Key Takeaways

- Company registration in Bhutan is governed by the Companies Act of Bhutan and administered by the Office of the Registrar of Companies under the Ministry of Economic Affairs.

- Private Limited Companies are the most commonly registered vehicle in Bhutan, used by both resident entrepreneurs and foreign joint venture partners under the Companies Act of Bhutan 2016.

- Foreign investors seeking full or majority ownership must operate through an FDI Company structure, as permitted under Bhutan's FDI Policy for approved sectors.

- Branch and Representative Offices provide a lower-commitment market entry option for foreign firms, while Partnerships and Sole Proprietorships are reserved for smaller, domestically oriented operations.

Introduction to Entity Types in Bhutan

Bhutan is a landlocked constitutional monarchy in South Asia, bordered by India to the south, east, and west, and by China to the north. Company registration and regulatory oversight fall under the Companies Act of Bhutan 2000 and are administered by the Office of the Registrar of Companies under the Ministry of Economic Affairs. Businesses operating in the country are subject to corporate income tax, with Bhutan following a standard territorial tax system rather than an offshore or zero-tax model.

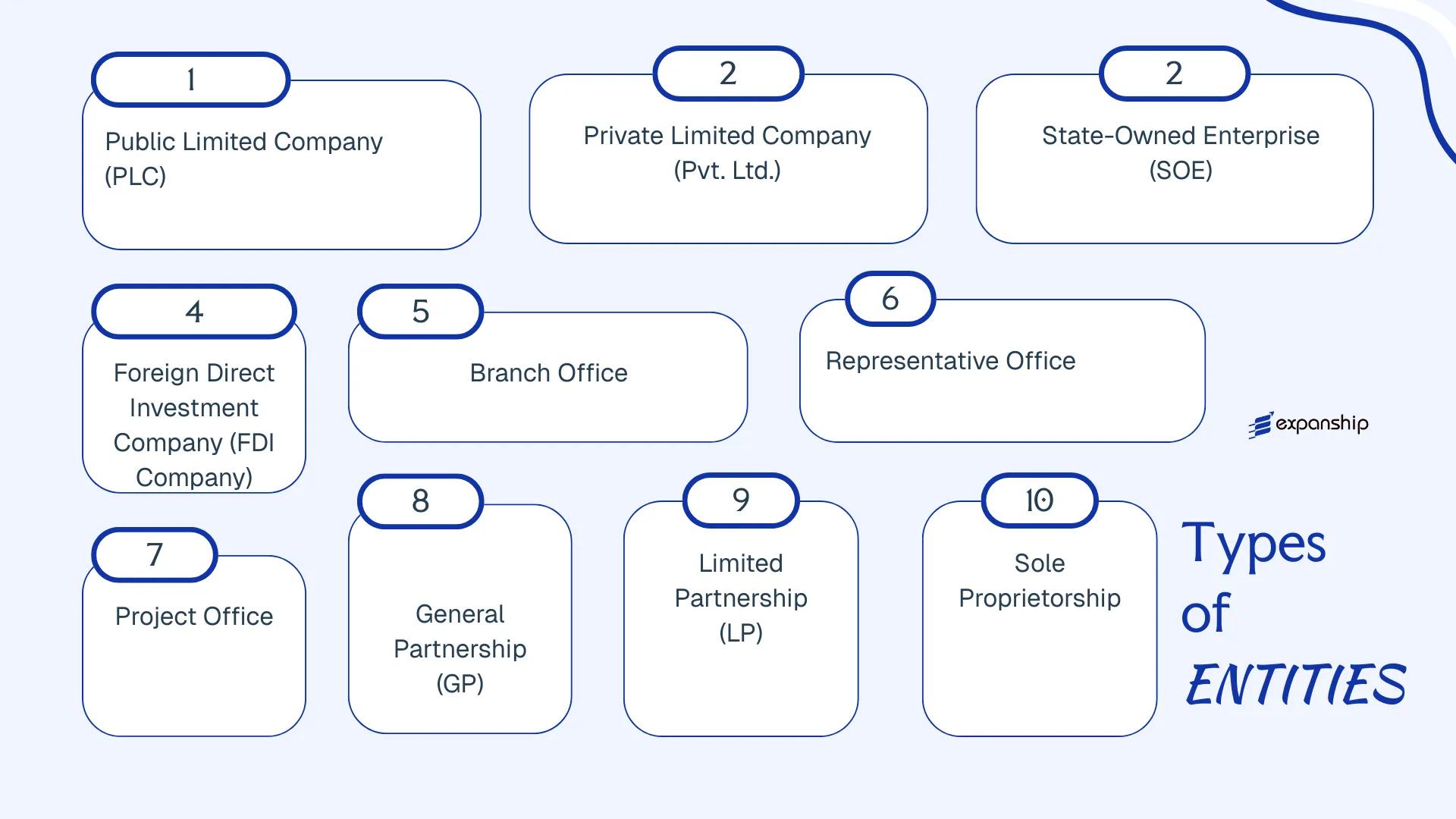

Selecting from the available types of business entities in Bhutan requires understanding the legal distinctions between each structure and what each permits in terms of ownership, liability, and operational scope. The entity options recognized under Bhutanese law include:

- Public Limited Company

- Private Limited Company

- State-Owned Enterprise

- Foreign Direct Investment (FDI) Company

- Branch Office

- Representative Office

- Project Office

- General Partnership

- Limited Partnership

- Sole Proprietorship

Each of these structures carries distinct registration requirements, ownership rules, and compliance obligations that this article examines in turn.

An Overview of Business Structures in Bhutan

Under the Companies Act of Bhutan 2000 and its subsequent amendments, businesses operating in or from the country can be registered under several distinct legal forms. The Ministry of Economic Affairs, through the Office of the Companies Registrar, administers company formation and maintains the official business registry. Each structure carries different rules on ownership, liability, and permitted activities.

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Public Limited Company | Incorporated company | Limited | Taxed | Yes | 7 shareholders | Office of Companies Registrar | Companies Act 2000 |

| Private Limited Company | Incorporated company | Limited | Taxed | Yes | 2 shareholders | Office of Companies Registrar | Companies Act 2000 |

| State-Owned Enterprise | Government entity | Limited | Taxed / Varies | Yes | Government-owned | Ministry of Finance | SOE Policy |

| FDI Company | Incorporated company | Limited | Taxed | Restricted | 1 shareholder | DITT / MoEA | FDI Policy |

| Branch Office | Foreign entity extension | Parent liability | Taxed | Restricted | N/A | Office of Companies Registrar | Companies Act 2000 |

| Representative Office | Non-trading presence | Parent liability | Generally exempt | No | N/A | Office of Companies Registrar | Companies Act 2000 |

| Project Office | Temporary entity | Parent liability | Taxed | Project-specific | N/A | Office of Companies Registrar | Companies Act 2000 |

| General Partnership | Unincorporated firm | Unlimited | Taxed | Yes | 2 partners | Office of Companies Registrar | Companies Act 2000 |

| Limited Partnership | Unincorporated firm | Mixed | Taxed | Yes | 2 partners | Office of Companies Registrar | Companies Act 2000 |

| Sole Proprietorship | Individual trader | Unlimited | Taxed | Yes | 1 owner | Dzongkhag Administration | Trade Rules |

Each of these structures is examined in full in the sections below.

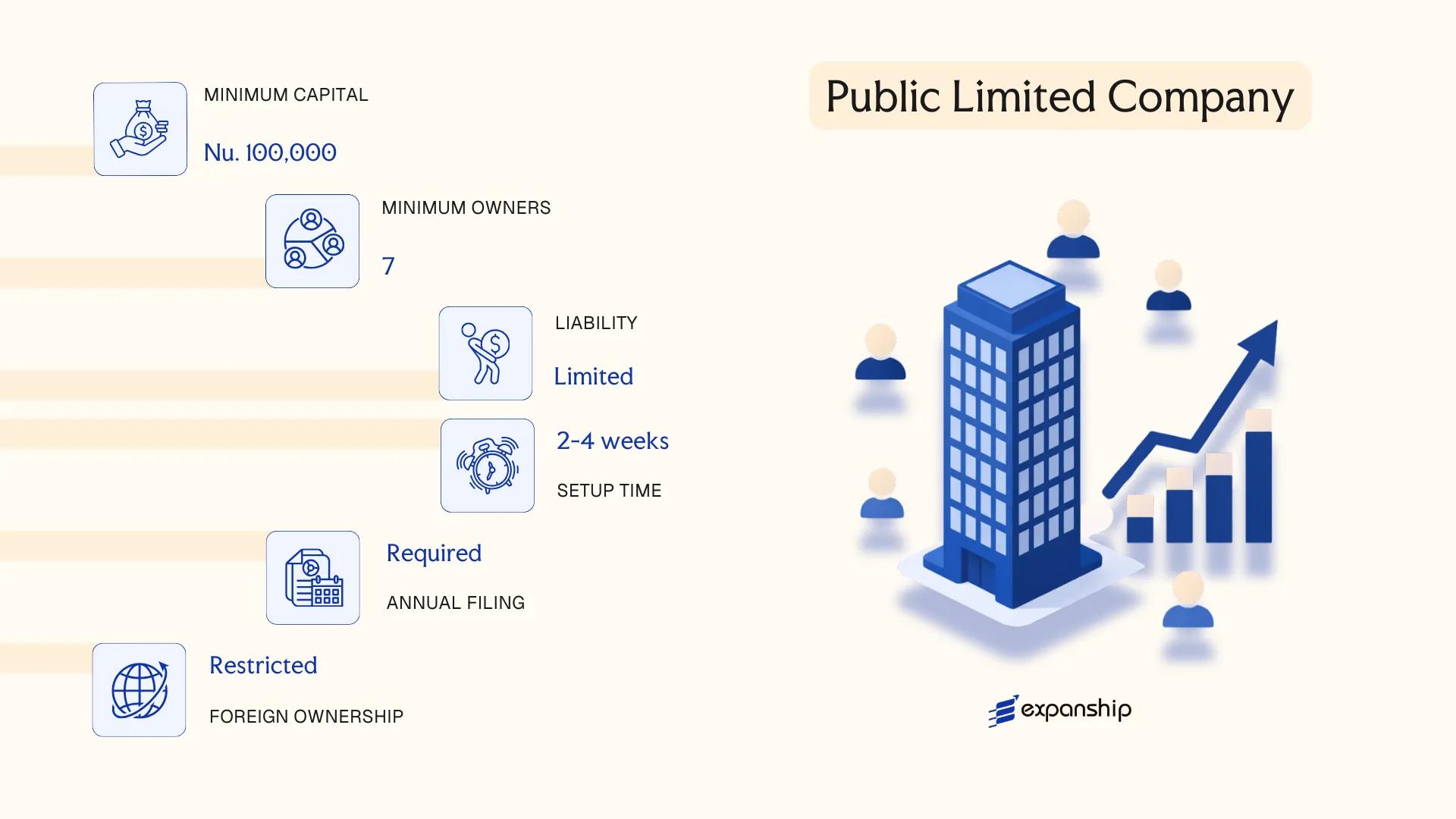

Public Limited Company

Governed by the Companies Act of Bhutan 2016, a public limited company is a distinct legal entity with separate legal personality, meaning it can own assets, enter contracts, and incur liabilities in its own name. Shareholder liability is limited to the amount unpaid on their shares. This structure sits at the more regulated end of the corporate spectrum and is the required vehicle for any business seeking to list its securities on the Royal Securities Exchange of Bhutan (RSEB).

Public limited company Bhutan registration involves filing with the Office of the Companies Registrar under the Ministry of Economic Affairs. The entity must meet disclosure obligations that private companies are not subject to, including public filing of financial statements.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Limited Company (PLC) | Separate legal personality; limited liability |

| Members | Min. 7 shareholders; no statutory maximum | Directors: min. 3; a board structure is required |

| Local Presence | Registered office in Bhutan required | Must maintain a physical address on record |

| Capital | Minimum paid-up capital applies; denominated in Bhutanese Ngultrum (BTN) | Exact threshold set by the Registrar; higher than for private companies |

| Disclosure | Audited financials must be filed publicly | Greater transparency obligations than private entities |

| Privacy | Low | Shareholder and director details are part of the public record |

Focus Points

- Taxation: Corporate income tax applies at the standard rate; VAT equivalents, withholding tax on dividends, and other levies are administered by the Department of Revenue and Customs

- Annual Compliance: Mandatory annual general meetings, audited accounts, and regulatory filings with the Registrar and, if listed, the RSEB

- Listing Eligibility: Only this structure qualifies for listing on the Royal Securities Exchange of Bhutan, subject to RSEB listing rules

- Conversion: Can be converted from a private limited company once statutory thresholds are met under the Companies Act 2016

- Foreign Participation: Subject to the FDI policy administered by the Department of Industry; sector-specific restrictions apply

Recommendations

A public limited company suits large-scale enterprises seeking access to public capital markets or those anticipating significant investor participation. The primary advantage is the ability to raise funds from the public through share issuance; the principal drawback is the administrative burden of ongoing disclosure and compliance obligations.

This structure is best suited for large businesses targeting public fundraising or eventual listing on the Royal Securities Exchange of Bhutan.

Company Incorporation in Bhutan

Incorporate your business entity in Bhutan with end-to-end support from Expanship.

Private Limited Company

A private limited company in Bhutan is governed by the Companies Act of Bhutan 2016, administered by the Office of the Attorney General and registered through the Registrar of Companies under the Ministry of Economic Affairs. It constitutes a separate legal person, meaning the company can own assets, enter contracts, and incur liabilities independently of its shareholders. Liability is limited to the amount unpaid on shares held, making this structure a hybrid between sole ownership and a publicly listed vehicle.

This is the most widely used commercial structure for domestic operators and foreign investors seeking a locally incorporated entity with defined ownership boundaries.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private Company Limited by Shares | Separate legal personality; governed by Companies Act 2016 |

| Members | Shareholders (1–30) | Minimum 1 shareholder; maximum 30; shares cannot be offered to the public |

| Directors | Minimum 1 director required | At least one director must be resident in Bhutan |

| Local Presence | Registered office address in Bhutan | A physical registered address is mandatory; a registered agent is advisable |

| Capital | No statutory minimum share capital | Denominated in Bhutanese Ngultrum (BTN); amount is determined in the articles |

| Privacy | Shareholder and director details filed with Registrar | Information is accessible through the Registrar of Companies; no public register equivalent to some offshore jurisdictions |

Focus Points

- Taxation: Corporate income tax is levied at 30% on net profits; a Business Income Tax (BIT) applies to sole traders and small firms, while sales tax and customs duties may apply depending on the sector; withholding tax applies to dividends and certain payments to non-residents.

- Annual Compliance: Annual returns and audited financial statements must be filed with the Registrar of Companies; audit is mandatory regardless of size.

- Economic Substance: No formally codified economic substance regime equivalent to those in offshore jurisdictions; however, resident director requirements and physical office obligations create a de facto local presence standard.

- Treaty Access: Bhutan has a limited tax treaty network; treaty benefits should be verified on a case-by-case basis before structuring cross-border arrangements.

- Restrictions: Foreign equity participation is subject to the Foreign Direct Investment Policy; certain sectors are reserved for Bhutanese nationals or require joint venture arrangements.

Closing

A private limited company suits trading operations, service businesses, and joint ventures where partners require defined liability and a locally recognised corporate identity. The separate legal personality is a clear structural advantage; however, the mandatory resident director requirement and restricted foreign ownership in certain sectors can constrain fully foreign-controlled setups.

This structure is best suited for small to mid-sized businesses, joint ventures, and foreign investors entering Bhutan through a locally incorporated entity with defined shareholding and operational presence.

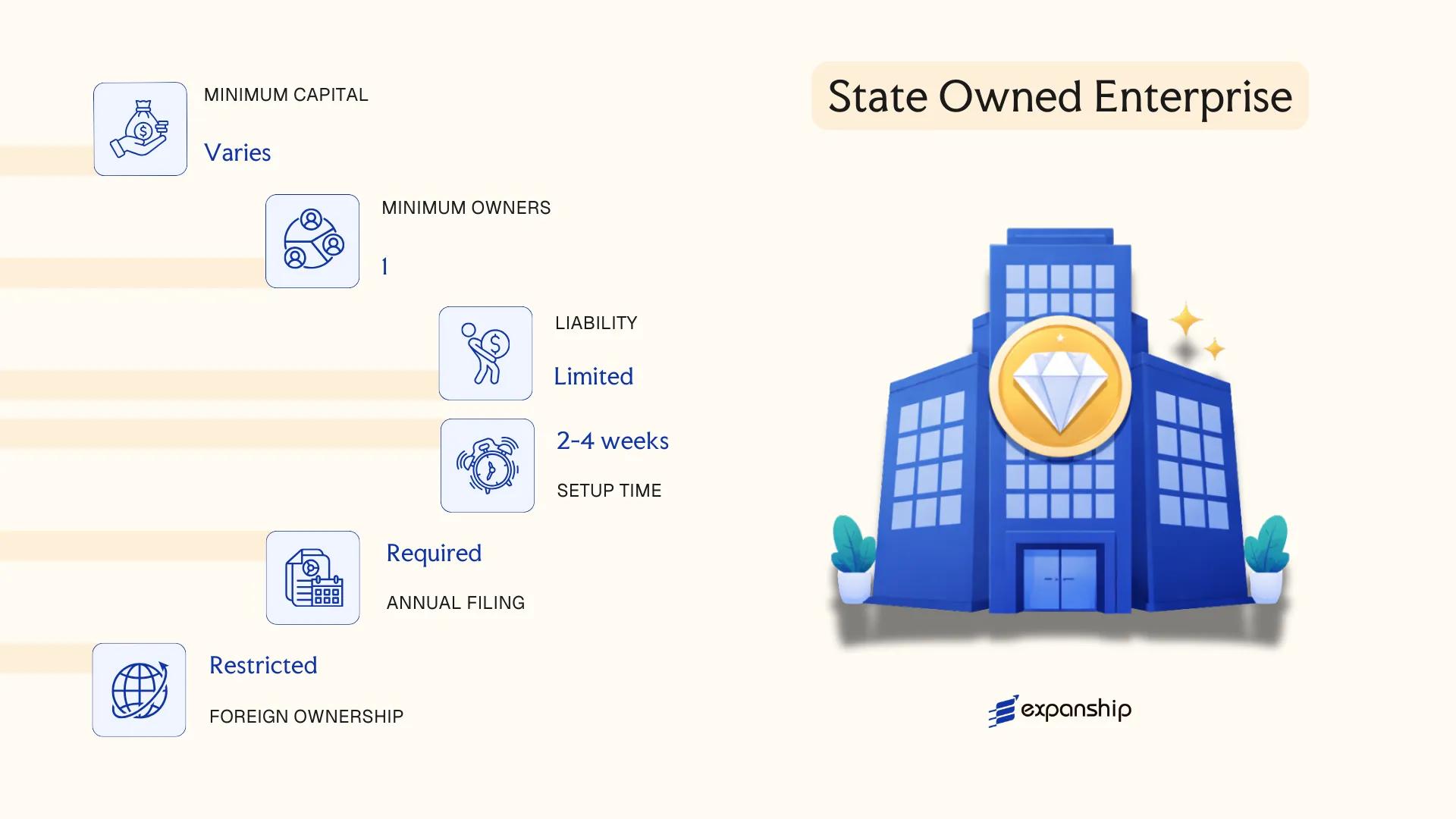

State-Owned Enterprise

Established under the Companies Act of Bhutan 2000 and subject to oversight by the Ministry of Finance, a state-owned enterprise (SOE) operates as a distinct legal entity separate from the government, giving it the capacity to own assets, enter contracts, and incur liabilities in its own name. The state-owned enterprise Bhutan structure typically combines government ownership with a commercial mandate, functioning as a hybrid between a public body and a private corporation.

Shareholding is held entirely or predominantly by the Royal Government, though some entities may admit minority private or institutional investors depending on their enabling legislation or sector-specific policies.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Incorporated company or statutory entity | Governed under Companies Act 2000 or sector-specific statute |

| Members | Board of Directors appointed by the government | Minister or Ministry may hold authority over board composition |

| Ownership | 51%–100% government shareholding | Minority private stakes permitted in select entities |

| Local Presence | Registered office in Bhutan required | Operations conducted domestically; no offshore equivalent |

| Capital | Bhutanese Ngultrum (BTN); no universal statutory minimum | Capitalisation set by founding legislation or Cabinet directive |

| Privacy | Ownership and financials subject to public accountability | Annual reports often tabled before Parliament |

Focus Points

- Taxation: SOEs are generally subject to corporate income tax at the standard rate of 30% under the Income Tax Act, though specific entities may receive exemptions or preferential treatment by Cabinet order; VAT and withholding tax obligations apply as with any registered company.

- Annual Compliance: Mandatory audit by the Royal Audit Authority; financial statements filed with the Registrar of Companies and the Ministry of Finance.

- Restrictions: Foreign nationals cannot incorporate or hold controlling interests in an SOE; formation requires a Cabinet decision or an Act of Parliament.

- Conversion: Partial privatisation is possible through divestiture of government shares, subject to approval by the Ministry of Finance and, in some cases, the National Assembly.

- Treaty Access: As government-affiliated entities, SOEs may benefit from bilateral agreements and preferential procurement arrangements under government policy.

Closing

SOEs in Bhutan operate primarily in strategic sectors such as hydropower, telecommunications, banking, and infrastructure, where the government retains control to serve national interest objectives. The primary limitation is structural: these entities cannot be formed by private parties and are not accessible as a vehicle for private investment or commercial incorporation.

Best suited for government bodies or state-sponsored projects requiring a commercially structured entity with public accountability obligations in regulated sectors.

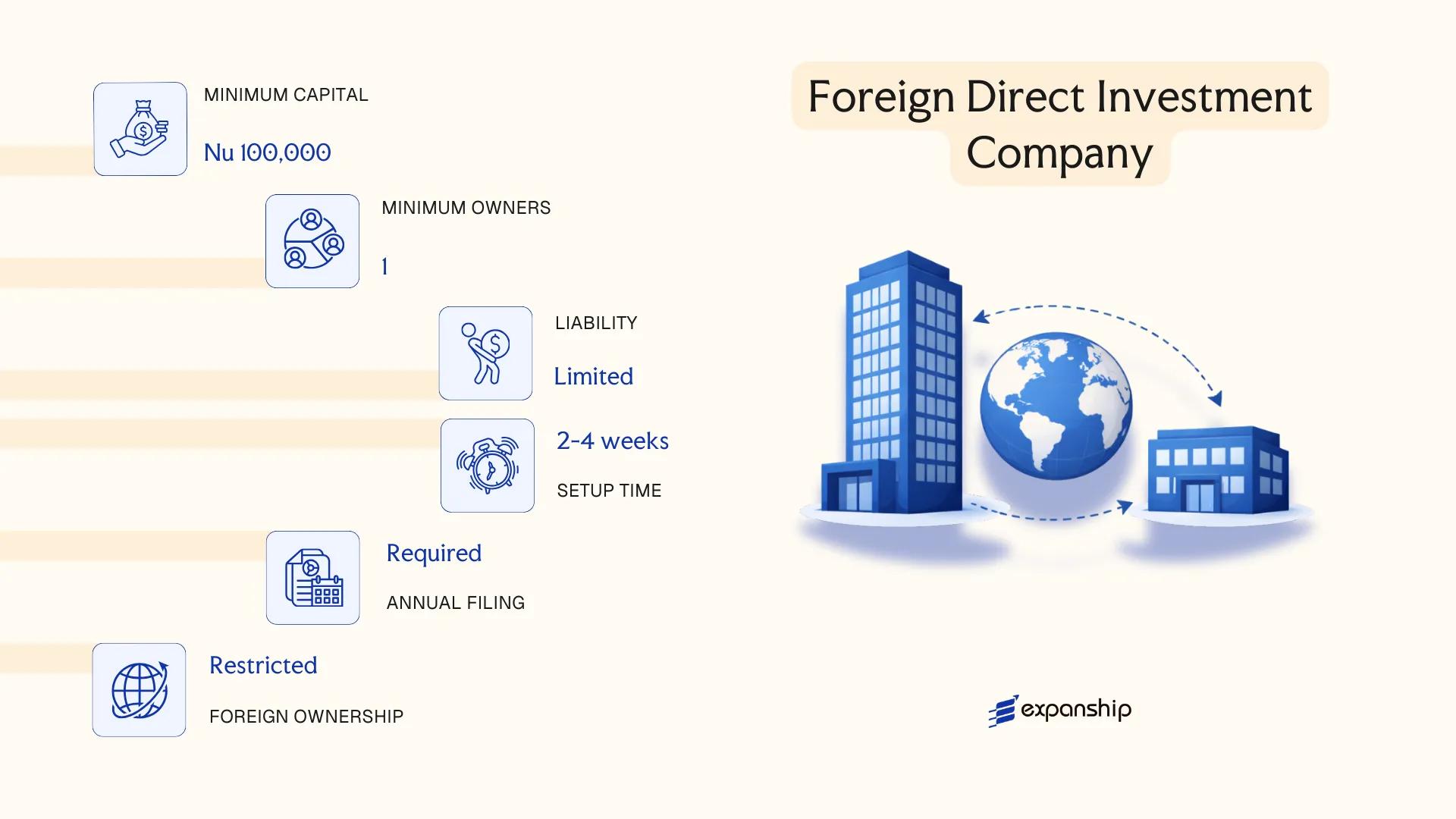

Foreign Direct Investment (FDI) Company

Bhutan regulates foreign direct investment companies primarily through the Foreign Direct Investment Policy and the Companies Act of Bhutan 2016, administered by the Bhutan Economic Forum for Innovative Transformation (BEFIT) and the Department of Industry under the Ministry of Economic Affairs. A foreign direct investment company in Bhutan is incorporated as a distinct legal entity with separate legal personality and limited liability, structured similarly to a private limited company but subject to additional FDI-specific conditions and approvals.

Foreign investors cannot hold equity in all sectors equally. Certain industries are reserved exclusively for Bhutanese nationals, others permit joint ventures with defined foreign equity caps, and specific sectors allow up to 100% foreign ownership. Approval from the relevant line ministry is required before registration proceeds with the Office of the Companies Registrar (OCR).

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private limited company with FDI approval | Incorporated under the Companies Act 2016 with additional FDI licensing |

| Members | Minimum 2 shareholders; no prescribed maximum | At least one director required; foreign directors permitted |

| Local Presence | Registered office in Bhutan required | A local Bhutanese joint venture partner may be mandated depending on sector |

| Capital | Minimum paid-up capital varies by sector (generally BTN 10 million or equivalent) | Specified in the FDI Policy; capital must be remitted through approved banking channels |

| Foreign Equity Cap | Ranges from 0% to 100% depending on sector | Restricted list, permitted list, and open list categories apply |

| Privacy | Shareholder and director details filed with OCR | Register is accessible to authorities; not fully private |

Focus Points

- Taxation: Subject to corporate income tax at 30% on net profit; Business Income Tax (BIT) applies; sales tax and customs duties may apply on imports; withholding tax applies to dividends and service payments remitted abroad.

- Repatriation: Profit and dividend repatriation is permitted subject to Royal Monetary Authority (RMA) approval and applicable foreign exchange regulations.

- Annual Compliance: Annual returns, audited financial statements, and tax filings must be submitted to the OCR and Department of Revenue and Customs respectively.

- Sector Restrictions: FDI is prohibited in certain sectors including retail trade below specified thresholds, religious institutions, and defence-related activities.

- Treaty Access: Bhutan has a limited double tax treaty network; treaty benefits are accordingly narrow for most foreign investors.

Closing

An FDI company suits foreign investors seeking operational presence in sectors such as hospitality, hydropower ancillaries, manufacturing, or technology services, with the key advantage of full legal recognition as a locally incorporated entity. The principal limitation is the sector-specific ownership ceiling and the multi-agency approval process, which can extend the setup timeline considerably.

Foreign businesses entering Bhutan through a joint venture or sector-specific licensing arrangement that requires a locally incorporated operational entity.

Foreign Business Entities [Branch Office, Representative Office, Project Office]

Foreign companies seeking a presence in Bhutan without incorporating a separate local entity can do so through three recognised structures. Foreign branch office registration in Bhutan is governed by the Companies Act of Bhutan 2016, administered by the Registrar of Companies under the Ministry of Industry, Commerce and Employment. None of these structures constitute a separate legal person — each remains an extension of the parent company, which retains full legal liability for the entity's activities in-country.

Approval from the Foreign Investment Promotion Division (FIPD) of the Department of Industry is generally required before registration, and the permitted scope of activities differs materially across all three structures.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Extension of foreign parent company | No separate legal personality; parent bears full liability |

| Authorised Representative | Appointed local representative or manager required | Must be resident in Bhutan |

| Local Presence | Registered office address mandatory | Physical office required; virtual offices generally not accepted |

| Capital | No universal statutory minimum; project-specific thresholds may apply | FDI minimum capital rules under FIPD guidelines may apply separately |

| Permitted Activities | Varies by structure (commercial, liaison, or project-specific) | Branch may earn revenue; representative and project offices face restrictions |

| Privacy | Parent company details disclosed on registration | Public register maintained by Registrar of Companies |

Focus Points

- Taxation: Branch offices are subject to corporate income tax at the standard rate on Bhutan-sourced income; representative and project offices with no revenue generation may have limited tax exposure, though withholding tax obligations on payments to the parent can still apply.

- Economic Substance: No formal substance regime equivalent to offshore financial centres applies, but physical presence and operational requirements are enforced through licensing conditions.

- Annual Compliance: Annual renewal of business licences, filing of audited accounts, and reporting to FIPD are standard obligations for active entities.

- Restrictions: Representative offices are prohibited from conducting revenue-generating commercial activities; project offices are limited strictly to the scope of the approved contract or project.

- Conversion: Conversion from a branch or representative structure to a locally incorporated entity requires a separate application and does not carry forward automatically.

Sub-Types

Branch Office

A branch office may conduct commercial operations and generate revenue, subject to sectoral approvals. It is the most operationally active of the three structures and is commonly used by foreign firms entering trade or service sectors.

Representative Office

Permitted activities are confined to market research, liaison, and promotional functions on behalf of the parent. A Bhutan representative office setup does not permit direct sales or contract execution in-country.

Project Office

A project office in Bhutan is established for the duration of a specific contract or infrastructure project, typically awarded by a government body or state enterprise. Once the project concludes, the office must be wound down or converted.

Closing

Foreign business entities in Bhutan suit multinational firms testing market entry, fulfilling a specific contract, or maintaining a liaison presence before committing to full incorporation. The primary advantage is speed of setup relative to incorporating a new company; the principal limitation is restricted operational scope, particularly for representative and project structures.

Foreign companies with an existing contract in Bhutan, or those conducting preliminary market assessment before pursuing full local incorporation.

Partnerships [General Partnership, Limited Partnership]

Partnership registration in Bhutan is governed by the Companies Act of Bhutan 2000, along with its subsequent amendments, which recognise both general and limited partnership structures. Partnerships do not possess a separate legal personality distinct from their partners, meaning the partners themselves bear direct legal responsibility for the obligations of the business.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Partnership (General or Limited) | No separate legal personality; governed under the Companies Act of Bhutan 2000 |

| Members | Partners (minimum 2) | General Partnership: all partners; Limited Partnership: at least one general and one limited partner |

| Liability | Unlimited (GP); Mixed (LP) | General partners bear unlimited liability; limited partners are liable only to the extent of their capital contribution |

| Local Presence | Registered office in Bhutan required | Must maintain a principal place of business within the country |

| Capital | No statutory minimum; denominated in Ngultrum (BTN) | Capital contributions are defined in the partnership agreement |

| Privacy | Partnership deed is filed with the Office of the Attorney General | Deed contents may be accessible to regulators |

Focus Points

- Taxation: Partnerships are generally taxed at the partner level under Bhutan's Business Income Tax framework; partners declare their share of profits individually, though specific withholding and indirect tax obligations depend on the nature of business activities.

- Annual Compliance: Partners must file annual returns and maintain updated records with the relevant authority; the partnership deed must reflect any changes in partner composition.

- Restrictions: Foreign nationals face limitations on direct participation in certain sectors; partnership eligibility for FDI purposes is restricted and generally not the preferred structure for foreign investors.

- Conversion: Conversion from a partnership to a company structure is possible but requires formal dissolution or restructuring procedures under the applicable legislation.

- Treaty Access: Partnerships may have limited access to Bhutan's double taxation agreements, as treaty benefits typically apply to entities recognised as tax residents with distinct legal personality.

Sub-Types

General Partnership

All partners in a general partnership share equal management rights and bear unlimited personal liability for the debts and obligations of the firm. This structure is commonly used for small professional practices or family-run trading businesses where partners maintain direct operational control.

Limited Partnership

A limited partnership separates management responsibility from passive investment: general partners manage the business and carry unlimited liability, while limited partners contribute capital and bear liability only to the extent of that contribution. This structure suits arrangements where investors wish to participate financially without taking on management duties or unlimited personal exposure.

Closing Paragraph and Recommendations

Partnerships suit smaller domestic ventures, professional service arrangements, or family businesses where partners are known to one another and operational simplicity is prioritised. The absence of a minimum capital requirement lowers the entry barrier, though unlimited liability for general partners represents a material risk that should factor into any structural decision.

Partnerships in Bhutan are most appropriate for small-scale domestic businesses or professional collaborations between Bhutanese nationals, particularly where the partners prefer a straightforward governance structure over the formality of a corporate entity.

Sole Proprietorship

A sole proprietorship in Bhutan is the most basic business structure available to individual entrepreneurs, governed under the Companies Act of Bhutan 2016 and administered through the Office of the Registrar of Companies under the Ministry of Economic Affairs. Unlike a private limited company, this structure does not confer separate legal personality on the business — the proprietor and the business are legally the same person, meaning personal assets are exposed to business liabilities without limitation.

Registration is handled through Bhutan's online business registration portal, and the process is comparatively straightforward. Foreign nationals face significant restrictions; Bhutan sole trader registration is generally reserved for Bhutanese citizens, reflecting the country's broader policy on foreign participation in small-scale trade.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated sole trader | No separate legal personality from the owner |

| Members | Single proprietor | Must be a Bhutanese citizen; one owner only |

| Local Presence | Physical business address required | Must maintain a registered place of business in Bhutan |

| Capital | No statutory minimum | Declared in the registration application |

| Liability | Unlimited personal liability | Proprietor bears all business debts personally |

| Privacy | Owner name is publicly registered | No meaningful privacy protection for the proprietor |

Focus Points

- Taxation: Subject to personal income tax on business profits under the Income Tax Act; no separate corporate income tax applies, as income flows directly to the proprietor.

- Annual Compliance: Annual renewal of the business licence is required; financial records must be maintained but audit requirements are less demanding than for incorporated entities.

- Restrictions: Foreign nationals are generally ineligible; activity scope may be limited by sector-specific licensing requirements.

- Conversion: Can be converted into a private limited company if the business grows, though this requires fresh incorporation rather than a simple structural amendment.

Closing

A sole proprietorship suits individual Bhutanese citizens running small-scale trading, service, or artisanal businesses where administrative overhead must be kept low. The principal limitation is unlimited personal liability, which exposes the proprietor's personal assets to any business obligation.

Bhutanese citizens operating small, low-risk, owner-managed businesses who do not require external investment or a formal corporate structure.

How to Choose the Right Entity Type in Bhutan

Choosing the right business entity in Bhutan is a structural decision with direct legal and financial consequences that persist for the life of the company.

Why Your Entity Choice Matters

A misaligned structure creates concrete operational and regulatory problems:

- Registering as a foreign business entity when you intend to conduct ongoing commercial activity with Bhutanese residents places you in breach of the Companies Act of Bhutan 2016, exposing the business to penalties or deregistration.

- Selecting a structure that does not qualify as a tax resident entity under Bhutanese law forfeits access to any applicable double taxation relief.

- Choosing an entity that mandates audited financial statements for a single-person consultancy introduces recurring compliance costs that a sole proprietorship would not require.

- Forming a private limited company when your activity is purely asset-holding locks you into annual shareholder meeting obligations and directorship requirements that may be disproportionate to the business purpose.

Key Factors to Consider

- Business Activity: Active trading, regulated sector operations, and passive asset-holding each point toward distinct entity structures under Bhutanese law.

- Ownership Structure: Single-owner operations align with sole proprietorships or private limited companies, while multi-party arrangements may require a partnership or company with a defined shareholder agreement.

- Foreign Ownership: FDI companies must meet sector-specific thresholds and receive approval from the Department of Industry under the Foreign Direct Investment Policy.

- Tax Position: Your need for treaty access, full exemption, or standard corporate tax treatment determines which structures are viable.

- Substance Capacity: If you cannot maintain a physical presence and local decision-making, certain entity types will expose your firm to compliance failures.

- Exit Flexibility: Confirm whether your chosen structure permits conversion, redomiciliation, or voluntary winding-up under the Companies Act before committing.

Compliance Services for Companies in Bhutan

Ongoing compliance support for Bhutanese entities, covering annual filings, statutory obligations, and regulatory reporting.

Conclusion

Selecting the right structure from this Bhutan company incorporation conclusion guide comes down to matching your ownership profile, operational scope, and capital requirements to what the law actually permits. Private Limited Companies remain the most commonly registered vehicle, favored by resident entrepreneurs and foreign joint venture partners under the Companies Act of Bhutan 2016. State-Owned Enterprises serve public mandates rather than private investors. FDI Companies apply where full or majority foreign ownership is permitted under the FDI Policy. Branch and Representative Offices suit firms testing the market before committing to a subsidiary. Partnerships and Sole Proprietorships address smaller, domestically oriented operations.

Bhutan's regulatory environment continues to evolve, with the Ministry of Economic Affairs periodically revising its FDI-approved sectors list. Your choice of entity will affect everything from repatriation rights to audit obligations under the Ministry of Finance.

How Expanship Can Assist You

Expanship's company formation services in Bhutan cover the full range of entities examined in this blog — from Private Limited Companies and FDI Companies to Branch Offices and Partnerships. Each structure carries distinct registration requirements under the Companies Act of Bhutan 2016, and filings are processed through the Ministry of Economic Affairs (MoEA). Our team works directly with these regulatory processes so your setup is structured correctly from the start.

Bhutan business registration assistance from Expanship includes:

- Document preparation, notarization, and legalization

- Registered agent and registered office provision

- Government filing and MoEA liaison

- Post-incorporation compliance management

- Banking introduction assistance

Every engagement is handled by specialists who work within Bhutan's regulatory framework — not generalists applying a generic process to an unfamiliar market.

To discuss your specific requirements, contact Expanship Bhutan directly.

Frequently Asked Questions (FAQ)

The Private Limited Company is the most frequently registered structure. It permits up to 30 shareholders, limits personal liability, and suits small to mid-sized domestic ventures without requiring public disclosure of financials.

An FDI Company operates under conditions set by the FDI Policy and requires approval from the Department of Industry under the Ministry of Economic Affairs, whereas a Private Limited Company is registered for domestic operations without foreign ownership restrictions. FDI entities may face sector-specific equity caps, and compliance obligations differ accordingly.

A Private Limited Company discloses less publicly than a Public Limited Company, which must publish audited financial statements. Nominee arrangements are subject to the regulatory framework under the Companies Act; any nominee service must comply with Bhutan's anti-money laundering requirements.

A sole proprietorship requires only one individual. Private and Public Limited Companies require at least one director and one shareholder, but a General Partnership mandates a minimum of two partners, and a Limited Partnership similarly requires at least one general and one limited partner.

Foreigners may register an FDI Company, a Branch Office, a Representative Office, or a Project Office. Direct registration of a Private Limited Company by a foreign national generally requires FDI Policy compliance and sector clearance from the relevant ministry.

The Companies Act of Bhutan 2016 provides for re-registration of companies, allowing a Private Limited Company to convert to a Public Limited Company subject to meeting the requisite shareholder and capital thresholds. Conversion from a company structure to a sole proprietorship or partnership is not a continuation process under the same legal framework.

Public Limited Companies, Private Limited Companies, State-Owned Enterprises, and FDI Companies each hold separate legal personality distinct from their owners. Sole proprietorships and general partnerships do not carry this separation, meaning personal assets remain exposed to business liabilities.

A sole proprietorship has the most limited reporting requirements, with no mandatory audit or board governance. By contrast, Public Limited Companies carry the highest compliance burden, including annual audits, shareholder meetings, and regulatory filings with the Registrar of Companies.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.