Key Takeaways

- The OHADA Uniform Act on Commercial Companies and Economic Interest Groups is the primary legislative instrument governing all business entity types in the Central African Republic.

- Among the available structures, the SARL is the most frequently registered entity due to its lower capital threshold and greater operational flexibility compared to the SA.

- Société en Nom Collectif (SNC) partnerships impose unlimited personal liability on partners, making them generally unsuitable outside closely held professional arrangements.

- Foreign entities seeking a formal presence in the Central African Republic without establishing an independent local legal entity may do so through a branch office or representative office.

Introduction to Entity Types in Central African Republic

Landlocked in central Africa, the Central African Republic (CAR) borders Chad, Sudan, South Sudan, the Democratic Republic of Congo, the Republic of Congo, and Cameroon. It is an independent sovereign state and a member of the Organisation pour l'Harmonisation en Afrique des Affaires (OHADA), the regional legal framework that governs commercial law across 17 member states including CAR.

Company registration falls under the jurisdiction of the Registre du Commerce et du Crédit Mobilier (RCCM), administered at the national level through the court system. The OHADA Uniform Act on Commercial Companies and Economic Interest Groups (Acte Uniforme relatif aux Sociétés Commerciales) is the primary legislative instrument governing business entity types in the Central African Republic.

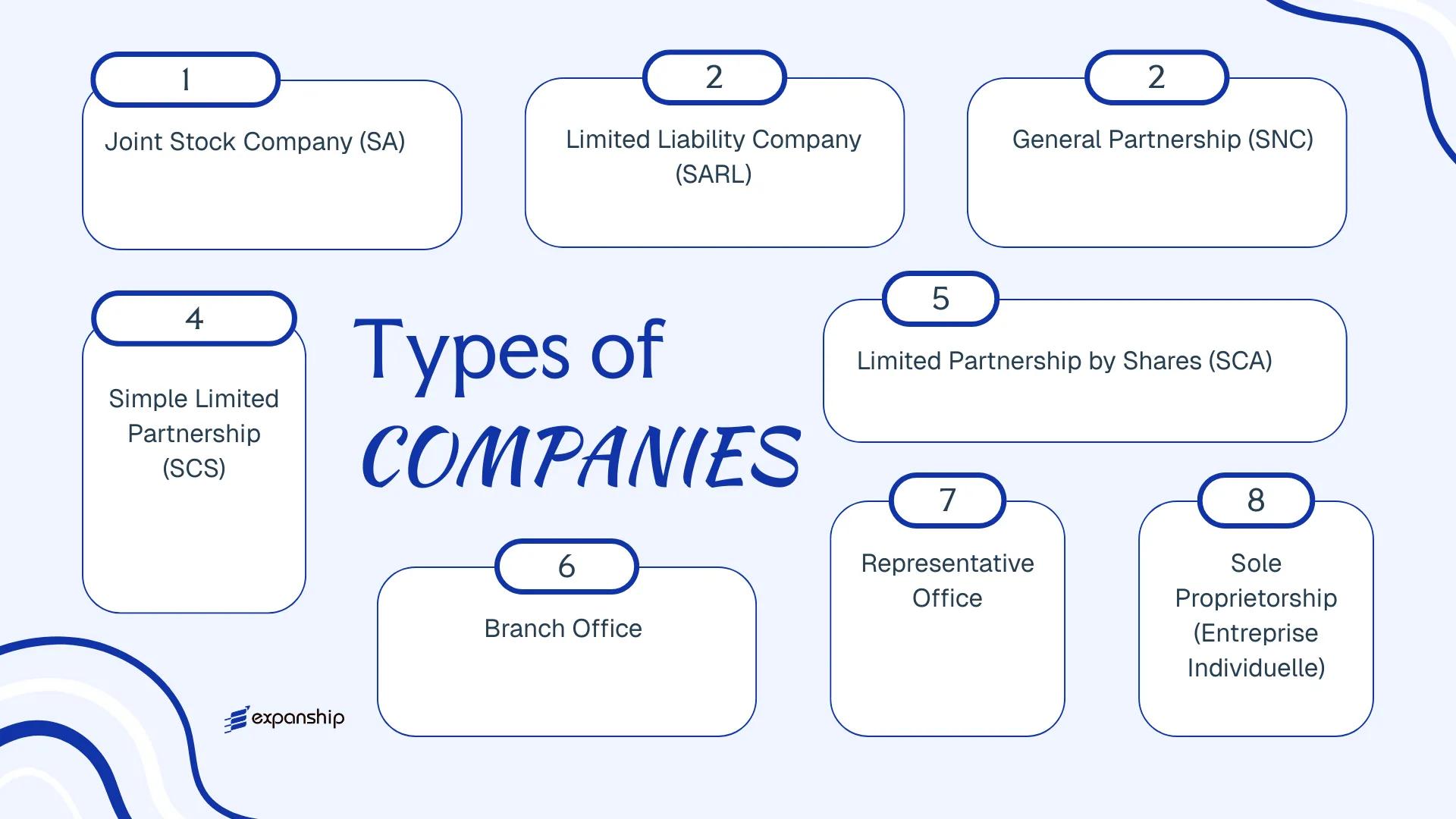

CAR operates a standard corporate tax regime — it is neither a zero-tax nor an offshore jurisdiction. Business entities available under OHADA and national law include the Société Anonyme (SA), Société à Responsabilité Limitée (SARL), Société en Nom Collectif (SNC), Société en Commandite Simple (SCS), Société en Commandite par Actions (SCA), branch offices, representative offices, and the Entreprise Individuelle. Each structure carries distinct legal, liability, and operational implications that this article examines in full.

An Overview of Business Structures in Central African Republic

Under the OHADA Uniform Act on Commercial Companies and Economic Interest Groups (Acte Uniforme relatif au droit des sociétés commerciales et du groupement d'intérêt économique), the Central African Republic recognises several distinct legal forms for conducting business. OHADA law, adopted across 17 member states including CAR, provides the primary legislative framework governing company registration, governance, and dissolution. Each structure carries different implications for liability, ownership, and operational scope.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Société Anonyme (SA) | Corporation | Limited to shares | Taxable | Yes | 1 shareholder | RCCM | OHADA AUSCGIE |

| Société à Responsabilité Limitée (SARL) | Private limited company | Limited to contribution | Taxable | Yes | 1 member | RCCM | OHADA AUSCGIE |

| Société en Nom Collectif (SNC) | General partnership | Unlimited, joint | Taxable | Yes | 2 partners | RCCM | OHADA AUSCGIE |

| Société en Commandite Simple (SCS) | Limited partnership | Mixed | Taxable | Yes | 2 partners | RCCM | OHADA AUSCGIE |

| Société en Commandite par Actions (SCA) | Partnership limited by shares | Mixed | Taxable | Yes | 4 members | RCCM | OHADA AUSCGIE |

| Branch Office | Non-legal entity | Parent liability | Taxable | Yes | N/A | RCCM | OHADA AUSCGIE |

| Representative Office | Non-legal entity | Parent liability | Limited scope | No | N/A | RCCM | OHADA AUSCGIE |

| Entreprise Individuelle | Sole proprietorship | Unlimited, personal | Taxable | Yes | 1 individual | RCCM | National law |

Each of these structures is examined in full in the sections below.

Société Anonyme (SA)

The Société Anonyme Central African Republic framework operates under the OHADA Uniform Act on Commercial Companies and Economic Interest Groups, which the Central African Republic adopted as part of its membership in the Organisation pour l'Harmonisation en Afrique du Droit des Affaires. The SA carries separate legal personality, meaning the entity exists independently of its shareholders, and liability is capped at each shareholder's capital contribution.

Structured for larger commercial operations, this form suits businesses seeking to raise capital through share issuance. SA incorporation CAR requires a minimum of one shareholder, as OHADA reforms eliminated the historical multi-shareholder threshold for this structure.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Limited Company | Governed by OHADA Uniform Act on Commercial Companies |

| Members | Shareholders: minimum 1, no maximum | Shareholders may be individuals or legal entities; single-shareholder SA is permitted |

| Directors | Board of Directors (minimum 3 members) or a single Administrator if one shareholder | Directors need not be CAR residents |

| Local Presence | Registered office in CAR required | Physical or legal address; registered agent not formally mandated but advisable |

| Share Capital | Minimum XAF 10,000,000 (approx. USD 16,500) | Must be fully subscribed; at least one-quarter paid up at incorporation |

| Privacy | Shareholder register is not publicly accessible; board composition filed with the RCCM | RCCM: Registre du Commerce et du Crédit Mobilier |

Focus Points

- Taxation: Corporate income tax applies under CAR's General Tax Code; VAT and withholding taxes on dividends, royalties, and service fees also apply — consult the Direction Générale des Impôts et des Domaines for current rates.

- Annual Compliance: Financial statements must be prepared under OHADA accounting standards (SYSCOHADA) and filed annually with the RCCM.

- Treaty Access: CAR has limited double tax treaty coverage; confirm treaty eligibility before structuring cross-border flows through this entity.

- Conversion: An SA may be converted into a SARL or other OHADA-recognised form by shareholder resolution, subject to capital and membership adjustments.

- Restrictions: Certain regulated sectors (banking, insurance, mining) require additional licensing and may impose local shareholding conditions.

Closing

The SA is suited to trading, holding, and joint-venture structures where multiple investors require defined governance and the potential for future capital raises. Its formal board structure provides governance clarity, though the XAF 10,000,000 minimum capital and mandatory auditor appointment (where required by OHADA thresholds) add administrative weight compared to simpler forms.

The SA works best for larger enterprises, joint ventures, or businesses planning phased equity investment where defined shareholder governance is a priority.

Company Incorporation in Central African Republic

Set up your Société Anonyme or other business entity in the Central African Republic with end-to-end incorporation support.

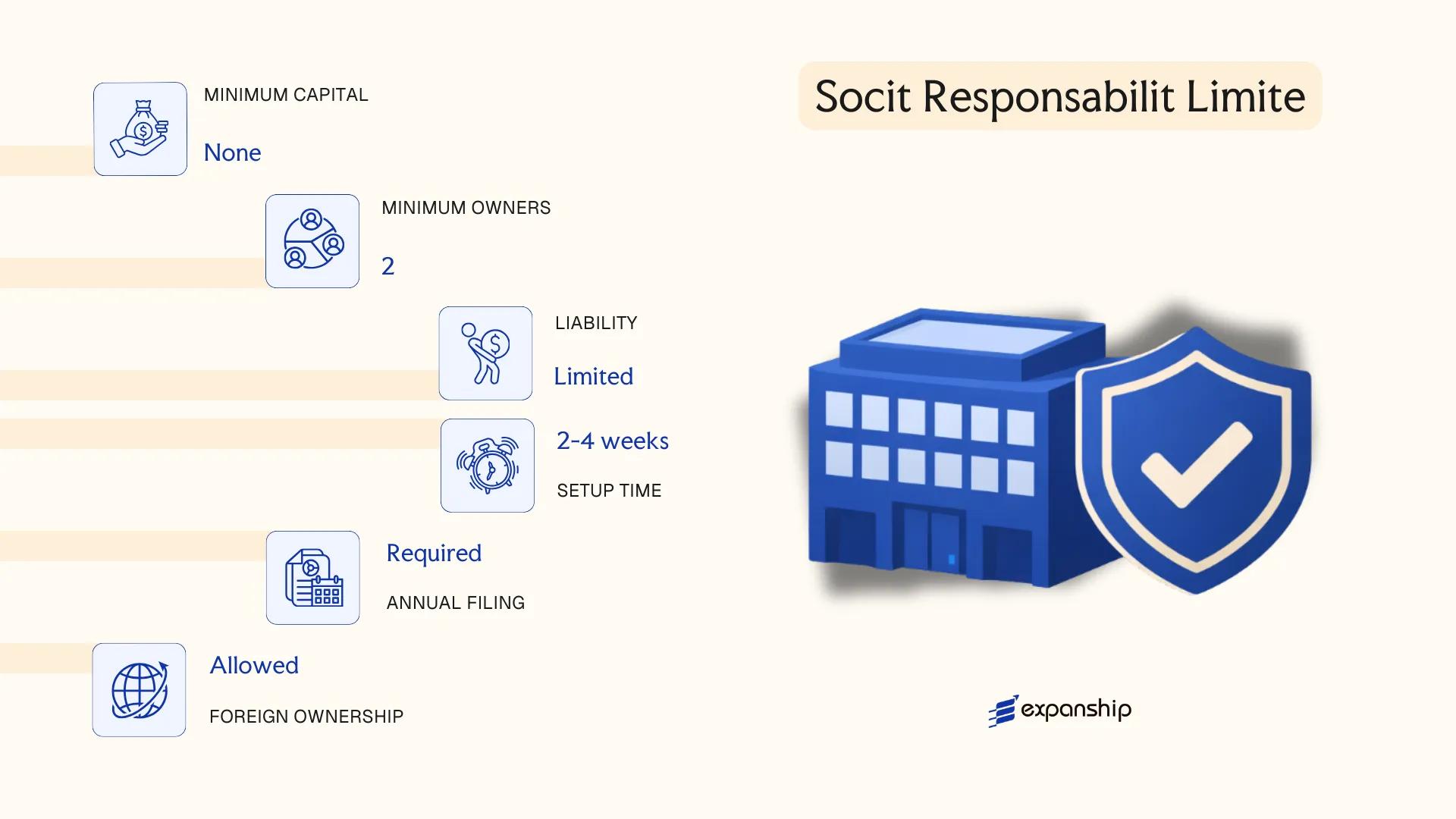

Société à Responsabilité Limitée (SARL)

The Société à Responsabilité Limitée CAR SARL is governed by the OHADA Uniform Act on Commercial Companies and Economic Interest Groups, most recently revised in 2014. As a hybrid between a partnership and a joint-stock company, the SARL carries separate legal personality and limits each member's liability to their capital contribution.

Structurally, the SARL suits small to mid-sized enterprises that require formal limited liability without the administrative demands of a full SA. SARL registration in Central African Republic follows OHADA-standardised procedures, administered locally through the Greffe du Tribunal de Commerce (Commercial Court Registry).

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited liability company | Separate legal personality under OHADA |

| Members | 1–100 associés (shareholders) | A single-member SARL is called a SARLU |

| Management | One or more gérants (managers) | Need not be a shareholder; nationality restrictions may apply |

| Local Presence | Registered office in CAR required | Must maintain a physical address on record |

| Capital | No statutory minimum under revised OHADA 2014 | Capital divided into parts sociales, not negotiable shares |

| Privacy | Member details filed with the Registry | Publicly accessible through the RCCM |

Focus Points

- Taxation: Subject to corporate income tax, VAT at the standard rate, and withholding taxes on dividends and service fees; stamp duties apply to certain instruments.

- Annual Compliance: Annual financial statements must be filed with the RCCM; statutory accounting follows OHADA's SYSCOHADA accounting framework.

- Transfer Restrictions: Parts sociales are not freely transferable; third-party transfers require approval from members holding at least three-quarters of the share capital.

- Treaty Access: CAR's limited tax treaty network may restrict access to reduced withholding rates for profit repatriation.

- Conversion: A SARL may be converted to an SA once it meets the applicable membership and capital thresholds under the OHADA Uniform Act.

Closing

The SARL is a practical structure for trading operations, family-held businesses, and joint ventures where members prefer liability protection without the governance complexity of a public company. Its main limitation is the restriction on transferring parts sociales, which reduces liquidity for investors seeking an exit.

The SARL is best suited for small to medium enterprises, foreign investors establishing a locally registered operating subsidiary, and joint venture partners requiring capped liability under OHADA law.

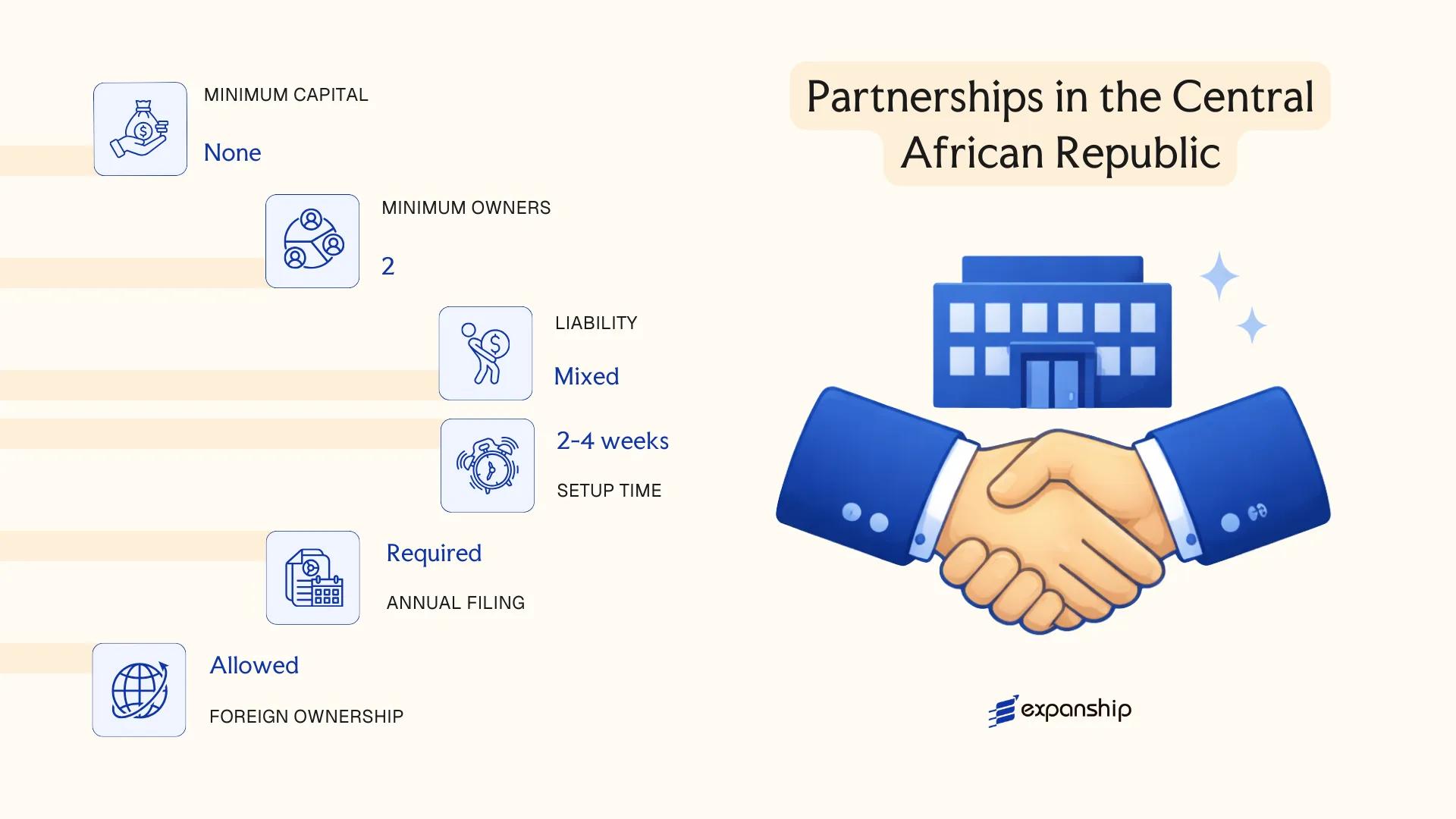

Partnerships in the Central African Republic [Société en Nom Collectif (SNC), Société en Commandite Simple (SCS), Société en Commandite par Actions (SCA)]

All three partnership structures available in the Central African Republic are governed by the OHADA Uniform Act on Commercial Companies and Economic Interest Groups (1997, revised 2014). The Société en Nom Collectif (SNC), Société en Commandite Simple (SCS), and Société en Commandite par Actions (SCA) each carry distinct liability profiles, making the choice between them consequential for partners.

Under OHADA rules, all three forms possess separate legal personality upon registration with the Greffe du Tribunal de Commerce. Despite this legal separation, partnerships Central African Republic SNC SCS SCA structures impose unlimited joint and several liability on at least one category of partner, which distinguishes them fundamentally from capital-based entities.

Key Characteristics

| Requirement | SNC | SCS / SCA | Notes |

|---|---|---|---|

| Legal Form | General partnership | Limited partnership | SCA combines partnership with share capital |

| Partners | Associés (all general) | Commandités (general) + Commanditaires (limited) | SCA commanditaires hold transferable shares |

| Minimum Members | 2 general partners | 1 general + 1 limited partner | No statutory maximum under OHADA |

| Minimum Capital | None stipulated | None (SCS) / Defined by articles (SCA) | SCA articles must specify share capital |

| Local Presence | Registered office in CAR required | Registered office in CAR required | No statutory requirement for a local resident manager |

| Privacy | Partner names filed publicly | General partner names disclosed; limited partners may have reduced exposure | Registry filings are public records |

Focus Points

- Taxation: Profits are generally taxed at partner level under CAR fiscal rules; corporate tax, VAT at 19%, and applicable withholding taxes on distributions apply depending on the partner's status and residency.

- Liability: General partners (commandités) in SCS and SCA bear unlimited personal liability; commanditaires are liable only to the extent of their contribution.

- Annual Compliance: Entities must file annual financial statements with the Greffe and maintain accounting records consistent with the OHADA Uniform Act on Accounting Law (SYSCOHADA).

- Restrictions: General partners in an SNC cannot transfer their interest without unanimous consent of all partners, limiting exit flexibility considerably.

- Treaty Access: Access to CAR's limited double tax treaty network depends on the partner's individual residency, not the partnership's registration jurisdiction.

Sub-Types

Société en Nom Collectif (SNC)

All partners hold merchant status and bear unlimited, joint, and several liability for the firm's debts. This structure is typically used by small professional or family-run businesses where partners maintain equal control and mutual trust is the operational foundation.

Société en Commandite Simple (SCS)

The SCS separates active management — held by commandités — from passive investors (commanditaires), whose liability is capped at their capital contribution. Interests of limited partners are not represented by negotiable securities, which restricts transferability compared to the SCA.

Société en Commandite par Actions (SCA)

The SCA structure introduces transferable share capital held by commanditaires, making it closer in capital mechanics to the SA while retaining at least one general partner with unlimited liability. This form is suited to ventures requiring capital-raising capacity alongside concentrated management control.

Closing

OHADA partnership structures in CAR are primarily used for closely held businesses, family enterprises, or arrangements where management control must remain with a defined group of general partners. The ability to segregate passive investors from active managers is a functional advantage, though the unlimited liability exposure of general partners remains a significant structural constraint.

These structures are best suited for closely held ventures or family businesses where partners have an established relationship and capital-raising from outside investors is not a primary objective.

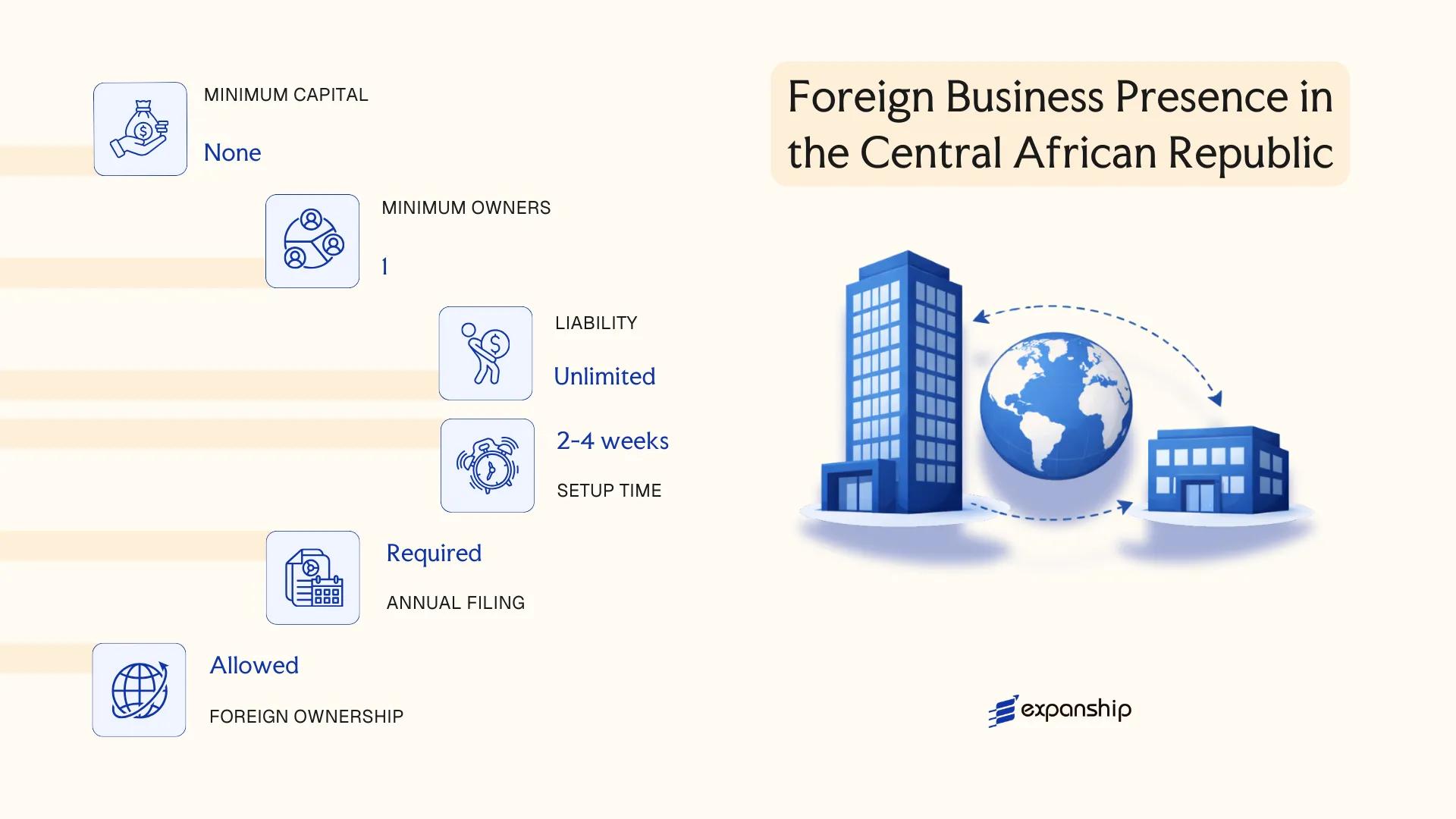

Foreign Business Presence in the Central African Republic [Branch Office, Representative Office]

Establishing a foreign company branch office in the Central African Republic is governed by the OHADA Uniform Act on Commercial Companies and Economic Interest Groups (AUDSCGIE), which the CAR adopted as a member state of the OHADA treaty. Under this framework, a branch office has no separate legal personality — the parent company remains fully liable for its obligations. A representative office operates under a similarly subordinate structure, existing solely to conduct preparatory or auxiliary activities on behalf of the foreign entity.

Both structures must be registered with the Registre du Commerce et du Crédit Mobilier (RCCM). Registration also requires notification to the Ministère du Commerce and, where applicable, sector-specific regulators. Neither form constitutes an independent legal entity.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Personality | None — extension of parent company | None — extension of parent company |

| Commercial Activity | Permitted | Not permitted; limited to liaison, market research, promotion |

| Liability | Parent bears full liability | Parent bears full liability |

| Registration Body | RCCM | RCCM |

| Local Representative | Mandatory resident representative required | Mandatory resident representative required |

| Minimum Capital | No statutory minimum; parent's capital applies | No statutory minimum |

Focus Points

- Taxation: Branch profits are subject to corporate income tax at the standard rate; withholding tax may apply on remittances to the parent; VAT registration is required if taxable supplies are made through the branch.

- Economic Substance: A resident representative must be appointed; the branch must maintain a registered address within the jurisdiction.

- Annual Compliance: Annual financial statements must be filed with the RCCM; the branch is subject to local accounting obligations under the OHADA Uniform Act on Accounting Law (AUDCIF).

- Treaty Access: Access to any applicable double tax treaties depends on the parent company's jurisdiction of incorporation, not the branch itself.

- Restrictions: A representative office cannot generate revenue, enter commercial contracts, or invoice clients locally.

Sub-Types

Branch Office

A branch conducts revenue-generating operations under the parent company's name and liability. It is typically used by foreign firms seeking an operational foothold without incorporating a separate local entity.

Representative Office

A representative office is restricted to non-commercial functions such as market research, promotion, and liaison activities. It carries no authority to sign contracts or generate income locally.

A branch suits foreign businesses that require operational activity without a separately incorporated subsidiary, though the parent's unlimited exposure to local liabilities is a meaningful constraint. A representative office is appropriate for market entry research but cannot support commercial transactions.

A branch office is best suited for established foreign companies seeking direct operational presence; a representative office fits firms in early-stage market assessment only.

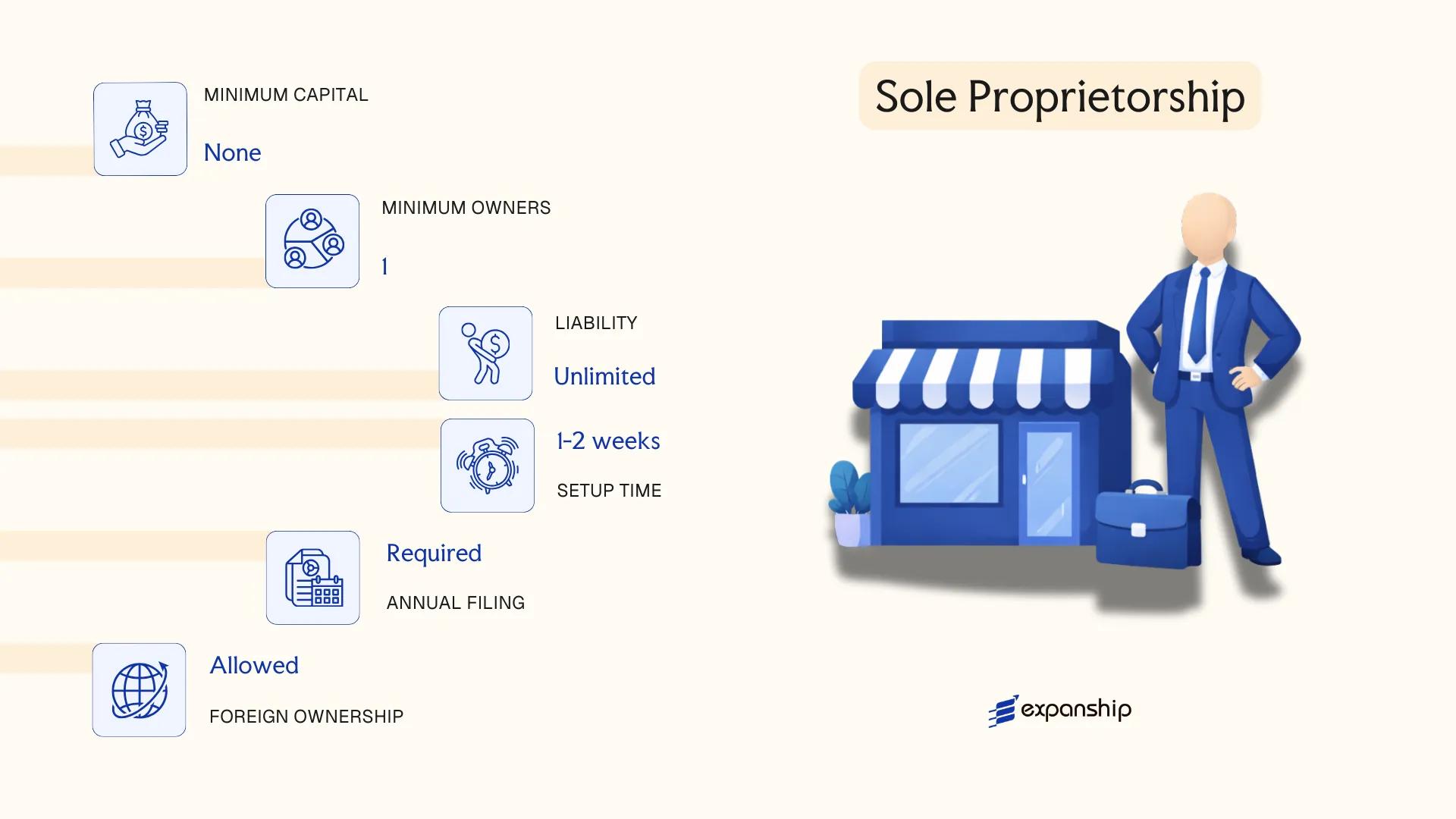

Sole Proprietorship (Entreprise Individuelle)

The sole proprietorship Central African Republic Entreprise Individuelle is the most basic form of business registration available to individuals operating commercially. Governed by the OHADA Uniform Act on General Commercial Law (Acte Uniforme relatif au Droit Commercial Général), most recently revised in 2010, this structure carries no separate legal personality distinct from its owner.

Because the proprietor and the business are legally the same person, all debts and obligations of the enterprise fall directly on the individual. Registration is handled through the Registre du Commerce et du Crédit Mobilier (RCCM), the commercial registry overseen at the national level.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole proprietorship (unincorporated) | No separate legal personality from the owner |

| Member Designation | Proprietor / Sole Trader | One individual only; no partners or shareholders |

| Membership | Minimum 1, Maximum 1 | Natural person only; legal entities cannot be proprietors |

| Local Presence | Registered business address required | Must correspond to the declared principal place of activity |

| Capital | No statutory minimum | Owner's personal assets constitute the operational base |

| Liability | Unlimited personal liability | Personal assets are fully exposed to business creditors |

Focus Points

- Taxation: Subject to personal income tax rather than corporate tax; VAT registration applies once turnover exceeds the applicable OHADA-aligned threshold; no withholding tax layer between the enterprise and the proprietor.

- Annual Compliance: Annual declaration of activity and turnover must be filed with the RCCM and relevant tax authority; accounting obligations apply under OHADA's SYSCOHADA accounting system.

- Treaty Access: As an unincorporated entity, the proprietor cannot independently access double taxation treaty benefits in a corporate capacity.

- Conversion: Can be converted into an incorporated structure such as a SARL, though this requires a new registration process rather than a simple amendment.

- Restrictions: Foreign nationals face additional constraints on eligibility and may require specific authorisations before registering as a sole trader.

Closing

The Entreprise Individuelle suits low-capital, locally operated activities where administrative simplicity outweighs the need for liability protection. The absence of a minimum capital requirement reduces the barrier to entry, but unlimited personal liability represents a significant exposure for any business with meaningful financial risk.

This structure is best suited for individual CAR residents or nationals running small-scale trading, artisanal, or service-based activities with limited third-party financial exposure.

How to Choose the Right Entity Type in Central African Republic

Selecting the correct structure before registration prevents legal, tax, and operational problems that are difficult to unwind once a business is active. Understanding how to choose the right entity type in the Central African Republic requires honest assessment of your operational model, not simply picking the most familiar structure.

Why Your Entity Choice Matters

Incorrect entity selection produces concrete legal and financial consequences:

- Forming an SA when your business has a single owner and limited capital forces you into minimum share capital requirements and mandatory board composition rules that serve no practical purpose for your structure.

- Choosing a branch office when your activities constitute a permanent commercial presence may trigger reclassification by tax authorities under the OHADA Uniform Act framework, resulting in penalties and back-tax assessments.

- Registering a representative office to conduct direct revenue-generating transactions breaches its permitted scope under OHADA rules, exposing the parent entity to liability.

- Selecting a partnership structure when investor exit flexibility is required creates complications, since partner transfers in an SNC require unanimous consent by default.

Key Factors to Consider

- Business Activity: Active trading, passive asset-holding, and regulated sectors such as banking each point to a different structure under the OHADA Uniform Act on Commercial Companies.

- Ownership and Management: A sole owner with no co-investors should evaluate the SARL or Entreprise Individuelle rather than structures requiring multiple shareholders.

- Liability Exposure: If personal asset protection is a priority, unlimited liability structures like the SNC are unsuitable regardless of their administrative simplicity.

- Tax Objectives: Your eligibility for specific fiscal regimes under CAR's General Tax Code depends partly on your entity classification, so confirm treatment before registering.

- Substance Capacity: If you cannot maintain a physical office or local employees, structures requiring genuine operational presence will create compliance gaps.

- Exit Strategy: Consider whether your chosen structure permits redomiciliation, conversion, or voluntary winding-up without triggering disproportionate regulatory steps.

Corporate Compliance Services in Central African Republic

Maintain statutory obligations, filing deadlines, and regulatory requirements for your entity in the Central African Republic.

Conclusion

Incorporating a company in Central African Republic requires selecting a legal structure that matches your operational scope, liability tolerance, and shareholder composition. Under the OHADA Uniform Act on Commercial Companies, which governs corporate law across the country, each entity form serves a distinct function. The SA suits larger ventures requiring broad capital access and formal governance, while the SARL remains the most frequently registered structure due to its lower capital threshold and operational flexibility. Partnerships such as the SNC carry unlimited personal liability and are generally reserved for closely held professional arrangements. Branch and representative offices serve foreign entities that need a formal presence without establishing an independent local legal entity.

Regulatory oversight in the Central African Republic continues to align with OHADA-wide harmonisation efforts, which gradually standardises compliance expectations across member states. For your business, understanding where that framework currently sits is a practical starting point before engaging with local registration authorities.

How Expanship Can Assist You

Expanship company formation Central African Republic services are structured around the specific legal framework established under the OHADA Uniform Act on Commercial Companies, which governs every entity type discussed in this blog. From registering a Société à Responsabilité Limitée (SARL) with the Centre de Formalités des Entreprises to filing a Société Anonyme (SA) with the Registre du Commerce et du Crédit Mobilier (RCCM), our team manages each step directly with the relevant authorities.

Across entity types, our service scope covers the full formation cycle and beyond:

- Document preparation, notarization, and legalization

- Registered agent and local office provision

- Government filing and RCCM liaison

- Post-incorporation compliance management

- Corporate secretarial support

- Banking introduction assistance

Reach out to Expanship Central African Republic to discuss your specific structure and requirements.

Frequently Asked Questions (FAQ)

The Société à Responsabilité Limitée (SARL) is the most frequently registered business structure. Its lower minimum capital requirements and simplified governance make it accessible to small and medium enterprises compared to the SA.

Both are governed by the OHADA Uniform Act on Commercial Companies, but the SA requires a higher share capital and a formal board of directors, while the SARL permits a single manager. The SA is suited to larger firms seeking public or institutional investment; the SARL is generally preferred for closely held operations.

The SARL offers relatively greater confidentiality, as detailed shareholder registers are not routinely published in publicly accessible registries under current CAR administrative practice. Nominee arrangements are not formally regulated under OHADA but may be structured contractually.

A single individual can form a SARL under OHADA rules, which permit a sole associate. Partnerships such as the SNC and SCS require at least two partners by definition, and the SA requires a minimum of one shareholder but mandates a board structure that typically involves multiple persons.

Foreign investors may register an SA, SARL, or establish a branch of a foreign company through the Registre du Commerce et du Crédit Mobilier (RCCM). Representative offices are also available but restricted to non-commercial activities. Foreigners should verify sector-specific restrictions, as certain industries require local participation under CAR investment legislation.

Conversion between entity types is permitted under the OHADA Uniform Act on Commercial Companies, most commonly from a SARL to an SA as a business grows and seeks broader capital structures. The process requires a shareholder resolution, updated statutes, and re-registration with the RCCM.

The SA, SARL, SCS, and SCA all hold separate legal personality under OHADA. The Société en Nom Collectif (SNC) and the Entreprise Individuelle do not provide the same liability separation, leaving partners or the sole proprietor personally exposed to business obligations.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.