Key Takeaways

- The Sociedad por Acciones (SpA) is Chile's most registered entity type, distinguished by its single-shareholder eligibility and flexible bylaw structure.

- Corporations in Chile are governed by Law 18,046 on Sociedades Anónimas, with open corporations subject to oversight by the Comisión para el Mercado Financiero (CMF) and closed corporations operating without stock exchange obligations.

- Chile's company registration system falls under the Registro de Empresas y Sociedades, administered through the Ministry of Economy, with filings governed primarily by the Código de Comercio.

- Partnerships such as the Sociedad Colectiva and Sociedad en Comandita structures carry unlimited liability and are generally reserved for professional or family arrangements rather than general commercial use.

Introduction to Entity Types in Chile

Chile sits in the southwestern cone of South America, bordered by Peru, Bolivia, and Argentina, with coastline stretching along the Pacific Ocean. It is an independent republic and one of the region's more open economies, operating a territorial-based corporate tax system under which foreign-sourced income may receive differential treatment depending on the structure used.

Company registration falls under the jurisdiction of the Registro de Empresas y Sociedades, administered through the Chilean Ministry of Economy. Filings are governed primarily by the Código de Comercio and, for corporations, by Law 18,046 on Sociedades Anónimas.

The main types of business entities in Chile available to local and foreign investors include:

- Sociedad Anónima (S.A.) — Open and Closed

- Sociedad por Acciones (SpA)

- Sociedad de Responsabilidad Limitada (SRL)

- Sociedad Colectiva

- Sociedad en Comandita Simple

- Sociedad en Comandita por Acciones

- Empresa Individual de Responsabilidad Limitada (EIRL)

- Branch Office (Agencia de Sociedad Extranjera)

- Representative Office

Each structure carries distinct implications for liability, governance, ownership, and tax treatment. This article examines each option in detail to help your business identify the most suitable formation path.

An Overview of Business Structures in Chile

Chilean company law recognizes several distinct legal forms, each governed primarily by the Código de Comercio (Commercial Code) and specific statutes such as Law No. 18,046 on Corporations and Law No. 3,918 on Limited Liability Companies. Understanding the available business structures in Chile overview is essential before selecting a formation path, as each form carries different implications for liability, governance, and taxation. The sections that follow examine each structure in full.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Tax Treatment | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Sociedad Anónima Abierta (S.A.) | Corporation | Limited | Taxable | Permitted | 2 shareholders | CMF | Law No. 18,046 |

| Sociedad Anónima Cerrada (S.A.) | Corporation | Limited | Taxable | Permitted | 2 shareholders | Registro de Comercio | Law No. 18,046 |

| Sociedad por Acciones (SpA) | Stock Company | Limited | Taxable | Permitted | 1 shareholder | Registro de Comercio | Law No. 20,190 |

| Sociedad de Responsabilidad Limitada (SRL) | LLC | Limited | Taxable | Permitted | 2–50 partners | Registro de Comercio | Law No. 3,918 |

| Sociedad Colectiva | Partnership | Unlimited | Taxable | Permitted | 2+ partners | Registro de Comercio | Código de Comercio |

| Sociedad en Comandita Simple | Limited Partnership | Mixed | Taxable | Permitted | 2+ partners | Registro de Comercio | Código de Comercio |

| Sociedad en Comandita por Acciones | Joint-Stock LP | Mixed | Taxable | Permitted | 2+ partners | Registro de Comercio | Código de Comercio |

| Branch Office | Foreign Branch | Parent liable | Taxable | Permitted | 1 parent entity | Registro de Comercio | Código de Comercio |

| Representative Office | Non-trading office | Parent liable | Generally exempt | Not permitted | 1 parent entity | Registro de Comercio | General Civil Law |

| Empresa Individual de Responsabilidad Limitada (EIRL) | Sole entity | Limited | Taxable | Permitted | 1 individual | Registro de Comercio | Law No. 19,857 |

Each of these structures is examined in full in the sections below.

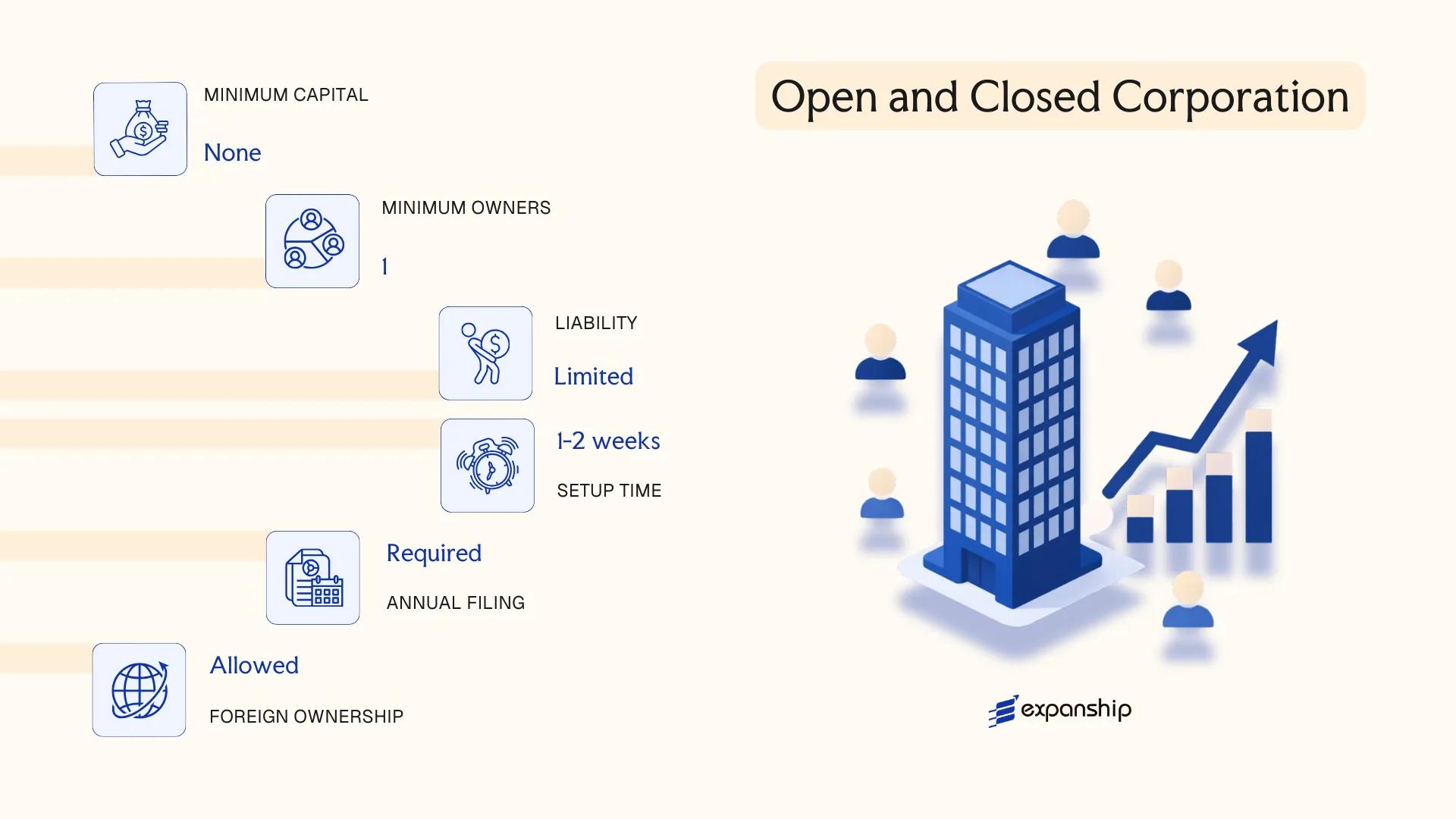

Sociedad Anónima (S.A.) — Open and Closed Corporation

Governed by Law No. 18,046 (Ley de Sociedades Anónimas, 1981), the Sociedad Anónima is Chile's principal vehicle for large-scale commercial activity. It carries separate legal personality, meaning the entity's obligations are distinct from those of its shareholders, whose liability is limited to their subscribed capital.

Capital is divided into shares, which may be transferred subject to the type of S.A. in question. Two formally recognised categories exist under the same statute: the open corporation (S.A. abierta) and the closed corporation (S.A. cerrada), each with distinct regulatory obligations. This structure is often chosen for the Sociedad Anónima Chile open closed corporation distinction it affords investors seeking different levels of regulatory oversight and share transferability.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Corporation (Sociedad Anónima) | Incorporated by public deed; registered with the CBR and published in the Diario Oficial |

| Members | Shareholders (accionistas); Board of Directors (Directorio) | Minimum 2 shareholders; no maximum. Open S.A. requires minimum 3 board directors; closed S.A. minimum 3 (unless bylaws specify otherwise) |

| Local Presence | Registered domicile in Chile required | Must maintain a registered address; a local legal representative is standard practice |

| Capital | CLP; no statutory minimum for closed S.A. | Shares must be subscribed at incorporation; open S.A. subject to CMF capital adequacy rules |

| Privacy | Shareholder register maintained internally | Open S.A. must file public disclosures with the CMF; closed S.A. has no public reporting obligation |

| Governance | Mandatory board of directors | Open S.A. requires an external auditor (auditor externo); closed S.A. may appoint an internal inspector of accounts |

Focus Points

- Taxation: Corporate income tax (Impuesto de Primera Categoría) applies at 27% for companies under the semi-integrated system; dividends distributed to non-residents are subject to a 35% Additional Tax with a partial credit for corporate tax paid; VAT applies at 19% on taxable transactions; stamp duty (impuesto de timbres y estampillas) applies to certain credit instruments.

- Annual Compliance: Open S.A. must file audited financial statements and periodic disclosures with the Comisión para el Mercado Financiero (CMF); closed S.A. files annual tax returns with the Servicio de Impuestos Internos (SII) but faces no CMF reporting.

- Treaty Access: Chile's network of double taxation agreements is available to resident S.A. entities, provided substance and beneficial ownership conditions are satisfied.

- Conversion: A closed S.A. that exceeds 500 shareholders or lists its shares is automatically reclassified as an open S.A. under Law No. 18,046, triggering full CMF supervision.

- Restrictions: Foreign shareholders face no ownership caps in most sectors; regulated industries (banking, insurance, broadcasting) require sector-specific authorisations.

Sub-Types

Open Corporation (S.A. Abierta)

An open S.A. is one that registers its shares with the CMF — either voluntarily or because it surpasses statutory thresholds — and is therefore subject to continuous public disclosure, audited accounts, and securities market regulation under Law No. 18,045. This structure is used by publicly traded firms and entities seeking access to capital markets.

Closed Corporation (S.A. Cerrada)

A closed S.A. does not register with the CMF and restricts share transfers through its bylaws. It is the standard choice for private investment vehicles, joint ventures between institutional partners, and family-held operating businesses that do not require public capital.

When to Use a Sociedad Anónima

The S.A. is the standard structure for joint ventures with institutional partners, holding platforms, and businesses requiring equity investment from multiple parties. Its principal advantage is the clear separation between shareholder and corporate liability. The principal drawback is administrative weight — particularly for the open variant, where ongoing CMF compliance, mandatory audits, and disclosure obligations generate sustained cost.

The Sociedad Anónima is best suited for mid-to-large enterprises, foreign direct investment vehicles, and any business where multiple shareholders require formal governance and transferable equity.

Company Incorporation in Chile

Incorporate a Sociedad Anónima or other Chilean entity with end-to-end support from Expanship.

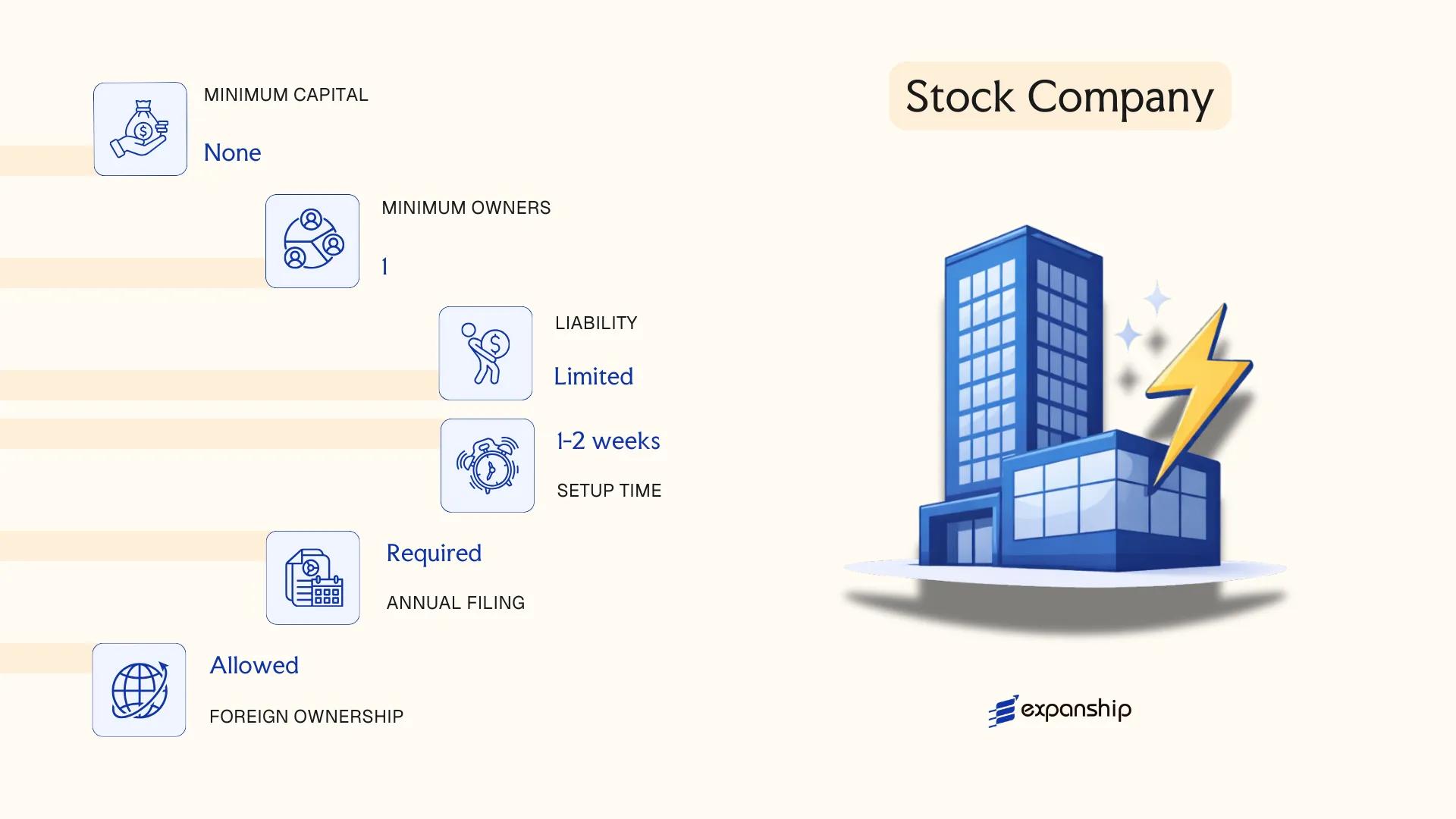

Sociedad por Acciones (SpA) — Stock Company

Introduced under Law 20,190 of 2007, the Sociedad por Acciones SpA Chile is a flexible capital-based structure that occupies a middle ground between a closely held limited liability company and a full corporation. It carries separate legal personality, meaning the entity's obligations are distinct from those of its shareholders, whose liability is confined to their subscribed capital.

Originally conceived to facilitate venture capital and startup activity, the SpA has since become a widely used vehicle for domestic commercial operations, holding structures, and foreign investment. Its statutes-driven design allows shareholders to customise governance, economic rights, and transfer restrictions with considerable freedom under the Companies Act framework administered by the Comisión para el Mercado Financiero (CMF).

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedad por Acciones (SpA) | Governed by Law 20,190; separate legal personality |

| Members | Shareholders; minimum 1, maximum 499 | Exceeding 500 shareholders triggers mandatory conversion to S.A. |

| Local Presence | Registered address in Chile required | No statutory requirement for a local director |

| Share Capital | No minimum capital; denominated in Chilean Pesos (CLP) | Capital defined in the company's statutes |

| Governance | Single shareholder can act as sole administrator | Articles of incorporation can establish any governance structure |

| Privacy | Shareholder information filed with the Civil Registry | Not publicly listed; limited public disclosure compared to open S.A. |

Focus Points

- Taxation: Subject to the general corporate income tax (First Category Tax) at 27% for entities under the partially integrated system; VAT applies at 19% on taxable supplies; dividends distributed to foreign shareholders attract a 35% withholding tax offset partially by corporate tax credits; stamp duty applies to certain credit operations.

- Annual Compliance: Must file annual tax returns with the Servicio de Impuestos Internos (SII); financial statements are not required to be audited unless specific thresholds are met.

- Conversion: Automatically required to convert to a Sociedad Anónima Abierta if shareholder numbers exceed 500 or if shares are offered publicly.

- Treaty Access: Eligible for benefits under Chile's double tax treaties, subject to beneficial ownership and residency conditions.

- Transfer Restrictions: Share transfers may be restricted or conditioned by the statutes, giving founders control over ownership changes.

Closing

The SpA suits foreign investors establishing a Chilean operating subsidiary, entrepreneurs seeking a single-member structure, and holding entities requiring flexible dividend and governance arrangements. Statutory freedom in drafting the articles is a material advantage, though the 499-shareholder ceiling limits its use as a broadly held investment vehicle.

The SpA is particularly well-suited to foreign-owned subsidiaries, early-stage companies, and single-investor holding structures requiring customisable governance without the formality of a full corporation.

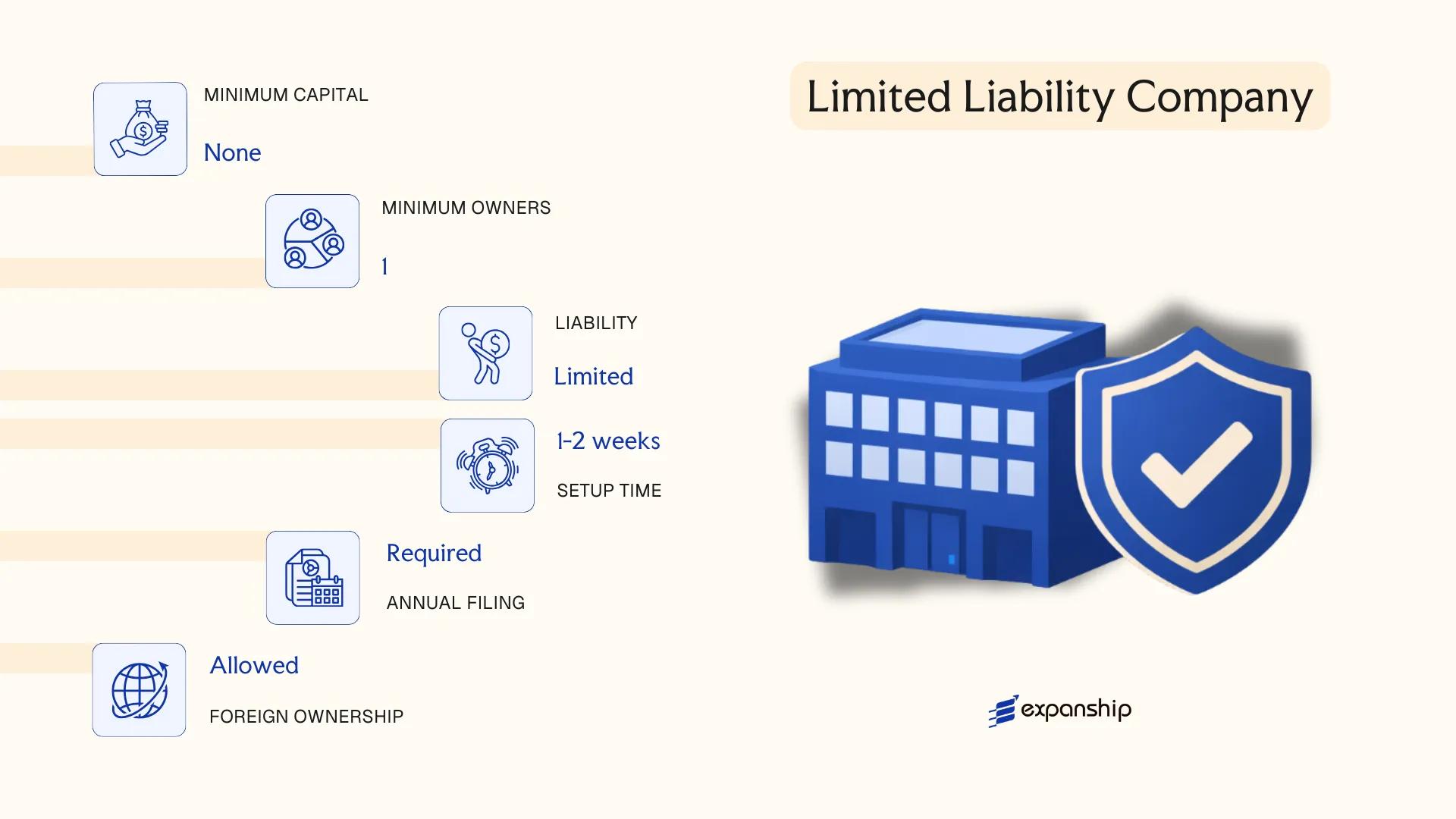

Sociedad de Responsabilidad Limitada (SRL) — Limited Liability Company

The Sociedad de Responsabilidad Limitada Chile is governed primarily by Law No. 3,918 of 1923, as subsequently amended, and operates as a separate legal entity distinct from its members. Liability is capped at each member's capital contribution, though the constitutive deed may extend liability to a higher agreed amount.

Structurally, the SRL sits between a partnership and a corporation. Ownership interests are non-transferable without unanimous consent from all members, which makes it a naturally closed structure suited to small groups of known partners.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Company | Separate legal personality; governed by Law No. 3,918 of 1923 |

| Members | 2 minimum, 50 maximum | Members (socios); no corporate officer distinction required by law |

| Local Presence | Registered address in Chile required | No mandatory resident manager, but a legal representative (apoderado) is standard practice |

| Capital | No statutory minimum; denominated in Chilean Pesos (CLP) | Capital divided into quotas (cuotas), not shares; quota transfers require deed amendment |

| Privacy | Constitutive deed must be registered with the Conservador de Bienes Raíces and published in the Diario Oficial | Member names are publicly accessible |

Focus Points

- Taxation: Subject to corporate income tax (27% for entities under the semi-integrated regime); VAT at 19% applies to taxable supplies; withholding tax applies to profit distributions to non-residents; stamp duty (Impuesto de Timbres y Estampillas) applies to certain credit instruments.

- Annual Compliance: Annual tax return filed with the Servicio de Impuestos Internos (SII); no mandatory statutory audit unless the entity meets size thresholds.

- Quota Transfers: Any transfer of quotas requires a notarised deed amendment, re-registration, and re-publication — unanimous member consent is required unless the deed specifies otherwise.

- Treaty Access: Resident entities qualify for benefits under Chile's network of double taxation treaties, subject to substance and beneficial ownership conditions.

- Conversion: An SRL may be converted into a Sociedad por Acciones (SpA) or Sociedad Anónima through a formal deed amendment process, without dissolving the entity.

Closing

The SRL is commonly used for closely held trading operations, family businesses, and domestic joint ventures where ownership stability is a priority. Its simple governance structure reduces administrative overhead, though the quota transfer restriction can complicate exits or the admission of new investors.

Best suited for small groups of known partners seeking limited liability with minimal ongoing governance requirements, provided they do not anticipate frequent changes in ownership.

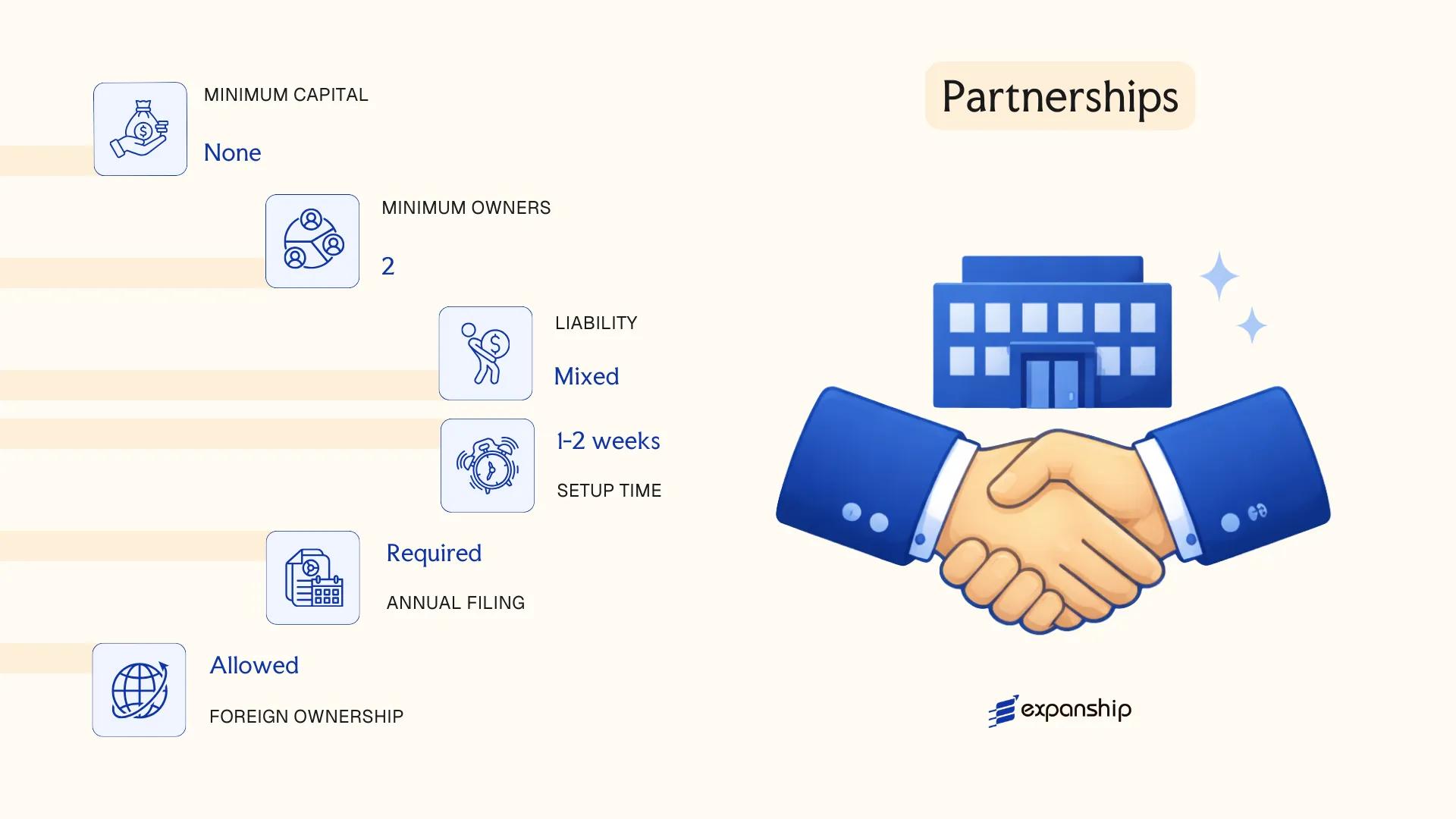

Partnerships in Chile [Sociedad Colectiva, Sociedad en Comandita Simple, Sociedad en Comandita por Acciones]

Partnership structures in Chile are governed primarily by the Chilean Commercial Code (Código de Comercio) and the Civil Code, with additional provisions under Law No. 3.918 and subsequent commercial legislation. These structures predate modern corporate forms and carry distinct characteristics, most notably that partners in a Sociedad Colectiva bear unlimited personal liability for the firm's obligations.

Unlike capital-based entities, partnership forms are defined by the identity and relationships of their members. Registration is completed through a public deed (escritura pública) before a notary and published in the Diario Oficial, with the firm registered at the relevant Conservador de Bienes Raíces y Comercio.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedad Colectiva / Sociedad en Comandita Simple / Sociedad en Comandita por Acciones | Three distinct structures under Chilean commercial law |

| Members | Partners (socios); general and limited partners in Comandita types | Sociedad Colectiva: minimum 2, no statutory maximum; Comandita types: at least 1 general (gestor) and 1 limited (comanditario) partner |

| Liability | Unlimited for general partners; limited to capital contribution for limited partners | Comandita por Acciones limited partners hold transferable shares |

| Local Presence | Registered address in Chile required; notarial deed and Diario Oficial publication mandatory | No statutory requirement for a local resident agent, though a domicile representative is standard practice |

| Capital | No statutory minimum; denominated in Chilean Pesos (CLP) | Comandita por Acciones requires share capital division |

| Privacy | Partner names appear in the public deed and Diario Oficial notice | No meaningful privacy for partners |

Focus Points

- Taxation: General partners in a Sociedad Colectiva are taxed under the Global Complementario or Impuesto Adicional regime; entities themselves are subject to corporate income tax (currently 27% for attributed income regimes), VAT at 19% on applicable transactions, and withholding tax applies to remittances to non-resident partners.

- Annual Compliance: Partners must file annual tax returns with the Servicio de Impuestos Internos (SII); no mandatory annual report to a corporate registry but accounting records must be maintained.

- Treaty Access: Access to Chile's double tax treaty network depends on the residence status of individual partners, not the partnership itself, since attribution rules may treat income at the partner level.

- Conversion: Chilean law permits conversion of partnership structures into capital companies, subject to unanimous partner consent and re-registration formalities.

- Restrictions: Foreign nationals may be partners, but all entities require a Chilean tax identification number (RUT) and a Chilean domicile for the firm.

Sub-Types

Sociedad Colectiva

All partners carry joint and unlimited liability for the entity's debts, and the firm's name (razón social) must include at least one partner's surname. This structure is used primarily in professional practices and traditional family businesses.

Sociedad en Comandita Simple

Two classes of partners coexist: socios gestores (general partners) who manage the firm and bear unlimited liability, and socios comanditarios (limited partners) whose liability is capped at their agreed capital contribution. Limited partners are prohibited from participating in management.

Sociedad en Comandita por Acciones

The limited partners' interests are divided into transferable shares (acciones), making capital more fungible than in the simple variant. General partners retain unlimited liability and exclusive management authority, while shareholders participate economically without management rights.

These partnership forms are used mainly in professional services, family-held trading operations, and structures where flexibility in profit distribution among a defined group of partners outweighs the drawback of unlimited liability for at least one class of member. The primary limitation across all three types is that general partners cannot shield personal assets from business creditors.

Partnership structures in Chile are best suited to closely held professional firms or family businesses where partners have an established trust relationship and accept the liability implications of the chosen structure.

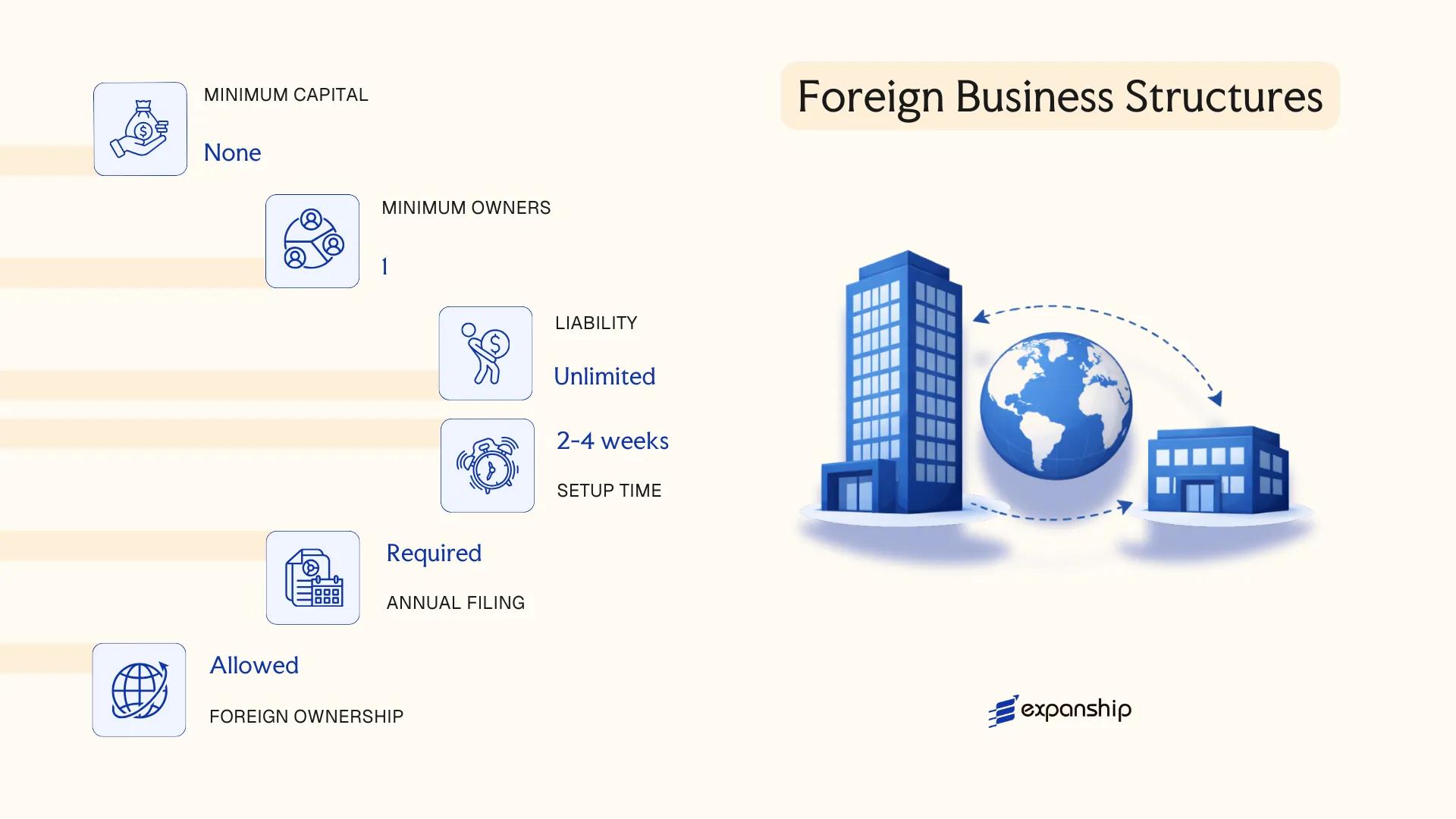

Foreign Business Structures in Chile [Branch Office, Representative Office, Agency]

Establishing a foreign company branch office Chile is governed primarily by Articles 447 to 469 of the Chilean Commercial Code, along with Law No. 18,046 for corporations operating as branches. A foreign entity operating through a branch does not create a separate legal person under Chilean law — the parent company remains fully liable for the branch's obligations. Representative offices and agencies occupy distinct positions along this spectrum, with varying degrees of commercial activity permitted under each structure.

Registration of any foreign entity in Chile requires authorization from the Ministry of Economy through the Companies Registry (Registro de Empresas y Sociedades) or, for corporations, via the Commission for the Financial Market (CMF) when applicable. Each structure type triggers different tax exposure, regulatory reporting obligations, and operational scope, so the choice between them carries material consequences.

Key Characteristics

| Requirement | Branch Office | Representative Office | Notes |

|---|---|---|---|

| Legal Form | Extension of foreign parent | Non-trading presence | Neither is a separate legal entity from the parent |

| Legal Representative | Mandatory local agent (apoderado) | Mandatory local representative | Must be resident in Chile and hold notarized power of attorney |

| Parent Liability | Full and unlimited | Full and unlimited | No liability shield exists between parent and Chilean operations |

| Registered Address | Required | Required | A physical address in Chile must be maintained |

| Capital | No statutory minimum, but must be declared | Not applicable | Branch capital must be declared before the Servicio de Impuestos Internos (SII) |

| Commercial Activity | Permitted | Not permitted | Representative offices are restricted to liaison, market research, and promotion |

| Privacy | Parent company details publicly disclosed | Parent company details publicly disclosed | Chilean registry records are publicly accessible |

Focus Points

- Taxation: Branch profits are subject to the standard corporate income tax (First Category Tax) at 27%, plus an Additional Withholding Tax of 35% on remittances to the foreign parent, with partial credit available; VAT at 19% applies to taxable supplies; stamp duty applies to certain credit instruments.

- Treaty Access: Chile's double taxation treaties may apply to branch income, but eligibility depends on the treaty's permanent establishment provisions and the parent's country of residence.

- Annual Compliance: Branches must file annual tax returns with the SII, maintain local accounting records in accordance with Chilean GAAP, and report financial statements annually.

- Economic Substance: No formal substance regime equivalent to some offshore jurisdictions exists, but the branch must demonstrate genuine operations if conducting commercial activity.

- Restrictions: Representative offices are prohibited from generating revenue or executing contracts in Chile; breach of this restriction can result in reclassification or penalties by the SII.

Sub-Types

Branch Office (Agencia)

A branch, referred to locally as an agencia, is the most operationally complete foreign structure available. It may enter contracts, generate revenue, employ staff, and hold assets — all under the full legal and financial responsibility of the parent company.

Representative Office

This structure is limited to promotional and preparatory activities. It cannot invoice clients or execute binding commercial agreements, making it suited only for market entry research or managing relationships with local partners prior to full establishment.

Agency (Contrato de Agencia)

A commercial agency is a contractual arrangement rather than a registered corporate structure — a local agent is appointed to act on behalf of the foreign firm under a formal agreement. Liability exposure and scope of authority are defined by the contract terms and governed by Chilean commercial law.

When to Use a Foreign Business Structure

Foreign entities that need a commercial presence without incorporating a separate subsidiary typically use a branch; representative offices are appropriate only for pre-commercial activities. The primary advantage of a branch is operational speed relative to full subsidiary incorporation, though the absence of liability separation between the Chilean operation and the parent company is a significant structural drawback.

Foreign companies seeking a direct operational footprint in Chile without creating a separate local entity, particularly those with existing parent-level liability capacity.

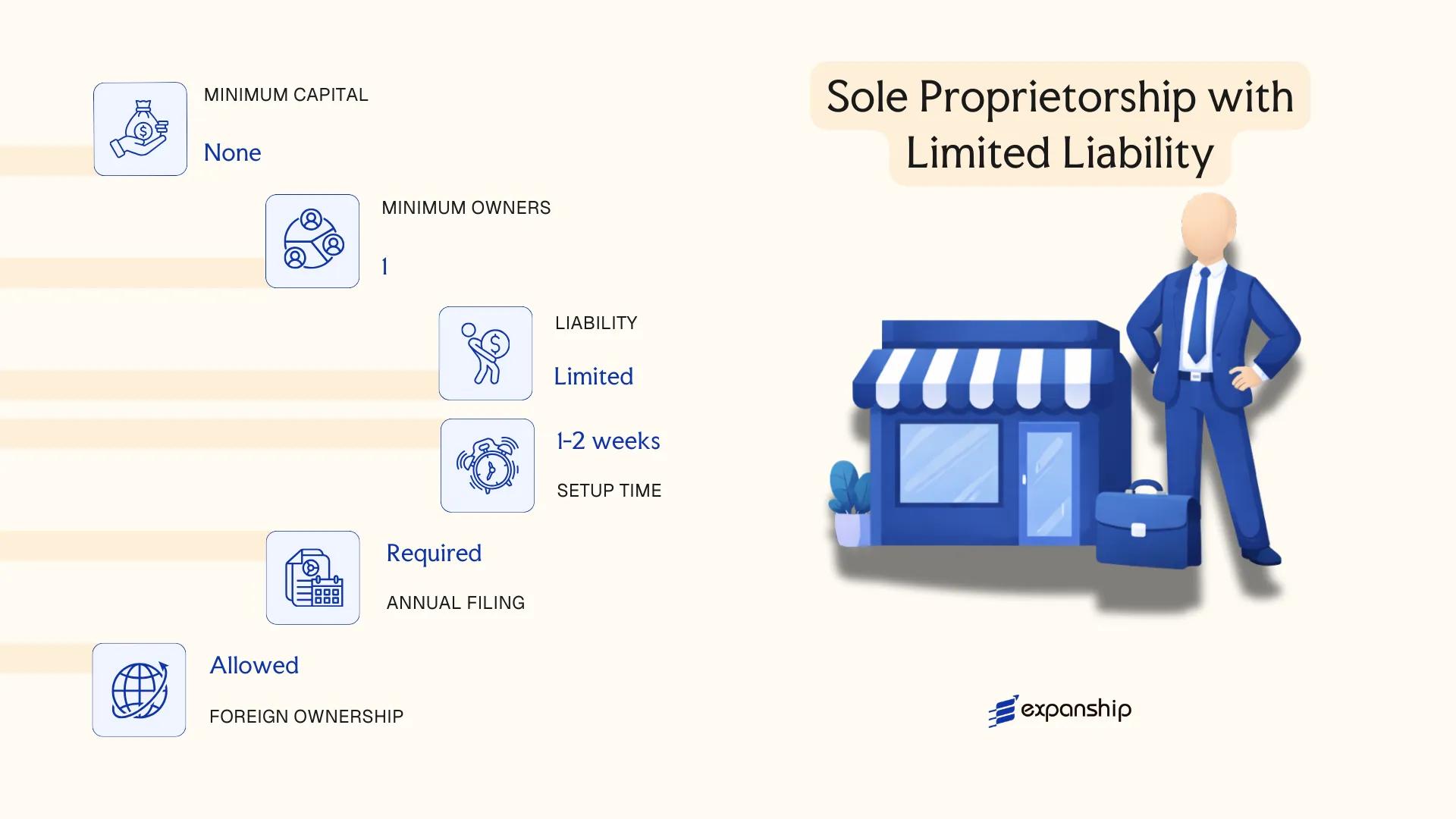

Empresa Individual de Responsabilidad Limitada (EIRL) — Sole Proprietorship with Limited Liability

The Empresa Individual de Responsabilidad Limitada is governed by Law No. 19.857, enacted in 2003, which created a distinct legal vehicle for single-person commercial activity in Chile. As an EIRL Chile sole proprietorship limited liability structure, it carries separate legal personality from its owner, meaning the individual's personal assets are shielded from the firm's commercial obligations.

Unlike a general sole proprietorship, the EIRL is treated as a juridical person under Chilean law. The proprietor assigns a defined capital amount to the entity at formation, and liability is confined to that contributed capital.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Empresa Individual de Responsabilidad Limitada (EIRL) | Single-owner juridical person under Law 19.857 |

| Members | 1 Proprietor (natural person only) | Legal entities cannot be proprietors |

| Local Presence | Registered legal domicile in Chile required | No mandatory local director beyond the proprietor |

| Capital | No statutory minimum; denominated in Chilean Pesos (CLP) | Capital declared in the constitutive deed |

| Privacy | Constitutive deed registered publicly via the Registro de Comercio | Ownership is publicly traceable |

Focus Points

- Taxation: Subject to First Category Tax on net income at the standard corporate rate (currently 27% for attributed regime entities); VAT applies to commercial transactions at 19%; distributions may trigger Additional Withholding Tax for non-resident proprietors.

- Annual Compliance: Annual financial statements must be filed with the Servicio de Impuestos Internos (SII); bookkeeping obligations apply from incorporation.

- Conversion: An EIRL may be converted into a Sociedad por Acciones or other recognised entity type through a formal deed amendment registered with the Conservador de Bienes Raíces.

- Restrictions: Only natural persons may establish an EIRL; the same individual may hold multiple EIRLs simultaneously, but each operates as a separate legal entity.

Recommendations

The EIRL suits self-employed professionals, consultants, and small traders seeking personal asset protection without the administrative overhead of a multi-member structure. Its principal advantage is the legal separation of personal and business patrimony; its core limitation is that it cannot be capitalised through third-party shareholders, restricting growth financing options.

This entity is best suited for individual entrepreneurs or freelancers conducting commercial activity in Chile who require formal liability separation but do not anticipate bringing in equity partners.

How to Choose the Right Entity Type in Chile

Selecting how to choose the right company structure in Chile is not a formality — the entity you register shapes your tax exposure, liability, governance obligations, and operational capacity from day one.

Why Your Entity Choice Matters

- Trading actively with Chilean residents through a foreign entity not registered under the Código de Comercio constitutes unauthorized operation and exposes the firm to administrative penalties or forced dissolution.

- Forming a Sociedad Anónima Cerrada when your objectives are purely asset-holding adds mandatory shareholder meeting requirements and statutory audit thresholds that a SpA would not impose.

- Selecting an entity without the capacity to demonstrate local substance, where Chilean tax authorities apply transfer pricing scrutiny under Article 41-E of the Ley de Impuesto a la Renta, can trigger adjustments and surcharges on related-party transactions.

- Registering an EIRL when the business later requires outside equity investment forces a full restructuring, since this structure does not permit additional shareholders by law.

Key Factors to Consider

- Business Activity: Active trading, regulated sectors (banking, insurance, fund management), and passive asset holding each correspond to distinct structural requirements under Chilean law.

- Ownership Structure: A single founder may use a SpA or EIRL, while multi-party ventures require a structure with defined share or quota mechanisms.

- Tax Objectives: Your eligibility for the Pro-Pyme regime under the Ley 21.210 or access to Chile's tax treaty network depends on the entity type and residency classification.

- Governance Flexibility: An SpA allows the constitutive deed to define management rules freely, whereas an S.A. must comply with the Ley 18.046 board and meeting requirements.

- Exit and Conversion: Not all Chilean entity types permit statutory conversion; confirm whether your chosen structure allows redomiciliation or transformation before incorporating.

The full text of Chile's principal companies legislation, the Ley 20.659 on simplified companies, is available through the Biblioteca del Congreso Nacional.

Compliance Services for Companies in Chile

Ongoing compliance support for Chilean entities, including annual filings, statutory obligations, and regulatory reporting.

Conclusion

Selecting the right structure is one of the first binding decisions you make when incorporating a company in Chile, and each entity type under Chilean law serves a distinct purpose. The Sociedad Anónima Abierta suits large businesses seeking public capital markets access under CMF supervision, while the Sociedad Anónima Cerrada fits private firms requiring formal governance without stock exchange obligations. The SpA has become the most registered entity type in Chile, favored for its single-shareholder eligibility and flexible bylaws. The SRL remains common among small to mid-sized domestic ventures, and the EIRL serves sole operators who need personal liability separation. Partnerships carry unlimited liability and are generally reserved for specific professional or family arrangements. Branch offices serve foreign firms testing the market without a separate legal person.

Chile continues to expand its tax treaty network and has signaled ongoing modernization of its Registro de Empresas y Sociedades platform, reflecting a broader trajectory toward administrative efficiency for business registration.

How Expanship Can Assist You

Expanship's company formation services Chile cover the full incorporation process, from selecting the right structure — whether a Sociedad por Acciones, a Sociedad de Responsabilidad Limitada, or a Sociedad Anónima — through registration with the Registro de Comercio and publication in the Diario Oficial. Your compliance obligations begin the moment your entity is constituted, and our team is positioned to manage those requirements from day one.

From document preparation to ongoing filings, here is what our Chile business registration assistance includes:

- Drafting and notarizing constitutional documents

- Registered agent and legal domicile provision

- Filing with the Servicio de Registro Civil e Identificación and relevant commercial registries

- RUT and tax registration with the Servicio de Impuestos Internos (SII)

- Post-incorporation compliance management and annual reporting support

- Banking introduction assistance for corporate account opening

Reach out to Expanship Chile to discuss how we can support your entry into the Chilean market.

Frequently Asked Questions (FAQ)

The Sociedad por Acciones (SpA) is the most frequently registered entity, primarily because it can be formed by a single person and its constitutional flexibility is codified under Law No. 20.190. Its simplified governance requirements make it accessible to both local entrepreneurs and foreign investors.

A SpA is not subject to the SVS oversight requirements that apply to open S.A. corporations, resulting in lower ongoing compliance costs. An open S.A. must register with the Comisión para el Mercado Financiero (CMF) and publish audited financial statements, whereas a SpA has no such public disclosure obligation.

The Sociedad de Responsabilidad Limitada (SRL) and SpA both offer relatively limited public disclosure compared to an open S.A. Beneficial ownership information, however, is reportable to the SII under anti-money laundering obligations. Nominee arrangements are legally permissible but do not override tax transparency requirements.

No. A Sociedad Colectiva and both forms of Sociedad en Comandita require at least two parties to constitute a valid partnership agreement. The SpA and EIRL are the only structures expressly designed for single-founder formation.

Foreigners may form a SpA, SRL, or S.A. without residency, though a Chilean RUT (tax identification number) is required. Establishing a branch under Article 447 of the Commercial Code requires designating a resident agent with sufficient powers of attorney. An EIRL is restricted to natural persons and may present practical constraints for non-residents.

Chilean corporate law permits transformation between entity types without dissolving the original entity, provided statutory requirements and creditor notification procedures are observed. An SRL may convert to an S.A. or SpA, and the transformation must be registered with the Conservador de Bienes Raíces e Comercio. Not all combinations are equally straightforward, and tax implications should be assessed before initiating the process.

The EIRL, SpA, SRL, and both S.A. variants each possess separate legal personality under Chilean law. General partnerships (Sociedad Colectiva) also hold legal personality, though partners retain unlimited liability for firm obligations. A representative office, by contrast, does not constitute an independent legal entity.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.