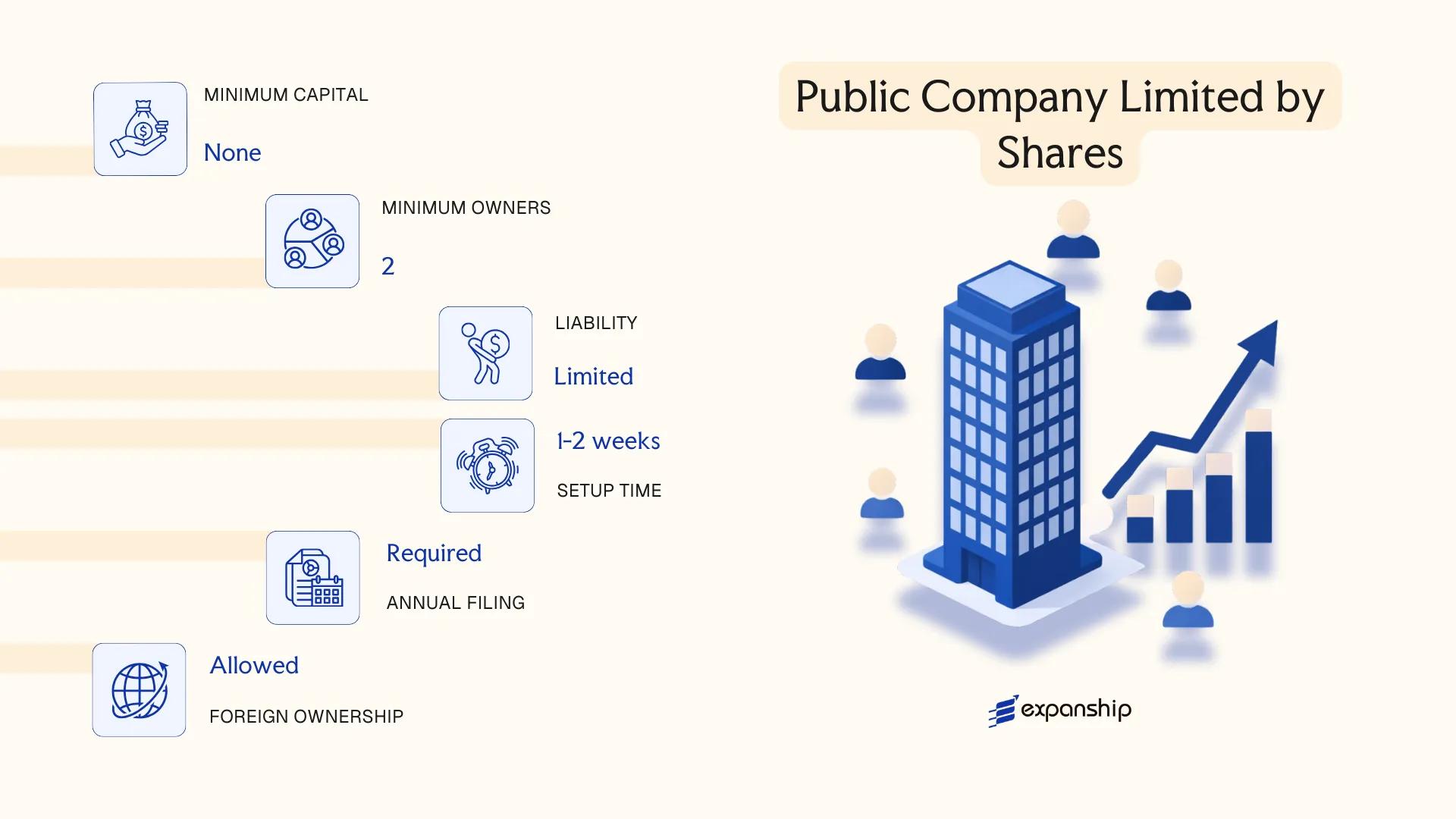

Public Company Limited by Shares in Grenada

A Grenada public company limited by shares is governed by the Companies Act, Cap. 82 of the Laws of Grenada, the same legislation that regulates private companies but with distinct structural and disclosure requirements. The entity holds separate legal personality, meaning shareholders bear liability only to the extent of their unpaid share capital.

Shares in a public company may be offered to the general public, which distinguishes its capital-raising capacity from that of a private firm. This structure suits businesses seeking broader investor participation or eventual listing on a recognised stock exchange.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Company Limited by Shares | Separate legal entity; liability limited to unpaid share capital |

| Members | Shareholders: minimum 7; no statutory maximum | Directors: minimum 3 required |

| Local Presence | Registered office address in Grenada required | Registered agent not mandated by statute but common in practice |

| Share Capital | No prescribed minimum; denominated in Eastern Caribbean Dollars (XCD) or foreign currency | Shares may be offered publicly; prospectus requirements apply |

| Privacy | Director and shareholder details filed with the Registrar of Companies | Public disclosure requirements are more extensive than for private companies |

Focus Points

- Taxation: Subject to corporate income tax; no capital gains tax; stamp duty applies to share transfers; VAT may apply depending on business activities.

- Annual Compliance: Annual returns and audited financial statements must be filed with the Registrar of Companies.

- Public Offering Obligations: Any public share offering requires a prospectus compliant with applicable securities regulations.

- Conversion: A public company may convert to a private company subject to shareholder approval and regulatory filing requirements.

- Restrictions: Cannot restrict share transferability in the same manner as a private company.

Closing Paragraph

A public company limited by shares is suited to large-scale commercial enterprises or businesses planning to raise capital from the public, though the associated disclosure obligations and administrative requirements are considerably more demanding than those of a private firm.

This structure fits established businesses with broad investor bases or those planning a future public offering — not early-stage or closely held operations.

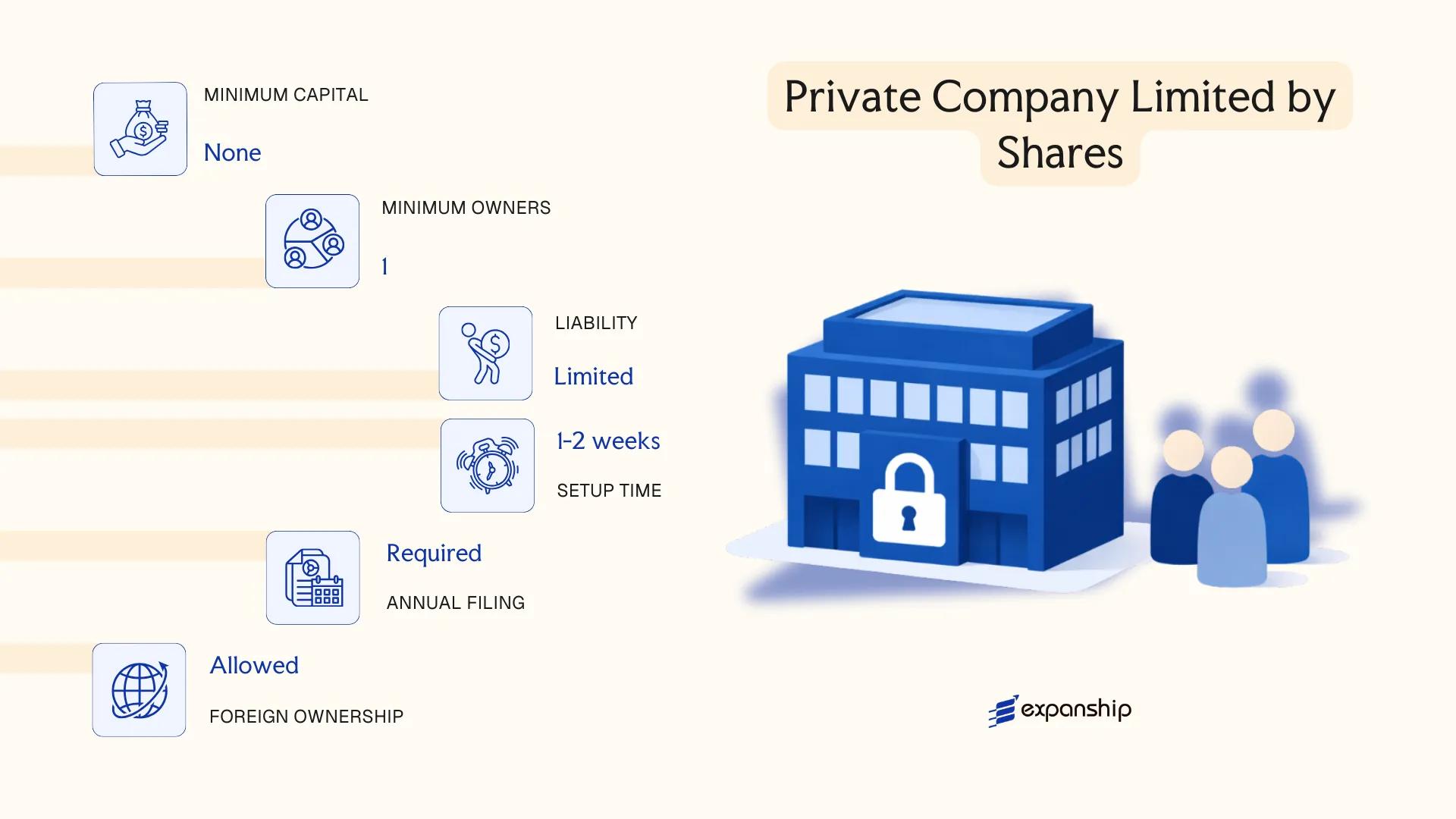

Private Company Limited by Shares in Grenada

A Grenada private company limited by shares is governed by the Companies Act, Cap. 22 of the Laws of Grenada, which establishes it as a separate legal entity distinct from its shareholders. Liability is confined to the amount unpaid on shares held, meaning personal assets of shareholders remain protected from company debts.

Incorporation requires the filing of Articles of Incorporation with the Grenada Companies Registry. The private designation restricts public share offers and imposes transfer restrictions on shares.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private Company Limited by Shares | Separate legal personality; shareholders not personally liable beyond share value |

| Members | Shareholders: 1–50 | Directors: minimum 1; no nationality restriction |

| Local Presence | Registered office address required in Grenada | Registered agent not mandated but common in practice |

| Capital | No statutory minimum share capital; denominated in Eastern Caribbean Dollars (XCD) | Shares must be fully described in Articles |

| Privacy | Director and shareholder names filed with Companies Registry | Register is accessible; limited confidentiality |

Focus Points

- Taxation: Subject to corporate income tax on locally sourced profits; VAT applies to taxable supplies; stamp duty applies on share transfers and certain instruments; no withholding tax on dividends under general domestic rules.

- Annual Compliance: Annual return and financial statements must be filed with the Companies Registry; failure attracts penalties.

- Economic Substance: Domestic-focused operations are not subject to the economic substance requirements applicable to IBCs under Grenada's substance legislation.

- Restrictions: Cannot offer shares to the public; share transfer requires compliance with restrictions set out in the Articles.

- Conversion: Can be re-registered as a public company subject to Companies Act provisions, provided statutory conditions are met.

Closing

This structure suits resident-owned trading businesses, local holding arrangements, and family-run operations that require limited liability without the compliance obligations of a public entity. One clear limitation is the shareholder cap of 50, which constrains equity expansion.

Resident entrepreneurs and small-to-medium businesses conducting commercial activity within Grenada who require limited liability and a straightforward corporate structure.

Partnerships in Grenada [General Partnership, Limited Partnership]

Partnership registration in Grenada is governed by the Partnership Act, Cap. 235 of the Laws of Grenada. A general partnership does not confer separate legal personality on the firm, meaning partners remain personally liable for the debts and obligations of the business.

A limited partnership offers a structural distinction: it combines at least one general partner bearing unlimited liability with one or more limited partners whose exposure is capped at their capital contribution. Registration is handled through the Grenada Companies Registry.

Key Characteristics

| Requirement | General Partnership | Limited Partnership |

|---|---|---|

| Legal Form | Unincorporated firm; no separate legal personality | Unincorporated; no separate legal personality |

| Partners | Minimum 2 general partners; no statutory maximum | Minimum 1 general partner + 1 limited partner |

| Liability | All partners: unlimited personal liability | General partner: unlimited; limited partner: capped at contribution |

| Local Presence | Registered office address in Grenada required | Registered office address in Grenada required |

| Capital | No prescribed minimum; contributions in any agreed form | No prescribed minimum; limited partner's contribution must be defined |

| Privacy | Partner names generally filed with the Registry | Partner names generally filed with the Registry |

Focus Points

- Taxation: Partnerships are generally treated as pass-through structures; profits are taxed at the partner level under personal or corporate income tax rates, with no separate entity-level corporate tax. VAT registration may apply if turnover thresholds are met.

- Annual Compliance: Annual renewal filings are required with the Companies Registry to maintain good standing.

- Treaty Access: Partnerships, lacking separate legal personality, may face limitations in accessing double tax treaty benefits available to corporate entities.

- Restrictions: Limited partners must not participate in the management of the firm; doing so risks losing their limited liability protection under the Partnership Act.

Sub-Types

General Partnership

All partners share management authority and carry unlimited personal liability. This structure is commonly used by professional service providers and small trading businesses where partners are actively involved in operations.

Limited Partnership

At least one general partner manages the firm and bears full liability, while limited partners contribute capital without taking part in management. This structure is often used for investment vehicles and project-specific arrangements where passive investors require defined liability exposure.

A partnership suits small commercial ventures or investment arrangements where two or more parties want a straightforward shared-ownership structure without the formalities of incorporation. The primary advantage is minimal setup complexity; the principal drawback is the unlimited personal liability that general partners carry.

Partnerships in Grenada are most appropriate for small domestic businesses or passive investment arrangements where partners are comfortable accepting defined liability roles under a relatively simple legal framework.

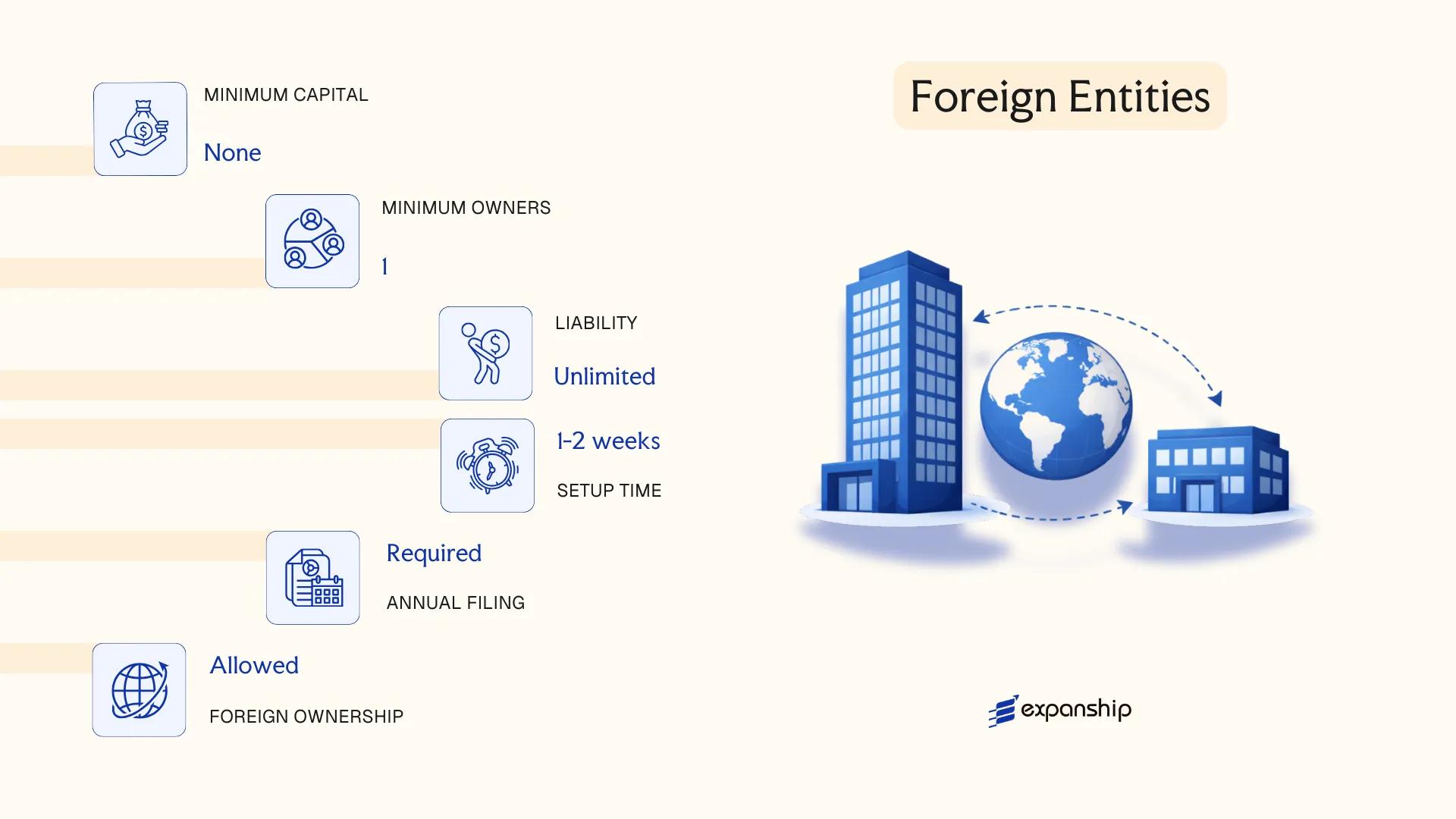

Foreign Entities in Grenada [Branch Office, Representative Office]

Foreign companies seeking a presence in Grenada without incorporating a new local entity have two primary options: registering a foreign company branch office Grenada or establishing a representative office. Both structures are governed by the Companies Act, Cap. 76 of the Laws of Grenada, which requires foreign entities to register with the Grenada Companies Registry before conducting any business activity on the island.

A branch is not a separate legal entity — it remains an extension of the parent company, which retains full liability for the branch's obligations. Registration requires filing certified copies of the parent company's constitutive documents, along with details of a local agent authorized to accept service of process.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Form | Extension of parent company; no separate legal personality | Extension of parent; no independent legal status |

| Liability | Parent company bears full liability | Parent company bears full liability |

| Local Presence | Registered agent and local address required | Registered agent and local address required |

| Permitted Activities | Full commercial and trading activities | Limited to promotional, liaison, or market research activities only |

| Capital Requirement | No minimum capital prescribed; parent's financials govern | None prescribed |

| Privacy | Parent company documents become part of public registry record | Parent company documents become part of public registry record |

Focus Points

- Taxation: Branch profits are subject to corporate income tax at the standard rate applicable to resident companies; withholding tax may apply to remittances to the parent depending on treaty status.

- Economic Substance: No dedicated economic substance regime applies to branches in the way it does to IBCs, but physical activity must correspond to declared operations.

- Annual Compliance: Annual returns and updated parent company documents must be filed with the Companies Registry to maintain active registration status.

- Treaty Access: Grenada's tax treaty network is limited; branches do not automatically benefit from treaty provisions unless the parent's jurisdiction has a relevant agreement in force.

- Restrictions: A representative office cannot generate revenue or enter into commercial contracts in its own right; any commercial activity requires conversion to a branch or locally incorporated entity.

Sub-Types

Branch Office

A branch conducts active business operations on behalf of the parent company and can enter contracts, generate revenue, and employ staff locally. It is typically used by foreign firms seeking a trading or service delivery presence without the administrative burden of incorporating a separate subsidiary.

Representative Office

A representative office is restricted to non-commercial functions such as market research, promotional activity, and liaison with local clients or government bodies. It cannot invoice clients or execute binding commercial agreements, making it suitable for foreign businesses in an exploratory or pre-market phase.

Closing

Registering a foreign entity in Grenada suits parent companies that require operational continuity across borders without establishing a standalone subsidiary, though the absence of liability separation between the branch and parent is a structural exposure that should be assessed against the business risk profile.

Foreign companies with existing operations seeking a direct commercial presence or a non-revenue market entry point in Grenada, rather than those requiring liability separation from local activity.

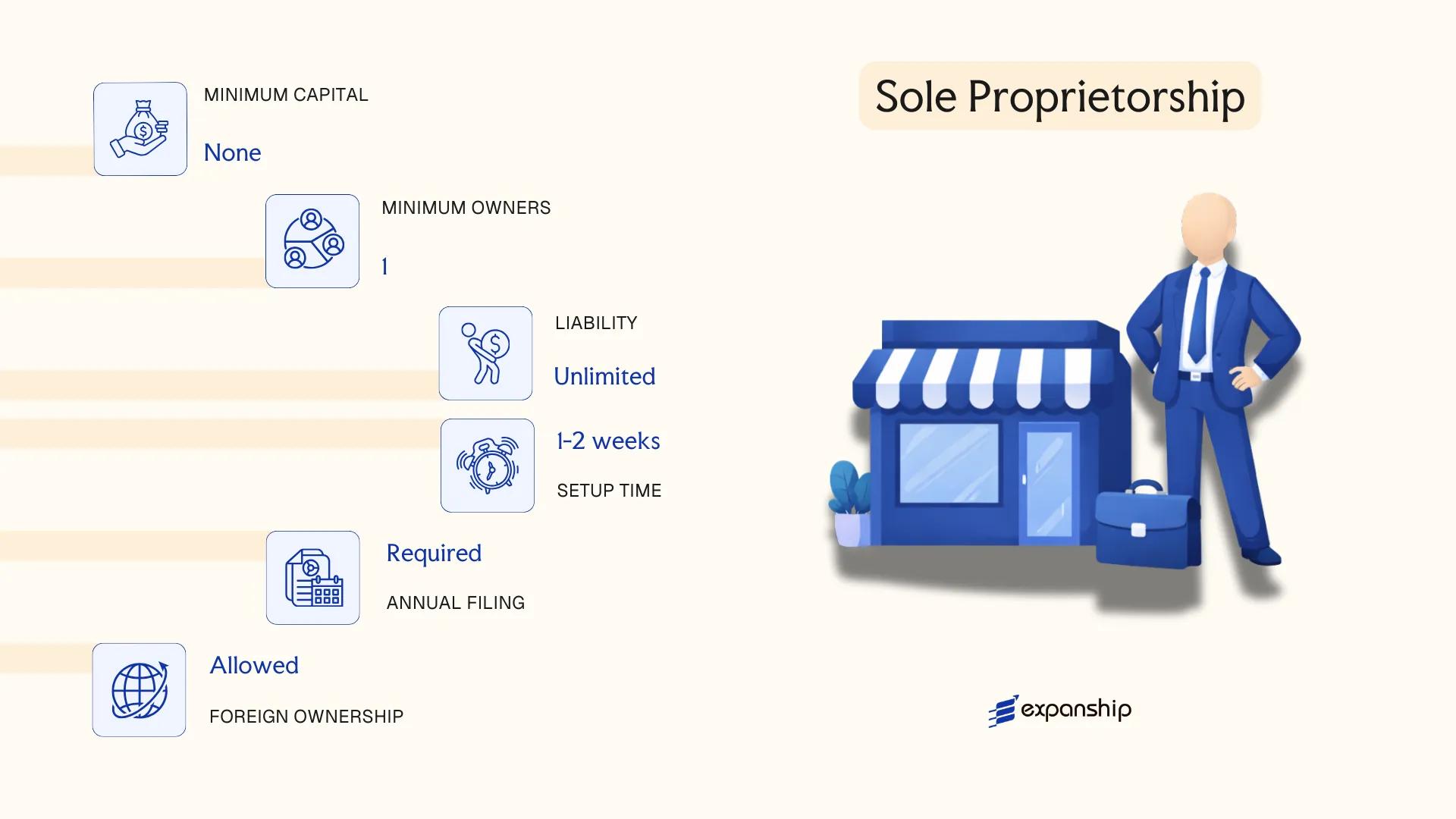

Sole Proprietorship in Grenada

Sole proprietorship registration Grenada falls under the general business registration framework governed by the Companies Act (Cap. 218) and the Registration of Business Names Act. Unlike incorporated entities, a sole proprietorship carries no separate legal personality — the owner and the business are legally the same person, meaning personal assets remain fully exposed to business liabilities.

Registration is handled through the Grenada Companies Registry. Before commencing operations, a sole trader must register the business name if trading under any name other than their own. This is a straightforward administrative process, though the absence of limited liability is a defining structural constraint.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated business | No separate legal personality from the owner |

| Owner Title | Sole Proprietor / Sole Trader | Single individual only; no co-owners |

| Membership | 1 individual (minimum and maximum) | Cannot have multiple owners without converting to a partnership or company |

| Local Presence | Registered business address required | No registered agent requirement, but a local address must be on file |

| Capital | No statutory minimum; Eastern Caribbean Dollar (XCD) | Owner's personal funds used directly |

| Privacy | Business name and owner details registered publicly | Limited privacy compared to incorporated structures |

Focus Points

- Taxation: Sole proprietors are taxed as individuals under personal income tax; no separate corporate tax applies, though VAT registration is required once turnover exceeds the statutory threshold.

- Annual Compliance: Business name registration must be renewed periodically with the Companies Registry; no annual return filing equivalent to incorporated entities.

- Economic Substance: No economic substance obligations apply to sole proprietorships, as these requirements target incorporated entities conducting specific business activities.

- Conversion: A sole proprietorship can be converted into a private company or partnership, but this requires a fresh incorporation process rather than a simple structural amendment.

- Restrictions: Foreign nationals face residency and work permit requirements before operating as a sole trader; this structure is generally accessible to citizens and permanent residents.

Closing Paragraph

A sole proprietorship suits local service providers, freelancers, and small traders who operate with minimal administrative overhead and do not require a formal corporate structure. The primary advantage is operational simplicity, while the complete absence of liability protection remains a significant structural drawback for any business carrying meaningful financial or legal risk.

This structure is best suited for Grenadian residents running low-risk, owner-operated businesses where simplicity outweighs the need for liability separation.

How to Choose the Right Entity Type in Grenada

Selecting the correct structure before incorporation is a decision with direct legal and financial consequences — understanding how to choose a business entity in Grenada requires mapping your operational reality against what each structure legally permits.

Why Your Entity Choice Matters

The structure you register determines what you can and cannot do under Grenadian law. Getting it wrong produces concrete, correctable-but-costly outcomes:

- Registering an International Business Company and then transacting with Grenadian residents places the entity in breach of the International Business Companies Act, which can result in the Registrar striking off the company.

- Choosing a tax-exempt entity when you require double taxation treaty access renders you ineligible to claim withholding tax reductions in treaty partner countries, as exempt entities are typically excluded from treaty benefits.

- Forming a private company limited by shares for estate planning or asset protection purposes subjects your arrangement to annual shareholder obligations, filing requirements, and potential succession complications that a trust structure would not carry.

- Selecting a structure with audited financial statement requirements for a single-director consultancy introduces recurring professional costs disproportionate to the business's scale and complexity.

Key Factors to Consider

- Business Activity: Whether your firm will trade actively, hold assets passively, or operate in a licensed sector such as insurance or banking determines which structures are legally available to you.

- Local vs. Offshore Operations: Entities restricted from local trading, such as IBCs, are unsuitable if your business intends to contract with Grenadian residents or operate domestically.

- Ownership and Management Structure: A single-owner business with no need for a formal board may find an LLC or sole proprietorship more administratively proportionate than a multi-director company structure.

- Tax Objectives: Your requirement for full tax exemption, access to a specific treaty network, or eligibility under the domestic corporate tax regime each point toward a different entity category.

- Privacy Requirements: Some structures expose directors and shareholders on the public register; others permit nominee arrangements that limit disclosure.

- Exit Strategy: If you anticipate redomiciliation, conversion, or winding up, confirm in advance whether the structure you select legally accommodates those procedures under Grenadian corporate law.

Corporate Compliance Services in Grenada

Maintain good standing with Grenada's Registry of Companies and meet your ongoing statutory obligations across all entity types.

Conclusion

Incorporating a company in Grenada involves selecting from a defined set of structures, each suited to a distinct operational profile. The IBC remains the default choice for non-resident entrepreneurs seeking tax-exempt holding or trading arrangements. Private companies limited by shares suit small-to-medium domestic or foreign-owned businesses requiring separate legal personality with controlled ownership. Public companies are reserved for larger ventures intending to raise capital from the public. LLCs offer a hybrid structure combining contractual flexibility with liability protection. General partnerships carry unlimited personal liability, while limited partnerships allow passive investors to cap their exposure. Branch offices and representative offices serve foreign entities testing or maintaining a local presence without forming a separate legal person. Sole proprietorships remain the simplest registration path for individual traders.

Registered under the Companies Act (Cap. 77) and overseen by the Grenada Companies and Intellectual Property Office, the private company limited by shares is the most commonly registered structure. The jurisdiction has been gradually expanding its bilateral investment treaty network, signaling a measured approach to strengthening its international standing for cross-border business registration. Professional guidance remains relevant when aligning your chosen structure with both local compliance obligations and the laws of your home jurisdiction.

How Expanship Can Assist You

Expanship company formation services Grenada cover the full range of entity types examined in this guide, from the International Business Company governed by the International Companies Act to domestic private limited companies registered with the Grenada Companies Registry. Your specific structure determines the compliance path ahead, and Expanship's corporate services in Grenada are built around those distinctions.

From initial registration through ongoing obligations, the firm handles the operational details so your business stays in good standing.

- Document preparation and notarization

- Registered agent and registered office provision

- Government filing and Grenada Companies Registry liaison

- Post-incorporation compliance management, including annual returns

- Banking introduction assistance for corporate accounts

For questions about your Grenada business setup, reach out directly through Expanship Grenada.

Frequently Asked Questions (FAQ)

The International Business Company (IBC) is the most frequently incorporated structure in Grenada. Its zero-tax treatment on foreign-sourced income and minimal reporting requirements make it the default choice for non-resident entrepreneurs.

An IBC is restricted from trading with Grenadian residents or owning local real estate, whereas a Private Company Limited by Shares can conduct business domestically. The latter carries annual filing obligations with the Registrar of Companies, while an IBC operates under a lighter compliance regime.

The IBC provides the greatest degree of confidentiality. Beneficial ownership details and shareholder registers are not publicly accessible, and nominee director and shareholder arrangements are permitted under the IBC Act.

A sole individual can register an IBC or a Private Company Limited by Shares, as both require a minimum of one shareholder and one director. Partnerships, by definition, require at least two partners, so a single person cannot form a General or Limited Partnership.

All entity types in Grenada are available to foreign nationals. IBCs are specifically structured for non-residents, but foreigners may equally register a Private Company, Public Company, LLC, or branch office without nationality-based restrictions.

Conversion between entity types is generally permitted under Grenada's corporate legislation, subject to Registrar approval and compliance with the relevant statutory requirements. A Private Company, for instance, may re-register as a Public Company if it meets the applicable conditions.

IBCs, Private and Public Companies, and LLCs each hold legal personality distinct from their members. General Partnerships do not possess separate legal personality, meaning partners bear direct liability for the firm's obligations.

The IBC carries the lightest compliance burden. There are no public financial disclosure requirements, no mandatory audit for most IBCs, and no local residency requirement for directors or officers.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.