Key Takeaways

- China's corporate framework distinguishes sharply between domestic entities and foreign-invested enterprises, a division enforced through the Company Law of the People's Republic of China and administered by the State Administration for Market Regulation (SAMR).

- The Wholly Foreign-Owned Enterprise (WFOE) is the only structure that grants full foreign ownership and operational independence without requiring a domestic Chinese partner.

- Foreign investors seeking market or regulatory access may instead pursue a Sino-Foreign Equity Joint Venture, while those requiring flexible profit distribution arrangements can structure their presence as a Sino-Foreign Cooperative Joint Venture.

- Ongoing revisions to foreign investment catalogues and bilateral investment treaty commitments continue to shape which sectors are accessible to foreign capital and under what structural conditions.

Introduction to Entity Types in China

China sits in East Asia, sharing borders with 14 countries including Russia, India, and Vietnam, and spanning the world's third-largest landmass. As the world's second-largest economy by nominal GDP, it operates under a legal system that distinguishes sharply between domestic and foreign-invested entities — a distinction that directly affects how your business is structured, taxed, and regulated.

Company registration falls under the authority of the State Administration for Market Regulation (SAMR), which oversees business entity formation, modification, and deregistration at the national level, with provincial and municipal Market Supervision and Administration Bureaus handling local filings. The tax posture is territorial-based, with corporate income tax applied at a standard rate subject to preferential treatments depending on the entity type and industry.

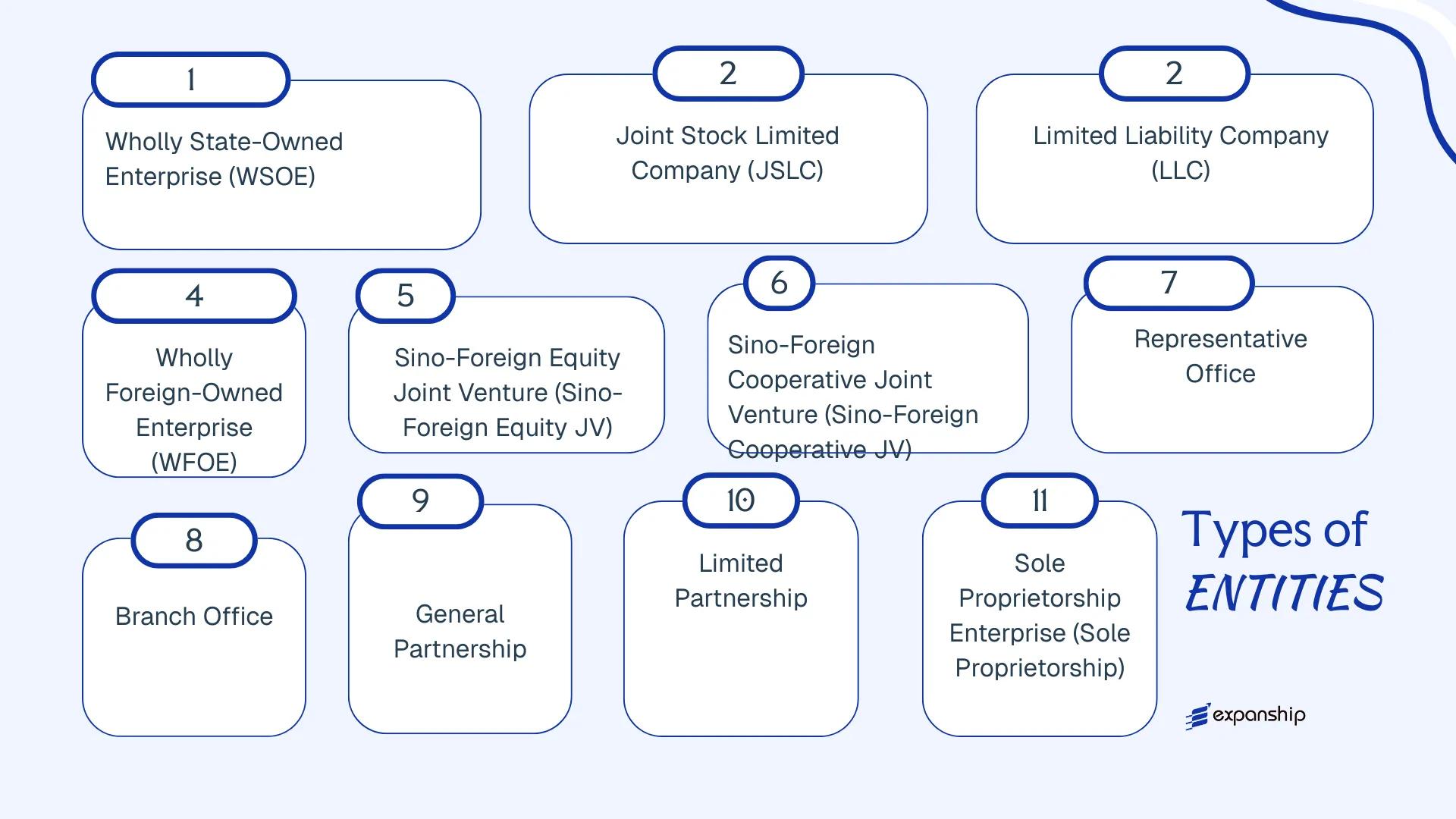

The types of business entities in China available to both domestic and foreign investors include:

- Wholly State-Owned Enterprise (WSOE)

- Joint Stock Limited Company (JSLC)

- Limited Liability Company (LLC)

- Foreign-Invested Enterprise (FIE) — encompassing Wholly Foreign-Owned Enterprises, Sino-Foreign Equity Joint Ventures, and Sino-Foreign Cooperative Joint Ventures

- Representative Office

- Branch Office

- General Partnership, Limited Partnership, and Special General Partnership

- Sole Proprietorship Enterprise

Each structure carries distinct capital requirements, liability rules, ownership restrictions, and compliance obligations, all of which this article examines in detail.

An Overview of Business Structures in China

Under China's current legal framework, foreign and domestic investors can choose from eight principal entity types, each governed primarily by the Company Law of the People's Republic of China (2023 revision), supplemented by the Partnership Enterprise Law, the Law on Wholly Foreign-Owned Enterprises, and related regulations administered by the State Administration for Market Regulation (SAMR). Each structure carries distinct implications for ownership, liability, taxation, and permitted commercial activity.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Tax Status | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Wholly State-Owned Enterprise (WSOE) | State-owned company | Limited | Taxable | Yes | State as sole shareholder | SAMR / State-owned Assets Supervision | Company Law 2023 |

| Joint Stock Limited Company (JSLC) | Share-based company | Limited | Taxable | Yes | 2+ promoters (no min. for listed) | SAMR / CSRC (if listed) | Company Law 2023 |

| Limited Liability Company (LLC) | Private company | Limited | Taxable | Yes | 1–50 shareholders | SAMR | Company Law 2023 |

| Wholly Foreign-Owned Enterprise (WFOE) | LLC variant | Limited | Taxable | Yes | 1 foreign shareholder | SAMR / MOFCOM | Foreign Investment Law 2020 |

| Sino-Foreign Equity Joint Venture | LLC or JSLC variant | Limited | Taxable | Yes | 1 foreign + 1 domestic | SAMR / MOFCOM | Foreign Investment Law 2020 |

| Sino-Foreign Cooperative Joint Venture | Contractual entity | Limited or unlimited | Taxable | Yes | 1 foreign + 1 domestic | SAMR / MOFCOM | Foreign Investment Law 2020 |

| Representative Office | Non-legal-person presence | Parent liable | Exempt from CIT on trading | No | N/A | SAMR / relevant authority | Administrative Regulations on ROs |

| Branch Office | Non-legal-person presence | Parent liable | Taxable | Restricted | N/A | SAMR | Company Law 2023 |

| General Partnership | Partnership | Unlimited | Pass-through | Yes | 2+ partners | SAMR | Partnership Enterprise Law 2006 |

| Limited Partnership | Partnership | Mixed | Pass-through | Yes | 2–50 partners | SAMR | Partnership Enterprise Law 2006 |

| Special General Partnership | Partnership | Mixed | Pass-through | Yes | 2+ partners | SAMR | Partnership Enterprise Law 2006 |

| Sole Proprietorship Enterprise | Unincorporated entity | Unlimited | Pass-through | Yes | 1 individual | SAMR | Sole Proprietorship Enterprise Law 1999 |

Each of these structures is examined in full in the sections below.

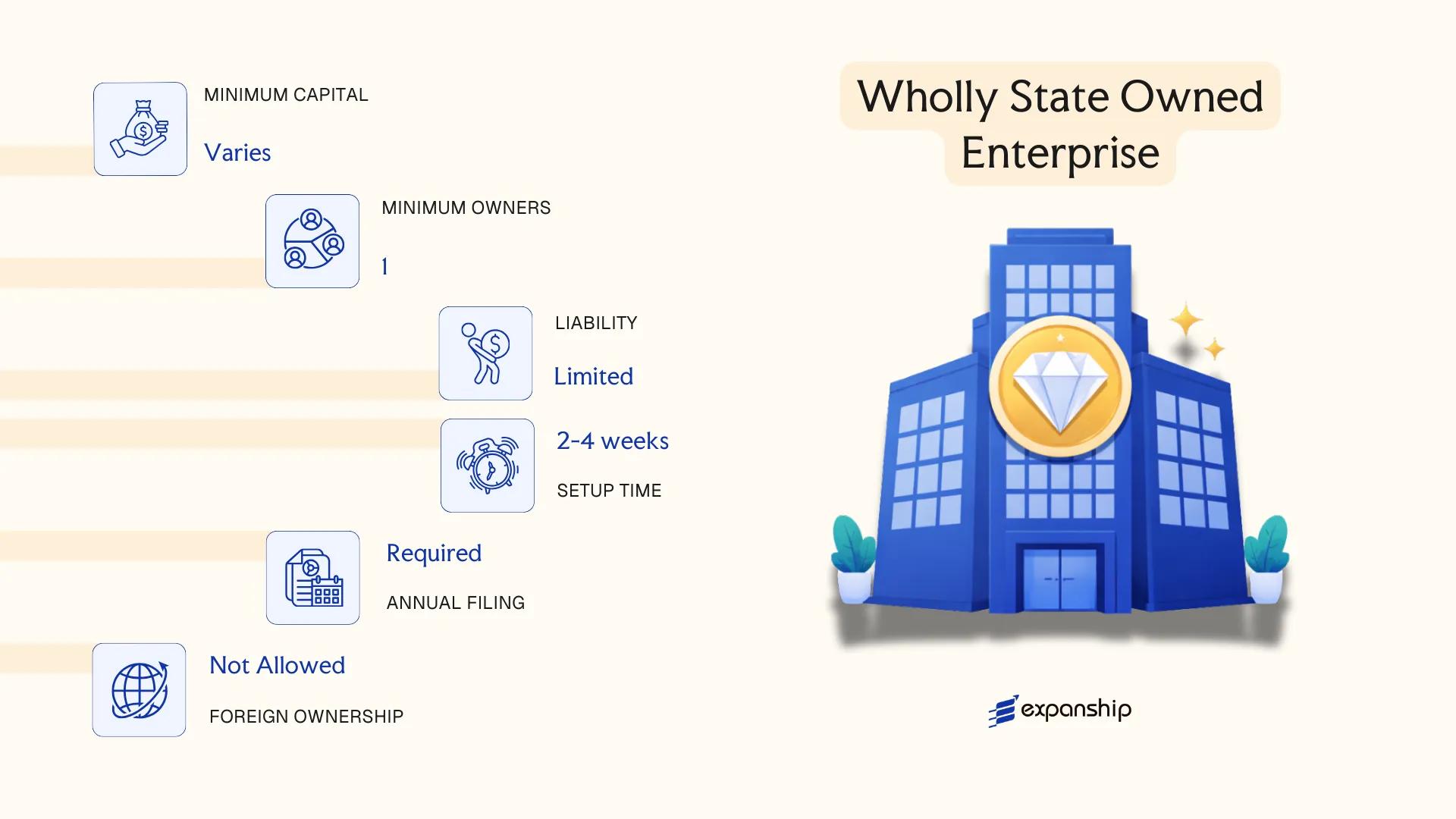

Wholly State-Owned Enterprise (WSOE)

A wholly state-owned enterprise China designates as a WSOE is a distinct corporate form governed primarily by the Company Law of the People's Republic of China (2023 revision) and the Law on State-Owned Assets of Enterprises (2008). Unlike a conventional limited liability company, this entity is funded entirely by the state, with the State Council or a local government acting as the sole investor.

The WSOE carries separate legal personality and benefits from limited liability, meaning the state's financial exposure is capped at its contributed capital. Oversight of state-owned assets and investor responsibilities is exercised through the State-owned Assets Supervision and Administration Commission (SASAC), which sits at both national and provincial levels.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited liability company (state-owned) | Structured as an LLC but with the state as sole investor |

| Governing Body | Board of Directors or Executive Director; Supervisory Board | Appointed by SASAC or the relevant government authority |

| Investor | Single investor: State (central or local government) | No private or foreign shareholders permitted |

| Registered Capital | No statutory minimum under the 2023 Company Law | Capital defined by the state's contribution commitment |

| Local Presence | Registered address within China required | Must maintain operational presence; nominee arrangements not applicable |

| Privacy | Ownership and financials subject to public disclosure and SASAC reporting | Limited confidentiality given state scrutiny |

Focus Points

- Taxation: Subject to Corporate Income Tax at the standard 25% rate; VAT applies to goods and services supplied; dividends paid to the state are not subject to withholding tax in the conventional sense, as profits are remitted to the state budget under a profit-sharing mechanism regulated by the Ministry of Finance.

- Annual Compliance: Annual financial statements must be audited and submitted to SASAC; filings with the State Administration for Market Regulation (SAMR) are required.

- Restrictions: Foreign investors cannot hold equity in a WSOE; the structure is reserved exclusively for state-funded operations.

- Conversion: A WSOE may be restructured into a joint stock limited company through a state-authorised reorganisation process, often preceding a public listing.

- Economic Substance: Full operational presence is expected; these entities cannot function as shell structures.

Closing

WSOEs are used for large-scale infrastructure, strategic industries, and state-mandated public services rather than private commercial ventures. The primary structural advantage is access to state credit and government support; the key limitation is that the form is entirely inaccessible to private or foreign investors.

WSOEs are suited only for government bodies or state agencies establishing or operating an enterprise with 100% public capital — private parties and foreign investors have no route into this structure.

Company Incorporation in China

Explore incorporation options available to foreign and domestic businesses across China's recognised legal structures.

Joint Stock Limited Company (JSLC /股份有限公司)

Governed by the Company Law of the People's Republic of China (amended 2023), the joint stock limited company China 股份有限公司 is a capital-based entity structure designed for larger enterprises seeking to raise equity from a broader investor base. It carries separate legal personality, meaning the company bears its own liabilities distinct from those of its shareholders.

Shares are freely transferable, subject to regulatory conditions, which distinguishes this structure fundamentally from a limited liability company. Shareholders bear liability only to the extent of their subscribed shares.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Joint Stock Limited Company | Separate legal personality; regulated under the 2023 Company Law |

| Members | Shareholders; minimum 2, maximum 200 (non-publicly listed) | Promoters must hold shares for a lock-up period post-incorporation |

| Directors & Supervisors | Board of Directors (5–19 members); Supervisory Board required | Listed companies must include independent directors |

| Capital | RMB; no statutory minimum under 2023 reforms for most structures | Paid-up capital commitments are recorded in the articles of association |

| Local Presence | Registered address in China mandatory | A domicile within the registered jurisdiction is required |

| Privacy | Shareholder and director details filed with SAMR; publicly searchable | Limited privacy; disclosure is a structural feature |

Focus Points

- Taxation: Subject to 25% Corporate Income Tax (standard rate); VAT applies to goods and services; dividends paid to foreign shareholders attract 10% withholding tax (reducible under applicable tax treaties); stamp duty applies on share transfers.

- Annual Compliance: Annual financial statements, audited accounts, and annual reports to the State Administration for Market Regulation (SAMR) and relevant securities regulators if listed.

- Treaty Access: Resident entities are eligible for benefits under China's extensive double taxation agreement network, subject to beneficial ownership requirements.

- Conversion: A JSLC may convert from an LLC through a formal restructuring process governed by the Company Law, requiring shareholder approval and regulatory filings.

- Listing Eligibility: Only this structure qualifies for domestic listing on the Shanghai Stock Exchange or Shenzhen Stock Exchange.

Sub-Types

Non-Listed Joint Stock Limited Company

Shares are held privately and not traded on a public exchange. This form is used by large private enterprises or pre-IPO companies that require a share-based capital structure without public market obligations.

Listed Company (上市公司)

Shares are publicly traded following approval by the China Securities Regulatory Commission (CSRC). Additional disclosure, governance, and ongoing reporting obligations apply under the Securities Law of the PRC.

When to Use This Structure

This structure suits large enterprises preparing for a public offering or requiring a transferable share-based framework to accommodate multiple institutional investors. The primary advantage is capital-raising capacity through equity issuance; the principal limitation is the high administrative and governance burden, making it unsuitable for small or mid-sized operations.

Best suited for large private enterprises with IPO ambitions or businesses requiring institutional equity participation across a broad shareholder base.

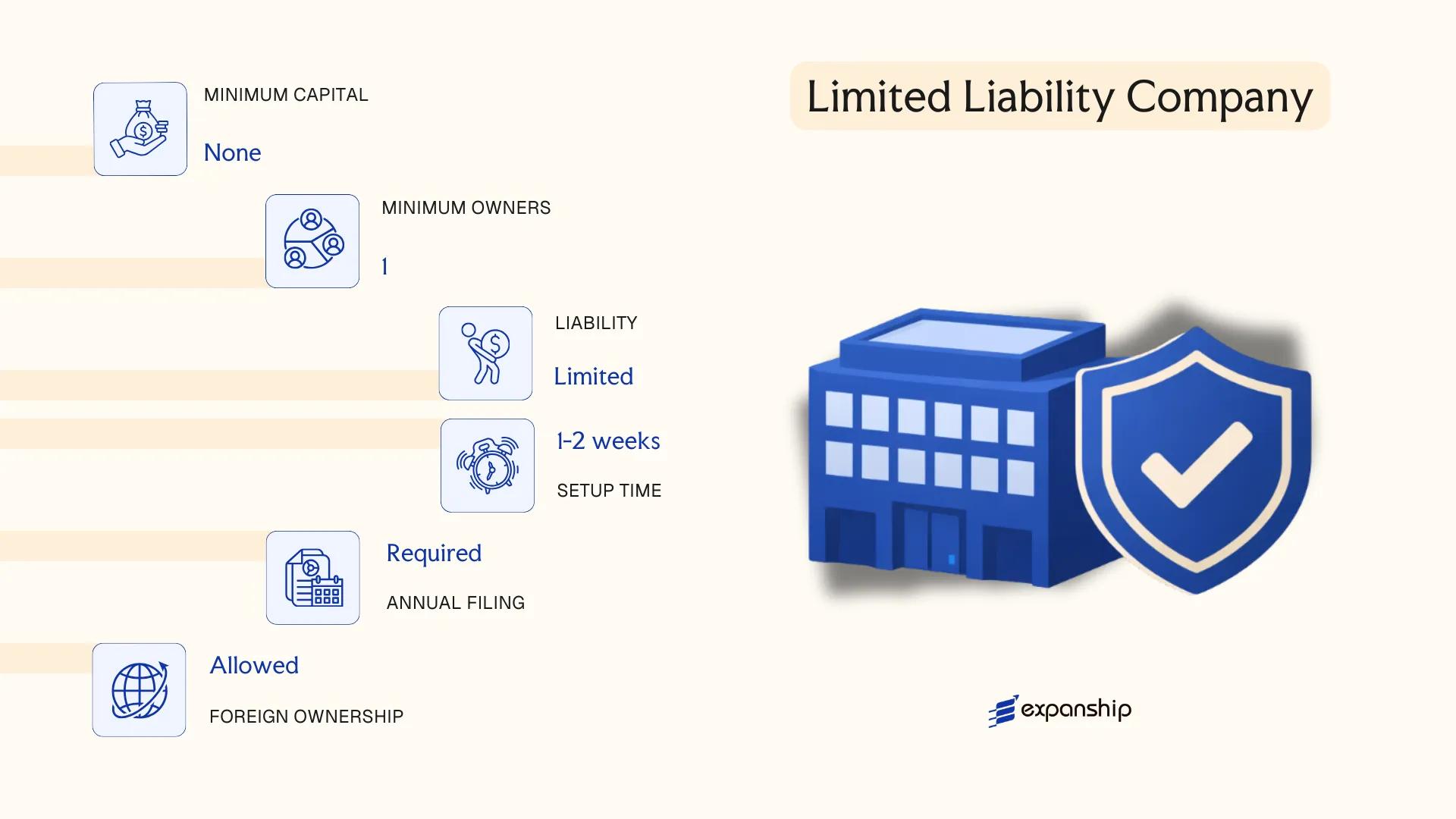

Limited Liability Company (LLC / 有限责任公司)

Governed by the Company Law of the People's Republic of China (first enacted in 1993, significantly revised in 2023), the limited liability company China 有限责任公司 represents the most widely adopted corporate structure for both domestic and foreign investors. The 2023 amendments introduced substantive changes to capital contribution rules, shareholder rights, and director liability.

As a separate legal entity, an LLC shields its shareholders from personal liability beyond their subscribed capital contributions. The structure sits between a sole proprietorship and a joint stock company, making it suited to businesses that require formal corporate standing without the public disclosure obligations of a listed entity.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Company (有限责任公司) | Separate legal personality; governed by Company Law 2023 |

| Members | Shareholders: 1–50 | Single-shareholder LLCs are permitted; shareholders hold equity interests, not shares |

| Management | Board of Directors or sole Executive Director; Supervisory Board or sole Supervisor | The 2023 revision allows small companies to appoint a single director and omit a supervisory board under certain conditions |

| Registered Capital | No statutory minimum (post-2013 reform); must be fully paid within 5 years of incorporation per 2023 amendments | Denominated in CNY; contributions may be cash or non-cash assets at agreed valuation |

| Local Presence | Registered address in China required; no mandatory resident director rule for domestic LLCs | Foreign-invested LLCs follow additional SAMR and MOFCOM registration requirements |

| Privacy | Shareholder names filed with SAMR and publicly accessible via the National Enterprise Credit Information Publicity System | Beneficial ownership disclosure obligations apply |

Focus Points

- Taxation: Subject to 25% Corporate Income Tax (standard rate); VAT applies at 6%, 9%, or 13% depending on activity; dividends paid to foreign shareholders attract 10% withholding tax (reducible under applicable tax treaties); stamp duty applies to capital contributions and certain contracts.

- Annual Compliance: Annual report submission to SAMR via the enterprise credit publicity system; statutory audit required; financial statements filed with tax authorities.

- Treaty Access: Resident in China for tax purposes; eligible for China's extensive double tax treaty network, subject to beneficial ownership and substance tests.

- Transfer Restrictions: Shareholder transfers to third parties require prior consent from the majority of other shareholders, who also hold a right of first refusal.

- Conversion: An LLC may convert to a Joint Stock Limited Company through a formal restructuring process under the Company Law, subject to regulatory approval.

Closing Paragraph

An LLC suits trading operations, wholly foreign-owned subsidiaries, domestic holding structures, and small-to-medium enterprises that require a formal legal entity without mandatory public share issuance. The capped shareholder number (50) limits its suitability for businesses anticipating a broad investor base or eventual public listing.

Best suited for foreign investors establishing a controlled operating or holding entity in China, and for domestic founders who want structural simplicity with defined liability protection.

Foreign-Invested Enterprise (FIE) [Wholly Foreign-Owned Enterprise (WFOE), Sino-Foreign Equity Joint Venture, Sino-Foreign Cooperative Joint Venture]

Governed primarily by the Foreign Investment Law of the People's Republic of China (2020) and its implementing regulations, a Foreign-Invested Enterprise is any business entity established in China where the investor is a foreign national or foreign-incorporated company. FIEs carry separate legal personality and, depending on their structural form, offer limited liability to their investors. A foreign-invested enterprise China WFOE setup falls under this overarching FIE framework.

Prior to 2020, FIEs were regulated under three separate laws specific to each sub-type. The unified Foreign Investment Law consolidated these into a single framework, aligning FIE governance with the Company Law of the People's Republic of China (2023 revision).

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited liability company or joint stock company | Structural form depends on sub-type chosen |

| Members | Shareholders; minimum 1, maximum 50 (LLC form) | Joint stock form allows broader shareholder base |

| Local Presence | Registered address within China mandatory | Virtual offices are generally not accepted |

| Capital | RMB-denominated; no statutory minimum in most sectors | Certain regulated industries impose sector-specific minimums |

| Foreign Ownership | Up to 100% permitted outside restricted sectors | Negative List defines restricted and prohibited industries |

| Privacy | Shareholder information filed with SAMR; publicly accessible | No nominee shareholder arrangements recognized |

Focus Points

- Taxation: Subject to 25% Corporate Income Tax (CIT); reduced 15% rate available in high-tech or encouraged sectors; 6% VAT applies to services; dividends remitted abroad attract a 10% withholding tax (reducible under tax treaties); stamp duty applies to capital contributions and contracts.

- Negative List: Foreign ownership restrictions are defined by the national and free-trade-zone Negative Lists, updated periodically by the NDRC and Ministry of Commerce (MOFCOM).

- Annual Compliance: Annual reporting via the National Enterprise Credit Information Publicity System is mandatory; failure to file results in inclusion on the abnormal operations list.

- Profit Repatriation: Foreign exchange controls administered by SAFE govern dividend remittance; documentation requirements are substantial.

- Conversion: An FIE may convert between sub-types, though conversion triggers regulatory re-registration with SAMR and potential MOFCOM filing.

Sub-Types

Wholly Foreign-Owned Enterprise (WFOE)

A WFOE is wholly foreign-invested enterprise China registration structure where no Chinese equity partner is required, giving the foreign investor complete operational and managerial control. It is the preferred structure for manufacturing operations, technology firms, and service businesses seeking to protect proprietary processes or intellectual property.

Sino-Foreign Equity Joint Venture (EJV)

In an EJV, the foreign and Chinese partners contribute capital and share profits, losses, and management responsibilities in direct proportion to their respective equity stakes. This structure is commonly used to access sectors where full foreign ownership remains restricted under the Negative List.

Sino-Foreign Cooperative Joint Venture (CJV)

A CJV allows more flexible profit-sharing and cost-recovery arrangements that need not mirror the equity ratio, with terms negotiated contractually between the parties. It is typically used in project-based industries such as natural resources, construction, and media, where cash flow timing and risk allocation matter more than proportional equity returns.

Recommendations

An FIE suits foreign businesses seeking a fully operational, revenue-generating presence in the Chinese market, with WFOEs offering the greatest ownership control and joint ventures providing market access in restricted sectors. The primary limitation across all FIE sub-types is the Negative List, which can restrict or entirely prohibit foreign participation in specific industries without a Chinese partner.

Foreign companies entering the Chinese market that require direct operational control, local invoicing capability, or access to sectors with partial foreign-ownership restrictions.

Foreign Business Presence [Representative Office, Branch Office]

A foreign company representative office in China offers an established route for overseas businesses to maintain a physical presence without incorporating a separate legal entity. Neither a representative office (RO) nor a branch office possesses independent legal personality — both operate as extensions of the parent company, which bears full legal and financial liability for their activities. Registration is governed by the Regulations on the Administration of Registration of Resident Representative Offices of Foreign Enterprises (2011) for ROs, while branch offices fall under the Company Law of the People's Republic of China (2023 revision).

Approved by the State Administration for Market Regulation (SAMR) and, in certain sectors, by industry-specific regulators, these structures suit businesses testing market entry or managing liaison functions before committing to full incorporation.

Key Characteristics

| Requirement | Representative Office | Branch Office |

|---|---|---|

| Legal Personality | None — extension of foreign parent | None — extension of foreign parent |

| Permitted Activities | Non-commercial liaison only (market research, promotion, coordination) | Commercial activities permitted within parent's business scope |

| Chief Representative / Head | At least one appointed Chief Representative | Designated person-in-charge required |

| Registration Authority | SAMR; sector regulators where applicable | SAMR |

| Registered Address | Physical office address required in China | Physical office address required |

| Validity Period | Renewed every 3 years | No fixed term; renewed annually |

Focus Points

- Taxation: ROs are taxed on a deemed-profit basis — typically 15% of expenses — with Enterprise Income Tax at 25% applied to that deemed profit; branch offices are taxed on actual profits at 25% EIT, plus VAT on applicable revenues.

- Scope Restrictions: ROs are prohibited from directly engaging in profit-generating business activities; any revenue-generating operations require a separate incorporated entity.

- Annual Compliance: Both structures must file annual inspection reports with SAMR; ROs are additionally subject to annual reporting to tax authorities based on their deemed-income calculations.

- Treaty Access: Neither structure provides independent access to double tax treaty benefits — treaty eligibility rests with the foreign parent entity.

- Conversion: An RO cannot be directly converted into a WFOE or other incorporated entity; the parent must separately register a new entity and wind down the RO.

Sub-Types

Representative Office

A Representative Office is strictly limited to non-commercial functions — coordinating with local suppliers, conducting market surveys, and facilitating communication between the foreign parent and Chinese counterparts. It cannot sign commercial contracts or invoice clients in its own name.

Branch Office

A Branch Office may conduct business activities consistent with the parent company's approved scope, making it operationally broader than an RO. Its use is more common in regulated sectors such as banking, insurance, and law, where specific sector regulators — including the National Financial Regulatory Administration (NFRA) — govern establishment.

Closing

Both structures are suited to foreign firms requiring a controlled, limited footprint — an RO for pre-market exploration, a branch for sector-specific commercial operations — though neither provides liability separation from the parent company.

Foreign companies seeking a non-committal market presence in China before committing to full incorporation, or those operating in regulated industries where branch licensing is sector-mandated.

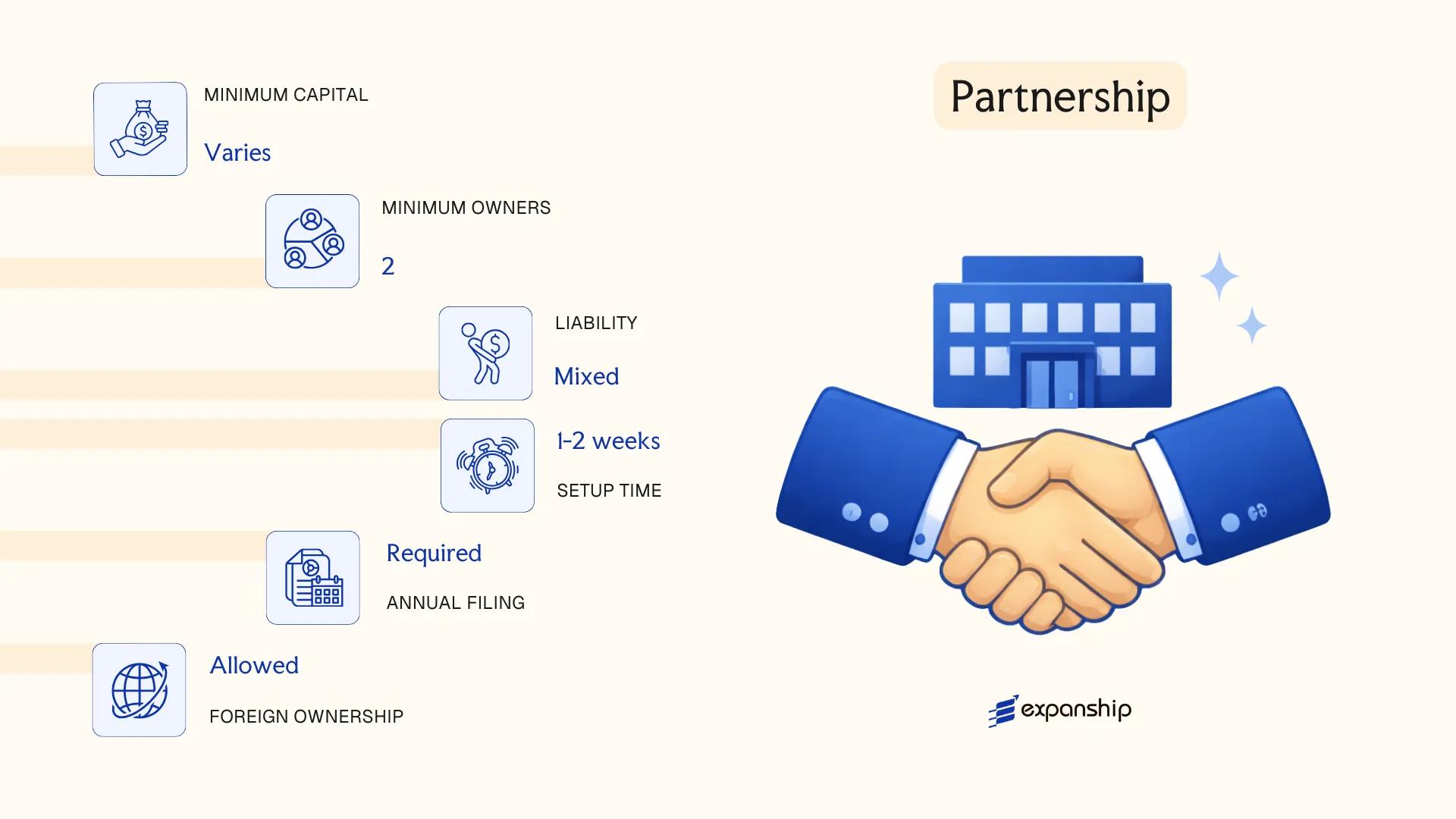

Partnership [General Partnership, Limited Partnership, Special General Partnership]

Governed by the Partnership Enterprise Law of the People's Republic of China (2006, amended 2007), partnerships in China do not possess separate legal personality. This distinguishes them structurally from limited liability companies and joint stock firms, where the entity itself bears legal responsibility distinct from its owners.

Limited partnership registration in China requires at least two partners, with one general partner assuming unlimited liability. All three partnership forms share the same governing statute, though each allocates liability and management rights differently.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Partnership Enterprise (非法人组织) | No separate legal personality; not a corporate entity |

| Members | Partners (合伙人) | GP: 2–50; LP: 2–50 (at least 1 GP and 1 LP); SGP: no statutory cap |

| Capital | No statutory minimum; contributions in cash, in-kind, or services | Agreed in the partnership agreement |

| Local Presence | Registered address required; no mandatory registered agent | Must register with local Administration for Market Regulation (AMR) |

| Privacy | Partner names disclosed on public register | Partnership agreement details not fully public |

Focus Points

- Taxation: Partnerships are fiscally transparent; partners pay Individual Income Tax or Corporate Income Tax on their respective share of profits — the entity itself is not subject to Enterprise Income Tax.

- Annual Compliance: Annual report filing required through the National Enterprise Credit Information Publicity System; financial statements not mandated to be audited at entity level.

- Treaty Access: As pass-through entities without legal personality, partnerships generally cannot independently access China's tax treaty network.

- Foreign Participation: Foreign investors face restrictions; foreign-invested partnerships are permitted under the 2010 Administrative Measures but subject to additional approval procedures.

- Conversion: Conversion between partnership types is possible under the Partnership Enterprise Law but requires partner consent and AMR re-registration.

Sub-Types

General Partnership (普通合伙企业)

All partners bear unlimited joint and several liability for partnership debts. This structure is typically used by domestic trading or professional service firms where all participants share management and full risk exposure.

Limited Partnership (有限合伙企业)

Comprises at least one general partner with unlimited liability and at least one limited partner whose liability is capped at their capital contribution. The limited partnership structure is widely used for private equity and venture capital funds in China, as it allows passive investors to participate without assuming operational risk.

Special General Partnership (特殊普通合伙企业)

Liability is partitioned by fault: a partner responsible for intentional misconduct or gross negligence bears unlimited personal liability, while other partners are shielded from that specific claim. Under Chinese law, this form is reserved exclusively for professional service organisations such as law firms and accounting practices.

Closing Paragraph

Partnerships suit professional services, fund structures, and domestic trading ventures where pass-through taxation outweighs the absence of liability protection. The fiscal transparency is a structural advantage, though the unlimited liability exposure of general partners remains a significant operational constraint.

Limited partnerships are best suited for private equity fund managers and venture capital structures seeking pass-through tax treatment with clearly separated investor and manager liability.

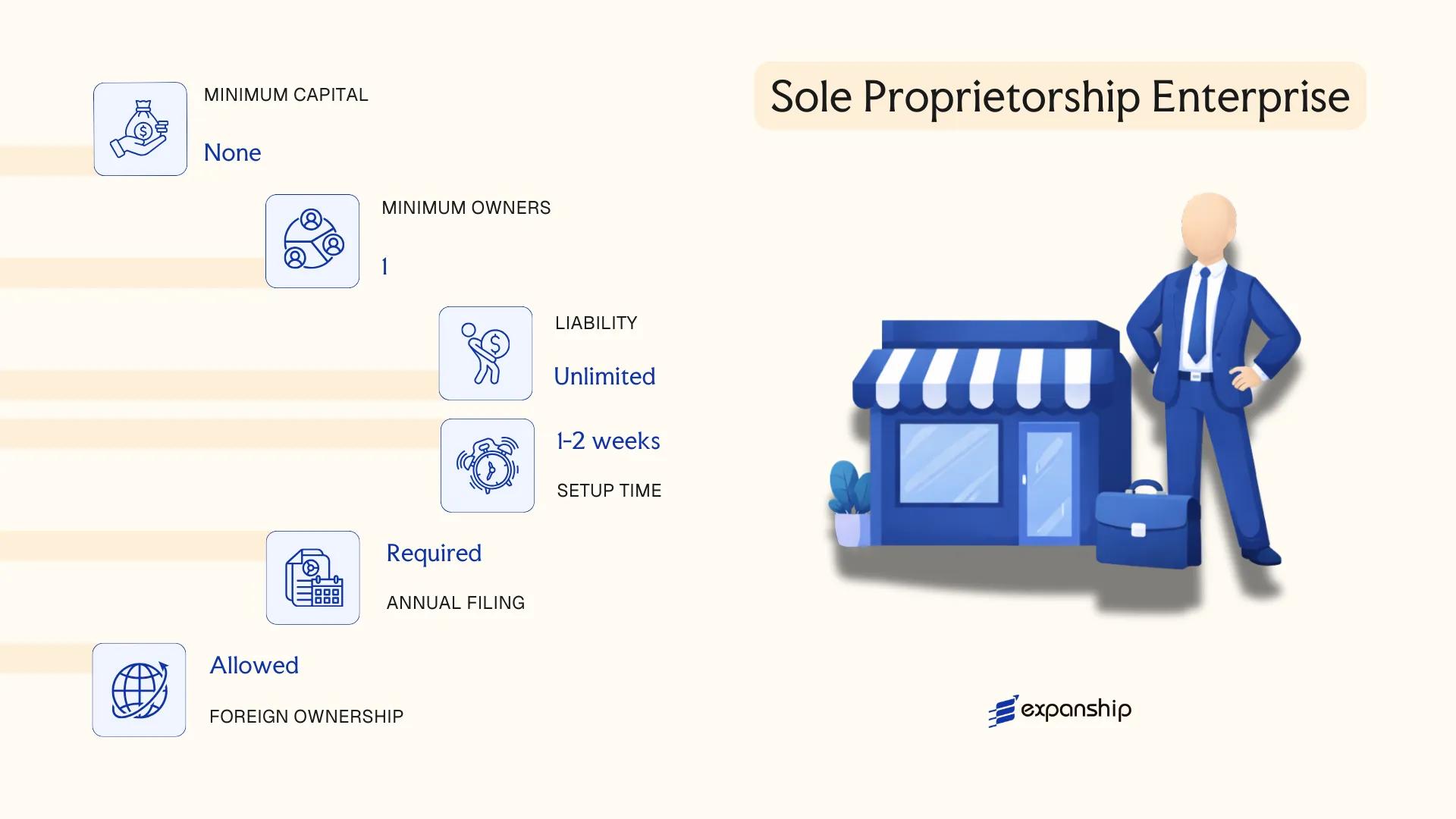

Sole Proprietorship Enterprise (个人独资企业)

Governed by the Law on Sole Proprietorship Enterprises (个人独资企业法), enacted in 1999 and effective from 1 January 2000, the sole proprietorship enterprise China 个人独资企业 is among the simplest legal forms available to individual investors. It is established and owned by a single natural person — Chinese or foreign resident — who invests personal assets and operates under their own name or a registered trade name.

Critically, this entity carries no separate legal personality. The proprietor and the business are treated as one legal subject, meaning personal assets are fully exposed to business liabilities. There is no limited liability protection of any kind.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated sole proprietorship | No separate legal personality; proprietor bears unlimited personal liability |

| Members | Single natural person (proprietor) | Must be an individual; corporations cannot establish this form |

| Registered Capital | No statutory minimum | Capital contribution is self-declared; no paid-up verification required |

| Local Presence | Registered address in China required | Must maintain a physical operating address within the registration locality |

| Privacy | Proprietor's name linked to the business in public records | Minimal separation between personal and business identity |

Focus Points

- Taxation: Subject to Individual Income Tax (IIT) on business income at progressive rates up to 35%; not subject to Corporate Income Tax. VAT applies based on turnover thresholds; no separate withholding tax layer on distributions.

- Annual Compliance: Annual reporting to the State Administration for Market Regulation (SAMR) via the National Enterprise Credit Information Publicity System is required.

- Treaty Access: As a non-corporate entity, it generally cannot access China's double tax treaty network for reduced withholding rates.

- Restrictions: Foreign nationals face practical restrictions — this form is not commonly approved for non-residents and is unavailable to legal persons.

- Dissolution: No formal liquidation procedure equivalent to a company wind-down; the proprietor settles debts directly using personal assets.

Closing

This structure suits small-scale, individually operated domestic businesses where administrative simplicity outweighs the need for liability protection. The absence of a minimum capital requirement reduces the setup burden, but unlimited personal liability makes it unsuitable for ventures carrying significant financial or operational risk.

Individual Chinese residents operating low-risk, small-scale service or trading businesses who prioritise minimal compliance overhead over personal asset protection.

How to Choose the Right Entity Type in China

Selecting the correct entity structure is a foundational decision that shapes your tax position, liability exposure, and operational permissions for the life of the business.

Why Your Entity Choice Matters

Choosing the wrong structure carries concrete legal and financial consequences:

- Registering a Representative Office when your activities constitute substantive business operations violates the scope restrictions under the Regulations on the Administration of Foreign-Invested Enterprises — exposing the entity to administrative penalties or forced closure.

- Forming a structure without legal person status means you cannot open dedicated corporate bank accounts or enter contracts as an independent entity, creating personal liability for the controlling party.

- Selecting a Wholly Foreign-Owned Enterprise in a sector listed on the Special Administrative Measures (Negative List) without obtaining prior approval results in registration refusal or post-incorporation revocation.

- Incorporating under a general partnership when your business involves multiple foreign investors in a regulated industry may disqualify the firm from obtaining the required operating licenses.

Key Factors to Consider

- Business Activity: Active trading, asset holding, and regulated-sector operations each require different structures under the Company Law of the People's Republic of China.

- Ownership Composition: A single foreign investor points toward a WFOE, while multi-party arrangements require either a joint venture structure or a joint stock framework.

- Sectoral Restrictions: Your intended industry must be cross-referenced against the current Negative List administered by the Ministry of Commerce (MOFCOM) before choosing a foreign-invested structure.

- Tax Objectives: Whether your business requires access to double taxation agreements, preferential Enterprise Income Tax rates, or High and New Technology Enterprise status affects which entity qualifies.

- Substance Capacity: If you cannot maintain a registered address, local staff, and operational decision-making within the jurisdiction, a Representative Office — with its limited permitted scope — may be the only viable foreign presence option.

- Exit and Restructuring: Not all entity types permit conversion; a Limited Liability Company can be restructured into a Joint Stock Limited Company under statutory conditions, but dissolution and re-registration may be required for other transitions.

Compliance Services for Companies in China

Ongoing compliance support for foreign-invested enterprises, LLCs, and other registered entities operating in China.

Conclusion

Selecting the right structure is one of the most consequential early decisions when incorporating a company in China. Each entity form carries a distinct legal character: the WFOE grants full foreign ownership and operational independence; the Equity Joint Venture suits foreign investors who require a domestic partner for market or regulatory access; the Cooperative Joint Venture offers contractual flexibility over profit distribution; and the LLC remains the most widely registered structure for both domestic and foreign-invested businesses. Partnerships serve professional services firms and fund vehicles, while the Sole Proprietorship is confined to individual operators under unlimited liability.

Registered under the Company Law of the People's Republic of China and supervised by the State Administration for Market Regulation (SAMR), the corporate framework continues to evolve, with ongoing revisions to foreign investment catalogues and bilateral investment treaty commitments shaping how external capital can be deployed across sectors. Your choice of entity will determine tax treatment, governance requirements, and exit options from the outset.

How Expanship Can Assist You

Expanship's China company incorporation services are built around the specific requirements of the State Administration for Market Regulation (SAMR), the authority responsible for registering entities ranging from WFOEs and Sino-Foreign Joint Ventures to domestic LLCs and partnerships. Your chosen structure determines which approvals, capital thresholds, and ongoing filings apply — and our team works through those requirements with you directly.

From initial documentation through to post-registration obligations, our service scope covers the full formation and maintenance cycle:

- Document preparation, notarization, and legalization

- Registered address and resident agent provision

- SAMR filing and government authority liaison

- Business license processing and company chop arrangements

- Post-incorporation compliance management, including annual reporting

- Banking introduction assistance for corporate account opening

Ready to establish your business in China? Reach out to Expanship China to discuss your entity formation requirements.

Frequently Asked Questions (FAQ)

The Limited Liability Company (有限责任公司) is the most frequently established entity type, particularly among small to medium-sized businesses and foreign investors. Its combination of capped liability, relatively straightforward registration under the Company Law of the People's Republic of China, and flexible shareholder structure makes it the default choice across most industries.

Both structures are registered as limited liability companies under Chinese company law, but a Wholly Foreign-Owned Enterprise is 100% foreign-held and subject to additional scrutiny under the Foreign Investment Law of 2019, including negative list restrictions. A domestic LLC faces fewer foreign-ownership compliance layers and generally encounters a simpler approval process through the State Administration for Market Regulation (SAMR). Tax treatment under the Enterprise Income Tax Law applies equally to both, though a WFOE may face transfer pricing and related-party transaction reporting requirements that a purely domestic firm does not.

Among the available structures, the Limited Partnership offers comparatively restricted public disclosure, as limited partners are not prominently featured in all public filings. Nominee arrangements are legally permissible for certain roles, though the actual controller disclosure requirements under SAMR regulations limit the extent of privacy achievable. No structure entirely shields beneficial ownership from regulatory scrutiny.

A Sole Proprietorship Enterprise (个人独资企业) is by definition a single-person structure, and a one-person LLC is also permitted under the Company Law. Partnerships, however, require a minimum of two partners, while a Joint Stock Limited Company requires a minimum of two shareholders for a non-state-promoted formation. Representative Offices and Branch Offices are not independent entities and require a parent company rather than an individual as the establishing party.

Foreign individuals and entities may establish a WFOE, participate in a Sino-Foreign Equity Joint Venture, or form a Sino-Foreign Cooperative Joint Venture, subject to the negative list administered jointly by the National Development and Reform Commission (NDRC) and the Ministry of Commerce (MOFCOM). Foreign investors may also open a Representative Office, though it cannot generate revenue directly. Access to domestic LLC or partnership structures by foreign nationals is subject to sector-specific restrictions.

Conversion between certain entity types is permitted under Chinese law. An LLC may be restructured into a Joint Stock Limited Company through a formal conversion process, which requires updated registration with SAMR and amendments to the articles of association. Converting a Partnership or Sole Proprietorship into a company-type entity involves a more complex re-registration process, and not all conversions are treated as continuations of the original legal entity.

No. The Sole Proprietorship Enterprise and General Partnership do not possess separate legal personality distinct from their founders, meaning personal assets may be exposed to business liabilities. The LLC, Joint Stock Limited Company, and WFOE all hold independent legal personality under the Civil Code and Company Law. Representative Offices and Branch Offices also lack independent legal personality, as they are extensions of their parent entities.

The Sole Proprietorship Enterprise carries the lightest compliance burden, with no mandatory audit requirement and simplified tax filing under the individual income tax framework. By contrast, a WFOE or LLC must maintain annual audits, file enterprise income tax returns, and submit annual reports to SAMR. A Representative Office, while structurally simple, requires periodic renewal filings and is subject to deemed-profit tax calculations on its operating costs.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.