Key Takeaways

- Egypt's primary corporate legislation, Companies Law No. 159 of 1981, governs the key business structures available to investors, including the Joint Stock Company, the Limited Liability Company, and the One-Person Company.

- The Limited Liability Company is the most commonly registered entity for small to mid-sized foreign investment due to its comparatively straightforward setup requirements.

- Foreign companies can enter the Egyptian market without full incorporation by establishing a Branch Office or Representative Office, both of which fall under GAFI oversight.

- Registration and compliance for all commercial entities in Egypt is administered by the General Authority for Investment and Free Zones (GAFI), which has continued to digitize its incorporation procedures.

Introduction to Entity Types in Egypt

Egypt sits in northeastern Africa, bordered by Libya, Sudan, and Israel, with coastlines along both the Mediterranean Sea and the Red Sea. It is an independent republic, and the registration of commercial entities falls under the oversight of the General Authority for Investment and Free Zones (GAFI), the body responsible for processing incorporations and maintaining the commercial register.

The country operates a territorial tax system, with corporate income tax applied to profits earned within its borders, alongside a network of double taxation treaties.

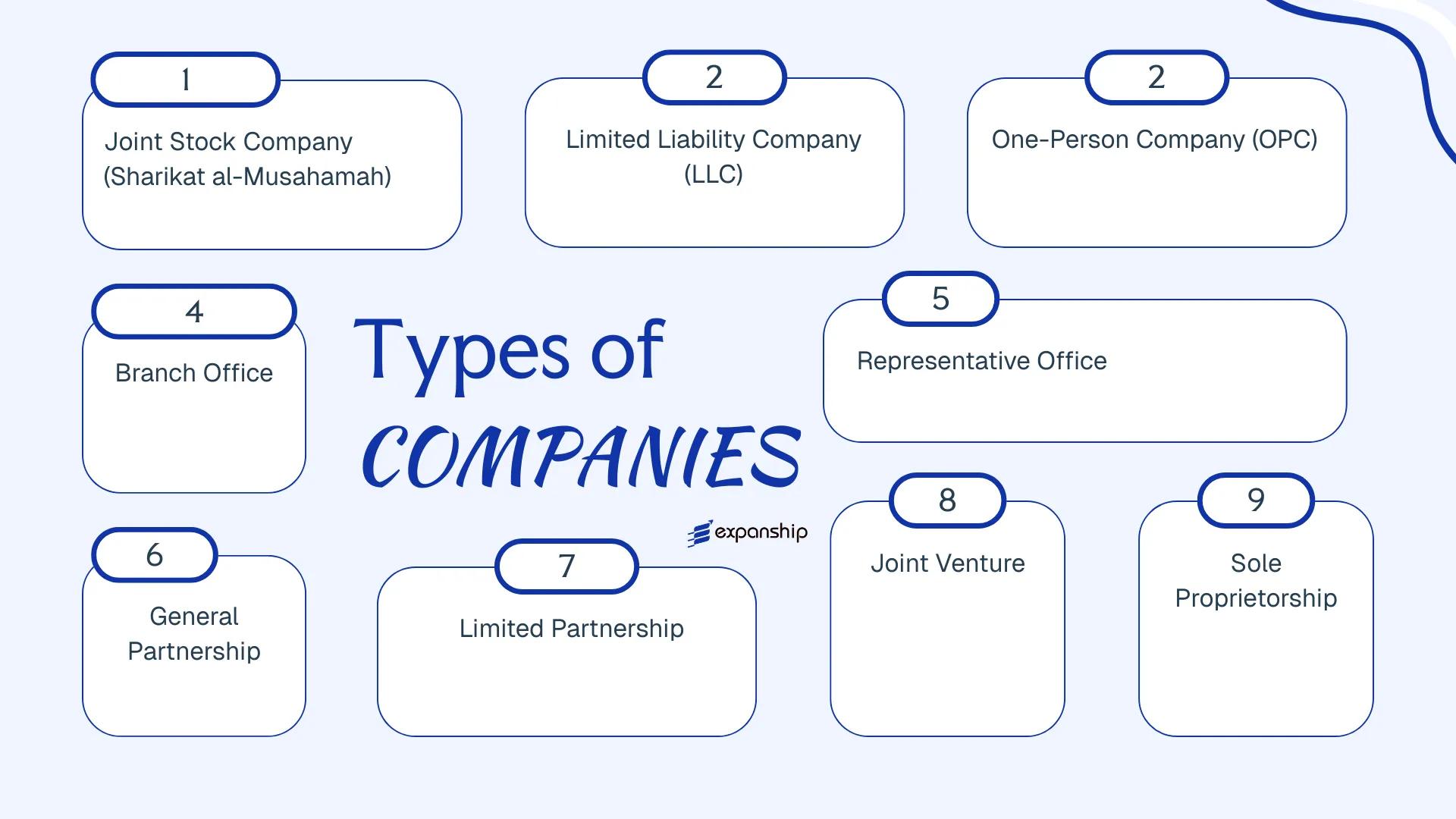

Several legal entity structures are available to investors and operators under Egyptian law, primarily governed by Companies Law No. 159 of 1981 and its subsequent amendments. These include the Joint Stock Company, the Limited Liability Company, the One-Person Company, the Branch Office, the Representative Office, the General Partnership, the Limited Partnership, the Joint Venture, and the Sole Proprietorship.

Each structure carries distinct requirements around capital, liability, governance, and foreign ownership. This article examines each option in detail so your business can assess which structure aligns with its operational and legal requirements.

An Overview of Business Structures in Egypt

Under Egyptian law, several distinct entity types are available to businesses operating within the country. The principal legislation governing business formation is Companies Law No. 159 of 1981, supplemented by Investment Law No. 72 of 2017 and regulated through the General Authority for Investment and Free Zones (GAFI). Each structure carries different implications for liability, ownership, taxation, and permitted activities.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Joint Stock Company (JSC) | Corporate entity | Limited to shares | Taxable | Permitted | 3 shareholders | GAFI / MCDR | Law No. 159 of 1981 |

| Limited Liability Company (LLC) | Corporate entity | Limited to capital | Taxable | Permitted | 2 shareholders | GAFI | Law No. 159 of 1981 |

| One-Person Company (OPC) | Corporate entity | Limited to capital | Taxable | Permitted | 1 shareholder | GAFI | Law No. 159 of 1981 |

| Branch Office | Extension of parent | Parent bears liability | Taxable on local income | Permitted | N/A | GAFI | Law No. 159 of 1981 |

| Representative Office | Non-trading presence | Parent bears liability | Generally exempt | Not permitted | N/A | GAFI | Law No. 159 of 1981 |

| General Partnership | Unincorporated firm | Unlimited, joint | Taxable | Permitted | 2 partners | Commercial Registry | Commercial Law No. 17 of 1999 |

| Limited Partnership | Unincorporated firm | Mixed liability | Taxable | Permitted | 2 partners | Commercial Registry | Commercial Law No. 17 of 1999 |

| Joint Venture | Contractual arrangement | Per agreement | Taxable | Permitted | 2 parties | No specific authority | Commercial Law No. 17 of 1999 |

| Sole Proprietorship | Individual business | Unlimited, personal | Taxable | Permitted | 1 individual | Commercial Registry | Commercial Law No. 17 of 1999 |

Each of these structures is examined in full in the sections below.

Joint Stock Company (Sharikat al-Musahamah) under the Egyptian Companies Law No. 159 of 1981

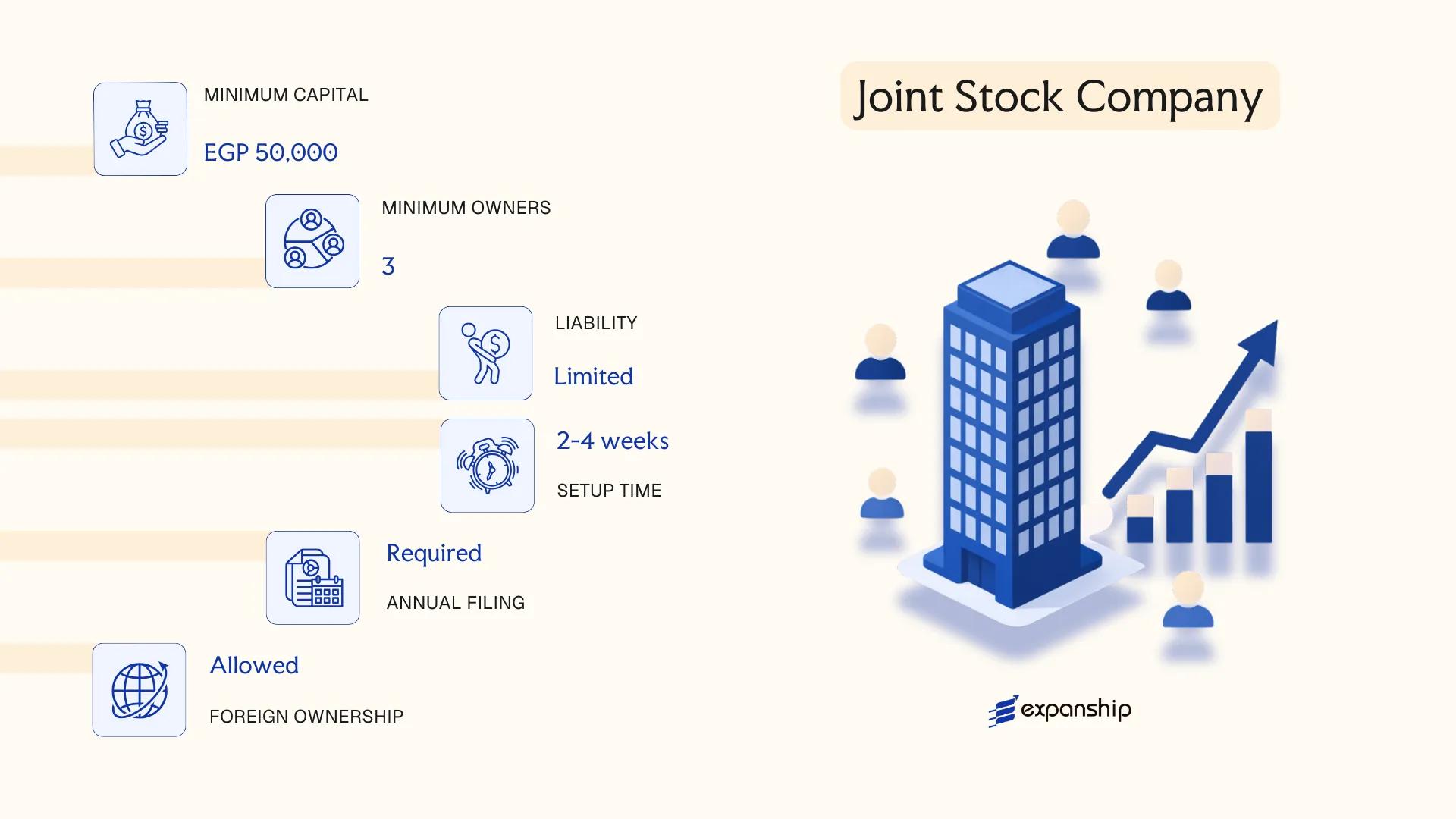

Governed by the joint stock company Egypt Companies Law 159 of 1981, the Joint Stock Company — locally designated as Sharikat al-Musahamah and abbreviated as S.A.E. (Société Anonyme Égyptienne) — is the primary vehicle for large-scale commercial activity and public capital formation. It carries separate legal personality, meaning the entity exists independently of its shareholders and can own assets, incur liabilities, and enter contracts in its own name.

Liability is strictly limited to each shareholder's subscribed capital contribution. The General Authority for Investment and Free Zones (GAFI) oversees Sharikat al-Musahamah Egypt registration, and certain regulated sectors may require additional approvals from sector-specific authorities.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Joint Stock Company (S.A.E.) | Governed by Companies Law No. 159 of 1981 and its executive regulations |

| Members | Shareholders | Minimum 3 shareholders; no statutory maximum; natural or legal persons permitted |

| Governing Body | Board of Directors | Minimum 3 directors; majority must attend board meetings; a Chairman is required |

| Local Presence | Registered office in Egypt | Must maintain a physical registered address; no mandatory local resident director under general rules, though regulated sectors may impose residency requirements |

| Capital | EGP; minimum EGP 250,000 for private JSCs; EGP 5,000,000 for publicly offered companies | At least 10% of each share's nominal value must be paid upon subscription; full payment required within 10 years |

| Privacy | Shareholder register maintained at GAFI; publicly listed companies subject to Egyptian Exchange (EGX) disclosure rules | Private JSCs have limited public disclosure obligations beyond statutory filings |

Focus Points

- Taxation: Corporate income tax applies at a flat 22.5% on net profits; VAT is charged at 14% on applicable supplies; dividends distributed to non-resident shareholders are subject to a 10% withholding tax; stamp duty applies to certain contracts and documents — see the Egyptian Tax Authority for current rates and obligations.

- Annual compliance: Mandatory audited financial statements, annual general assembly, and filing of tax returns with the Egyptian Tax Authority; listed companies must also comply with the Financial Regulatory Authority (FRA) disclosure requirements.

- Treaty access: Egypt maintains a broad network of double taxation agreements, and the S.A.E. structure generally qualifies for treaty benefits, subject to beneficial ownership and substance conditions.

- Conversion: A JSC may be converted into another company form under Companies Law No. 159 provided the conversion satisfies creditor protection requirements and receives shareholder approval.

- Restrictions: Foreign ownership is permitted in most sectors, but specific industries — including media, aviation, and certain defence-related activities — impose foreign equity caps or require prior ministerial consent.

Sub-Types

Privately Held Joint Stock Company

Shares are not offered to the public and cannot be listed on the Egyptian Exchange. This structure is used for large family-owned businesses, holding structures, and joint ventures where the parties want the liability protection and governance formality of a JSC without public market obligations.

Publicly Held Joint Stock Company

Shares are offered to the public or listed on the EGX. This sub-type is subject to additional FRA oversight, mandatory prospectus requirements, and continuous disclosure obligations beyond those imposed on private JSCs.

Who Uses This Structure

The S.A.E. is the standard vehicle for foreign direct investment projects, large trading operations, and regional holding structures where credibility with financial institutions and contractual counterparties matters. The ability to issue multiple share classes and accommodate an unlimited number of shareholders gives it structural flexibility that smaller entity forms cannot provide. The principal drawback is administrative burden — mandatory audits, a formal board, general assembly requirements, and dual regulatory oversight make this structure disproportionate for small or single-owner operations.

The S.A.E. is best suited for large-scale commercial enterprises, foreign investors seeking majority or full ownership, and businesses that may require external capital or institutional financing.

Company Incorporation in Egypt

Expanship assists with end-to-end S.A.E. formation in Egypt, including GAFI registration, capital requirements, and post-incorporation compliance setup.

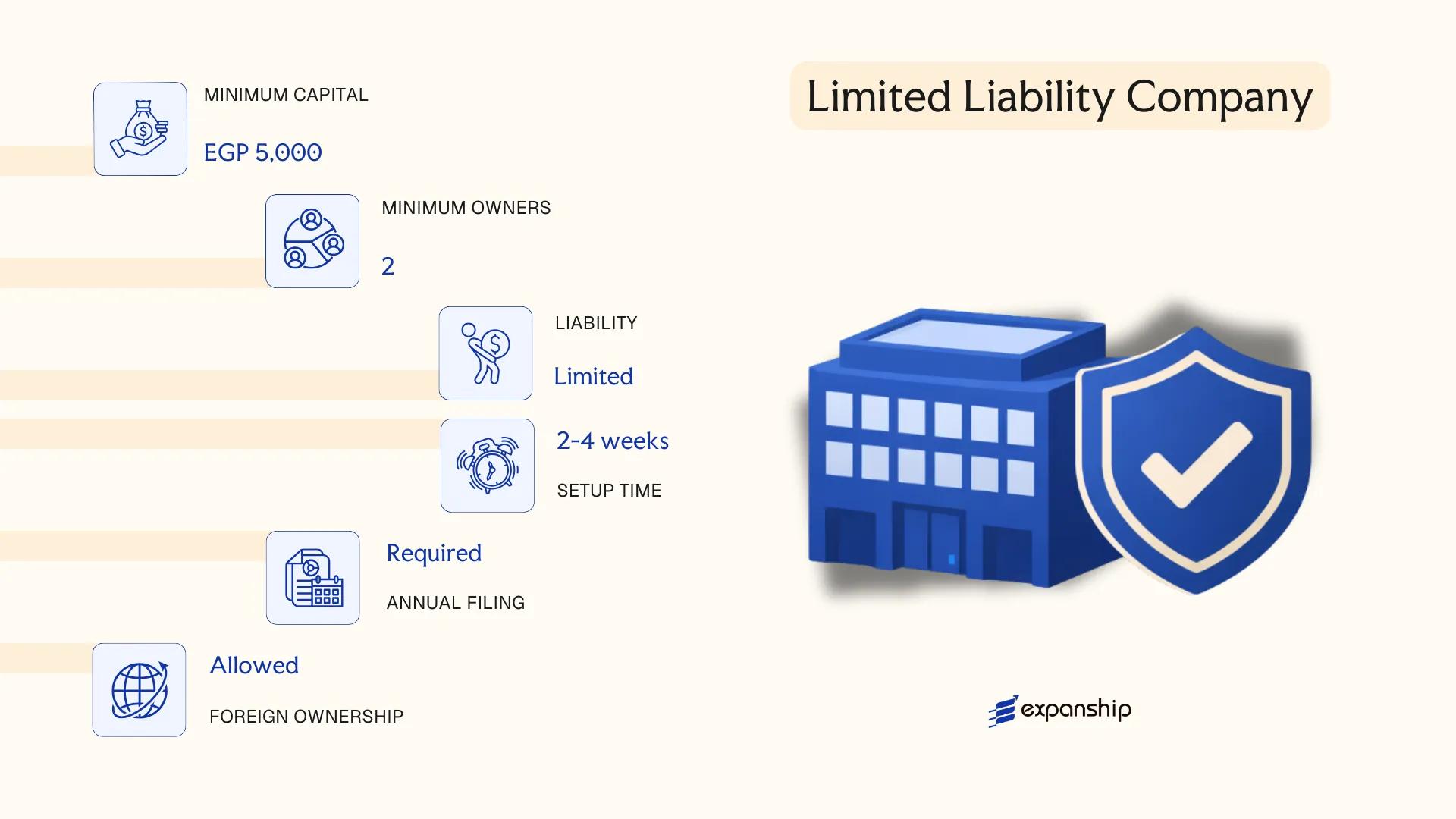

Limited Liability Company (LLC / Sharikat Dhat Mas'ouliyah Mahdoudah)

Governed by Law No. 159 of 1981 (the Companies Law) alongside supplementary provisions under Investment Law No. 72 of 2017, the limited liability company Egypt LLC formation framework creates a separate legal entity distinct from its members. Liability is confined to each member's capital contribution, meaning personal assets remain outside the reach of company creditors.

The Sharikat Dhat Mas'ouliyah Mahdoudah is structured as a hybrid — combining the capital characteristics of a corporation with the operational flexibility typically associated with smaller commercial entities. Registration is administered through the General Authority for Investment and Free Zones (GAFI) or the Commercial Registry, depending on the activity type.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Company (LLC) | Separate legal personality; governed by Law No. 159 of 1981 |

| Members | 2 minimum, 50 maximum | Members hold "quotas," not shares; no public trading of interests permitted |

| Management | One or more managers (not a board) | Managers may be members or third-party appointees; no mandatory Egyptian residency requirement for managers |

| Local Presence | Registered office address in Egypt required | A physical or registered address must be maintained; no statutory registered agent requirement |

| Capital | No statutory minimum for standard LLCs under current rules | Capital must be adequate for declared activity; GAFI may impose sector-specific minimums |

| Privacy | Member names filed with the Commercial Registry | Registry records are publicly accessible; no nominee quota-holder framework exists under local law |

Focus Points

- Taxation: Subject to corporate income tax at 22.5% on net profits; VAT applies at the standard rate of 14% on taxable supplies; withholding tax obligations apply to dividends, royalties, and certain service payments; stamp duty applies to contracts and commercial instruments.

- Annual Compliance: Must file audited financial statements annually; appointment of a licensed auditor is mandatory regardless of company size.

- Treaty Access: Egypt maintains an extensive double tax treaty network; an LLC resident in Egypt is generally treaty-eligible, though substance and beneficial ownership conditions may apply.

- Restrictions: LLCs may not engage in banking, insurance, or investment fund activities, which require distinct legal structures.

- Conversion: An LLC may be converted into a Joint Stock Company (JSC) upon meeting the applicable capital and shareholder thresholds under the Companies Law.

Closing Paragraph

The LLC suits trading operations, service businesses, and holding structures where public capital-raising is not a priority and a leaner governance framework is preferred. Its main advantage is operational simplicity relative to a Joint Stock Company; the principal limitation is the 50-member cap, which restricts scalability for businesses anticipating broad equity participation.

Best suited for small-to-medium foreign or domestic enterprises seeking a straightforward operating structure in Egypt without the compliance burden of a full corporate board.

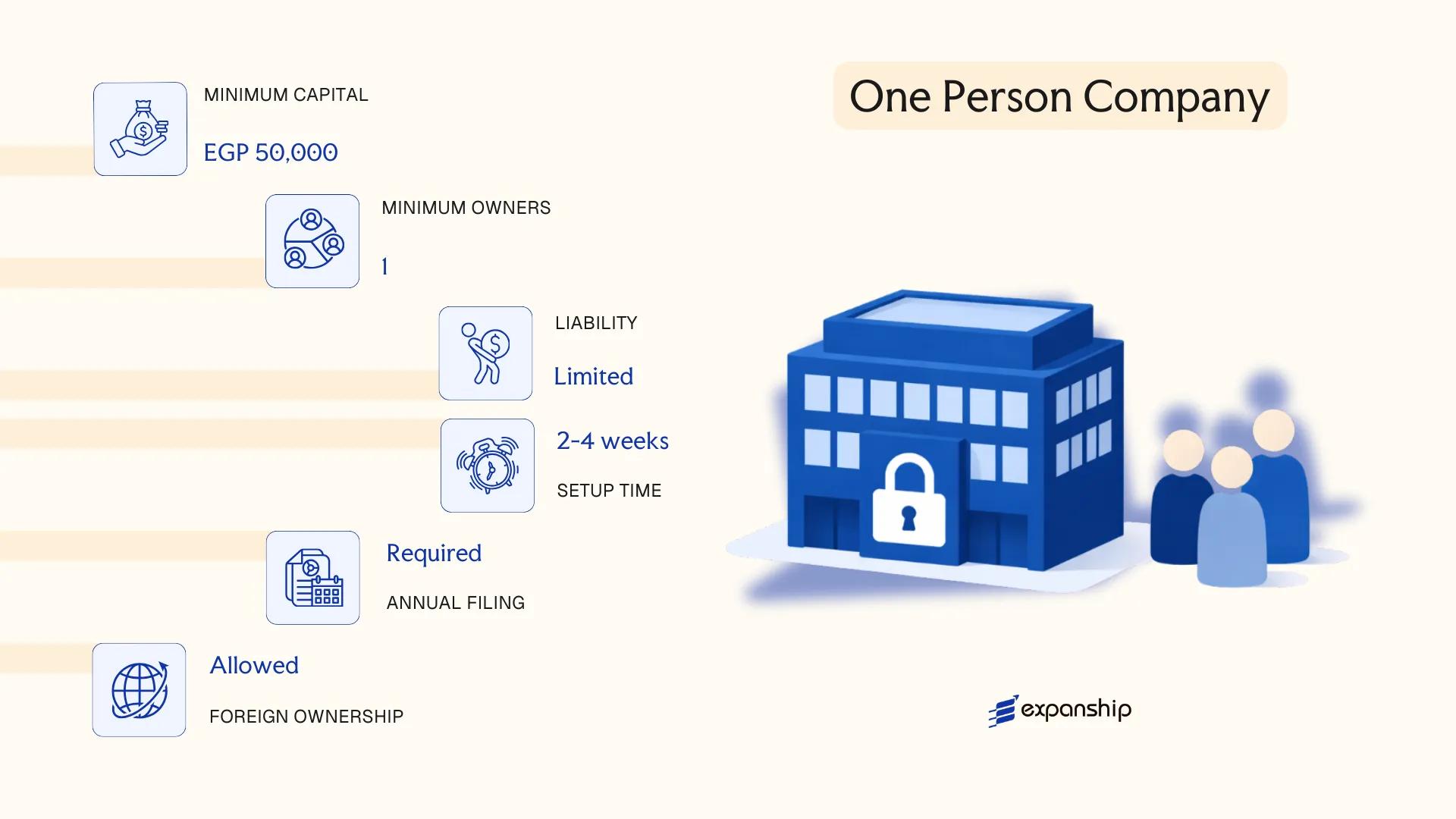

One-Person Company (OPC)

Introduced under Law No. 4 of 2018, which amended the Egyptian Companies Law No. 159 of 1981, the One-Person Company (OPC) allows a single natural or legal person to establish a company for one person company Egypt OPC registration purposes with full limited liability. The entity holds a distinct legal personality, meaning your personal assets remain separate from the company's obligations.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability – Single Shareholder | Governed under the amended Companies Law No. 159 of 1981 |

| Members | Sole Owner (natural or legal person); no minimum share split required | Referred to as the "Owner"; a manager may be appointed separately |

| Capital | EGP 50,000 minimum | Must be fully paid upon incorporation |

| Local Presence | Registered office address required in Egypt | No mandatory local director, but a manager must be designated |

| Privacy | Owner details filed with GAFI; not publicly searchable by default | Commercial Register entry is publicly accessible |

Focus Points

- Taxation: Subject to 22.5% corporate income tax; standard VAT at 14% applies; withholding tax obligations apply on dividends and service payments; stamp duty applies to certain contracts.

- Annual Compliance: Financial statements must be filed annually; an auditor appointment is mandatory regardless of size.

- Conversion: Can be converted into an LLC or Joint Stock Company if ownership or capital thresholds change.

- Restrictions: Cannot engage in banking, insurance, or investment fund activities under this structure.

- Treaty Access: Qualifies for double taxation treaty benefits under Egypt's treaty network, subject to substance requirements.

Closing

The OPC suits consultants, freelancers, and holding structures where a single founder requires limited liability without co-shareholders. The primary limitation is the EGP 50,000 minimum capital requirement and the prohibition on certain regulated industries.

Best suited for a single founder or parent company seeking a standalone operating or holding entity with capped personal liability under Egyptian law.

Foreign Business Structures in Egypt [Branch Office, Representative Office]

A foreign company branch office Egypt setup is governed primarily by Law No. 159 of 1981 (the Companies Law) alongside Investment Law No. 72 of 2017, with oversight from the General Authority for Investment and Free Zones (GAFI). Both a Branch Office and a Representative Office allow foreign entities to establish a legal presence without incorporating a separate Egyptian company.

Neither structure carries independent legal personality. Each operates as an extension of the parent company, which retains full liability for obligations incurred in Egypt.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Form | Extension of foreign parent; no separate legal personality | Extension of foreign parent; no separate legal personality |

| Permitted Activities | Commercial and operational activities | Promotional and liaison activities only; no revenue-generating transactions |

| Governing Authority | GAFI | GAFI |

| Local Presence | Registered address in Egypt required | Registered address in Egypt required |

| Capital | No statutory minimum, but must demonstrate sufficient funding from parent | No statutory minimum |

| Liability | Parent company bears full liability | Parent company bears full liability |

Focus Points

- Taxation: Branch profits are subject to 22.5% corporate income tax; VAT at 14% applies to taxable supplies; withholding tax may apply to remittances to the parent depending on applicable double tax treaties.

- Treaty Access: Egypt's double tax treaty network may reduce withholding tax rates, but treaty eligibility depends on the parent's jurisdiction and treaty terms.

- Annual Compliance: Both structures require annual renewal with GAFI and submission of audited financial statements.

- Restrictions: A Representative Office cannot invoice clients or generate local revenue; commercial activity is strictly prohibited.

- Conversion: A Branch Office may be converted into a locally incorporated entity, though this involves a separate registration process with GAFI.

Sub-Types

Branch Office

A Branch Office may conduct full commercial operations — entering contracts, generating revenue, and employing staff — on behalf of its foreign parent. It is the standard choice for foreign firms seeking operational presence without a locally incorporated subsidiary.

Representative Office

A Representative Office is limited to market research, promoting the parent company's products or services, and liaising with local clients. It cannot sign commercial contracts or collect payments, making it unsuitable for revenue-generating activity.

Closing

Both structures suit foreign businesses testing the Egyptian market or supporting an existing client base without committing to full local incorporation. The primary advantage is speed and lower setup cost relative to a new entity; the key limitation is that the parent company carries unlimited liability for all local obligations.

Foreign companies seeking a controlled, low-commitment operational or promotional presence before committing to full local incorporation.

Partnership Structures in Egypt [General Partnership, Limited Partnership, Joint Venture]

Partnership structures in Egypt — general, limited, and joint venture forms — are governed primarily by the Egyptian Commercial Code (Law No. 17 of 1999) and, where applicable, by the Companies Law No. 159 of 1981. General and limited partnerships carry separate legal personality upon registration, while joint ventures do not acquire legal personality and exist solely through contractual agreement between the parties.

Registration of partnership entities is handled through the General Authority for Investment and Free Zones (GAFI) or the relevant commercial registry, depending on the activity and structure involved.

Key Characteristics

| Requirement | General Partnership | Limited Partnership | Joint Venture |

|---|---|---|---|

| Legal Form | Separate legal personality | Separate legal personality | No legal personality; contractual only |

| Members | Partners (min. 2; no statutory maximum) | Min. 1 general partner + 1 limited partner | Min. 2 parties; no statutory cap |

| Liability | Unlimited for all partners | Unlimited for general partners; limited to capital contribution for limited partners | Governed by the joint venture agreement |

| Local Presence | Registered address required | Registered address required | No formal registration requirement |

| Capital | No statutory minimum; denominated in EGP | No statutory minimum; limited partner's contribution must be defined | Determined contractually |

| Privacy | Partner names disclosed in commercial registry | Partner names and contribution amounts disclosed | Agreement is private; not filed publicly |

Focus Points

- Taxation: All partnership income is subject to Egyptian corporate income tax at 22.5%; VAT at 14% applies to taxable supplies; withholding tax obligations apply on payments to non-residents; stamp duty may apply to partnership agreement execution.

- Annual Compliance: Audited financial statements and tax filings are required for registered partnerships; joint ventures file through the participating entities individually.

- Treaty Access: Registered partnerships may access Egypt's double tax treaty network, subject to residency and beneficial ownership conditions; joint ventures have no independent treaty standing.

- Restrictions: General partners in a limited partnership bear full personal liability; foreign nationals forming general partnerships should confirm sector-specific foreign ownership rules apply equally.

- Conversion: Conversion from a partnership to a limited liability company or joint stock company is permissible but requires a formal restructuring process through GAFI and the commercial registry.

Sub-Types

General Partnership (Sharikat al-Tadamon)

All partners hold unlimited joint liability for the firm's obligations. This structure is typically used by small professional or family-run commercial businesses where partners operate the entity directly and personal liability is commercially accepted.

Limited Partnership (Sharikat al-Tawsiyah al-Basitah)

At least one general partner manages the business and bears unlimited liability, while limited partners contribute capital without participating in management. This arrangement suits investors seeking passive exposure without operational involvement.

Joint Venture (Sharikat al-Muhasa)

A contractual arrangement with no separate legal personality, the joint venture operates internally between parties and is not registered as a standalone entity. It is frequently used for project-specific collaboration, construction contracts, or co-investment arrangements where public disclosure is not desired.

Closing

Partnership structures suit trading operations, project-based collaborations, and professional service arrangements where operational flexibility outweighs the need for formal corporate structure. The absence of a minimum capital requirement lowers the entry threshold, though unlimited liability exposure for general partners remains a significant structural risk in commercial disputes.

General and limited partnerships are most appropriate for closely held commercial ventures or investor-operator arrangements; joint ventures suit parties seeking project-specific collaboration without incorporating a new entity.

Sole Proprietorship (Individual Business)

A sole proprietorship Egypt individual business registration falls outside the corporate framework established by Companies Law No. 159 of 1981. Governed instead by the Commercial Code and the Income Tax Law No. 91 of 2005, this structure carries no separate legal personality — the owner and the business are treated as one entity under Egyptian law.

Registration is handled through the General Authority for Investment and Free Zones (GAFI) or the relevant commercial registry, depending on the activity type. Because the proprietor bears unlimited personal liability for all business obligations, personal assets remain fully exposed to creditors.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated individual business | No separate legal personality from the owner |

| Owner Title | Sole Proprietor | Single natural person only; no co-owners permitted |

| Membership | 1 (natural person only) | No minimum capital prescribed by law |

| Local Presence | Commercial registration address required | Must hold a valid local business address |

| Capital | EGP; no statutory minimum | Owner contributes at will |

| Liability | Unlimited personal liability | Personal assets exposed to business debts |

Focus Points

- Taxation: Subject to personal income tax under Law No. 91 of 2005 at progressive rates up to 25%; VAT registration required once turnover exceeds the statutory threshold; no separate corporate tax applies.

- Annual Compliance: Must maintain commercial registration, file annual income tax returns, and renew any applicable trade or professional licences.

- Treaty Access: As an unincorporated structure, the proprietor may not qualify for benefits under Egypt's double taxation treaties, which generally apply to corporate entities.

- Conversion: Can be converted into an LLC or other incorporated form, though the process requires fresh registration and does not carry over legal continuity automatically.

- Restrictions: Foreign nationals face significant restrictions on operating as sole traders; foreign ownership in this form is generally not permitted without specific regulatory approval.

Closing

This structure suits Egyptian nationals conducting small-scale trade, freelance, or service-based activities where administrative simplicity outweighs the need for liability protection. The absence of a minimum capital requirement lowers the entry barrier, but unlimited personal liability remains a material drawback for any business carrying financial or contractual risk.

Egyptian national individuals operating low-risk, small-scale commercial or professional activities who require minimal setup formality.

How to Choose the Right Entity Type in Egypt

Selecting the correct entity type is a structural decision with direct legal and financial consequences that persist for the life of your business.

Why Your Entity Choice Matters

- Registering a representative office when your business intends to generate local revenue breaches the permitted scope under Egyptian Companies Law No. 159 of 1981, exposing the entity to administrative penalties and potential cancellation by the General Authority for Investment and Free Zones (GAFI).

- Selecting a structure that falls outside Egypt's tax treaty network — such as certain offshore or free zone arrangements — means your business cannot claim reduced withholding tax rates available under bilateral agreements.

- Forming a Joint Stock Company when operations involve a single owner creates mandatory board and general assembly obligations under Law No. 159 of 1981 that an LLC or One-Person Company does not require, adding unnecessary compliance costs.

- Choosing a branch structure when local equity ownership is required for your activity category results in licensing refusals, since branches do not constitute an independent legal personality under Egyptian law.

Key Factors to Consider

- Business Activity: Active trading, regulated sectors such as banking or insurance, and passive asset-holding each point toward a distinct structure under Egyptian law.

- Ownership Configuration: A sole operator should evaluate the OPC, while multi-party ventures must decide between the governance requirements of an LLC and a JSC.

- Tax Position: Your need to access Egypt's bilateral tax treaty network, qualify for free zone exemptions, or operate under the standard corporate tax rate should drive entity selection.

- Liability Exposure: Unlimited personal liability under general partnership arrangements may be unsuitable where your firm carries significant commercial or contractual risk.

- Regulatory Licensing: Certain activities require GAFI approval or sector-specific licensing that is only available to particular entity forms.

- Exit and Conversion: Not all Egyptian entity types permit straightforward conversion or redomiciliation, so intended exit mechanisms should be assessed before incorporation.

The full text of Egyptian Companies Law No. 159 of 1981 is published through GAFI's official resources and should be reviewed alongside any sector-specific regulations applicable to your activity.

Compliance Services for Companies in Egypt

Ongoing compliance support for Egyptian entities, including annual filings, statutory obligations, and regulatory reporting under Egyptian Companies Law.

Conclusion

Selecting the right structure is one of the most consequential decisions in this Egypt company formation summary guide. The Joint Stock Company suits larger enterprises and those planning to raise public capital under Companies Law No. 159 of 1981. An LLC remains the most commonly registered entity for small to mid-sized foreign investment, given its comparatively straightforward setup under the same law. The One-Person Company serves solo founders requiring limited liability without partners. Branch and representative offices address foreign firms testing the market before committing to full incorporation.

Egypt's General Authority for Investment and Free Zones (GAFI) has continued to digitize registration procedures, and the country's expanding bilateral investment treaty network signals a gradual shift toward a more structured foreign investment framework. Incorporating in Egypt carries distinct regulatory considerations depending on the entity chosen, and Expanship's team works directly within these frameworks to support your setup.

How Expanship Can Assist You

As a corporate services company, Expanship handles incorporation in Egypt across all major entity types covered in this blog — from Limited Liability Companies registered under Law No. 159 of 1981 to One-Person Companies and branch office filings. Every engagement is coordinated with the General Authority for Investment and Free Zones (GAFI), Egypt's primary regulatory body for business registration.

Your documents, filings, and post-incorporation obligations are managed end to end. Expanship's Egypt business setup services include:

- Document preparation, notarization, and legalization

- Registered agent and local office address provision

- Government filing and GAFI liaison

- Commercial registry submissions and follow-up

- Post-incorporation compliance management

- Banking introduction assistance

Reach out to Expanship Egypt to discuss which structure fits your business objectives and what the registration process looks like for your specific situation.

Frequently Asked Questions (FAQ)

The Limited Liability Company (LLC), governed by Companies Law No. 159 of 1981, is the most frequently registered structure. Its relatively low minimum capital requirements, flexible management, and suitability for small to mid-size ventures make it the default choice for both local and foreign investors.

A Joint Stock Company (JSC) can offer shares to the public and access capital markets, while an LLC cannot issue publicly tradable shares. Both structures are subject to corporate tax under the Income Tax Law No. 91 of 2005, but the JSC carries heavier compliance obligations, including mandatory audits and a supervisory board requirement once shareholder numbers reach certain thresholds.

The One-Person Company (OPC) limits public disclosure compared to multi-shareholder structures, as beneficial ownership is concentrated in a single individual. Nominee arrangements are not a formally recognized mechanism under Egyptian law, so privacy derives primarily from structural simplicity rather than nominee services.

No. An LLC requires a minimum of two shareholders, and a General Partnership requires at least two partners. The OPC was specifically introduced to accommodate single-founder registration, while a Joint Stock Company requires a minimum of three founders under Companies Law No. 159 of 1981.

Foreigners may establish an LLC, JSC, OPC, or Branch Office in Egypt. Foreign investment is regulated primarily through the Investment Law No. 72 of 2017, administered by the General Authority for Investment and Free Zones (GAFI). Certain sectors remain restricted or require minimum Egyptian ownership percentages, so the applicable activity determines which structure is viable.

Egyptian law permits the conversion of one company form into another, subject to GAFI approval and compliance with the procedural requirements set out in Companies Law No. 159 of 1981. An LLC can be converted into a JSC, for example, provided the new entity meets the capital and shareholder requirements of the target structure.

Not all structures carry separate legal personality. The LLC, JSC, OPC, and Limited Partnership with shares are recognized as distinct legal persons. A General Partnership does not provide a corporate shield, meaning partners bear joint and unlimited liability for the firm's obligations.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.