Key Takeaways

- All UK business entities must be registered with Companies House and remain subject to ongoing compliance obligations under the Companies Act 2006.

- The Private Limited Company (Ltd) is the dominant incorporation choice in the United Kingdom, accounting for the large majority of new company registrations each year.

- An LLP provides liability protection suited to professional service firms without imposing the full governance formality of a corporate structure.

- Regulatory requirements around beneficial ownership are expanding under the Register of Overseas Entities and the Economic Crime Act, making forward-looking structure decisions increasingly important.

Introduction to Entity Types in United Kingdom

Located off the northwest coast of continental Europe, the United Kingdom is an independent sovereign nation comprising England, Scotland, Wales, and Northern Ireland. Company registration falls under the jurisdiction of Companies House, the statutory registrar operating under the Companies Act 2006. All incorporated entities must be registered with Companies House and file ongoing compliance documents through its systems.

The UK operates a residence-based corporate tax regime, with rates and reliefs set by HM Revenue & Customs (HMRC).

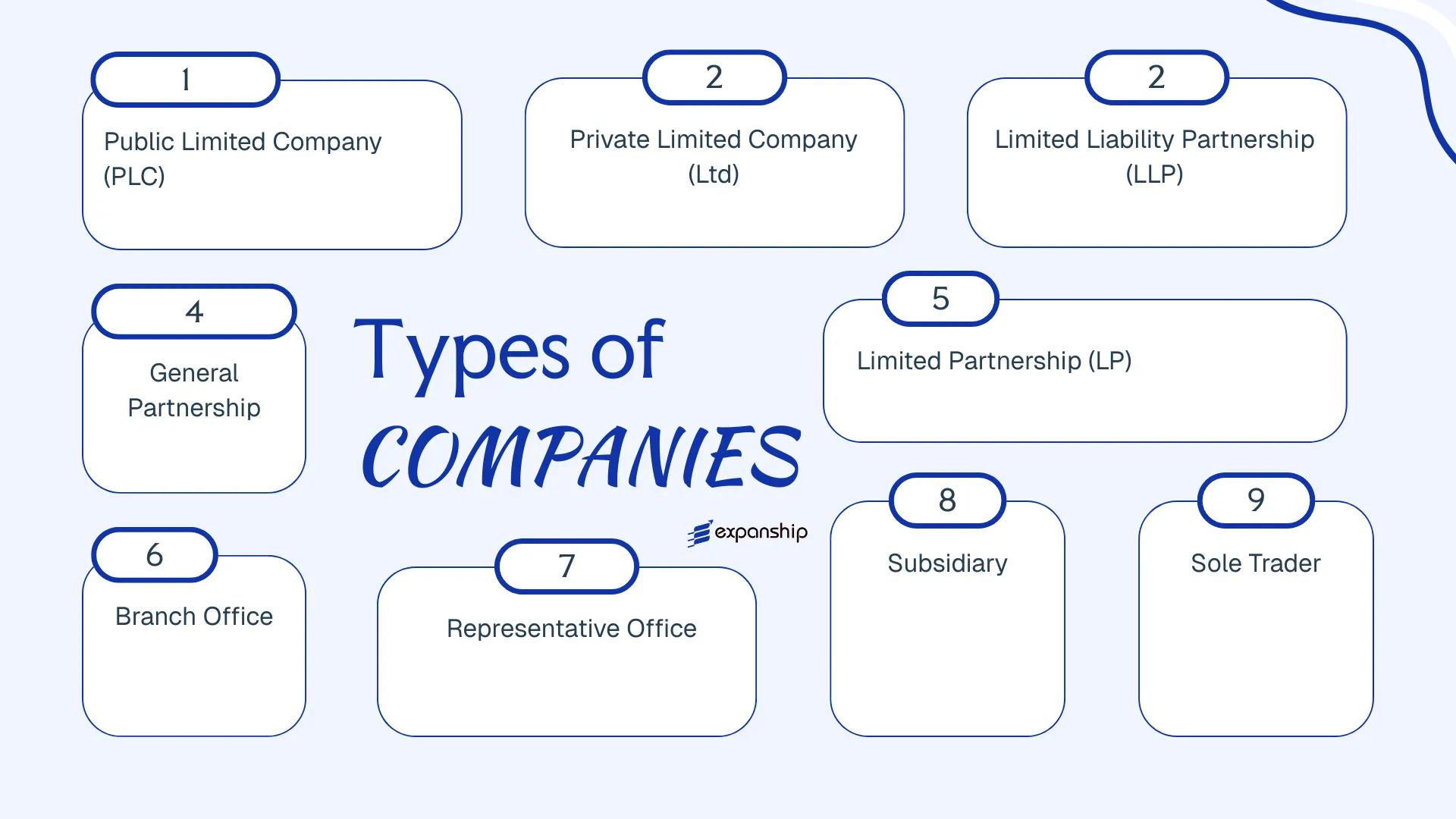

Several types of business entities in UK law are available to domestic and foreign founders alike. These include the Public Limited Company (PLC), Private Limited Company (Ltd), Limited Liability Partnership (LLP), General Partnership, Limited Partnership, Branch Office, Representative Office, Subsidiary, and Sole Trader. Each structure carries distinct legal standing, liability treatment, and regulatory obligations.

This article examines each of these UK company structures in detail — covering formation requirements, governance rules, and the circumstances under which each structure is typically used.

An Overview of Business Structures in United Kingdom

Governed primarily by the Companies Act 2006, the UK business structures comparison spans several distinct legal forms, each shaped by different liability, tax, and governance rules. The Act, alongside the Limited Liability Partnerships Act 2000 and the Partnership Act 1890, collectively defines the framework within which businesses operate. Each entity type serves a different commercial purpose, and the sections that follow examine them individually.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Tax Treatment | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Public Limited Company (PLC) | Incorporated body | Limited to shares | Corporation Tax | Permitted | 2 shareholders, 2 directors | Companies House | Companies Act 2006 |

| Private Limited Company (Ltd) | Incorporated body | Limited to shares | Corporation Tax | Permitted | 1 shareholder, 1 director | Companies House | Companies Act 2006 |

| Limited Liability Partnership (LLP) | Hybrid legal entity | Limited to contribution | Partner-level taxation | Permitted | 2 designated members | Companies House | LLP Act 2000 |

| General Partnership | Unincorporated | Unlimited, joint | Partner-level taxation | Permitted | 2 partners | HMRC registration | Partnership Act 1890 |

| Limited Partnership (LP) | Unincorporated | Mixed: general/limited | Partner-level taxation | Permitted | 1 general, 1 limited partner | Companies House | Limited Partnerships Act 1907 |

| Branch Office | Foreign extension | Parent bears liability | Corporation Tax on UK profits | Permitted | N/A | Companies House | Companies Act 2006 |

| Representative Office | Foreign presence | Parent bears liability | Generally non-taxable | Not permitted | N/A | HMRC / Companies House | No dedicated statute |

| Subsidiary | Separate incorporated body | Limited to shares | Corporation Tax | Permitted | 1 shareholder, 1 director | Companies House | Companies Act 2006 |

| Sole Trader | Unincorporated individual | Unlimited personal | Income Tax / NICs | Permitted | 1 person | HMRC registration | Self-Employment rules |

Each of these structures is examined in full in the sections below.

Public Limited Company (PLC)

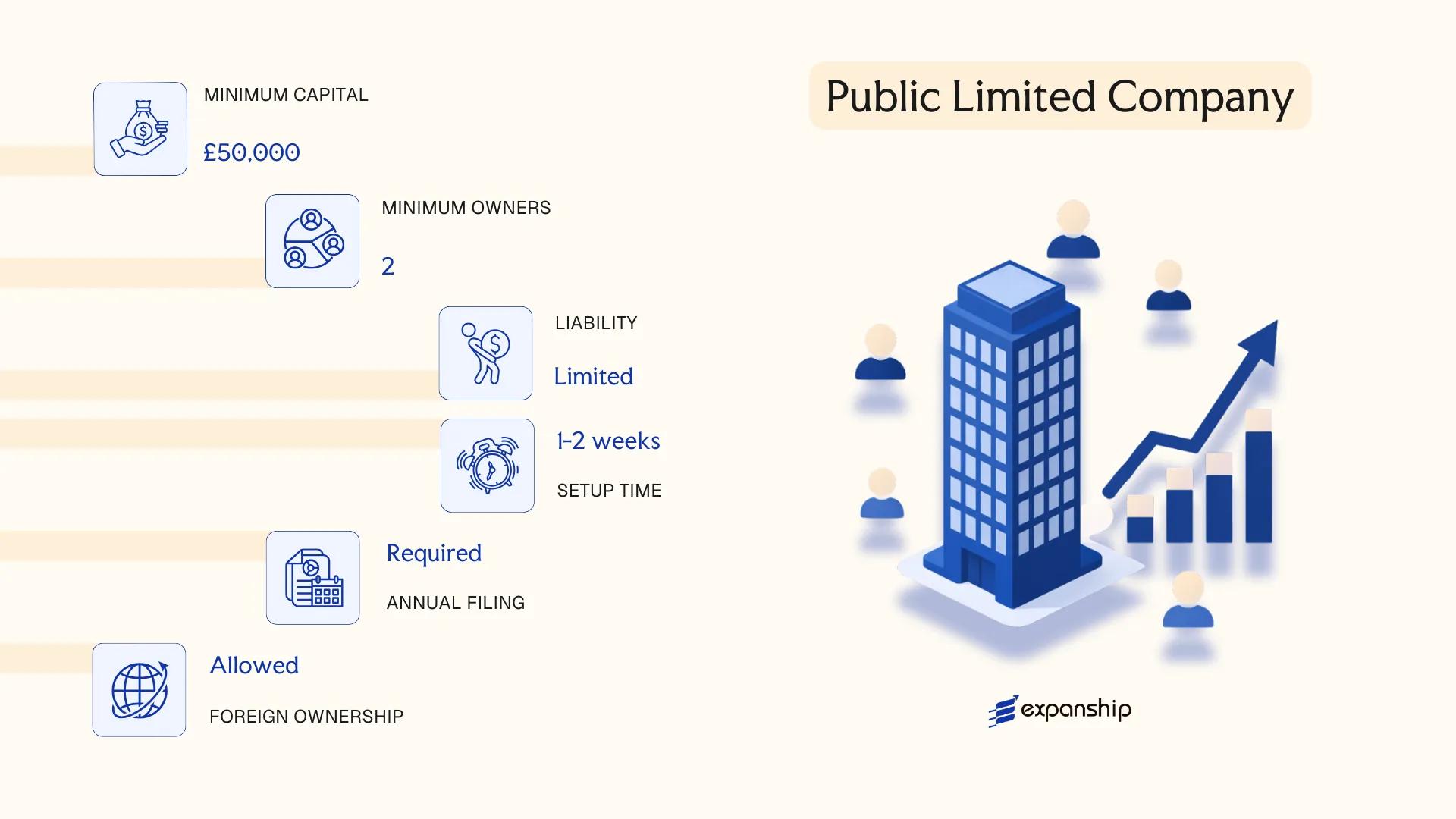

A Public Limited Company (PLC) in the UK is governed by the Companies Act 2006 and represents the only corporate structure permitted to offer shares to the general public. It carries separate legal personality, meaning the entity itself holds rights and obligations distinct from its shareholders.

Limited liability protection applies to all shareholders, capped at the value of their unpaid share capital. Listing on a recognised exchange such as the London Stock Exchange or AIM is optional — a PLC can remain unlisted while still retaining its public company status.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Limited Company (PLC) | Incorporated under Companies Act 2006 |

| Members | Shareholders (minimum 2); no maximum | At least 2 directors required; 1 must be a natural person |

| Local Presence | Registered office in England, Wales, Scotland, or Northern Ireland | Must be a physical address, not a PO box |

| Capital | Minimum allotted share capital of £50,000; at least 25% paid up before trading | Denominated in GBP or foreign currency |

| Privacy | Director and shareholder details on public record at Companies House | PSC (Person with Significant Control) register also publicly accessible |

| Company Secretary | Mandatory; must be qualified | LPs, chartered secretaries, or solicitors qualify |

Focus Points

- Taxation: Subject to UK Corporation Tax (currently 25% for profits above £250,000); VAT registration required if turnover exceeds the statutory threshold; dividends paid to non-residents may attract withholding tax under domestic law, reducible via applicable tax treaties; stamp duty applies on share transfers at 0.5%.

- Annual Compliance: Confirmation statement and annual accounts must be filed with Companies House; listed PLCs face additional FCA disclosure obligations.

- Treaty Access: UK's extensive double tax treaty network is accessible, subject to meeting beneficial ownership and substance conditions.

- Conversion: A PLC can be re-registered as a private limited company under Companies Act 2006, s.97, provided shareholder approval and Companies House requirements are met.

- Restrictions: Cannot commence trading or exercise borrowing powers until Companies House issues a trading certificate confirming minimum capital compliance.

Closing

A PLC suits businesses seeking public capital raises, institutional investment, or a listing on a regulated or exchange-regulated market. The structure offers unmatched access to equity markets, though the associated compliance burden — including mandatory audits, a qualified company secretary, and FCA obligations for listed entities — makes it disproportionate for most private ventures.

PLCs are most appropriate for established businesses pursuing public fundraising, a stock market listing, or a corporate profile that demands publicly verifiable capital adequacy.

Company Incorporation in the United Kingdom

Incorporate a UK entity with full compliance support across all major structure types.

Private Limited Company (Ltd)

Private Limited Company (Ltd)

The private limited company (Ltd) is the most widely used corporate structure in the UK, governed by the Companies Act 2006. As a separate legal entity, it can own assets, enter contracts, and incur liabilities in its own name, distinct from its shareholders. Liability is limited to the amount unpaid on shares held.

Registered and regulated through Companies House, the firm must maintain a registered office address in England and Wales, Scotland, or Northern Ireland, consistent with its place of incorporation. UK Ltd company registration is handled entirely through Companies House, either directly or via a formation agent.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private Limited Company by shares (most common) or by guarantee | By-guarantee variant is typically used for non-profits |

| Members | Shareholders: minimum 1, no maximum; Directors: minimum 1 (must be a natural person) | A corporate entity may serve as shareholder; a sole individual can hold both roles |

| Local Presence | Registered office address required in the jurisdiction of incorporation | A PO Box alone is not sufficient; a physical address is required |

| Share Capital | No minimum share capital in GBP; £1 nominal value per share is common | Shares must be fully paid or partly paid at issuance |

| Privacy | Director names and registered office are publicly listed on Companies House | A service address may be used to keep residential addresses private |

| Company Secretary | Optional for private companies since the Companies Act 2006 | If appointed, details are filed at Companies House |

Focus Points

- Taxation: Subject to Corporation Tax (currently 19–25% depending on profits), VAT registration required if taxable turnover exceeds £90,000, and withholding tax may apply to certain payments such as royalties and interest to non-residents.

- Annual Compliance: Must file annual Confirmation Statements and statutory accounts with Companies House; filing deadlines vary based on accounting reference date.

- Economic Substance: No formal economic substance regime equivalent to offshore jurisdictions, but HMRC assesses tax residency based on central management and control.

- Treaty Access: UK-resident companies have access to the UK's extensive double tax treaty network, subject to beneficial ownership and anti-avoidance provisions.

- Conversion: An Ltd can re-register as a Public Limited Company (PLC) under the Companies Act 2006, provided it meets the relevant share capital and compliance thresholds.

An Ltd structure suits trading businesses, group holding arrangements, and IP holding, offering clear liability separation and access to treaty benefits. One limitation is the public disclosure requirement — director names and financial accounts are visible on the Companies House register.

A private limited company is best suited for small to mid-sized businesses, foreign investors establishing a UK trading or holding entity, and entrepreneurs seeking a straightforward, credible corporate structure with limited personal liability.

Limited Liability Partnership (LLP)

A Limited Liability Partnership LLP UK is governed by the Limited Liability Partnerships Act 2000, which established it as a body corporate with a legal personality separate from its members. This hybrid structure combines the internal flexibility of a traditional partnership with the liability protection associated with a limited company.

Registration is handled through Companies House, and the entity must maintain a registered office address in England and Wales, Scotland, or Northern Ireland, depending on where it incorporates. At least two designated members must be appointed; they carry specific statutory duties, including filing annual confirmation statements and accounts.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Body corporate | Separate legal personality under the LLP Act 2000 |

| Members | Referred to as "members"; minimum 2, no statutory maximum | At least 2 must be designated members |

| Local Presence | Registered office in the jurisdiction of incorporation | Must be a physical address, not a PO box |

| Capital | No minimum capital requirement; denominated in GBP | Members contribute capital per the LLP agreement |

| Privacy | Members' names filed publicly at Companies House | LLP agreement itself is not filed publicly |

Focus Points

- Taxation: The LLP is tax-transparent; members are taxed individually on their profit share via Self Assessment, no corporate tax at entity level, VAT registration required above the £90,000 threshold, and stamp duty land tax applies on property transactions.

- Annual Compliance: Must file a confirmation statement and annual accounts with Companies House; accounts are publicly accessible.

- Economic Substance: No specific economic substance regime applies to domestic LLPs, though genuine commercial activity is expected.

- Treaty Access: As a tax-transparent entity, the LLP itself generally does not access double tax treaties; treaty benefits flow to members based on their own residency.

- Conversion: An LLP can be converted to a limited company, though the process involves legal restructuring and potential tax implications that require professional advice.

Closing

The LLP suits professional services firms, joint ventures, and fund structures where pass-through taxation and operational flexibility are priorities, though its public disclosure requirements and the personal tax exposure of members can be limiting for certain commercial arrangements.

LLPs are most appropriate for professional practices (law, accountancy, consulting) and multi-party joint ventures where partners want liability protection without corporate-level taxation.

Partnerships [General Partnership, Limited Partnership]

Under the Partnership Act 1890, a general and limited partnership UK structure does not carry separate legal personality — partners remain personally liable for the firm's obligations. Limited partnerships are governed separately by the Limited Partnerships Act 1907, which introduced a tiered liability model: at least one general partner bears unlimited liability while limited partners are liable only to the extent of their capital contribution.

Registration requirements differ between the two forms. General partnerships require no formal registration with Companies House, though a partnership agreement is strongly advisable. Limited partnerships must register with Companies House before conducting business.

Key Characteristics

| Requirement | General Partnership | Limited Partnership |

|---|---|---|

| Legal Form | Unincorporated; no separate legal personality | Unincorporated; no separate legal personality |

| Partners | Two or more partners (no maximum) | Minimum one general partner, one limited partner |

| Liability | Unlimited for all partners | Unlimited for general partners; capped for limited partners |

| Registration | Not required; no Companies House filing | Mandatory registration with Companies House |

| Registered Office | UK address required if operating in UK | UK address required |

| Capital | No minimum; contributed per agreement | Limited partners' liability capped to contributed capital |

Focus Points

- Taxation: Partnerships are fiscally transparent; each partner reports their share of profits under self-assessment and pays Income Tax or Corporation Tax accordingly — no entity-level tax applies. VAT registration is required if taxable turnover exceeds the current threshold.

- Annual Compliance: General partnerships have no statutory filing obligations; limited partnerships must maintain their Companies House registration and notify changes to partners or contributions.

- Treaty Access: As non-corporate entities, partnerships generally cannot independently access double tax treaty benefits — treaty eligibility falls to the individual partners based on their own residence.

- Conversion: A partnership cannot convert directly into a limited company without dissolution and re-registration.

Sub-Types

General Partnership

All partners share management responsibilities and carry joint and several liability for business debts under the Partnership Act 1890. This structure is most commonly used by professional practices operating with mutual trust between a small group.

Limited Partnership

Introduced under the 1907 Act, this structure separates passive investors (limited partners) from active managers (general partners). It is frequently used for private equity and investment fund structures where investor liability protection is a priority.

Scottish Limited Partnership (SLP)

Formed under Scots law, an SLP does possess separate legal personality — a distinction from its English counterpart. This characteristic has historically made SLPs attractive for certain fund and holding structures, though increased scrutiny under anti-money laundering regulations has tightened their use.

Recommendations

Partnerships suit professional services firms, joint ventures, and investment fund vehicles where pass-through taxation and structural flexibility outweigh the drawbacks of unlimited liability exposure for general partners. The absence of corporate-level tax is a genuine advantage, but the lack of liability protection for general partners remains a material risk for trading activities.

Partnerships are most appropriate for professional services practices, co-investment arrangements, or fund structures where partners are comfortable managing liability through contractual agreements rather than statutory protection.

Foreign Presence [Branch Office, Representative Office, Subsidiary]

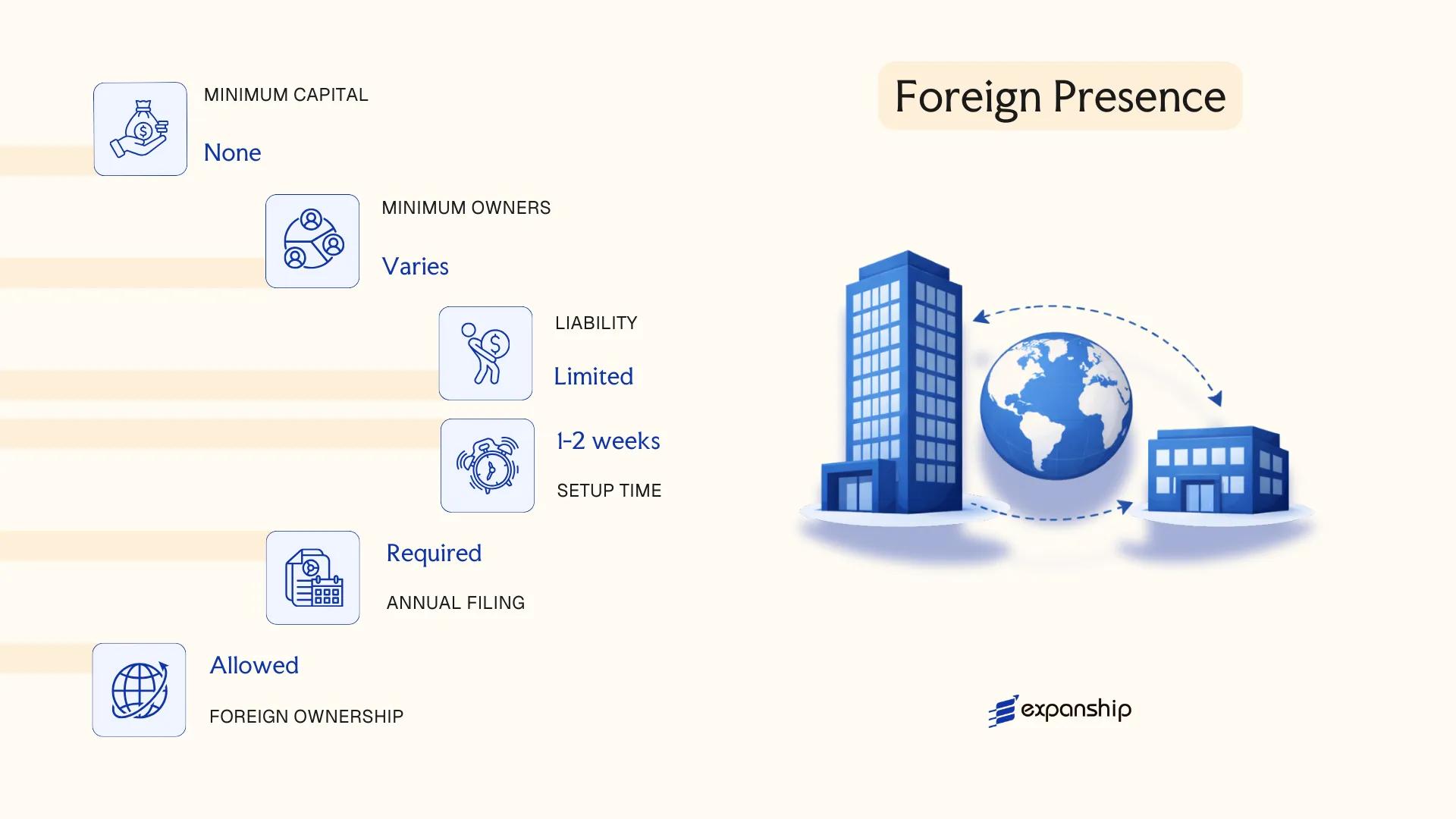

Foreign companies entering the UK market can establish a presence through three principal structures: a registered branch, a representative office, or a locally incorporated subsidiary. A foreign company branch office UK registration is governed by the Overseas Companies Regulations 2009, which requires any overseas company with a physical place of business in the UK to register with Companies House within one month of establishing that presence.

A subsidiary, by contrast, is a separately incorporated entity — typically a private limited company — and is therefore subject to the Companies Act 2006 rather than the overseas company regulations. The parent entity's liability exposure differs materially between the two structures.

Key Characteristics

| Requirement | Branch Office | Representative Office | Subsidiary (Ltd) |

|---|---|---|---|

| Legal Form | Extension of overseas parent; no separate legal personality | Informal presence; no separate legal personality | Separate legal entity incorporated under Companies Act 2006 |

| Governing Instrument | Overseas Companies Regulations 2009 | No statutory framework; self-regulated | Companies Act 2006 |

| Local Representative | Authorised UK-resident agent required | No statutory requirement | At least one director (no residency requirement) |

| Registered Office | Required UK address filed with Companies House | Not required | Required UK address |

| Share Capital | None (extension of parent) | None | No minimum; typically £1 |

| Privacy | Parent accounts must be publicly filed | Minimal public disclosure | Accounts filed at Companies House; small company exemptions may apply |

Focus Points

- Taxation: A branch is taxed on UK-source profits under Corporation Tax (currently 25% for profits over £250,000); a subsidiary is taxed as a standalone UK company; a representative office conducting no trading activity generally falls outside Corporation Tax scope. VAT registration applies to all structures once the £90,000 turnover threshold is met.

- Economic Substance: Branches must demonstrate genuine UK operational activity; HMRC scrutinises arrangements where profits are artificially shifted to or from the parent.

- Annual Compliance: Branches must file the parent's audited accounts and an annual return with Companies House; subsidiaries file their own accounts and confirmation statement independently.

- Treaty Access: Subsidiaries as UK tax residents can access the UK's double tax treaty network; branches may access treaties depending on the parent's jurisdiction and the specific treaty provisions.

- Conversion: There is no formal statutory conversion mechanism between a branch and a subsidiary — transitioning between structures requires establishing the new entity separately and transferring operations.

Sub-Types

Registered Branch

A registered branch has full trading capacity in the UK and must publicly disclose the parent company's financials through Companies House. This structure suits overseas firms that want direct operational control without creating a separate legal entity.

Representative Office

No statutory registration requirement applies to a representative office, and it is restricted to promotional, liaison, or market research activities — it cannot conclude contracts or generate revenue in the UK. This makes it suited only to early-stage market exploration.

A branch or representative office suits overseas firms testing the UK market or maintaining a light operational footprint, while a subsidiary is more appropriate for long-term trading, holding IP, or accessing the UK's treaty network as a resident entity. The key limitation of a branch is the public exposure of the parent company's full financial statements.

A UK subsidiary is best suited to foreign groups seeking legal separation from the parent, full treaty access, and the flexibility to bring in local shareholders or investors.

Sole Trader

Sole trader registration in the United Kingdom is governed not by a single incorporation statute but by registration requirements set out through HMRC, the UK's tax authority. Unlike a limited company, a sole trader has no separate legal personality — you and the business are a single legal entity, meaning personal assets are fully exposed to business liabilities.

Registration involves notifying HMRC that you are self-employed, typically through the Government Gateway portal, by 5 October of the second tax year in which you begin trading. There is no Companies House filing, no memorandum of association, and no share capital requirement.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated sole proprietorship | No separate legal personality from the owner |

| Proprietor | Sole trader / proprietor | One individual only; no partners or shareholders |

| Local Presence | No registered office required | A correspondence address for HMRC is sufficient |

| Capital | No minimum capital | No formal capital structure exists |

| Privacy | Name and address submitted to HMRC only | No public register entry unless trading under a business name |

Focus Points

- Taxation: Subject to Income Tax (20%–45%) on profits via Self Assessment; Class 2 and Class 4 National Insurance contributions apply; VAT registration mandatory once turnover exceeds the current threshold (£90,000 as of 2024–25); no corporate tax applies.

- Annual Compliance: Must file a Self Assessment tax return (SA100/SA103) with HMRC annually by 31 January for online submissions.

- Conversion: Can convert to a private limited company at any point; business assets and goodwill are transferred, with potential Capital Gains Tax implications.

- Restrictions: Cannot raise equity investment; no ability to issue shares or bring in shareholders.

- Treaty Access: As an unincorporated individual, access to UK double tax treaties is through personal residency status, not an entity-level claim.

Closing

A sole trader structure suits freelancers, consultants, and early-stage operators with low liability exposure who prioritise administrative simplicity over structural protection. The primary constraint is unlimited personal liability, which makes the structure unsuitable once business risk or turnover grows materially.

Individuals testing a business concept or operating low-risk, service-based activities with minimal overhead and no immediate plans to raise external capital.

How to Choose the Right Entity Type in United Kingdom

Selecting how to choose business structure UK is not a administrative formality — the structure you register shapes your tax position, liability exposure, and compliance obligations from day one.

Why Your Entity Choice Matters

The structure registered at Companies House follows your business through every filing cycle, funding round, and contractual relationship. Choosing the wrong one carries concrete consequences:

- Incorporating a private limited company when your activity requires FCA authorisation — and failing to obtain it — constitutes a criminal offence under the Financial Services and Markets Act 2000, carrying unlimited fines or imprisonment.

- Selecting a General Partnership when limited liability is required means each partner bears full personal liability for business debts, with no statutory cap.

- Registering a branch of a foreign company rather than a UK subsidiary means the parent entity remains directly exposed to UK liabilities generated by that branch.

- Forming a limited company for a single-person consultancy triggers mandatory annual accounts, Confirmation Statement filings, and Corporation Tax returns — obligations that do not apply to a Sole Trader registration.

Key Factors to Consider

- Business Activity: Active trading, passive asset-holding, and regulated activities (financial services, credit broking) each point toward distinct structures under UK law.

- Liability Exposure: If personal asset protection is a priority, structures registered under the Companies Act 2006 provide statutory limited liability; partnerships and sole trader arrangements do not.

- Ownership and Management: Multi-party ownership with flexible profit-sharing arrangements suits an LLP, whereas a company structure is required if you intend to issue share classes or raise equity investment.

- Tax Objectives: Corporation Tax applies to companies and LLPs differently from Income Tax on sole traders; your anticipated profit level and extraction strategy should drive this decision.

- Privacy Requirements: Directors and persons with significant control are listed on the public Companies House register; nominee arrangements are permissible but subject to transparency legislation.

- Exit Strategy: Not all UK structures permit redomiciliation or conversion — verify whether your chosen form allows a solvent members' voluntary liquidation or cross-border merger before incorporating.

Compliance Services for Companies in the United Kingdom

Maintain good standing with Companies House and HMRC through structured compliance support covering annual filings, confirmation statements, and statutory record-keeping.

Conclusion

Selecting the right structure is the first substantive decision in any UK company formation summary guide. Each entity type registered at Companies House carries distinct implications for liability, governance, and tax treatment. The Private Limited Company remains by far the most commonly incorporated structure in the UK, accounting for the large majority of new registrations each year. Sole traders suit individual operators with straightforward operations; general and limited partnerships serve specific collaborative arrangements; an LLP fits professional service firms that require liability protection without corporate formality. A PLC applies where public capital-raising is the objective.

Regulatory expectations continue to tighten, particularly around beneficial ownership disclosure under the Register of Overseas Entities and expanded Economic Crime Act obligations. Your structure choice should account for where these requirements are heading, not only where they currently stand.

How Expanship Can Assist You

Expanship's UK company incorporation services cover the full range of entities discussed in this blog — from Private Limited Companies registered with Companies House to Limited Liability Partnerships and foreign branch registrations. Your specific structure determines the filing requirements, and Expanship's team works with those details directly, not around them.

From the point of deciding on a structure, Expanship handles the administrative and legal groundwork on your behalf:

- Preparation and legalization of incorporation documents

- Registered office and agent provision in the UK

- Filing with Companies House and related government liaison

- Post-incorporation compliance management, including confirmation statements and annual accounts

- Banking introduction assistance for newly incorporated entities

Our corporate services in the United Kingdom extend through the full lifecycle of your business, not just the formation stage.

To discuss your UK business setup, contact Expanship UK directly.

Frequently Asked Questions (FAQ)

The Private Limited Company (Ltd) is by far the most frequently incorporated entity, registered through Companies House under the Companies Act 2006. Its combination of limited liability, single-shareholder eligibility, and relatively straightforward annual compliance makes it the default choice for most trading businesses and startups.

A branch is a direct extension of the foreign parent and carries no separate legal personality, meaning the parent bears full liability for its UK obligations. A Private Limited Company is a distinct legal entity, subject to UK corporation tax on its own profits. Compliance obligations also differ: branches must file the parent's accounts at Companies House alongside their own UK financials.

The Limited Liability Partnership provides comparatively more discretion than a Ltd, as members' profit shares are not publicly disclosed in the same granular way as director remuneration. That said, members' names remain on the public register at Companies House. Nominee member arrangements are legally permissible under general agency principles, though the beneficial ownership register under the Persons with Significant Control regime still applies.

A sole trader and a Private Limited Company can each be established by one person. General Partnerships and Limited Partnerships require a minimum of two partners by definition. An LLP also requires at least two designated members under the Limited Liability Partnerships Act 2000.

Non-residents can incorporate a Private Limited Company, form an LLP, register a branch, or trade as a sole trader without requiring prior UK residency or citizenship. There is no nationality restriction under the Companies Act 2006, though a registered UK address for the entity is mandatory. Directors of a Ltd must provide a service address, but need not be physically based in Britain.

A Private Limited Company can be re-registered as a Public Limited Company under Part 20 of the Companies Act 2006, and the reverse conversion is also permitted in defined circumstances. Converting a Ltd into an LLP is possible through a members' voluntary arrangement, though this involves dissolution and fresh incorporation rather than a direct statutory conversion. Partnerships cannot simply re-register as limited companies without winding down and forming a new entity.

No. A General Partnership has no separate legal personality under English law, meaning partners are personally liable for the firm's debts. A Private Limited Company, LLP, and Public Limited Company each hold distinct legal personality and can contract, hold assets, and litigate in their own name. A sole trader similarly has no separation between personal and business legal identity.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.