Key Takeaways

- Brazil's corporate framework is primarily governed by two legislative instruments: the Lei das Sociedades Anônimas (Law No. 6,404/1976) for joint stock companies and the Código Civil (Law No. 10,406/2002) for most other entity types.

- The Sociedade Limitada (Ltda.) remains the most registered business entity in Brazil, valued for its structural flexibility and comparatively lower compliance burden relative to the S.A.

- Company registration in Brazil falls under the jurisdiction of the state-level Junta Comercial, with federal coordination handled by the Departamento Nacional de Registro Empresarial e Integração (DREI) through the Redesim system.

- EIRELI is no longer available for new registrations following legislative changes in 2021, though entities formed prior to that change continue to exist and operate under that structure.

Introduction to Entity Types in Brazil

Brazil is the largest country in South America, sharing borders with every South American nation except Chile and Ecuador. As a federative republic, it operates under a civil law system heavily influenced by the 1976 Corporations Law (Lei das Sociedades por Ações, Law No. 6,404/1976) and the 2002 Civil Code (Law No. 10,406/2002), which together govern most corporate structures. Company registration falls under the jurisdiction of the Junta Comercial (Commercial Registry) in each state, with federal oversight coordinated through the Departamento Nacional de Registro Empresarial e Integração (DREI).

Brazil operates a worldwide taxation system, meaning resident entities are taxed on global income.

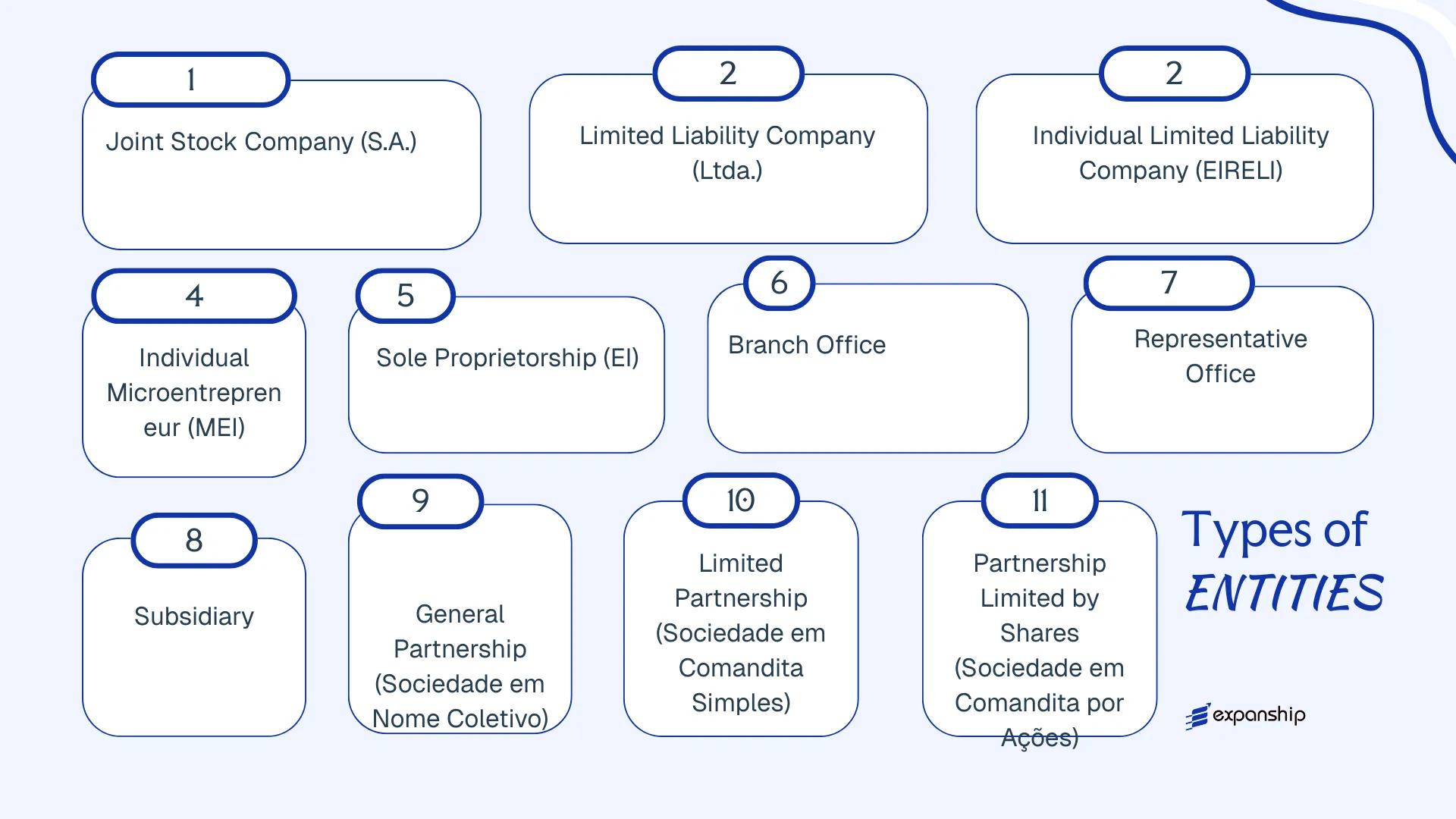

Depending on your business objectives and ownership structure, several legal entities in Brazil are available: Sociedade Anônima (S.A.), Sociedade Limitada (Ltda.), Empresa Individual de Responsabilidade Limitada (EIRELI), Microempreendedor Individual (MEI), Empresário Individual (EI), branch offices, representative offices, and various partnership structures under Brazilian corporate structures overview.

Each of these types of business entities in Brazil carries distinct incorporation requirements, liability implications, and tax treatment — all of which the following sections examine in detail.

An Overview of Business Structures in Brazil

Brazilian company law provides several distinct entity types, each governed primarily by the Lei das Sociedades Anônimas (Law 6.404/1976) for share-based companies and the Código Civil (Law 10.406/2002) for most other commercial and simple society forms. A further category — the individual microentrepreneur — operates under the Lei Complementar 128/2008. Each structure carries different rules on liability, membership, and permitted commercial activity.

| Entity Type | Legal Form | Liability | Tax Treatment | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Sociedade Anônima (S.A.) | Joint Stock Company | Limited to shares | Corporate tax (IRPJ/CSLL) | Yes | 2 shareholders | DREI / CVM (public S.A.) | Law 6.404/1976 |

| Sociedade Limitada (Ltda.) | LLC | Limited to capital | Corporate tax (IRPJ/CSLL) | Yes | 1 member | DREI / Junta Comercial | Civil Code 2002 |

| EIRELI | Individual LLC | Limited to capital | Corporate tax (IRPJ/CSLL) | Yes | 1 individual | DREI / Junta Comercial | Law 12.441/2011 |

| Microempreendedor Individual (MEI) | Sole trader | Unlimited | SIMEI (flat rate) | Yes | 1 individual | DAS / Junta Comercial | LC 128/2008 |

| Empresário Individual (EI) | Sole proprietorship | Unlimited | Varies by regime | Yes | 1 individual | Junta Comercial | Civil Code 2002 |

| Branch Office | Foreign branch | Parent liable | Corporate tax (IRPJ/CSLL) | Yes | Parent company | DREI / MDIC | Civil Code 2002 |

| Representative Office | Liaison office | Parent liable | Limited / exempt | Restricted | Parent company | MDIC | Civil Code 2002 |

| Sociedade Simples | Simple society | Unlimited | Corporate tax | Yes | 2 partners | Registro Civil PJ | Civil Code 2002 |

| Sociedade em Nome Coletivo | General partnership | Unlimited | Corporate tax | Yes | 2 partners | Junta Comercial | Civil Code 2002 |

| Sociedade em Comandita Simples | Limited partnership | Mixed | Corporate tax | Yes | 2 partners | Junta Comercial | Civil Code 2002 |

| Sociedade em Comandita por Ações | Share-based partnership | Mixed | Corporate tax | Yes | 2 shareholders | DREI / Junta Comercial | Law 6.404/1976 |

Each of these structures is examined in full in the sections below.

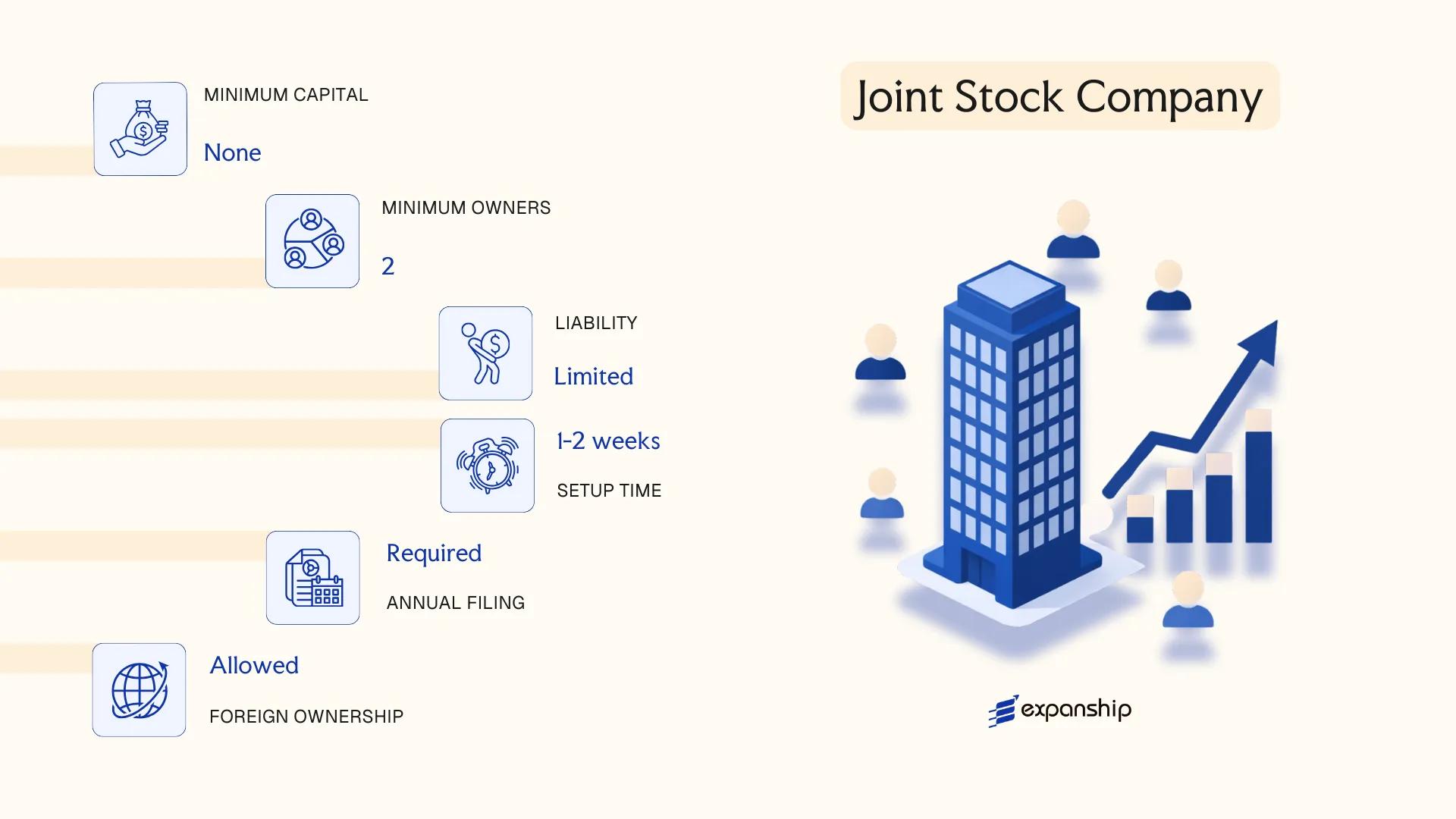

Sociedade Anônima (S.A.) — Joint Stock Company

Governed by Law No. 6,404/1976 (the Brazilian Corporations Law), the Sociedade Anônima SA Brazil formation process produces a capital-based entity with full separate legal personality. Shareholders' liability is limited to the price of shares they subscribe or acquire, leaving personal assets shielded from corporate obligations.

Capital is divided into shares, which can be freely transferred without amending the articles of association — a structural feature that distinguishes this form from the Ltda. The S.A. can be either publicly held (aberta) or privately held (fechada), each carrying distinct regulatory obligations under the Comissão de Valores Mobiliários (CVM), Brazil's securities regulator.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Corporation (Joint Stock Company) | Separate legal personality; governed by Law 6,404/1976 |

| Members | Shareholders (acionistas) | Minimum 2 shareholders; no maximum; managed by a Board of Directors (Conselho de Administração) and/or Executive Officers (Diretores) |

| Capital | BRL — no statutory minimum for fechada; publicly held companies subject to CVM rules | Divided into shares; can include common (ordinárias) and preferred (preferenciais) shares |

| Local Presence | Registered address in Brazil required; at least one resident Diretor | Director must be domiciled in Brazil per Art. 146 of Law 6,404/1976 |

| Governance | Board of Directors mandatory if publicly held; optional for fechada | Fiscal Council (Conselho Fiscal) may be permanent or convened on request |

| Privacy | Shareholder register maintained internally; publicly held companies must disclose to CVM | Fechada entities have limited public disclosure obligations |

Focus Points

- Taxation: Corporate income tax (IRPJ) at 15% plus a 10% surtax on profits exceeding BRL 240,000/year; Social Contribution on Net Income (CSLL) at 9% for most sectors; PIS/COFINS on gross revenue; withholding tax on dividends currently exempt under domestic law, though proposed reforms may alter this — refer to Receita Federal for current guidance.

- Annual Compliance: Annual general meeting (Assembleia Geral Ordinária) required within four months of fiscal year-end; audited financial statements mandatory for publicly held S.A.s and large privately held ones.

- Treaty Access: Qualifies as a resident entity for purposes of Brazil's tax treaty network; treaty benefits depend on structure and substance.

- Conversion: An S.A. may be converted to an Ltda. or other form by unanimous shareholder approval, subject to procedural requirements under Law 6,404/1976.

- Restrictions: Foreign shareholders are permitted; certain regulated sectors impose nationality or local-control requirements on shareholders or directors.

Sub-Types

S.A. Aberta (Publicly Held)

Shares are admitted to trading on a regulated exchange or OTC market supervised by the CVM. This sub-type is subject to continuous disclosure obligations, mandatory external audit, and stricter governance standards under CVM regulations.

S.A. Fechada (Privately Held)

Shares are not publicly traded, and the entity faces lighter regulatory requirements than its aberta counterpart. This structure is the standard choice for foreign-owned operating companies, holding vehicles, and joint ventures where public fundraising is not intended.

When to Use an S.A.

The S.A. suits businesses requiring a scalable shareholding structure — equity investment, multi-party joint ventures, or eventual public listing. The freely transferable share mechanism simplifies investor entry and exit. The main drawback is administrative overhead: governance requirements, mandatory meetings, and potential audit obligations make it more operationally demanding than an Ltda.

The S.A. is best suited for larger enterprises, foreign investors seeking equity flexibility, and businesses planning to raise third-party capital or pursue a future public offering.

Company Incorporation in Brazil

Incorporate an S.A. or other Brazilian entity with end-to-end support from registration through post-incorporation compliance.

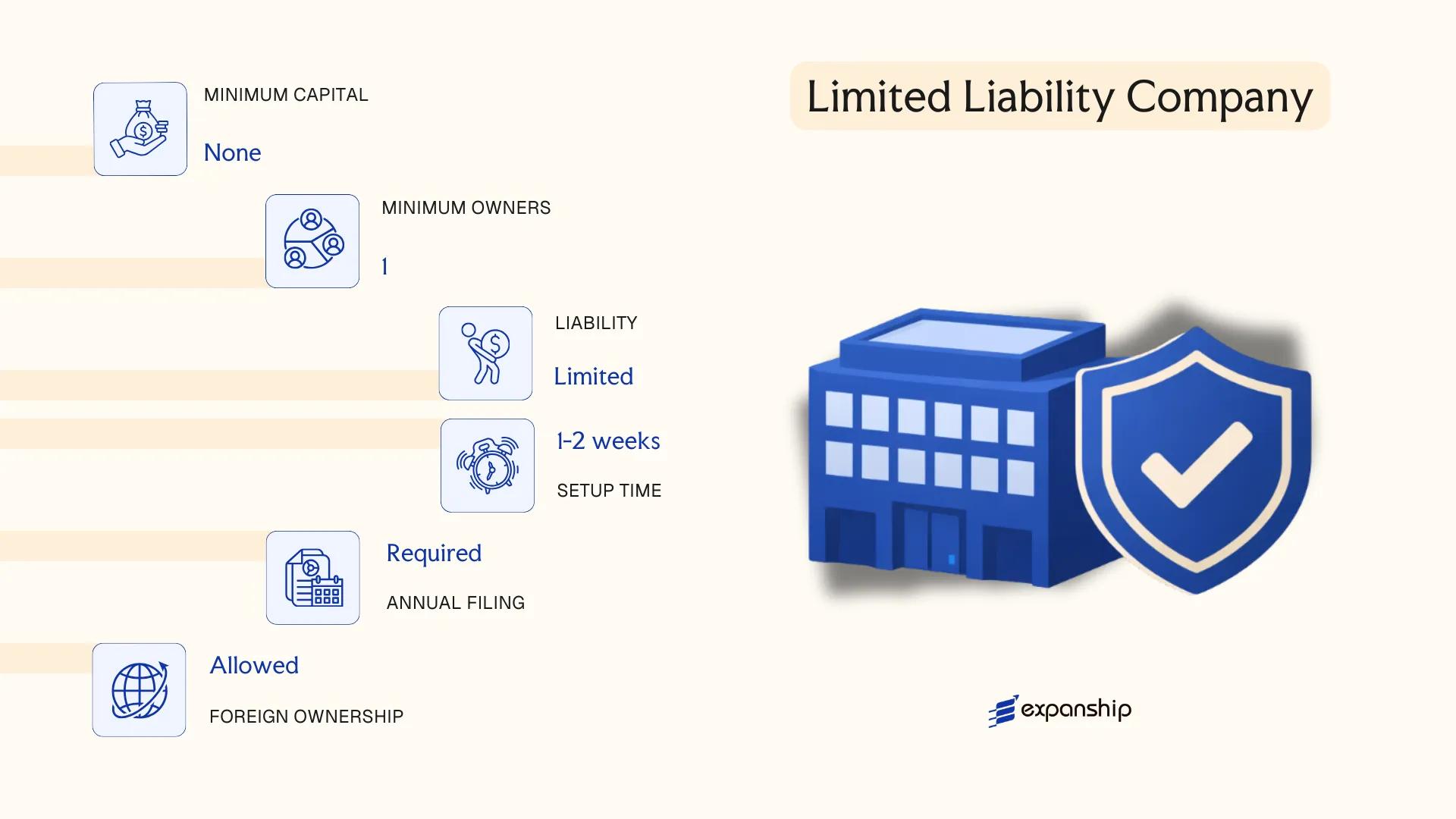

Sociedade Limitada (Ltda.) — Limited Liability Company

Sociedade Limitada Ltda Brazil registration is governed by the Brazilian Civil Code (Lei nº 10.406/2002), specifically Articles 1.052 to 1.087, which establish the entity as a distinct legal person separate from its owners. Liability is confined to each quotaholder's subscribed capital, though all members bear joint responsibility until the share capital is fully paid up.

Structurally, the Ltda. sits between a sole proprietorship and a publicly held corporation. Its governance is comparatively flexible, making it the most widely adopted business vehicle for both domestic and foreign investors operating in the country.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Company (Ltda.) | Governed by Civil Code, Arts. 1.052–1.087 |

| Members | Quotaholders; minimum 2, no statutory maximum | Since 2021, a single-quotaholder Ltda. is permitted under Lei nº 14.195/2021 |

| Management | One or more administrators (administradores); need not be quotaholders | Administrators must be resident in Brazil or hold a valid Brazilian visa with powers of attorney arrangements in practice |

| Local Presence | Registered address in Brazil required | A fiscal address (sede) must be maintained; a registered agent is not a statutory requirement but is common in practice |

| Share Capital | Denominated in Brazilian Reais (BRL); no statutory minimum | Capital is divided into quotas; full payment timeline should be stipulated in the articles |

| Privacy | Quotaholder names disclosed in the articles filed at the Junta Comercial | Beneficial ownership data reported to Receita Federal under current regulations |

Focus Points

- Taxation: Subject to federal corporate income tax (IRPJ) at 15% plus a 10% surtax on profits exceeding BRL 240,000 annually, social contribution on net income (CSLL) at 9%, PIS/COFINS contributions, and ISS or ICMS depending on activity; eligible for Simples Nacional or Lucro Presumido regimes depending on annual revenue thresholds.

- Annual Compliance: Must file annual income tax returns with Receita Federal, maintain statutory books, hold quotaholder meetings where required, and submit Sped (Sistema Público de Escrituração Digital) records electronically.

- Conversion: Can be converted into a Sociedade Anônima or restructured as a single-member Ltda. through an amendment to the articles registered at the Junta Comercial.

- Treaty Access: As a Brazilian tax resident entity, the Ltda. can access Brazil's network of double taxation agreements for applicable income streams.

- Foreign Ownership: Foreign quotaholders are permitted; however, foreign-owned entities must appoint a Brazilian-resident attorney-in-fact (procurador) with broad powers.

Closing

The Ltda. suits trading operations, service businesses, and holding structures where operational flexibility matters and public capital markets access is not required. Its primary structural limitation is that transferring quotas to third parties requires compliance with existing quotaholder pre-emption rights under the Civil Code, which can complicate exits.

The Ltda. is well suited to foreign investors and SMEs seeking a flexible, cost-efficient operating entity in Brazil without the administrative burden of a publicly held structure.

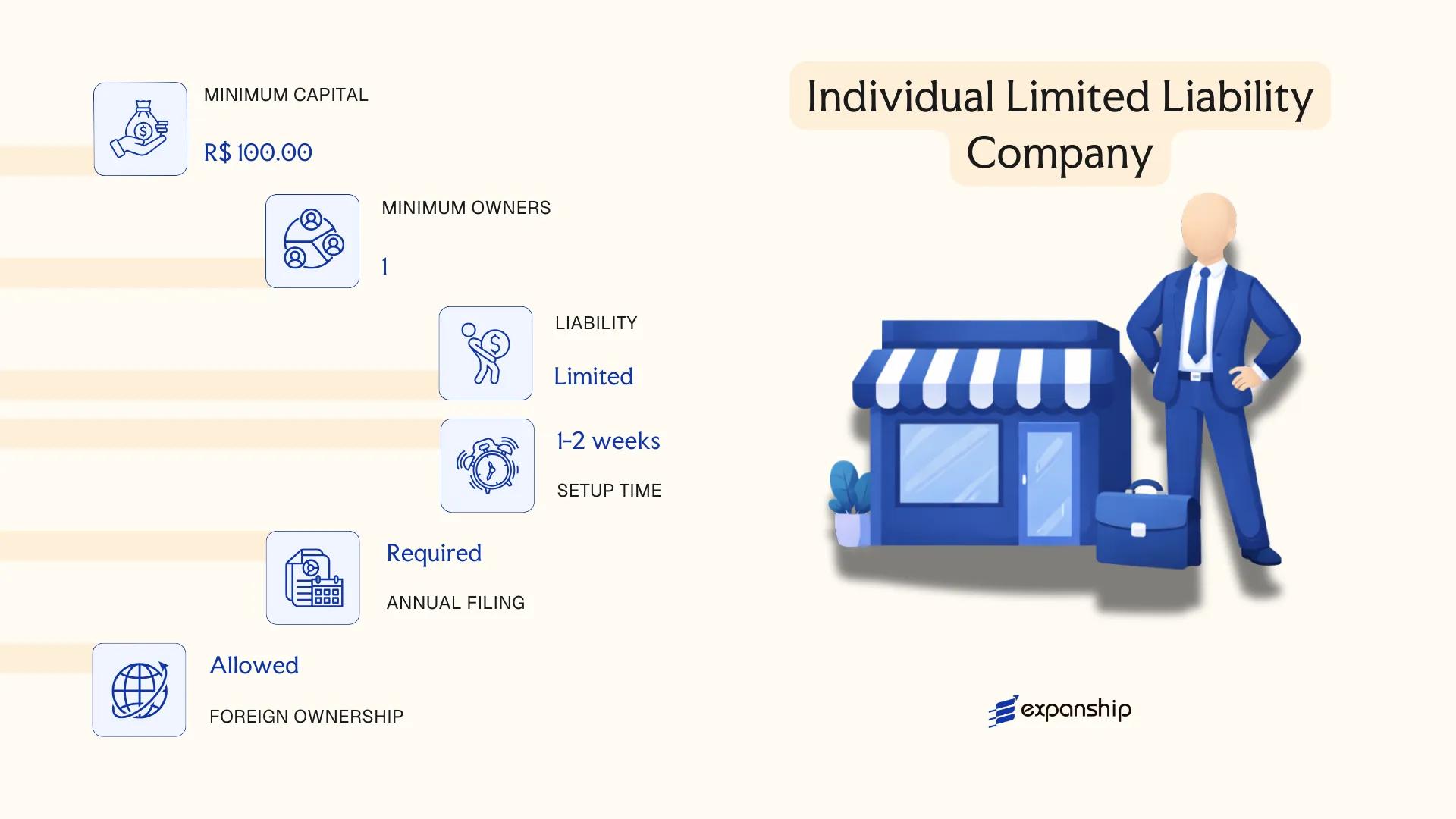

Empresa Individual de Responsabilidade Limitada (EIRELI) — Individual Limited Liability Company

Introduced by Law No. 12,441/2011, the EIRELI Brazil individual limited liability company was designed to allow a single natural or legal person to operate a business with full separation between personal and corporate assets. Unlike a sole proprietorship, it carries distinct legal personality, shielding the owner from personal liability beyond their subscribed capital contribution.

Registered with the Junta Comercial (state commercial registry) and recorded with the CNPJ through the Receita Federal, the entity functions as a hybrid form: structurally resembling a Ltda. in governance, yet held entirely by one person. As of late 2021, Law No. 14,195/2021 formally discontinued the EIRELI as a new registration category, absorbing its function into the Empresário Individual with limited liability provisions. Existing EIRELIs were automatically converted to Sociedade Limitada Unipessoal (SLU).

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Separate legal entity with limited liability | Governed originally by Art. 980-A of the Civil Code |

| Member Title | Titular (owner/holder) | Single natural or legal person permitted |

| Membership | 1 only | No minimum or maximum beyond sole ownership |

| Local Presence | Registered address in Brazil; CNPJ registration mandatory | Registered with the relevant Junta Comercial |

| Minimum Capital | 100x the national minimum wage at time of registration | Must be fully subscribed at incorporation |

| Privacy | Name and CNPJ publicly listed in commercial registry | Beneficial ownership disclosed to Receita Federal |

Focus Points

- Taxation: Subject to federal corporate income tax (IRPJ) and CSLL, plus PIS/COFINS on revenue, and ISS or ICMS depending on activity; eligible for Simples Nacional if within revenue thresholds.

- Conversion: Automatically converted to Sociedade Limitada Unipessoal (SLU) under Law No. 14,195/2021; no new EIRELI registrations are accepted.

- Annual Compliance: Annual declaration filings with the Receita Federal and bookkeeping obligations under Brazilian accounting standards (CFC norms) apply.

- Restrictions: Cannot be owned by another EIRELI; a natural person may hold only one EIRELI simultaneously.

- Treaty Access: Subject to standard Brazilian tax treaty provisions; no preferential treatment distinct from other domestic entities.

Closing

EIRELI was most commonly used for small service businesses, freelancers formalising operations, and sole traders requiring liability protection without partners. Its primary advantage was single-person ownership with limited liability; the key drawback was the relatively high minimum capital requirement tied to the minimum wage.

Existing EIRELI holders operating as sole traders who have been transitioned to SLU status and need to understand their current compliance standing under the post-2021 framework.

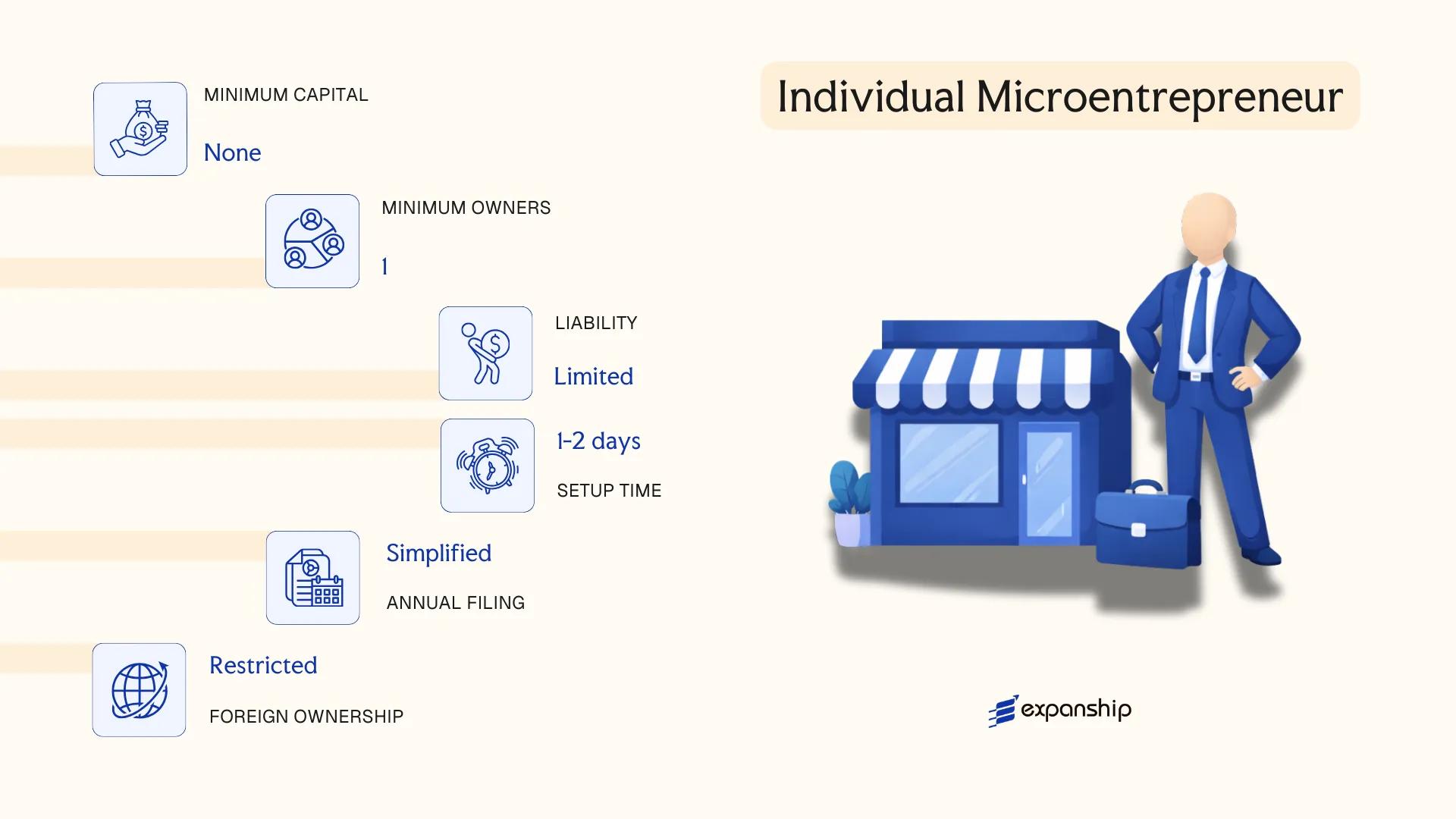

Microempreendedor Individual (MEI) — Individual Microentrepreneur

MEI registration Brazil microentrepreneur status is governed by Complementary Law No. 128/2008, which amended the General Law for Micro and Small Enterprises (Complementary Law No. 123/2006). The category was created specifically for self-employed workers operating informally, providing a formalized legal identity without the administrative burden associated with full corporate structures.

Registration is conducted exclusively through the Portal do Empreendedor, administered by the Federal government. Upon registration, the MEI acquires a CNPJ (Cadastro Nacional da Pessoa Jurídica), enabling access to banking services, social security coverage, and the right to issue invoices (notas fiscais).

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Individual entrepreneur with CNPJ | Not a separate legal entity; liability is not fully shielded |

| Proprietor | Single individual (proprietor) | Minimum and maximum: 1 person; cannot have partners |

| Annual Revenue Limit | BRL 81,000 per year | Proportional limit applies in the year of registration |

| Local Presence | Brazilian resident required; business address mandatory | Proprietor must be domiciled in Brazil |

| Capital | No minimum capital requirement | No formal paid-up capital structure |

| Permitted Activities | Restricted to listed occupations only | CGSN Resolution No. 140/2018 defines eligible activity codes |

Focus Points

- Taxation: MEI falls under Simples Nacional with a fixed monthly DAS payment covering INSS, ISS (services), and ICMS (commerce/industry); corporate income tax (IRPJ) and PIS/COFINS are exempt at this tier.

- Employee Restriction: The entity may employ a maximum of one employee, paid at minimum wage or the applicable floor wage for the category.

- Annual Compliance: A single annual declaration, the DASN-SIMEI, must be submitted to the Receita Federal by 31 May of each year.

- Conversion Obligation: Exceeding the annual revenue ceiling triggers mandatory migration to Microempresa (ME) status, with loss of MEI tax benefits.

- Restrictions: MEI status is unavailable to public servants, retirees receiving certain benefits, and individuals already holding equity in another company.

Sole operators running low-volume service or trade activities benefit from MEI's minimal compliance overhead, though the hard revenue ceiling and restricted activity list limit its applicability as a business scales.

MEI is best suited for individual self-employed professionals or tradespeople formalizing a one-person operation with annual revenues well below BRL 81,000.

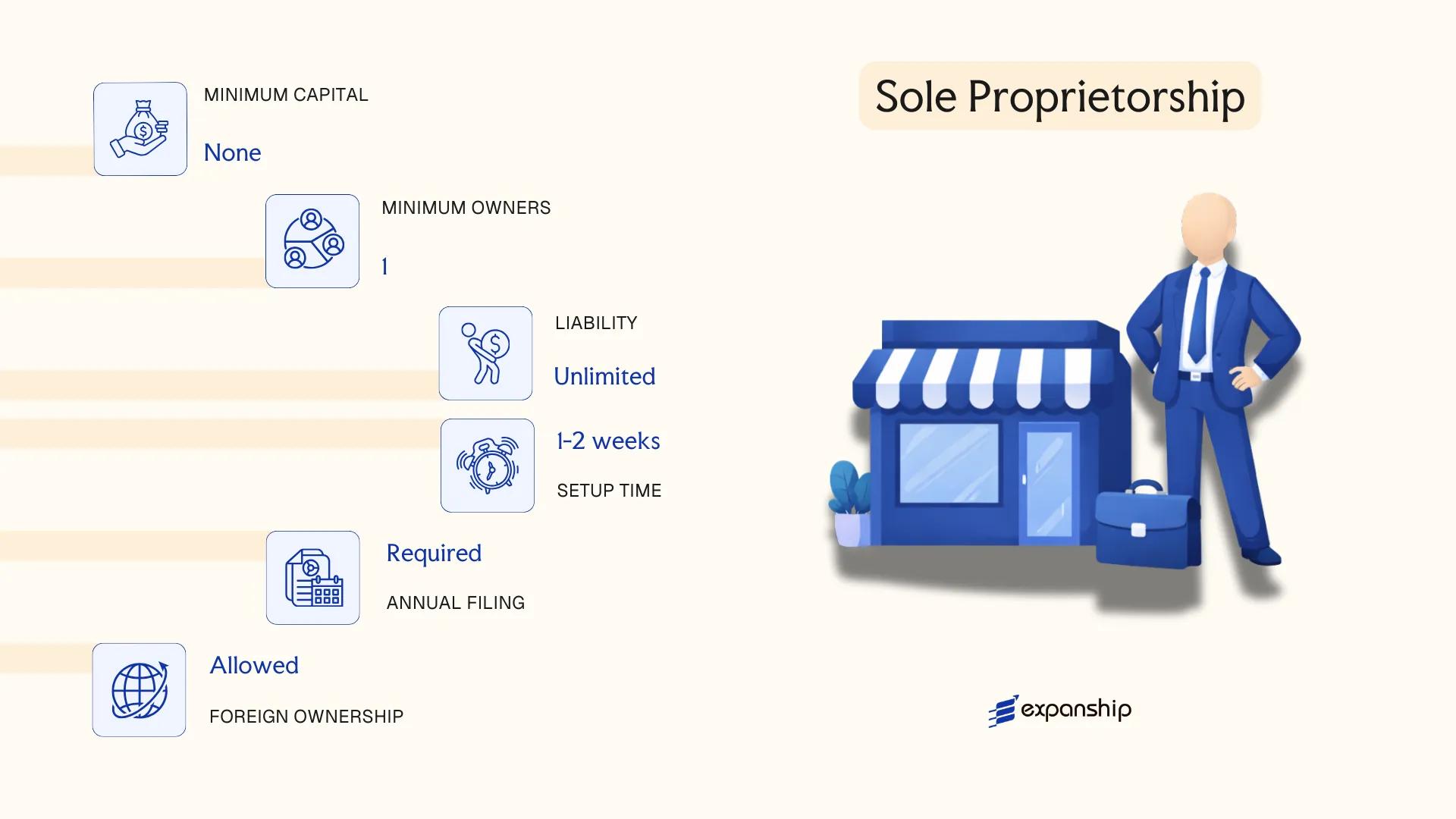

Empresário Individual (EI) — Sole Proprietorship

The Empresário Individual Brazil sole proprietorship structure is governed by the Brazilian Civil Code (Lei nº 10.406/2002), specifically Articles 966 to 969. Unlike a limited liability company, the EI does not constitute a separate legal entity distinct from its owner.

Full personal liability is the defining characteristic here. Your personal assets remain exposed to business debts and obligations, as no legal separation exists between you and the enterprise.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated sole proprietorship | No separate legal personality from the owner |

| Proprietor | Single individual (proprietor) | Only one natural person; legal entities cannot register as EI |

| Local Presence | Registered business address in Brazil | Must have a physical commercial address; a registered agent alone is insufficient |

| Capital | No statutory minimum; declared in BRL | Capital declared at registration but no paid-up requirement |

| Liability | Unlimited personal liability | Personal assets are fully reachable by creditors |

| Privacy | Owner's CPF (individual taxpayer number) linked publicly | Business records are publicly accessible via the Junta Comercial |

Focus Points

- Taxation: Subject to personal income tax (IRPF) under the Simples Nacional, Lucro Presumido, or Lucro Real regimes depending on annual revenue; no separate corporate tax applies, but ISS, ICMS, and PIS/COFINS obligations may arise depending on activity.

- Annual Compliance: Must file the Declaração de Imposto de Renda da Pessoa Física (DIRPF) and maintain bookkeeping records; registration is maintained through the Junta Comercial of the relevant state.

- Conversion: An EI can be converted to a Sociedade Limitada or EIRELI (where still applicable) without liquidation, under Article 1.113 of the Civil Code.

- Restrictions: Certain regulated professions and activities are prohibited from operating under this structure; intellectuals and professionals providing exclusively intellectual services must use Sociedade Simples instead.

- Treaty Access: As a pass-through entity taxed at the individual level, treaty benefits under Brazil's bilateral tax agreements generally apply to the proprietor directly, not to the business.

Closing

The EI structure suits individuals operating small commercial, industrial, or service activities who require a formal registration but face minimal third-party liability exposure. The primary advantage is administrative simplicity and low registration cost through the Junta Comercial; the significant drawback is unlimited personal liability, which makes it unsuitable for any activity carrying material financial or legal risk.

The Empresário Individual is best suited for individual traders or small operators in low-risk activities who need formal business registration without the overhead of a corporate structure.

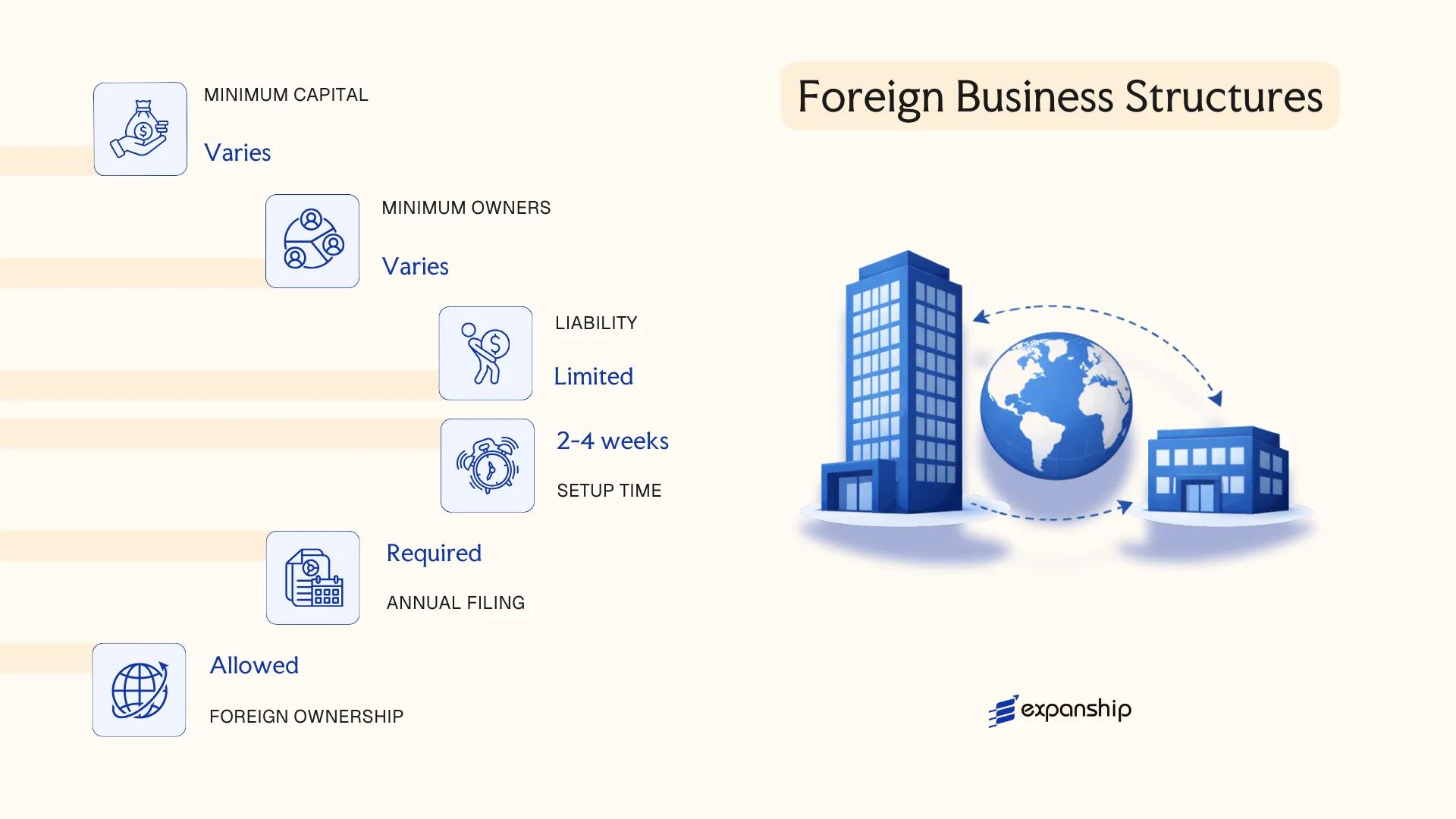

Foreign Business Structures in Brazil [Branch Office, Representative Office, Subsidiary]

A foreign company branch office Brazil registration is governed primarily by Articles 1,134 to 1,141 of the Brazilian Civil Code (Law No. 10,406/2002), which requires Presidential Decree authorisation before a branch can operate. Unlike a subsidiary, a branch does not hold separate legal personality — it remains an extension of the foreign parent, which bears unlimited liability for its Brazilian operations.

A representative office occupies a more restricted position: it may conduct market research and promotional activities but cannot execute commercial contracts or generate revenue directly. Formal registration still applies, typically through the Junta Comercial (state commercial registry) and the Receita Federal for tax enrolment purposes.

Key Characteristics

| Requirement | Branch Office | Representative Office | Subsidiary (Ltda. or S.A.) |

|---|---|---|---|

| Legal Personality | None (extension of parent) | None | Separate legal entity |

| Liability | Unlimited (parent bears full liability) | Unlimited (parent bears full liability) | Limited to subscribed capital |

| Authorisation | Presidential Decree required | Junta Comercial registration | Standard incorporation process |

| Local Representative | Mandatory Brazilian resident representative | Mandatory Brazilian resident representative | Local administrator required |

| Capital | No statutory minimum, but capital allocation must be declared | No statutory minimum | Varies by entity type |

| Permitted Activities | Full commercial operations | Non-commercial activities only | Unrestricted (within corporate object) |

Focus Points

- Taxation: Branches are taxed as Brazilian residents on Brazilian-sourced income; corporate income tax (IRPJ) applies at 15% plus a 10% surtax on profits exceeding BRL 20,000/month, with CSLL at 9%, and PIS/COFINS on gross revenues. Remittances to the foreign parent may attract withholding tax under domestic rules, subject to applicable tax treaty relief.

- Economic Substance: A branch must maintain genuine operational activity consistent with its stated corporate object; a dormant or shell branch carries regulatory risk.

- Annual Compliance: Annual financial statements, tax filings with the Receita Federal, and BACEN (Central Bank of Brazil) reporting for foreign capital registration under Resolution No. 4,373 or RDE-IED modules apply depending on the structure.

- Treaty Access: Subsidiaries incorporated as Brazilian legal entities generally access tax treaty benefits more straightforwardly than branches, where treaty application to permanent establishments can be subject to interpretation.

- Conversion: Converting a branch to a subsidiary requires a formal dissolution and reincorporation process; there is no administrative conversion pathway under current Brazilian law.

Sub-Types

Branch Office (Filial de Empresa Estrangeira)

Authorised via Presidential Decree, this structure allows full commercial activity but requires the foreign parent to formally allocate capital to Brazilian operations. The parent's unlimited exposure to Brazilian liabilities is the defining operational constraint.

Representative Office (Escritório de Representação)

Primarily used for liaison, procurement support, and market intelligence functions. Commercial activity — including signing contracts or invoicing clients — is not permitted, and any such activity risks reclassification by authorities as an unauthorised branch.

Foreign firms seeking full operational control with contained liability most commonly opt for a Ltda. subsidiary, while a branch suits those requiring a direct legal continuation of the parent entity for contractual or regulatory reasons. The principal drawback of both the branch and representative office is the parent's unrestricted exposure to Brazilian legal obligations.

Foreign businesses intending to trade, hire staff, or hold assets in Brazil are generally better served by incorporating a subsidiary (Ltda. or S.A.) rather than registering a branch, given the liability exposure and the administrative burden of Presidential Decree authorisation.

Partnership Structures in Brazil [Sociedade Simples, Sociedade em Nome Coletivo, Sociedade em Comandita Simples, Sociedade em Comandita por Ações]

Brazil's partnership structures in Brazil (Sociedade Simples) and related forms are governed by the Código Civil, Law No. 10.406/2002, which replaced the earlier Código Comercial for civil-purpose entities. These structures lack the commercial character of the Ltda. or S.A. and are typically reserved for professionals providing intellectual, scientific, literary, or artistic services.

Four distinct partnership forms exist under this framework. Each carries its own liability profile and membership rules, making the choice of form a substantive legal and financial decision rather than a formality.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Civil partnership (Sociedade Simples) or commercial partnership variants | Sociedade Simples has separate legal personality upon registration with JUCEB or Cartório |

| Members | Called "sócios" (partners); minimum 2, no statutory maximum | Sociedade em Comandita divides partners into general (comanditados) and limited (comanditários) |

| Local Presence | Registered address required; no mandatory local director in all forms | Sociedade em Comandita por Ações requires a board structure similar to an S.A. |

| Capital | No statutory minimum; denominated in BRL | Contributions may be in cash, assets, or services (services not permitted in Comandita por Ações) |

| Liability | Varies by type: unlimited for general partners, limited for silent/limited partners | Sociedade Simples partners may have unlimited personal liability unless the contract restricts it |

| Privacy | Partnership agreements (contrato social or estatuto) are publicly registered | No meaningful privacy — documents are accessible via the commercial or civil registry |

Focus Points

- Taxation: Sociedade Simples entities may qualify for Lucro Presumido or Simples Nacional regimes depending on revenue; subject to ISS on services, PIS/COFINS contributions, and standard IRPJ/CSLL corporate rates where applicable.

- Annual Compliance: Annual financial statements and maintenance of the partnership agreement at the registered address; changes to the contrato social require notarization and re-registration.

- Economic Substance: No formal economic substance legislation applies specifically to these entities, but professional partnerships must reflect genuine activity to retain their civil classification.

- Conversion: A Sociedade Simples may convert to a Ltda. or S.A. under the Código Civil without dissolution, subject to JUCEB or Cartório approval.

- Restrictions: Foreign nationals may participate as partners, but at least one administrator must hold a CPF (Brazilian tax identification number) and, if foreign-domiciled, a permanent visa or local representative under a public power of attorney.

Sub-Types

Sociedade Simples

The base form under Law No. 10.406/2002, intended for professionals such as lawyers, physicians, and engineers whose activity does not constitute a commercial enterprise. All partners bear joint and unlimited liability unless the contrato social expressly limits it.

Sociedade em Nome Coletivo

Sociedade em Nome Coletivo Brazil is restricted to individual persons (not legal entities) as partners, all of whom carry unlimited joint liability for the firm's obligations. It is rarely used in modern commercial practice but remains codified under Article 1.039 of the Código Civil.

Sociedade em Comandita Simples

This form separates partners into two classes: comanditados, who manage the business and hold unlimited liability, and comanditários, who contribute capital and are liable only up to their subscribed shares. The comanditários may not perform management acts without assuming unlimited liability.

Sociedade em Comandita por Ações

Sociedade em Comandita por Ações Brazil is governed by Law No. 6.404/1976 (the same statute as the S.A.) and issues share capital. Directors are personally and unlimitedly liable, while shareholders holding only shares bear limited liability. It is the most structurally complex of the four partnership forms.

When to Use Partnership Structures

These entities suit licensed professionals seeking a formal practice structure, or investors requiring tiered liability arrangements without the full governance burden of an S.A. The primary limitation across most forms is the exposure of at least one partner class to unlimited personal liability.

Partnership structures in Brazil are best suited for regulated professionals — such as law firms, medical practices, or architectural studios — operating under a civil-purpose mandate rather than a commercial one.

How to Choose the Right Entity Type in Brazil

Selecting the correct legal structure from the outset determines your tax position, liability exposure, and operational capacity — getting it wrong creates compliance burdens that can be costly to unwind.

Why Your Entity Choice Matters

- Registering a foreign branch while conducting regular commercial activity without proper authorization from the Junta Comercial exposes the business to sanctions under Law No. 6.404/1976 and the Civil Code, including potential deregistration.

- Choosing a structure ineligible for Simples Nacional when your revenue and activity qualify means paying higher taxes under Lucro Presumido or Lucro Real unnecessarily.

- Operating as a Microempreendedor Individual (MEI) beyond the annual revenue ceiling of R$81,000 without migrating to an Ltda. or EI triggers loss of the simplified tax regime and retroactive recalculation obligations.

- Forming an Ltda. when a single-shareholder structure would serve the business locks you into multi-party governance requirements that add unnecessary administrative overhead.

Key Factors to Consider

- Business Activity: Active trading, asset holding, and regulated sectors such as financial services each require distinct structures under Brazilian law.

- Ownership Structure: Single-person operations may qualify for MEI, EI, or EIRELI treatment, while multi-party ventures require an Ltda. or S.A.

- Tax Regime Eligibility: Your projected annual revenue and activity type determine whether the business qualifies for Simples Nacional, Lucro Presumido, or Lucro Real.

- Capital and Liability: The level of personal liability you can accept and the minimum capital you can commit narrow the available options.

- Scalability and Exit: If you anticipate equity investment or eventual restructuring, an S.A. allows share transfers and shareholder admission more readily than an Ltda.

- Foreign Ownership: Non-resident shareholders trigger specific registration obligations with the Banco Central do Brasil under the RDE-IED system, which affects entity selection.

The full text of the Lei das Sociedades Anônimas (Law No. 6.404/1976) and the Brazilian Civil Code (Law No. 10.406/2002) govern the formation and operation of most business structures and should be consulted directly when evaluating your options.

Compliance Services for Companies in Brazil

Maintain good standing with Brazilian regulatory bodies, including the Junta Comercial, Receita Federal, and Banco Central do Brasil.

Conclusion

Brazil's corporate framework offers several distinct paths depending on the scale, ownership structure, and liability requirements of your business. This incorporating a business in Brazil guide has covered each entity type governed by the Código Civil (Law No. 10,406/2002) and the Lei das Sociedades Anônimas (Law No. 6,404/1976). The Ltda. remains the most registered entity in the country, favored for its structural flexibility and proportionally lower compliance burden. The S.A. suits capital-intensive ventures requiring equity investment or public listings. The MEI serves micro-level self-employment, while the EI carries unlimited personal liability. EIRELI, though no longer available for new registrations since 2021, still exists for previously formed entities.

Regulatorily, Brazil continues to expand its tax treaty network and has undertaken ongoing reforms to simplify registration through the Redesim system. These changes affect how foreign capital enters and how corporate structures are maintained over time. Expanship's team works directly within this framework to support your registration and ongoing compliance requirements.

How Expanship Can Assist You

Expanship's Brazil company incorporation services cover the full registration process, from selecting the right entity type to finalising your records with the Junta Comercial (Board of Trade) or the relevant cartório for civil entities. Whether you are forming a Sociedade Limitada, a Sociedade Anônima, or registering as a foreign branch through the DREI, our team works within Brazil's specific regulatory requirements so nothing is missed.

From document preparation to ongoing compliance, our corporate services in Brazil include:

- Document preparation, notarisation, and consular legalization

- Registered agent and registered address provision

- Filing with the Junta Comercial, Receita Federal, and municipal authorities

- CNPJ registration and Inscrição Estadual/Municipal processing

- Post-incorporation compliance management, including annual obligations

- Banking introduction assistance for corporate account opening

Reach out to our team directly through Expanship Brazil to discuss your entity formation requirements.

Frequently Asked Questions (FAQ)

The Sociedade Limitada (Ltda.) is the most frequently registered entity, largely because it combines limited liability with a relatively straightforward governance structure under the Civil Code (Law No. 10.406/2002). Minimum capital requirements are flexible, and the administrative framework suits a wide range of commercial activities without the disclosure burdens of a Sociedade Anônima.

Both structures offer limited liability, but the S.A. is subject to Law No. 6.404/1976 and carries more extensive disclosure and board governance requirements, whereas an Ltda. operates under the Civil Code with fewer mandatory corporate formalities. Publicly held S.A.s fall under CVM oversight and must publish audited financial statements; Ltdas. generally do not. For tax purposes, both can elect Lucro Real or Lucro Presumido regimes, so the distinction lies in governance rather than tax access.

Among registered structures, the Sociedade Limitada held by a holding company offers the most relative privacy, as beneficial ownership disclosure requirements apply at the Receita Federal level rather than through public filings. Nominee arrangements, while not prohibited outright, face scrutiny under anti-money laundering regulations governed by COAF (Conselho de Controle de Atividades Financeiras). The EIRELI and MEI, by contrast, directly link the individual's CPF or CNPJ to public records.

Not all structures permit single-person formation. The EIRELI was specifically designed for sole individuals, and the MEI serves individual microentrepreneurs, while both the Sociedade Limitada and Sociedade Anônima traditionally required at least two members, though a 2021 amendment to the Civil Code now permits single-member Ltdas. Sociedade em Nome Coletivo and Sociedade em Comandita Simples require a minimum of two partners by definition.

Foreigners may form or invest in an Ltda., S.A., or establish a branch, provided they obtain a CPF (individual taxpayer registration) or CNPJ and meet residency or legal representative requirements under DREI (Departamento Nacional de Registro Empresarial e Integração) regulations. A non-resident investor must appoint a locally resident attorney-in-fact with powers to receive legal service. The MEI is restricted to Brazilian residents with CPF.

Conversion between entity types is permitted under the Civil Code and does not require dissolving the original entity. An Ltda. can be converted into an S.A., or a Sociedade Simples can be transformed into an Ltda., through an amendment registered with the Junta Comercial in the relevant state. The process involves updating the articles of organization and re-registration under the new structural framework.

Not uniformly. The Empresário Individual (EI) does not create a legal entity separate from the individual, meaning personal assets remain exposed to business liabilities. The EIRELI, Ltda., S.A., and Sociedade Simples all hold separate legal personality under Article 44 of the Civil Code. This distinction is material when assessing liability exposure and contracting capacity.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.