Key Takeaways

- The S.A.S., governed by Law 1258 of 2008, is Colombia's most widely registered entity type due to its flexibility and eligibility for single-shareholder formation.

- Colombian resident companies are subject to worldwide income taxation administered by the DIAN, while foreign entities such as branch offices are taxed only on Colombian-source income.

- Partnerships such as the Sociedad Colectiva and Sociedad en Comandita Simple expose at least some partners to unlimited personal liability, limiting their practical use to narrow professional arrangements.

- All primary business structures in Colombia must be registered with the Cámara de Comercio and fall under the supervisory authority of the Superintendencia de Sociedades for ongoing corporate governance and compliance.

Introduction to Entity Types in Colombia

Colombia sits in the northwestern corner of South America, sharing borders with Venezuela, Brazil, Peru, Ecuador, and Panama. It is an independent republic and one of the region's larger economies, operating under a legal framework that draws heavily from continental civil law traditions.

Company registration falls under the jurisdiction of the Cámara de Comercio (Chamber of Commerce), with the Superintendencia de Sociedades overseeing corporate governance and compliance for most business structures. The national tax authority, the DIAN (Dirección de Impuestos y Aduanas Nacionales), administers a territorial-based tax system under which resident companies are taxed on worldwide income, while foreign entities are generally taxed only on Colombian-source income.

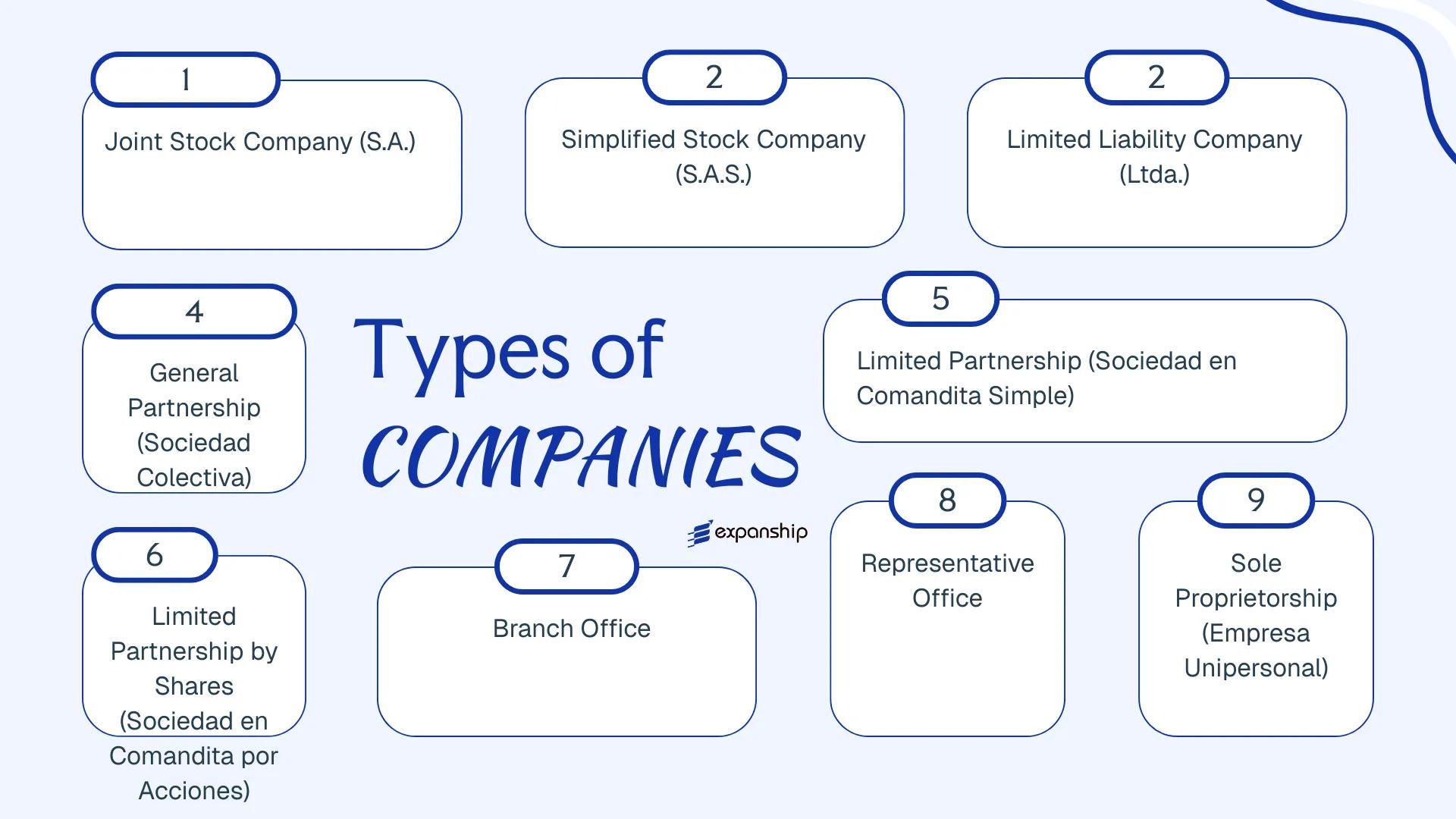

The types of business entities in Colombia available to both domestic and foreign investors include the Sociedad Anónima (S.A.), Sociedad por Acciones Simplificada (S.A.S.), Sociedad de Responsabilidad Limitada (Ltda.), Sociedad Colectiva, Sociedad en Comandita Simple, Sociedad en Comandita por Acciones, Branch Office, Representative Office, and Empresa Unipersonal. Each structure carries distinct requirements around capital, liability, governance, and registration. This article examines each option in detail to help you determine which form fits your operational and legal objectives.

An Overview of Business Structures in Colombia

Colombian company law recognises several distinct legal forms, each governed primarily by the Código de Comercio (Commercial Code) and, for the Sociedad por Acciones Simplificada, by Law 1258 of 2008. The Colombia business structures comparison below covers every major entity type available to domestic and foreign operators. Each form carries its own rules on liability, governance, membership, and taxation, reflecting different commercial purposes and scales of operation.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Sociedad Anónima (S.A.) | Corporation | Limited to shares | Taxed | Yes | 5 shareholders | Superintendencia de Sociedades | Código de Comercio |

| Sociedad por Acciones Simplificada (S.A.S.) | Simplified shares corp. | Limited to shares | Taxed | Yes | 1 shareholder | Superintendencia de Sociedades | Law 1258 of 2008 |

| Sociedad de Responsabilidad Limitada (Ltda.) | Limited liability co. | Limited to capital | Taxed | Yes | 2–25 partners | Superintendencia de Sociedades | Código de Comercio |

| Sociedad Colectiva | General partnership | Unlimited | Taxed | Yes | 2+ partners | Superintendencia de Sociedades | Código de Comercio |

| Sociedad en Comandita Simple | Limited partnership | Mixed | Taxed | Yes | 1 general + 1 limited | Superintendencia de Sociedades | Código de Comercio |

| Sociedad en Comandita por Acciones | Share-based cmd. partnership | Mixed | Taxed | Yes | 1 general + 5 limited | Superintendencia de Sociedades | Código de Comercio |

| Branch Office | Foreign branch | Parent liable | Taxed on local income | Yes | N/A | Superintendencia de Sociedades | Código de Comercio |

| Representative Office | Non-trading presence | Parent liable | Generally exempt | No | N/A | Superintendencia de Sociedades | Código de Comercio |

| Empresa Unipersonal | Sole proprietorship | Limited | Taxed | Yes | 1 owner | Cámara de Comercio | Law 222 of 1995 |

Each of these structures is examined in full in the sections below.

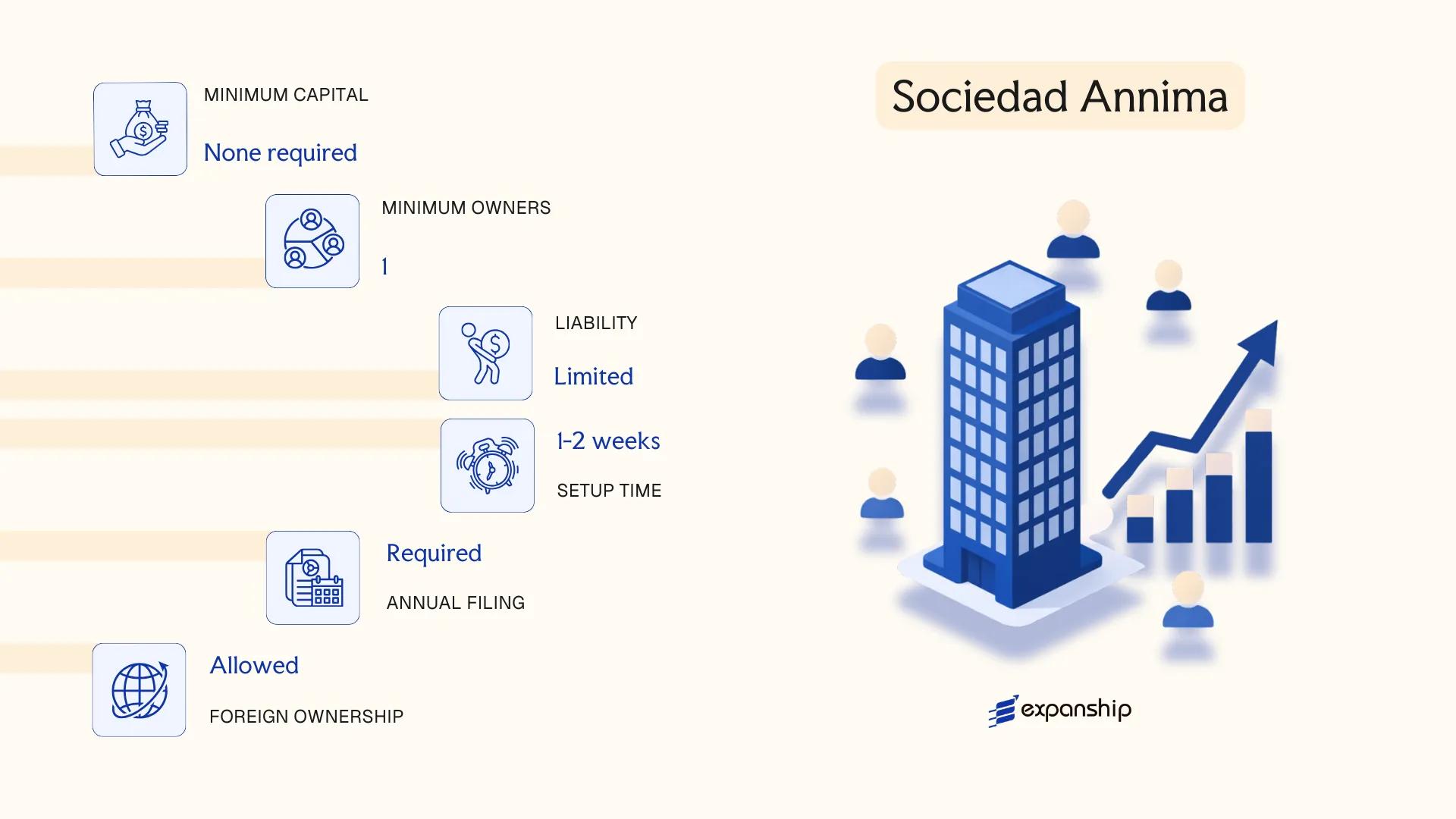

Sociedad Anónima (S.A.)

Sociedad Anónima SA Colombia formation is governed by the Código de Comercio (Commercial Code), specifically under Law 410 of 1971, which establishes the structural and operational requirements for this entity type. The S.A. carries full separate legal personality, meaning the company exists independently of its shareholders, and liability is limited to each shareholder's capital contribution.

Company Incorporation in Colombia

Incorporate your business in Colombia with expert guidance on entity selection, registration, and compliance.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedad Anónima (S.A.) | Regulated under the Código de Comercio, Law 410 of 1971 |

| Members | Minimum 5 shareholders; no statutory maximum | Members are referred to as shareholders (accionistas); shares are freely transferable unless restricted by bylaws |

| Management | Board of Directors (Junta Directiva) + Legal Representative | Board minimum 3 members; a statutory auditor (Revisor Fiscal) is mandatory |

| Local Presence | Registered address in Colombia required | A legal representative (who can be foreign) must be designated; no mandatory local director |

| Capital | No statutory minimum paid-in capital; denominated in COP | Capital divided into shares; at least 50% of subscribed capital must be paid at incorporation |

| Privacy | Shareholder information filed with the Cámara de Comercio | Beneficial ownership disclosures required under SAGRILAFT regulations |

Focus Points

- Taxation: Subject to corporate income tax at the standard rate (currently 35%); VAT applies to applicable goods and services; withholding tax obligations apply on payments to non-residents — see DIAN for current rates.

- Annual Compliance: Must hold an annual shareholders' meeting, file audited financial statements, and renew the Registro Mercantil with the Cámara de Comercio each year.

- Revisor Fiscal: A statutory auditor is mandatory for all S.A. entities, adding a layer of oversight not required in all other Colombian business forms.

- Treaty Access: As a Colombian tax resident entity, the S.A. has access to Colombia's network of double taxation agreements, including treaties with Spain, Canada, Chile, and others.

- Conversion: An S.A. can be converted to another legal form, such as an S.A.S., by a unanimous shareholder resolution and re-registration with the Cámara de Comercio.

Closing

The S.A. is commonly used for large-scale commercial operations, publicly oriented ventures, and businesses seeking to bring in institutional investors, given its structured governance and formal shareholder framework. The mandatory Revisor Fiscal and minimum five-shareholder threshold make it administratively heavier than more flexible alternatives available under Colombian law.

The S.A. is best suited for larger enterprises, joint ventures with institutional partners, or businesses that anticipate eventual public capital-raising activity.

Sociedad por Acciones Simplificada (S.A.S.)

Introduced under Law 1258 of 2008, the Sociedad por Acciones Simplificada SAS Colombia is a hybrid corporate structure that combines the flexibility of a partnership with the liability protection of a corporation. It holds separate legal personality, meaning the entity's obligations are distinct from those of its shareholders.

Shareholders bear liability only to the extent of their capital contributions. This structure is widely used for SAS company registration Colombia due to its minimal formation requirements and adaptable governance framework, which can be tailored through the company's bylaws rather than defaulting to rigid statutory rules.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Simplified Shares Company | Governed by Law 1258 of 2008 |

| Members | 1 or more shareholders (no maximum) | Referred to as accionistas; single-member formation is permitted |

| Local Presence | Registered address in Colombia required | No mandatory local director; a legal representative must be appointed |

| Capital | No minimum capital requirement; denominated in Colombian Pesos (COP) | Shares can be of different classes with varying rights |

| Share Transfers | Restrictions can be imposed via bylaws for up to 10 years | Shares are not publicly tradable on a stock exchange |

| Privacy | Shareholder information filed with the Cámara de Comercio | Beneficial ownership disclosures required under SAGRILAFT regulations |

Focus Points

- Taxation: Subject to corporate income tax (currently 35%), VAT at 19% on applicable transactions, industry and commerce tax (ICA) at municipal level, and withholding tax obligations on payments to non-residents; no stamp duty on share transfers in most cases.

- Annual Compliance: Must file annual financial statements with the Cámara de Comercio and renew the business registration (matrícula mercantil) each year.

- Economic Substance: No formal economic substance test, but the entity must maintain a registered address and appointed legal representative in-country.

- Treaty Access: Eligible to access Colombia's tax treaties as a resident entity, provided it meets residency criteria under domestic law.

- Conversion: An S.A.S. can be converted into another corporate form, but cannot be converted through a merger or spin-off that results in a different entity type without shareholder approval per Law 1258.

Closing

The S.A.S. suits trading operations, holding structures, and early-stage ventures where governance flexibility and low setup costs matter. Its primary advantage is the ability to customise share classes and management structures in the founding document, while its main limitation is the restriction on public share offerings, which prevents access to equity capital markets.

Best suited for foreign investors, startups, and SMEs seeking a cost-effective, flexible corporate vehicle without the governance complexity of a traditional S.A.

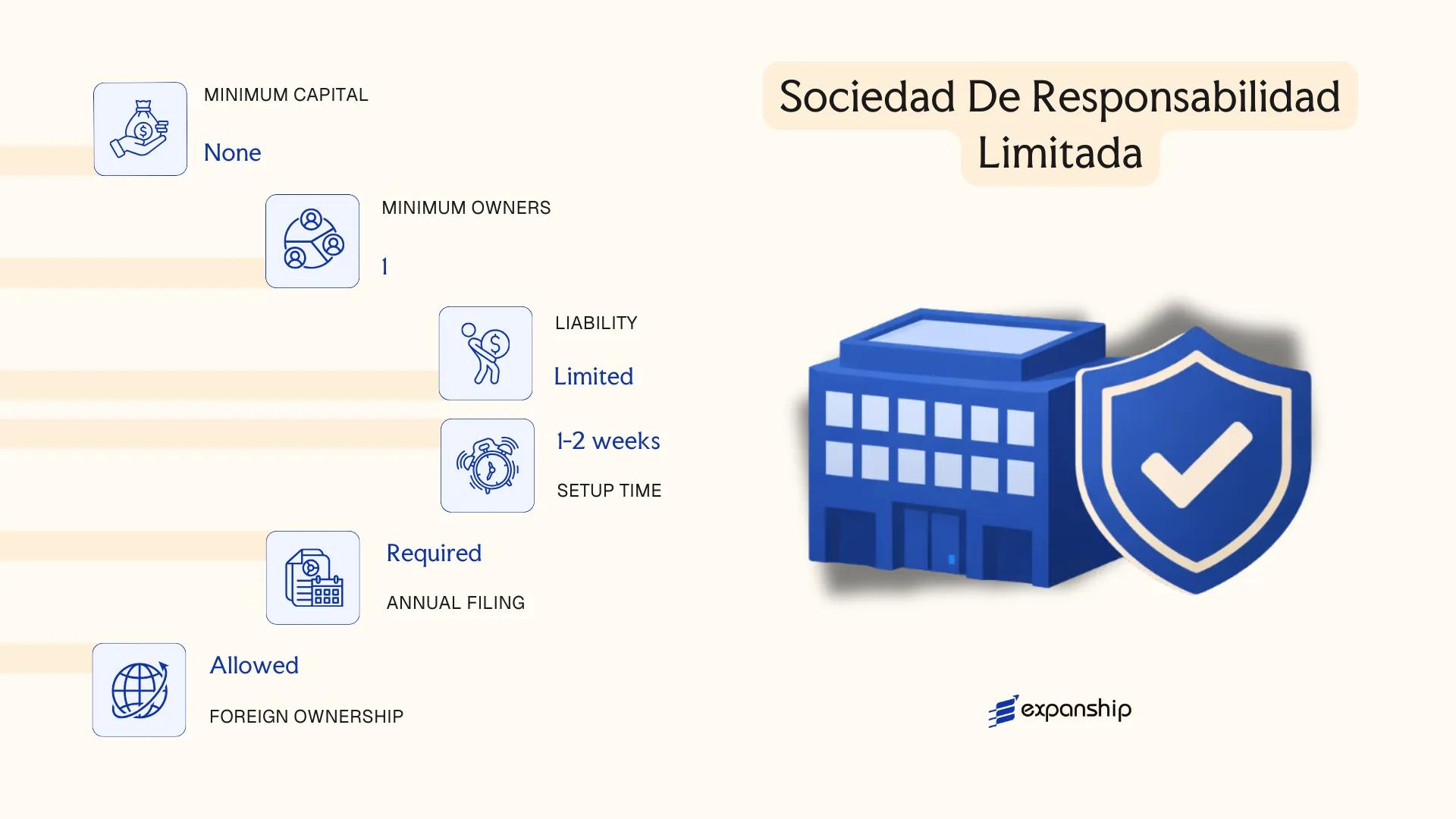

Sociedad de Responsabilidad Limitada (Ltda.)

The Sociedad de Responsabilidad Limitada (Ltda.) in Colombia is governed by the Código de Comercio (Commercial Code), specifically Articles 353 to 372. It carries separate legal personality from its members and limits each member's liability to the value of their capital contribution.

Structurally, the Ltda. occupies a middle ground between a closely held private firm and a more formally governed entity. Ownership is divided into cuotas (quotas) rather than shares, and the transfer of these quotas requires the consent of other members, making it a structure suited to businesses that prefer controlled ownership.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedad de Responsabilidad Limitada | Registered with the Cámara de Comercio; acquires legal personality upon registration |

| Members | Referred to as "socios" (partners/members); minimum 2, maximum 25 | Exceeding 25 members triggers mandatory conversion to an S.A. or S.A.S. |

| Capital Structure | Divided into cuotas (quotas); no minimum capital prescribed by law | All cuotas must be fully paid at the time of incorporation |

| Local Presence | Registered address in Colombia required; no mandatory resident director | A legal representative (representante legal) must be appointed |

| Privacy | Member names appear in the public registry at the Cámara de Comercio | No nominee quota-holder framework exists under Colombian law |

| Transfer Restrictions | Quota transfers require approval from other socios | Restriction must be included in or implied by the company's estatutos (bylaws) |

Focus Points

- Taxation: Subject to corporate income tax (currently 35%), VAT on applicable transactions, industry and commerce tax (ICA) at the municipal level, and withholding tax obligations as an agent of retention (agente retenedor).

- Annual Compliance: Must file annual financial statements, renew the Cámara de Comercio registration, and submit tax returns to the DIAN (Dirección de Impuestos y Aduanas Nacionales).

- Member Cap Restriction: The 25-member ceiling is a hard statutory limit; any breach requires conversion to another entity form.

- Treaty Access: As a Colombian tax resident entity, the Ltda. can access Colombia's network of double tax treaties, subject to beneficial ownership requirements.

- Conversion: Can be converted to an S.A.S. or S.A. by unanimous member agreement and re-registration with the Cámara de Comercio.

Closing

The Colombian Ltda. suits small to medium-sized closely held businesses, family enterprises, and joint ventures where ownership stability is a priority. Its quota structure gives members meaningful control over who can enter the business, though the 25-member ceiling limits its scalability for firms anticipating significant equity expansion.

Small to mid-sized closely held businesses or family ventures where controlled ownership and limited personal liability are the primary requirements.

Partnerships [Sociedad Colectiva, Sociedad en Comandita Simple, Sociedad en Comandita por Acciones]

Partnership structures in Colombia — Sociedad Colectiva, Sociedad en Comandita Simple, and Sociedad en Comandita por Acciones — are governed by the Código de Comercio (Commercial Code, Decree 410 of 1971). Each form carries distinct liability profiles, making the choice between them a substantive legal decision rather than a procedural one.

All three structures hold separate legal personality once registered with the Cámara de Comercio. The Sociedad Colectiva imposes unlimited personal liability on all partners, while the two comandita forms introduce a split between general partners (socios gestores) who bear unlimited liability and limited partners (socios comanditarios) whose exposure is capped at their contributed capital.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Partnership (Sociedad Colectiva / Sociedad en Comandita Simple / Sociedad en Comandita por Acciones) | All three require public deed and Cámara de Comercio registration |

| Members | Socios (partners); gestores (managing/general) and comanditarios (limited) in comandita forms | Sociedad Colectiva: min. 2, no statutory maximum; Comandita forms: min. 1 gestor + 1 comanditario |

| Local Presence | Registered address in Colombia required; no statutory resident partner requirement for all forms | A legal representative (representante legal) must be designated |

| Capital | No statutory minimum capital in COP for any of the three forms | Sociedad en Comandita por Acciones divides comanditario capital into shares (acciones) |

| Liability | Socios colectivos and gestores: unlimited personal liability; comanditarios: limited to capital contribution | Gestores in comandita forms cannot limit their liability by agreement |

| Privacy | Partner names and capital contributions are disclosed in the public deed | Registry filings are publicly searchable via the Registro Mercantil |

Focus Points

- Taxation: Corporate income tax applies at the standard rate (currently 35%); the entity is subject to VAT obligations where applicable, and profit distributions to foreign partners attract a withholding tax under domestic rules, subject to any applicable double tax treaty.

- Annual Compliance: Entities must file annual financial statements, renew their Cámara de Comercio registration, and submit tax returns to the DIAN.

- Treaty Access: Access to Colombia's tax treaty network depends on the entity's tax residency status and structure; comandita forms are generally treated as opaque entities for this purpose.

- Restrictions: Socios gestores are personally liable for partnership debts and cannot transfer their interest without consent of all other partners unless the deed provides otherwise.

Sub-Types

Sociedad Colectiva

All partners act as socios colectivos, each bearing joint and unlimited liability for the firm's obligations. This structure is rarely used for active commercial operations due to the unrestricted personal exposure it places on every member.

Sociedad en Comandita Simple

Capital contributions from comanditarios are not divided into transferable shares, keeping the structure relatively private and closely held. It is used in family-owned or closely controlled businesses where a managing partner wants operational control.

Sociedad en Comandita por Acciones

The comanditario's capital is divided into shares (acciones), which can be transferred more freely than interests in the Comandita Simple. This form suits ventures that anticipate bringing in passive investors while retaining a single active managing partner with full control.

Closing

Partnership structures suit scenarios where a defined managing partner needs operational authority alongside passive capital contributors, such as family enterprises or investment vehicles with a designated operator. The comandita por acciones offers greater capital flexibility than its simpler counterpart, though the unlimited liability of socios gestores remains a material limitation across all three forms.

These structures are best suited for closely held businesses or family ventures where at least one party is willing to accept personal liability in exchange for full management control.

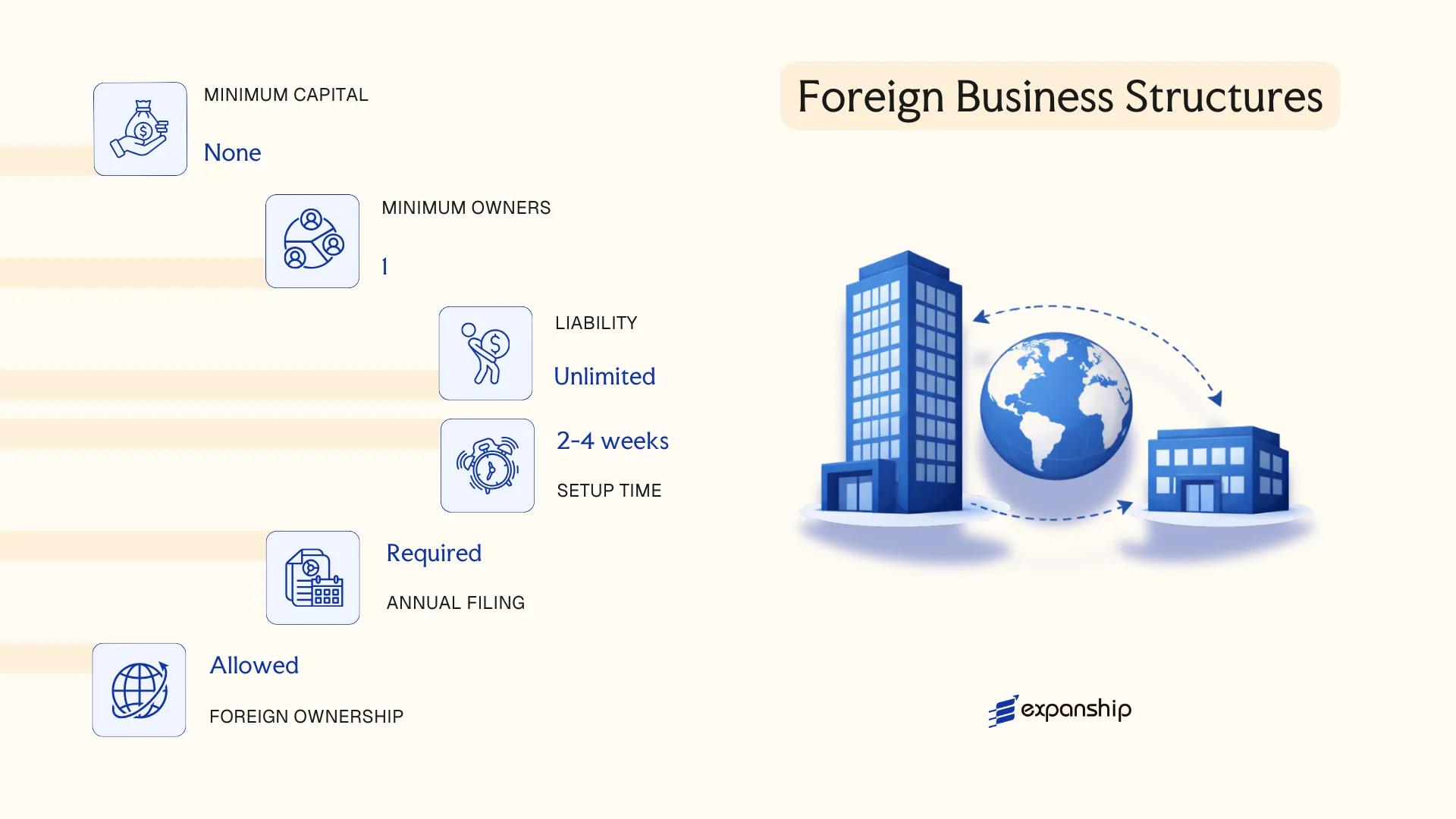

Foreign Business Structures [Branch Office, Representative Office]

Foreign companies seeking to operate in Colombia without incorporating a new local entity have two principal structural options: a branch office (sucursal de sociedad extranjera) and a representative office (oficina de representación). Both are governed by the Colombian Commercial Code and regulated by the Superintendencia de Sociedades or the relevant Chamber of Commerce, depending on the activity.

A foreign branch office Colombia registration does not create a separate legal entity — the parent company remains fully liable for the branch's obligations in Colombia. Registration is formalized through a public deed before a Colombian notary and must be filed with the Chamber of Commerce in the jurisdiction where the branch will operate.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Form | Extension of foreign parent; no separate legal personality | Extension of foreign parent; no separate legal personality |

| Representative | Appointed legal representative (apoderado) domiciled in Colombia | Appointed legal representative domiciled in Colombia |

| Permitted Activities | Full commercial operations, contracts, revenue generation | Limited to promotional, liaison, and market research activities |

| Capital Assignment | Assigned capital (capital asignado) required; no statutory minimum, but must reflect actual operations | No capital assignment required |

| Local Presence | Registered address in Colombia; legal representative required | Registered address; legal representative required |

| Privacy | Beneficial ownership details filed with SAGRILAFT where applicable | Same disclosure obligations apply |

Focus Points

- Taxation: Branch profits are subject to the standard corporate income tax rate (35%); a remittance tax (currently 20%) applies to after-tax profits transferred to the parent, in addition to VAT obligations on local supplies and withholding tax on applicable payments.

- Economic Substance: The branch must demonstrate genuine operational activity aligned with its registered purpose; representative offices are restricted from revenue-generating activity entirely.

- Annual Compliance: Both structures must file annual renewals with the Chamber of Commerce, submit financial statements, and comply with SAGRILAFT anti-money laundering obligations where thresholds are met.

- Treaty Access: Branches may access Colombia's double tax treaties as an extension of the foreign parent, subject to the specific treaty provisions and residency rules of the parent's home jurisdiction.

- Restrictions: Representative offices cannot sign commercial contracts, invoice clients, or generate local revenue — any such activity requires conversion to a branch or locally incorporated entity.

Sub-Types

Branch Office (Sucursal)

A sucursal is the only foreign branch structure permitted to conduct full commercial operations, execute contracts, and generate revenue locally. It is the standard choice for foreign companies establishing a billable operational presence without incorporating a separate Colombian subsidiary.

Representative Office (Oficina de Representación)

Distinct from a branch, this structure is confined to non-commercial activities such as market research, supplier coordination, and brand promotion. It carries no assigned capital requirement, making it administratively lighter, but its scope of permitted activity is significantly narrower.

Closing

Branch offices suit foreign companies that require direct operational control and revenue recognition in Colombia without the administrative overhead of a separate subsidiary, though the remittance tax on profit repatriation increases the effective tax burden compared to a locally incorporated entity.

Foreign companies testing the Colombian market or running regional operations under direct parent control, particularly where maintaining a single consolidated legal structure is a priority.

Sole Proprietorship [Empresa Unipersonal]

The Empresa Unipersonal Colombia sole proprietorship framework is governed by Law 222 of 1995, which established this structure as a distinct legal form for single-owner commercial activity. Upon registration with the Cámara de Comercio, the entity acquires a separate legal personality from its owner, meaning the business can hold assets, enter contracts, and incur liabilities in its own name.

Liability protection under this structure is limited to the capital assigned to the business at formation. However, Colombian courts have disregarded this separation where the proprietor has commingled personal and business assets — a risk that requires disciplined financial record-keeping.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Empresa Unipersonal (E.U.) | Separate legal personality; governed by Law 222 of 1995 |

| Members | Single proprietor | One natural or legal person; referred to as the proprietor |

| Local Presence | Registered address in Colombia | Must maintain a domicile registered with the Cámara de Comercio |

| Capital | No statutory minimum; denominated in COP | Capital must be stated in the formation document |

| Privacy | Proprietor's name and capital are publicly registered | Formation document filed in the public mercantile registry |

Focus Points

- Taxation: Subject to standard corporate income tax (currently 35%), VAT obligations where applicable, and industry and commerce tax (ICA) at the municipal level; withholding tax (retención en la fuente) applies to applicable transactions.

- Annual Compliance: Must renew the mercantile registration annually with the Cámara de Comercio and file financial statements as required by the Superintendencia de Sociedades thresholds.

- Conversion: Law 1258 of 2008 allows conversion to an S.A.S. without dissolution, making this a transitional structure for growing businesses.

- Restrictions: Cannot have more than one owner; admitting a second party requires conversion to a different entity type.

- Treaty Access: As a domestic entity, it is eligible for benefits under Colombia's double taxation agreements, subject to substance and residency requirements.

Closing

The Empresa Unipersonal suits small-scale trading operations or individual entrepreneurs who require legal separation from personal assets without the administrative overhead of a multi-member structure. Its primary limitation is the restriction to a single owner, which constrains capital-raising capacity and future equity participation.

Sole traders and individual entrepreneurs operating in Colombia who need a formal legal entity without partners or shareholders.

How to Choose the Right Entity Type in Colombia

Understanding how to choose a business entity type in Colombia requires more than comparing formation costs. The structure you select has direct legal, tax, and operational consequences that are difficult to reverse once the entity is registered with the Cámara de Comercio.

Why Your Entity Choice Matters

Selecting the wrong structure produces concrete, sometimes costly outcomes:

- Establishing a branch office when you intend to conduct independent commercial activity creates unlimited liability exposure for the foreign parent company, since branches do not form a separate legal entity under Colombian law.

- Registering an S.A. when your business qualifies for the simplified S.A.S. regime subjects you to statutory audit requirements and more rigid governance obligations under the Código de Comercio that do not apply to smaller S.A.S. companies below the audit thresholds.

- Choosing a Sociedad Colectiva when you need liability separation exposes all partners personally to the firm's debts without limit.

- Forming a capital-based entity when a sole proprietorship (Empresa Unipersonal) fits your operational scale adds annual governance costs that do not correspond to the actual size or complexity of the business.

Key Factors to Consider

- Business Activity: Active trading, asset holding, and regulated sectors such as financial services each point toward different structures, with regulated activities often requiring prior authorization from the Superintendencia Financiera de Colombia.

- Ownership Structure: A single founder operating independently suits the S.A.S. or Empresa Unipersonal, while multi-party ventures with differentiated share classes require the capital flexibility of an S.A. or S.A.S. with customized bylaws.

- Tax Objectives: Your eligibility for Colombia's tax treaty network, special free-trade zone regimes (Zonas Francas), or the preferential tax rates available to certain entities depends on the legal form you select.

- Liability Requirements: If personal asset protection is a priority, structures that maintain a clear separation between the shareholder and the entity — such as the S.A.S. or S.A. — are the appropriate starting point.

- Substance Capacity: If you cannot realistically maintain a physical presence, staff, or local decision-making, a representative office is legally prohibited from generating revenue, making that option unsuitable for operational businesses.

- Exit and Conversion: Not all Colombian entity types permit straightforward conversion; planning your exit or restructuring path at formation avoids the need for dissolution and re-registration later.

Compliance Services for Companies in Colombia

Maintain your Colombian entity in good standing with ongoing statutory, tax, and reporting obligations handled by local specialists.

Conclusion

Selecting the right structure is the first binding decision in any Colombia company incorporation summary — and the options are meaningfully distinct. The S.A.S. is the most registered entity in the country, favored for its statutory flexibility and single-shareholder eligibility under Law 1258 of 2008. The S.A. suits larger firms requiring public share issuance or regulated-sector licensing. An Ltda. works for closely held operations where member control takes priority over capital transferability. Partnerships carry unlimited liability exposure, making them a narrow fit for specific professional arrangements. A branch office serves foreign companies testing the market without separate legal personality.

Registered with the local Cámara de Comercio and supervised by the Superintendencia de Sociedades, Colombian corporate law continues to align with OECD standards following the country's accession process. Your formation choice shapes tax treatment, governance obligations, and exposure under that regulatory framework from day one.

How Expanship Can Assist You

Expanship provides corporate services Colombia company formation assistance covering the full range of entities discussed in this guide — from the S.A.S., which remains the most commonly incorporated structure, to branch offices registered through the Cámara de Comercio. Your obligations don't end at incorporation; Colombia's Superintendencia de Sociedades and DIAN impose ongoing compliance requirements that vary by entity type and shareholder structure.

From initial document preparation to post-incorporation filings, Expanship handles every stage of your Colombia business setup:

- Document preparation, notarization, and apostille legalization

- Government filing and liaison with the Cámara de Comercio

- Registered agent and registered address provision

- Post-incorporation compliance management, including annual reporting

- RUT registration coordination with DIAN

- Banking introduction assistance for corporate accounts

Reach out to Expanship Colombia to discuss your specific requirements.

Frequently Asked Questions (FAQ)

The Sociedad por Acciones Simplificada (S.A.S.) is the most frequently incorporated entity in the country, registered under Law 1258 of 2008. Its appeal stems from single-shareholder eligibility, no mandatory board structure, and flexible capital rules that reduce administrative overhead compared to older corporate forms.

Both are subject to standard Colombian corporate income tax, but the S.A. carries stricter governance mandates, including a statutory auditor (revisor fiscal) requirement once certain thresholds are met, and a minimum of five shareholders. An S.A.S. can be formed by one person, faces lighter ongoing disclosure obligations, and is not permitted to list shares on a public stock exchange.

Foreign nationals may form any of the main entity types, including an S.A.S., S.A., or Ltda., without residency requirements. However, at least one legal representative domiciled in Colombia must be appointed, and the entity must register with the relevant Cámara de Comercio. Branches of foreign companies require prior authorization from the Superintendencia de Sociedades or the relevant sectoral regulator.

No Colombian structure provides the equivalent of nominee shareholder arrangements found in some offshore jurisdictions. Shareholder information for all commercial entities is recorded in the public mercantile registry maintained by the Cámara de Comercio. The S.A.S. does not require public disclosure of internal governance documents beyond what is filed at registration, offering a modest degree of structural privacy relative to the S.A.

A sole proprietorship (Empresa Unipersonal) and an S.A.S. can each be formed by one individual. Partnerships, including the Sociedad Colectiva and Sociedad en Comandita Simple, require a minimum of two partners by definition, and some must have both general and limited partners as distinct roles.

Colombian corporate law allows entities to convert from one type to another through a formal transformation (transformación) procedure governed by the Código de Comercio. An S.A. may convert to an S.A.S., or a Ltda. may convert to an S.A., provided the transformation is approved by the required shareholder majority and registered with the Cámara de Comercio.

The S.A.S., S.A., Ltda., and both comandita forms have full separate legal personality under Colombian law. The Empresa Unipersonal also holds separate legal personality once registered, though it represents a single proprietor's commercial activity rather than a multi-party structure.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.