Key Takeaways

- The Anpartsselskab (ApS) is the most commonly registered business form in Denmark, offering limited liability without the capital and governance requirements of the Aktieselskab (A/S).

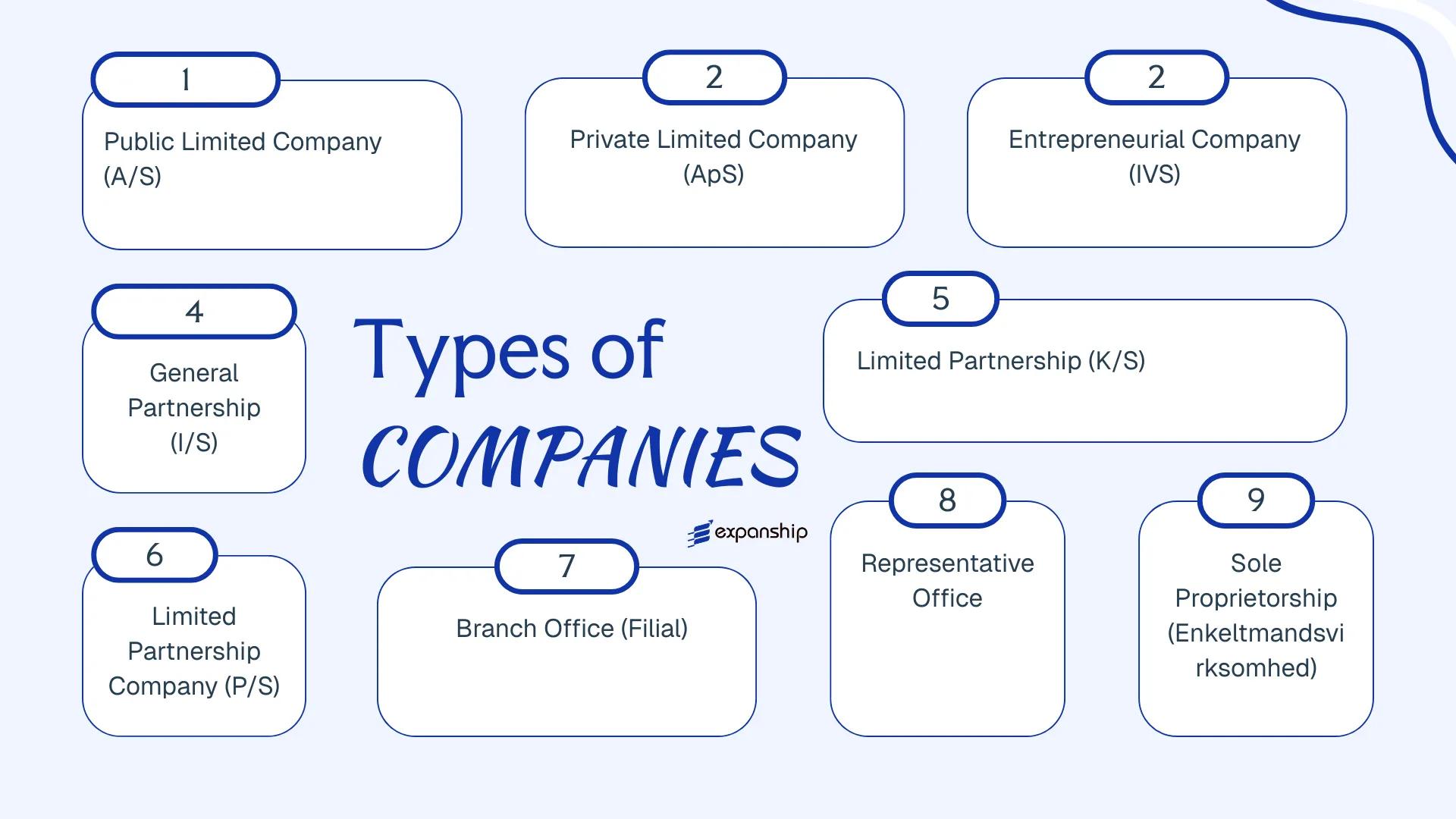

- Denmark's corporate landscape spans nine distinct entity types, each governed by the Danish Companies Act (Selskabsloven) and administered by the Danish Business Authority (Erhvervsstyrelsen).

- Foreign companies can enter the Danish market through a branch office (Filial) or representative office without incorporating a separate legal entity.

- Partnerships such as the Kommanditselskab (K/S) and Partnerselskab (P/S) serve distinct structural purposes, with the P/S combining partnership flexibility with share-based capital.

Introduction to Entity Types in Denmark

Denmark is a Scandinavian nation in Northern Europe, bordering Germany to the south and connected to Sweden via the Øresund Bridge. As an independent constitutional monarchy and EU member state, it maintains a well-regulated corporate environment governed by the Danish Business Authority (Erhvervsstyrelsen), which administers company registration and ongoing compliance.

The tax framework is treaty-based, with Denmark participating in an extensive network of double taxation agreements alongside domestic corporate tax obligations.

Businesses registering in Denmark can choose from several distinct types of business entities in Denmark: Aktieselskab (A/S), Anpartsselskab (ApS), Iværksætterselskab (IVS), Interessentskab (I/S), Kommanditselskab (K/S), Partnerselskab (P/S), branch offices (Filial), representative offices, and sole proprietorships (Enkeltmandsvirksomhed). Each structure carries different requirements around capital, liability, governance, and registration under the Danish Companies Act (Selskabsloven). This article examines each of these business structures available in Denmark in turn, covering formation requirements, liability implications, and regulatory obligations.

An Overview of Business Structures in Denmark

Governed primarily by the Danish Companies Act (Selskabsloven), enacted in 2009 and administered by the Danish Business Authority (Erhvervsstyrelsen), the overview of Danish business structures covers six distinct legal forms available to domestic and foreign investors. A seventh option, the sole proprietorship, falls outside Selskabsloven and is regulated separately under the Act on Certain Commercial Enterprises (Lov om visse erhvervsdrivende virksomheder). Each form carries a different liability profile, capital requirement, and tax treatment suited to specific commercial objectives.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Aktieselskab (A/S) | Public limited company | Limited | Taxed | Yes | 1 shareholder | Erhvervsstyrelsen | Selskabsloven |

| Anpartsselskab (ApS) | Private limited company | Limited | Taxed | Yes | 1 shareholder | Erhvervsstyrelsen | Selskabsloven |

| Iværksætterselskab (IVS) | Entrepreneurial company | Limited | Taxed | Yes | 1 shareholder | Erhvervsstyrelsen | Selskabsloven |

| Interessentskab (I/S) | General partnership | Unlimited | Taxed at partner level | Yes | 2 partners | Erhvervsstyrelsen | Lov om visse erhvervsdrivende virksomheder |

| Kommanditselskab (K/S) | Limited partnership | Mixed | Taxed at partner level | Yes | 1 general + 1 limited | Erhvervsstyrelsen | Lov om visse erhvervsdrivende virksomheder |

| Partnerselskab (P/S) | Limited partnership company | Mixed | Taxed at partner level | Yes | 1 general + 1 limited | Erhvervsstyrelsen | Selskabsloven |

| Filial (Branch) | Foreign branch | Parent liable | Taxed on Danish income | Yes | Parent company | Erhvervsstyrelsen | Selskabsloven |

| Representative Office | Non-trading presence | Parent liable | Generally exempt | No | Parent company | Erhvervsstyrelsen | General commercial law |

| Enkeltmandsvirksomhed | Sole proprietorship | Unlimited | Taxed personally | Yes | 1 individual | Erhvervsstyrelsen | Lov om visse erhvervsdrivende virksomheder |

Each of these structures is examined in full in the sections below.

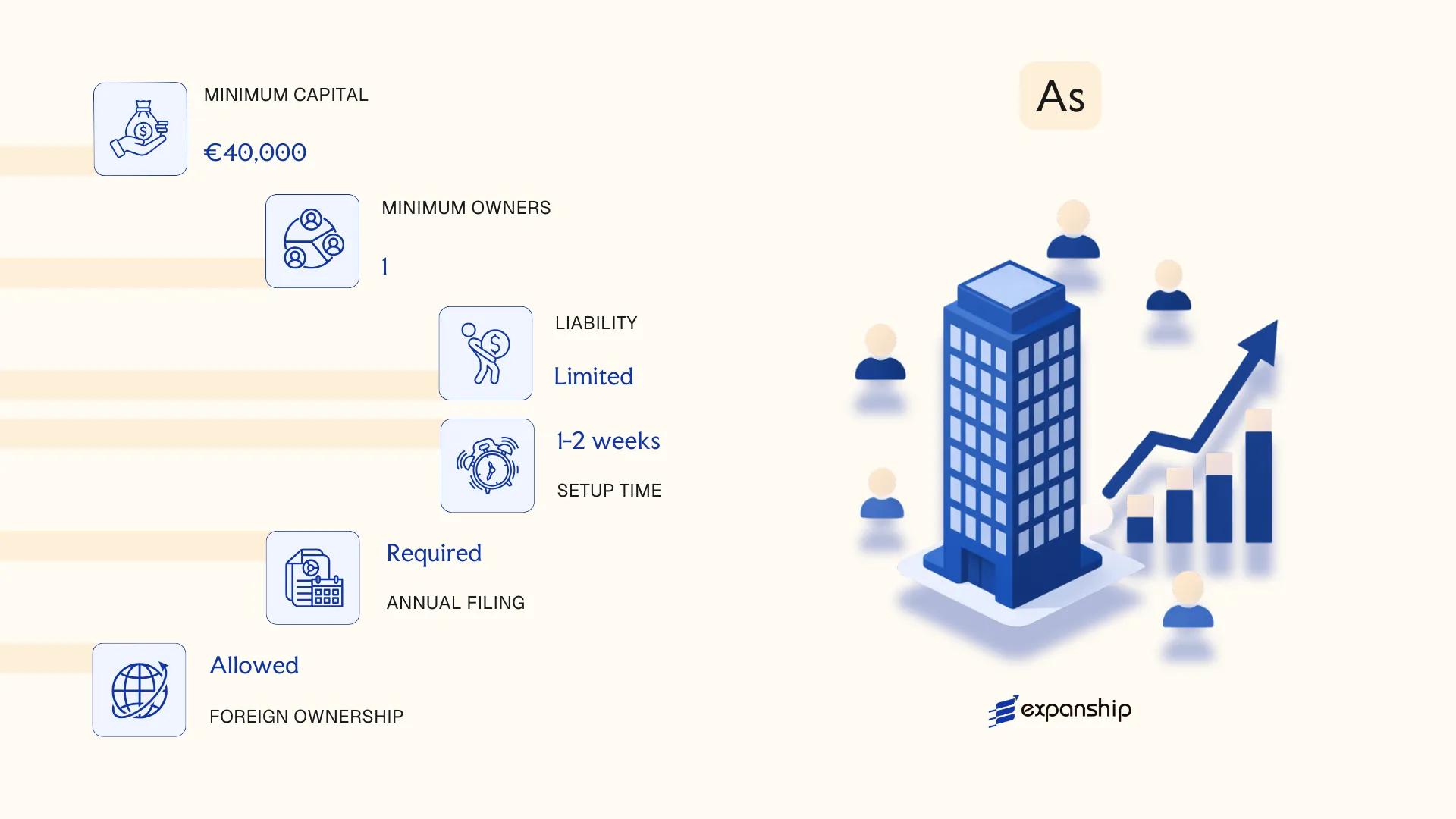

Public Limited Company (Aktieselskab – A/S)

The Denmark Aktieselskab A/S public limited company is governed by the Danish Companies Act (Selskabsloven), consolidated in 2009 and administered by the Danish Business Authority (Erhvervsstyrelsen). It carries separate legal personality, meaning the entity holds rights and obligations independently of its shareholders.

Shareholders bear no personal liability beyond their capital contribution. The A/S structure suits firms requiring external equity financing, as shares may be listed on a regulated market such as Nasdaq Copenhagen.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Limited Company (Aktieselskab) | Separate legal personality; limited liability |

| Members | Shareholders (no maximum); minimum 1 shareholder | Shareholders may be natural persons or legal entities |

| Governance | Board of Directors (Bestyrelse) + Executive Management (Direktion); or Supervisory Board + Executive Board | Two-tier or single-tier structure permitted under Selskabsloven |

| Local Presence | Registered office in Denmark required | No mandatory resident director, but a registered address with Erhvervsstyrelsen is compulsory |

| Share Capital | Minimum DKK 400,000; must be fully subscribed at formation | At least 25% paid up on registration; remainder within 12 months |

| Privacy | Shareholders and directors are publicly disclosed via the CVR register | Beneficial ownership is reported to the CVR register |

Focus Points

- Taxation: Subject to Danish corporate income tax at 22%; VAT registration required if taxable turnover exceeds DKK 50,000; withholding tax applies to dividends (standard 27%, reducible under applicable tax treaties), interest, and royalties.

- Annual Compliance: Obligatory annual general meeting, statutory audit (exemptions available for smaller firms), and filing of annual accounts with Erhvervsstyrelsen.

- Economic Substance: No specific offshore substance test, but genuine management and control in Denmark is relevant for tax residency determination under Danish and EU rules.

- Treaty Access: As a Danish tax-resident entity, an A/S has access to Denmark's extensive double tax treaty network and benefits under EU Directives, including the Parent-Subsidiary Directive.

- Conversion: An A/S may be converted into an ApS or other recognised form under the Selskabsloven without dissolution, provided statutory conditions are met.

Closing

The A/S is commonly used for large trading operations, holding structures, and businesses seeking capital-market access or institutional investment. The ability to issue publicly tradeable shares is a structural advantage, though the DKK 400,000 minimum capital requirement and mandatory audit obligations represent a higher administrative threshold than most other Danish entity forms.

The Aktieselskab is best suited for established businesses, joint ventures, or any operation intending to raise capital from the public or institutional investors.

Company Incorporation in Denmark

Incorporate an Aktieselskab or other Danish entity with full regulatory support from Expanship.

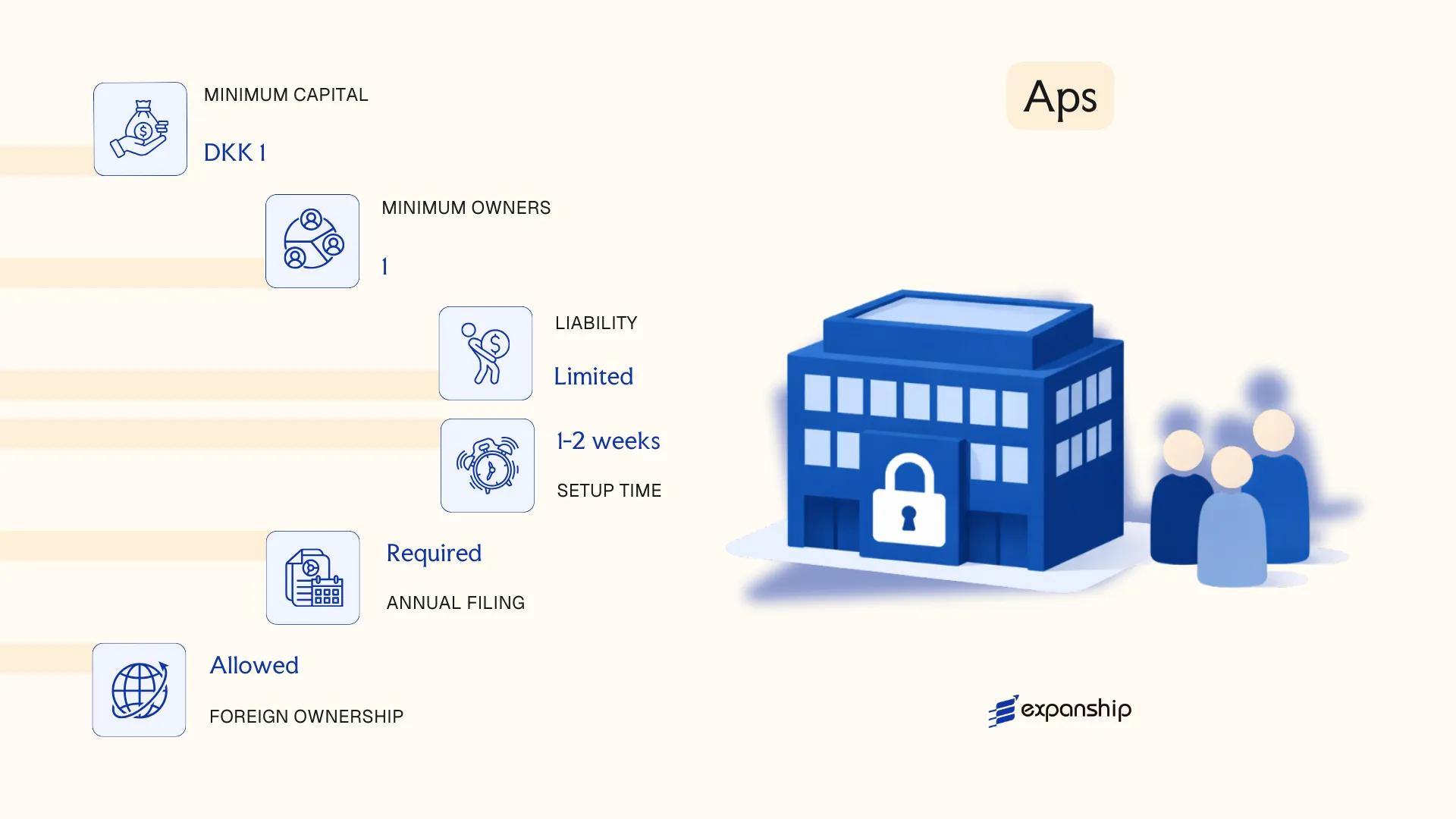

Private Limited Company (Anpartsselskab – ApS)

The Denmark Anpartsselskab ApS private limited company is governed by the Danish Companies Act (Selskabsloven), enacted in 2009, which consolidated and modernised the prior legislative framework for both private and public limited companies. The entity carries separate legal personality, meaning it exists independently of its owners, and liability is confined to the capital contributed.

Structurally, the ApS sits between a sole proprietorship and a publicly listed company. Ownership is divided into capital interests (anparter) rather than publicly tradeable shares, which restricts free transferability and makes the form better suited to closely held businesses.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private Limited Company (Anpartsselskab) | Registered with the Danish Business Authority (Erhvervsstyrelsen) |

| Members | 1 or more shareholders; no maximum | Shareholders are referred to as anpartshavere; single-member structure is permitted |

| Management | Board of Directors optional; at least 1 Executive Director required | A supervisory board (bestyrelse) becomes mandatory at 35+ employees |

| Local Presence | Registered office address in Denmark required | No statutory requirement for a local resident director |

| Share Capital | Minimum DKK 40,000 | Must be fully paid up at incorporation; no par value requirement |

| Privacy | Shareholders are listed in the public CVR register | Beneficial ownership is reported to the Register of Actual Owners |

Focus Points

- Taxation: Subject to standard Danish corporate income tax at 22%; VAT registration required once annual turnover exceeds DKK 50,000; dividend withholding tax applies at 27% (reduced under tax treaties); no stamp duty on share capital.

- Annual Compliance: Annual report must be filed with Erhvervsstyrelsen; audit requirements depend on company size classification under the Financial Statements Act (Årsregnskabsloven).

- Treaty Access: As a tax-resident entity, the ApS has access to Denmark's extensive double tax treaty network and benefits under EU directives, including the Parent-Subsidiary Directive.

- Conversion: An ApS can be converted to an A/S through a formal resolution process under Selskabsloven, subject to meeting the higher capital threshold.

- Transfer Restrictions: Articles of association (vedtægter) may impose pre-emption rights or consent requirements on the transfer of anparter.

Closing Paragraph

The ApS is widely used for trading operations, holding structures, and SME activity where founders require limited liability without the capital and administrative burden associated with a public company. The lower minimum capital threshold relative to an A/S makes incorporation accessible, though the restricted transferability of interests limits its utility for businesses seeking external equity investment.

Founders and SMEs seeking a structured limited liability vehicle with minimal capital outlay and no public share issuance requirements.

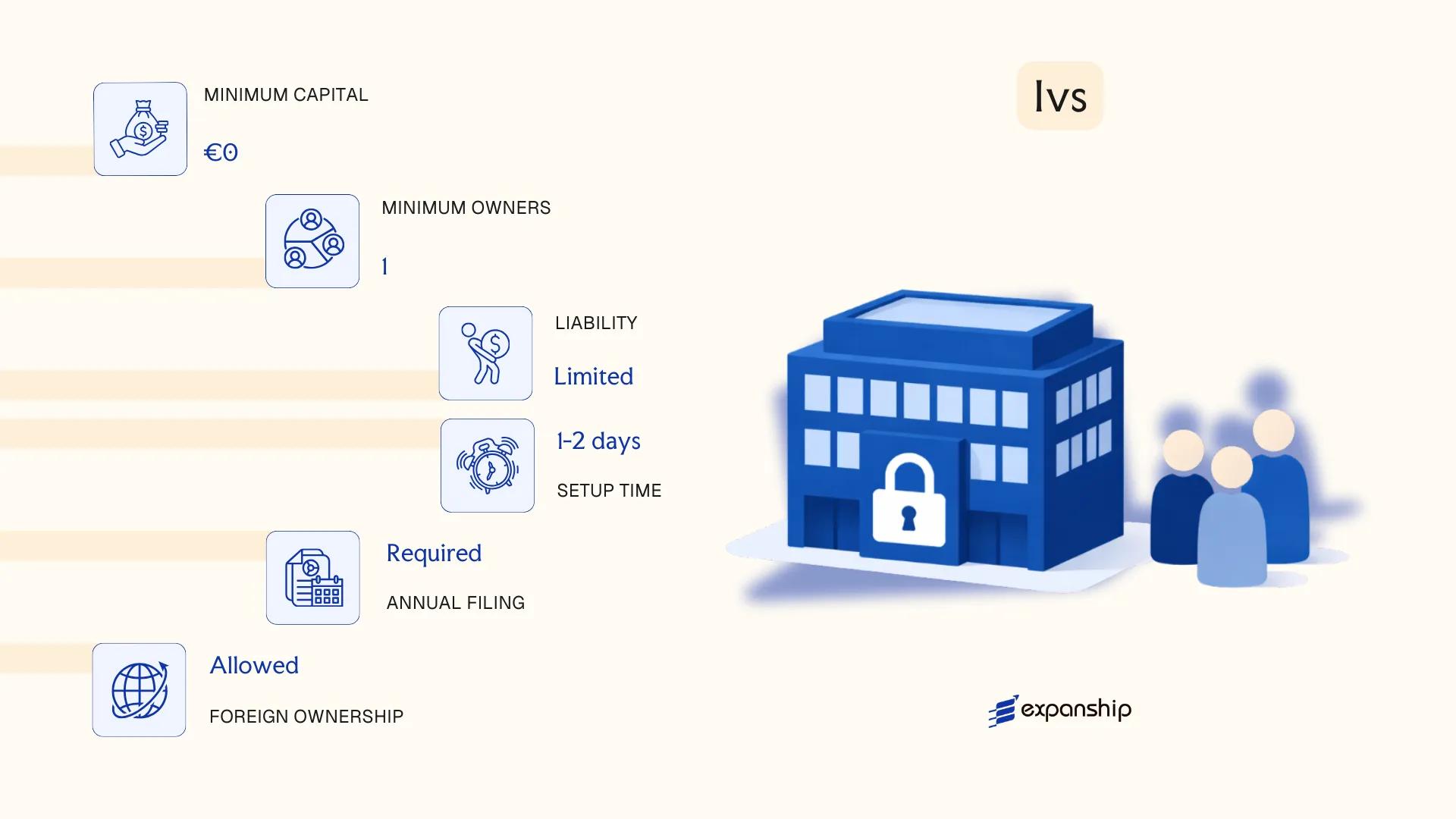

Entrepreneurial Company (Iværksætterselskab – IVS)

Introduced under the Danish Companies Act (Selskabsloven) in 2014, the IVS was designed as a low-capital entry point for startup founders. Denmark IVS entrepreneurial company registration was available with a minimum share capital of just DKK 1, making the structure accessible to early-stage ventures with limited funding.

Effective 15 April 2019, the Folketing abolished the IVS form through an amendment to Selskabsloven. Existing entities were granted a transitional period to either convert to an ApS by meeting the DKK 40,000 minimum capital requirement or face compulsory dissolution. No new IVS registrations have been accepted by Erhvervsstyrelsen (the Danish Business Authority) since that date.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Abolished private limited entity | No longer available for new registration as of April 2019 |

| Status | Dissolved or converted | Existing entities had to convert to ApS or dissolve |

| Conversion Path | IVS to ApS | Required meeting DKK 40,000 minimum capital threshold |

| Regulatory Body | Erhvervsstyrelsen | Administered all registrations and dissolutions |

Focus Points

- Taxation: During its active period, IVS entities were subject to the standard corporate tax rate of 22%, VAT registration obligations at the general 25% rate, and standard withholding tax rules on dividends.

- Conversion obligation: Iværksætterselskab Denmark rules required mandatory conversion or dissolution; no grandfathering was permitted beyond the transitional deadline.

- Treaty access: As a recognized corporate entity while active, the IVS had access to Denmark's tax treaty network, though its abolished status renders this point moot for new structuring.

- Current standing: The Danish IVS company abolished status is final; no legislative proposals to reinstate the form are currently under consideration.

Historically, the IVS served early-stage founders and sole operators testing a business concept before committing to full ApS capitalization. Its core limitation was precisely what defined it: the minimal capital requirement created creditor concerns and restricted the entity's operational credibility, which ultimately drove its abolition.

The IVS is no longer available; founders previously drawn to it should evaluate the ApS as the direct successor structure.

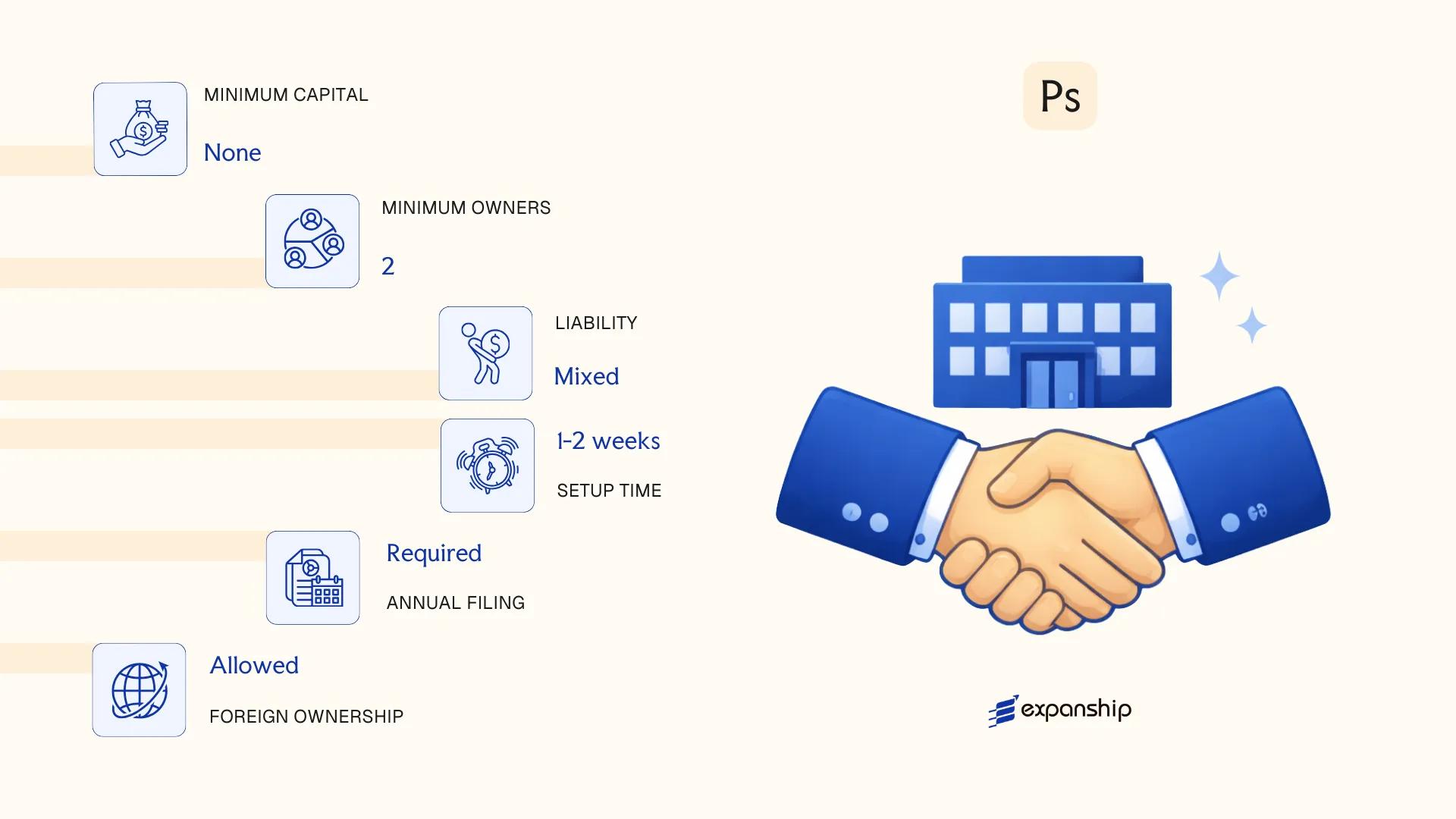

Partnerships (Interessentskab – I/S, Kommanditselskab – K/S, Partnerselskab – P/S)

Denmark partnership structures — I/S, K/S, and P/S — are governed primarily by customary commercial law and, where applicable, the Danish Companies Act (Selskabsloven, 2009). None of these forms carry separate legal personality in the same sense as a capital company, though the P/S is a notable exception with a hybrid structure.

Liability treatment differs sharply across the three forms. In an I/S, all partners bear joint and several unlimited liability. The K/S separates a general partner (with unlimited liability) from limited partners (liable only to the extent of their contribution). The P/S combines limited partnership mechanics with a share capital structure.

Key Characteristics

| Requirement | I/S | K/S | P/S |

|---|---|---|---|

| Legal Form | General partnership; no separate legal personality | Limited partnership; no separate legal personality | Limited partnership company; has separate legal personality |

| Members | Partners (minimum 2, no maximum) | General partner (min. 1) + limited partners (min. 1) | General partner (min. 1) + shareholders (min. 1) |

| Liability | All partners: unlimited, joint and several | General partner: unlimited; limited partners: capped at contribution | General partner: unlimited; shareholders: limited to share capital |

| Minimum Capital | None | None | DKK 400,000 share capital |

| Local Presence | Registered address in Denmark required | Registered address in Denmark required | Registered address; management requirements apply |

| Registration | Danish Business Authority (Erhvervsstyrelsen) | Danish Business Authority (Erhvervsstyrelsen) | Danish Business Authority; subject to Selskabsloven |

Focus Points

- Taxation: I/S and K/S are fiscally transparent — profits are taxed at the partner level under personal or corporate income tax rates; the P/S is subject to corporate tax at 22%. VAT registration is required across all forms once turnover thresholds are met.

- Annual Compliance: I/S is subject to minimal filing obligations; K/S and P/S must file annual accounts with Erhvervsstyrelsen.

- Treaty Access: Fiscally transparent entities (I/S, K/S) generally do not independently access Denmark's tax treaty network; access depends on the tax residency of the underlying partners.

- Conversion: A K/S may be converted into a P/S under Selskabsloven procedures without dissolving the underlying business.

Sub-Types

Kommanditaktieselskab (P/S)

Technically a sub-form of the limited partnership concept, the P/S issues shares rather than partnership interests, making it suitable for investment fund structures and private equity vehicles where transferability of interests matters.

Closing

K/S structures are frequently used for private equity, real estate, and fund vehicles where pass-through taxation is commercially desirable; the I/S suits professional service firms with a small number of known partners. The absence of liability protection in the I/S is a material drawback for most commercial purposes.

K/S is well-suited to institutional investors and fund managers seeking tax transparency; I/S fits closely held professional practices where partners accept personal exposure.

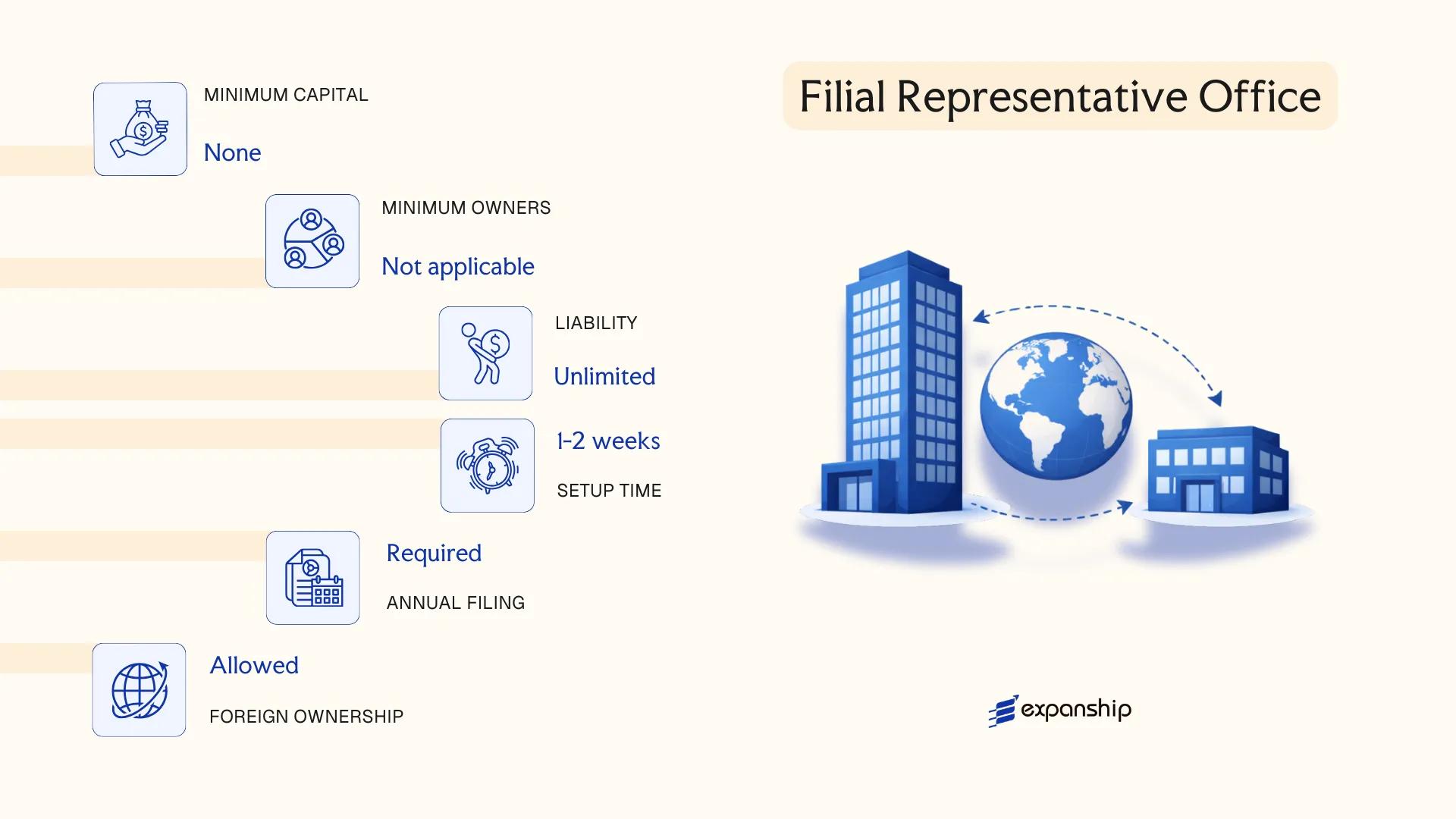

Foreign Business Structures (Branch Office – Filial, Representative Office)

Foreign companies seeking a presence in Denmark without incorporating a separate legal entity can register a branch, known as a Filial. Denmark branch office Filial registration is governed by the Danish Companies Act (Selskabsloven), specifically the provisions applicable to branches of foreign companies, along with the Executive Order on Registration with the Danish Business Authority (Erhvervsstyrelsen). A Filial is not a separate legal entity — the parent company bears full liability for all obligations incurred through the branch.

A representative office, by contrast, carries out only preparatory or auxiliary activities such as market research or liaison functions. It cannot enter into contracts or generate revenue in its own right, and registration requirements are less formal, though tax obligations may still arise depending on the level of activity.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Branch of a foreign company | Not a separate legal entity; parent is fully liable |

| Registered Representative | At least one local manager required | Must be resident in the EU/EEA or Denmark |

| Local Presence | Registered address in Denmark; registered with Erhvervsstyrelsen | Physical or c/o address acceptable |

| Capital | No minimum capital for the branch itself | Parent's capital structure governs |

| Financial Reporting | Must file annual accounts with Erhvervsstyrelsen | Parent accounts must also be submitted |

| Privacy | Manager's name is publicly registered | Parent company details disclosed |

Focus Points

- Taxation: A Filial is taxed on Danish-source income at the standard corporate rate of 22%; VAT registration is required if taxable turnover exceeds DKK 50,000; withholding tax may apply to certain payments to the parent depending on applicable tax treaties.

- Treaty Access: The branch itself does not independently access tax treaties; treaty entitlement depends on the parent company's jurisdiction of residence.

- Economic Substance: The branch must conduct genuine business activity in Denmark; a purely administrative presence risks being reclassified or denied treaty benefits.

- Annual Compliance: Audited financial statements must be filed annually; the branch is also subject to Danish bookkeeping requirements under Bogføringsloven.

- Closure: Deregistration requires formal application to Erhvervsstyrelsen and clearance of all outstanding liabilities.

Closing Paragraph

A Filial suits foreign companies testing the Danish market or executing a defined project without committing to full local incorporation. The primary advantage is operational speed — no share capital is required from the branch itself — but the key limitation is unlimited parent liability, which exposes the foreign firm's entire balance sheet to Danish creditors.

A Filial is best suited for established foreign companies with strong balance sheets that need an operational footprint in Denmark without creating a separate subsidiary.

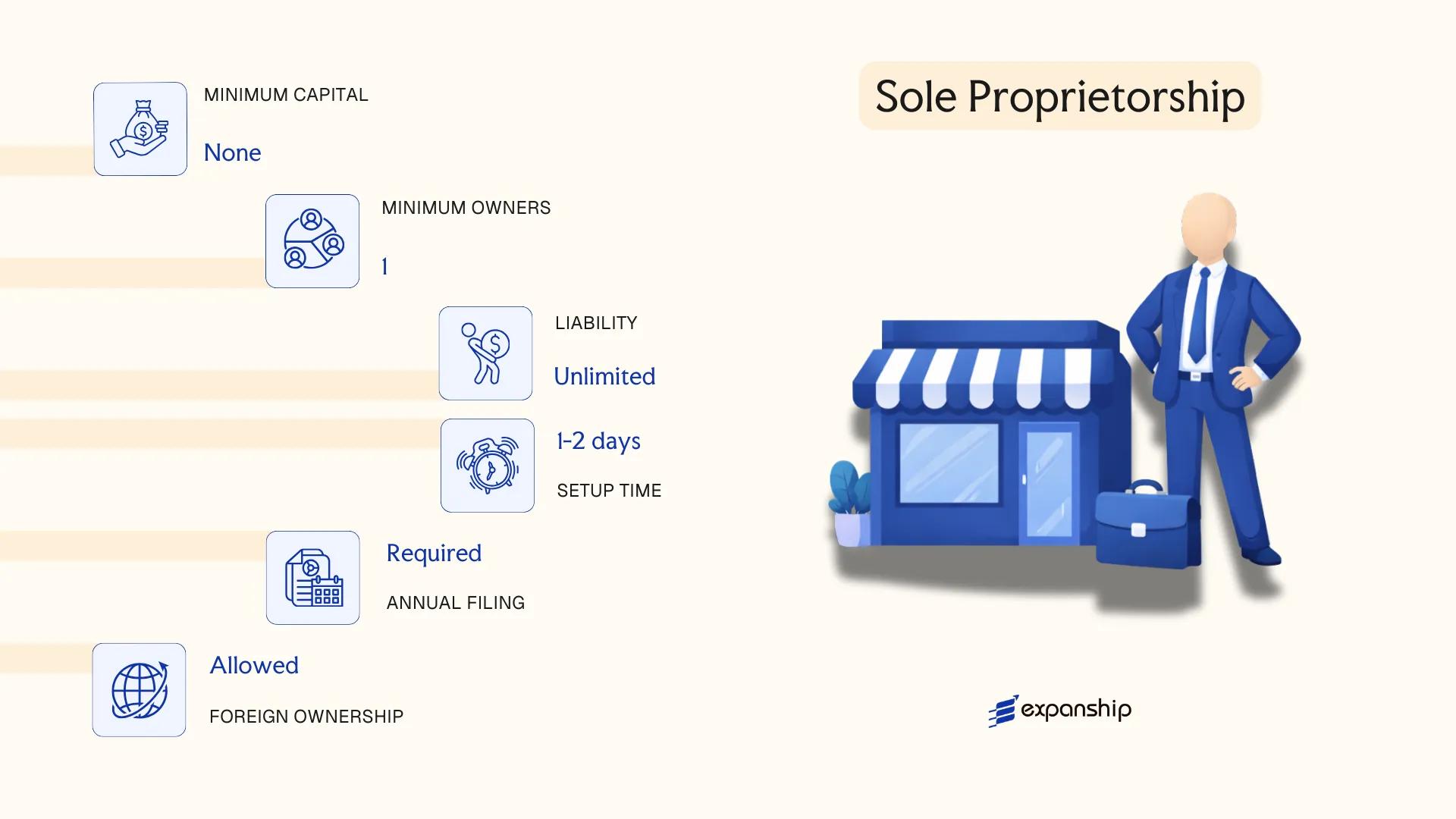

Sole Proprietorship (Enkeltmandsvirksomhed)

The Denmark Enkeltmandsvirksomhed sole proprietorship is the simplest business form available under Danish law. It carries no separate legal personality — the owner and the business are treated as one legal unit.

Registration is handled through the Danish Business Authority (Erhvervsstyrelsen) via the CVR register, and is required once annual revenue exceeds DKK 50,000. Below that threshold, registration remains optional in most cases.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole Proprietorship | No separate legal personality from the owner |

| Members | One proprietor | Cannot have co-owners; single natural person only |

| Liability | Unlimited personal liability | Owner's private assets are fully exposed to business debts |

| Local Presence | Registered address in Denmark required | Must be a physical address, not a P.O. box |

| Capital | No minimum capital requirement | No paid-in capital needed to establish |

| Privacy | Owner's name and address on public CVR register | Full transparency by default |

Focus Points

- Taxation: Profits are taxed as personal income under the Danish Tax Assessment Act (Ligningsloven), with rates up to approximately 56%; VAT registration is mandatory once turnover exceeds DKK 50,000; no separate corporate tax applies.

- Annual compliance: Annual accounts are not publicly required, though personal tax returns must include business financials.

- Virksomhedsordningen: Proprietors may elect the business scheme (Virksomhedsordningen) to achieve partial tax deferral on retained profits.

- Conversion: Can be converted into an ApS, though this triggers a formal transfer of assets and associated costs.

- Treaty access: No access to double tax treaties as a separate entity; treaty benefits flow through the individual owner's personal tax position.

Closing

This structure suits freelancers, consultants, and small traders who prioritise low setup costs over liability protection. The absence of minimum capital and reduced administrative burden are clear operational advantages, but unlimited personal liability remains a significant exposure for any business carrying financial risk.

Individual professionals and small-scale sole traders in Denmark with limited financial risk and no immediate plans to bring in co-owners or external investors.

How to Choose the Right Entity Type in Denmark

Selecting how to structure your business in Denmark has direct legal and financial consequences that vary depending on your specific operational profile.

Why Your Entity Choice Matters

The structure you register shapes your obligations from day one. Concrete outcomes of a mismatched choice include:

- Registering a branch (Filial) when you intend to conduct independent commercial activity can result in the parent company bearing unlimited liability for Danish operations — contrary to the limited liability protections available under the Selskabsloven (Danish Companies Act).

- Choosing an entity without access to Denmark's tax treaty network means withholding tax reductions available under bilateral agreements cannot be claimed by your business.

- Selecting a structure that triggers mandatory audit requirements — which apply to A/S companies and larger ApS entities under the Danish Financial Statements Act (Årsregnskabsloven) — adds recurring compliance costs that may be disproportionate for a single-person consultancy.

- Forming an ApS or A/S when a foundation structure better suits long-term asset holding locks your firm into annual general meeting obligations and shareholder reporting that foundations are not subject to.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors (financial services, investment funds) each point toward a distinct legal form under Danish law.

- Ownership Structure: Single-owner operations may suit a sole proprietorship or ApS, while multi-party arrangements may require partnership deeds or a formal board under A/S rules.

- Tax Objectives: Your eligibility for Denmark's participation exemption, joint taxation regime, or treaty access depends on the entity type you select.

- Substance Capacity: If you cannot maintain genuine management and decision-making in Denmark, certain structures will trigger transfer pricing scrutiny or residency challenges by Skattestyrelsen (the Danish Tax Agency).

- Exit Strategy: Not all Danish entity types support conversion or redomiciliation — an ApS can be converted to an A/S under the Selskabsloven, but other transitions require full dissolution and re-registration.

- Disclosure Tolerance: Beneficial ownership information for most Danish entities is filed with the Danish Business Authority (Erhvervsstyrelsen) and is accessible through the CVR public register.

The full text of the Selskabsloven (Companies Act) is available on Retsinformation, Denmark's official legal database.

Compliance Services for Companies in Denmark

Ongoing compliance support for Danish entities, including annual reporting, beneficial ownership filings, and Erhvervsstyrelsen obligations.

Conclusion

Selecting the right structure is the first binding decision you make when incorporating a business in Denmark, and each entity type reviewed in this guide addresses a different operational or liability profile. The ApS remains the most registered business form in the country, favoured by founders who want limited liability without the capital and governance requirements of the A/S. The A/S suits larger enterprises with multiple shareholders or public capital ambitions. Partnerships such as the I/S and K/S serve professional practices and investment structures respectively, while the P/S combines partnership flexibility with share-based capital. Branch offices and representative offices give foreign firms a controlled entry point without incorporating a separate legal entity.

Registered under the Danish Business Authority and governed primarily by the Companies Act (Selskabsloven), Danish corporate law continues to align with EU directives. That ongoing harmonisation reinforces the jurisdiction's standing as a transparent, treaty-connected location for holding and operational structures alike.

How Expanship Can Assist You

Expanship's Denmark company formation services cover the full spectrum of business structures discussed in this blog — from registering a private limited company (ApS) with the Danish Business Authority (Erhvervsstyrelsen) to establishing a branch office (Filial) for a foreign parent entity. Every engagement is built around the specific requirements of your chosen structure, not a generic process applied uniformly.

Across each engagement, the scope of support includes:

- Document preparation and notarization

- Registered address and local agent provision

- Filing with Erhvervsstyrelsen and CVR registration

- Post-incorporation compliance management, including annual reporting obligations

- Banking introduction assistance with local and international institutions

- Ongoing registered office maintenance

Ready to move forward? Contact Expanship Denmark to discuss your specific requirements.

Frequently Asked Questions (FAQ)

The Anpartsselskab (ApS) is the most frequently incorporated business form in the country. Its relatively low minimum capital requirement of DKK 40,000 and single-shareholder eligibility make it accessible for a wide range of founders.

Both structures are subject to Danish corporate tax at 22%, but the A/S carries stricter disclosure and governance requirements, including mandatory audits above certain thresholds and a minimum share capital of DKK 400,000. An ApS is generally suited for closely held firms, while the A/S is structured for entities seeking external investment or stock exchange listing.

A Kommanditselskab (K/S) does not require disclosure of limited partners in the same manner as shareholder registers for capital companies. Nominee arrangements are legally permissible in Denmark, though beneficial ownership must still be reported to the Erhvervsstyrelsen under anti-money laundering regulations.

A sole proprietorship and an ApS can each be formed by one individual. Partnerships — the Interessentskab (I/S), Kommanditselskab (K/S), and Partnerselskab (P/S) — each require at least two partners by definition.

All major entity types, including the ApS, A/S, and branch office (Filial), are accessible to foreign nationals. There is no Danish residency requirement for shareholders, though a registered address in Denmark is mandatory for the entity itself, and at least one member of the board of directors must be reachable for regulatory correspondence.

The Selskabsloven permits transformation between certain capital company forms, most commonly from ApS to A/S, provided the requirements of the target structure are met. Conversion from a partnership to a capital company follows a separate continuation procedure and generally requires a formal valuation of contributed assets.

Capital companies — the ApS, A/S, and IVS (though no longer available for new registration) — hold separate legal personality distinct from their owners. The Interessentskab (I/S) does not; partners bear joint and unlimited personal liability for obligations of the firm.

A sole proprietorship (Enkeltmandsvirksomhed) has minimal statutory reporting requirements relative to capital companies, though the owner assumes unlimited personal liability. Among corporate structures, a small ApS below the audit exemption thresholds under the Danish Financial Statements Act (Årsregnskabsloven) carries lighter ongoing obligations than a publicly listed A/S.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.