Key Takeaways

- All business entities in Bonaire, Sint Eustatius, and Saba are registered with the Kamer van Koophandel under the Wetboek van Koophandel BES and related civil codes adapted from Dutch legislation.

- The Besloten Vennootschap (BV) is the most widely registered entity type across the BES islands, making it the default structure for private investors and holding companies.

- Partners in a Vennootschap Onder Firma (VOF) or Commanditaire Vennootschap (CV) carry personal liability exposure, which limits their suitability for asset-holding purposes.

- The BES islands' status as special municipalities of the Netherlands — rather than autonomous offshore territories — provides institutional credibility that distinguishes them from conventional offshore jurisdictions.

Introduction to Entity Types in Bonaire Sint Eustatius and Saba

Bonaire, Sint Eustatius, and Saba are three islands located in the Caribbean Sea, situated northeast of Venezuela and forming part of the Lesser Antilles. Since 2010, these islands have held the status of special municipalities of the Netherlands, making them constituent parts of the Kingdom of the Netherlands rather than autonomous territories.

Company registration in the BES islands falls under the jurisdiction of the Kamer van Koophandel (Chamber of Commerce), which maintains the commercial register for all business entities operating across the three islands. The applicable civil and corporate law derives from Dutch legislation adapted for the Caribbean Netherlands context, specifically through the Wetboek van Koophandel BES and related civil codes.

The tax regime is generally considered low-tax relative to continental Europe, with distinct rules governing resident and non-resident entities — though specific rates vary by entity type and activity.

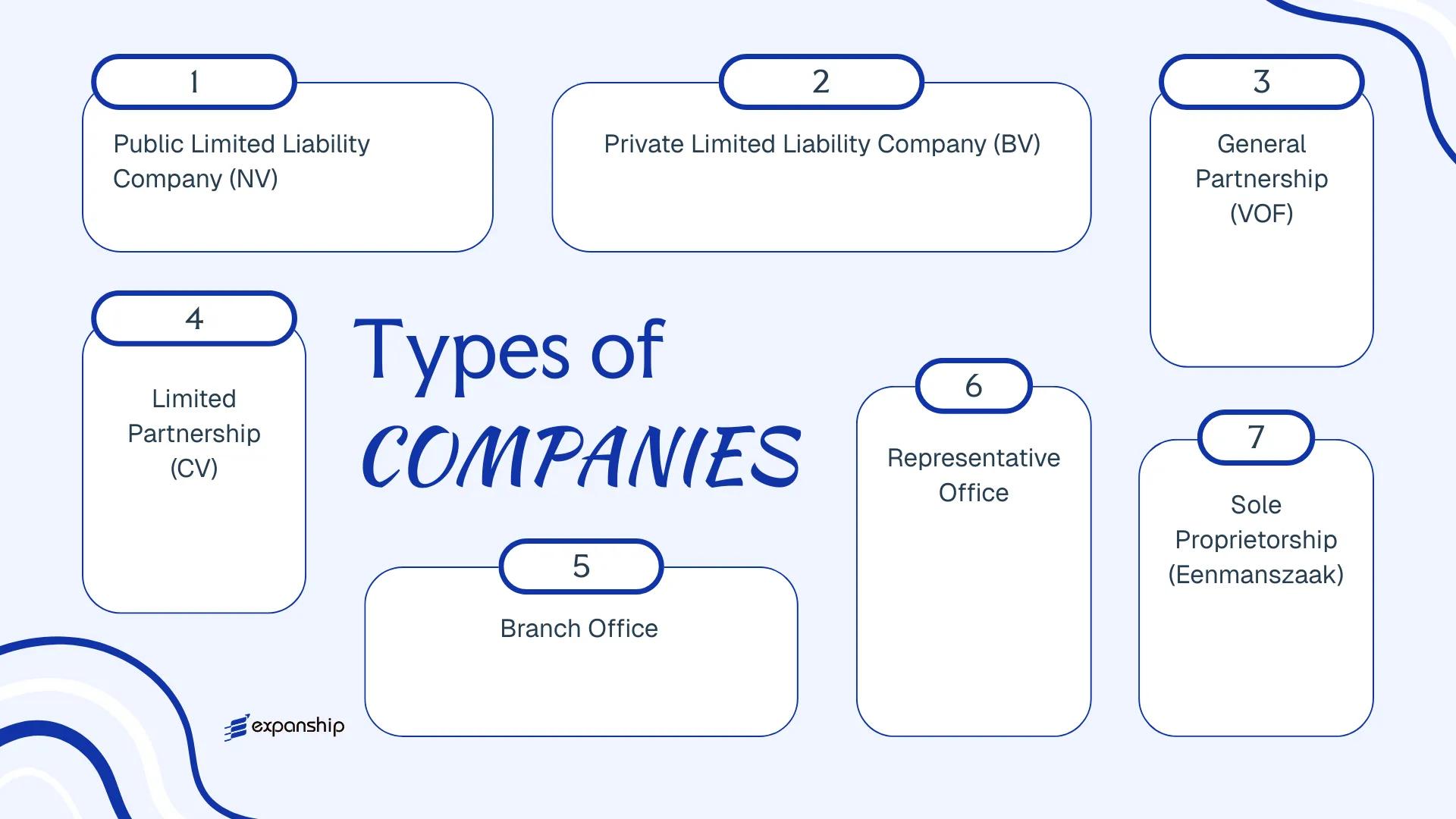

The business entity types in Bonaire Sint Eustatius Saba available under this framework include:

- Naamloze Vennootschap (NV)

- Besloten Vennootschap (BV)

- Vennootschap Onder Firma (VOF)

- Commanditaire Vennootschap (CV)

- Eenmanszaak

- Branch Office

- Representative Office

Each structure carries distinct requirements around liability, governance, and registration. This article examines each one in detail.

An Overview of Business Structures in Bonaire Sint Eustatius and Saba

Bonaire, Sint Eustatius, and Saba — collectively the BES islands — operate under a corporate legal framework that recognises several distinct entity types, each governed primarily by the Civil Code of the Caribbean Netherlands (Burgerlijk Wetboek BES) and related commercial legislation. The business structures overview for Bonaire Sint Eustatius Saba spans capital-based companies, partnerships, sole proprietorships, and foreign entity registrations. Each form carries different rules on liability, governance, and taxation, and the sections that follow address every structure individually.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Naamloze Vennootschap (NV) | Public Limited Company | Limited to share capital | Taxable | Permitted | 1 shareholder | Chamber of Commerce BES | BW BES |

| Besloten Vennootschap (BV) | Private Limited Company | Limited to share capital | Taxable | Permitted | 1 shareholder | Chamber of Commerce BES | BW BES |

| Vennootschap Onder Firma (VOF) | General Partnership | Unlimited, joint | Taxable | Permitted | 2 partners | Chamber of Commerce BES | BW BES |

| Commanditaire Vennootschap (CV) | Limited Partnership | Mixed | Taxable / Exempt | Permitted | 2 partners | Chamber of Commerce BES | BW BES |

| Eenmanszaak | Sole Proprietorship | Unlimited, personal | Taxable | Permitted | 1 owner | Chamber of Commerce BES | BW BES |

| Branch Office | Foreign Entity Extension | Parent liable | Taxable | Permitted | N/A | Chamber of Commerce BES | BW BES |

| Representative Office | Non-trading presence | Parent liable | Generally exempt | Not permitted | N/A | Chamber of Commerce BES | BW BES |

Each of these structures is examined in full in the sections below.

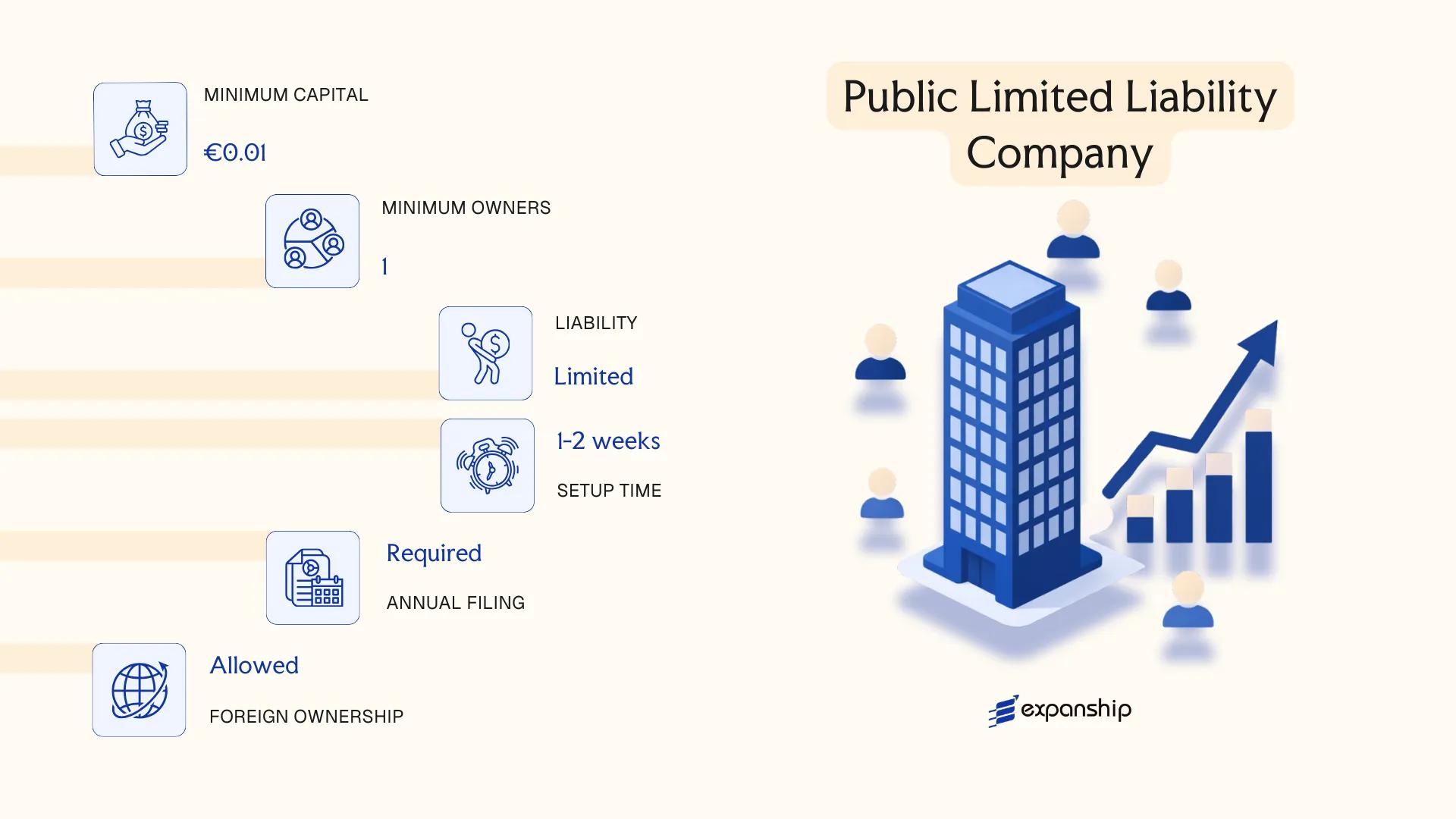

Naamloze Vennootschap (NV) — Public Limited Liability Company

Governed by the Civil Code of Bonaire, Sint Eustatius and Saba (Burgerlijk Wetboek BES), the Naamloze Vennootschap is a capital-based entity with full legal personality, meaning it exists independently of its shareholders and can hold assets, enter contracts, and incur liabilities in its own name. A Naamloze Vennootschap NV Bonaire registration is particularly suited to structures where shares may need to be freely transferable or publicly offered.

Liability is limited to each shareholder's capital contribution. Unlike a BV, shares in an NV are not subject to statutory transfer restrictions by default, giving the structure flexibility for larger investor groups or future capital market activity.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Limited Liability Company (NV) | Governed by Burgerlijk Wetboek BES |

| Members | Shareholders (min. 1); no maximum | Directors: min. 1; supervisory board optional |

| Local Presence | Registered office in BES required | Registered agent not statutorily mandated but common in practice |

| Share Capital | Minimum USD 1 (no prescribed minimum under BES law) | Shares may be issued in any currency; bearer shares are no longer permitted |

| Privacy | Shareholder names filed with the Chamber of Commerce | UBO registration required under local AML regulations |

Focus Points

- Taxation: Subject to profit tax (winstbelasting) under the BES fiscal regime; standard rate is 0% on most passive income for non-resident structures, though local trading income is taxed; no VAT applies — a turnover tax (OB) applies instead; dividend withholding tax may apply depending on shareholder residency.

- Economic Substance: Entities conducting relevant activities must satisfy substance requirements under BES economic substance legislation, including local management and board meetings.

- Annual Compliance: Annual financial statements must be prepared; filing obligations with the Chamber of Commerce of Bonaire (KvK) apply; audit requirements depend on company size.

- Treaty Access: The BES islands are not independent treaty jurisdictions; the Netherlands' tax treaty network does not automatically extend to BES entities.

- Conversion: An NV may be converted to a BV under BES civil law, subject to notarial deed and registration requirements.

Closing

The NV is used primarily for holding structures, joint ventures with multiple investors, and entities anticipating future share issuances to third parties. Its unrestricted share transferability is a structural advantage, though the public filing of shareholder information reduces confidentiality relative to some other offshore forms.

The NV is best suited for multi-investor holding companies, international joint ventures, and structures where share transferability without prior approval is operationally necessary.

Company Incorporation in Bonaire, Sint Eustatius and Saba

Incorporate an NV or other entity type in the BES islands with end-to-end support from Expanship.

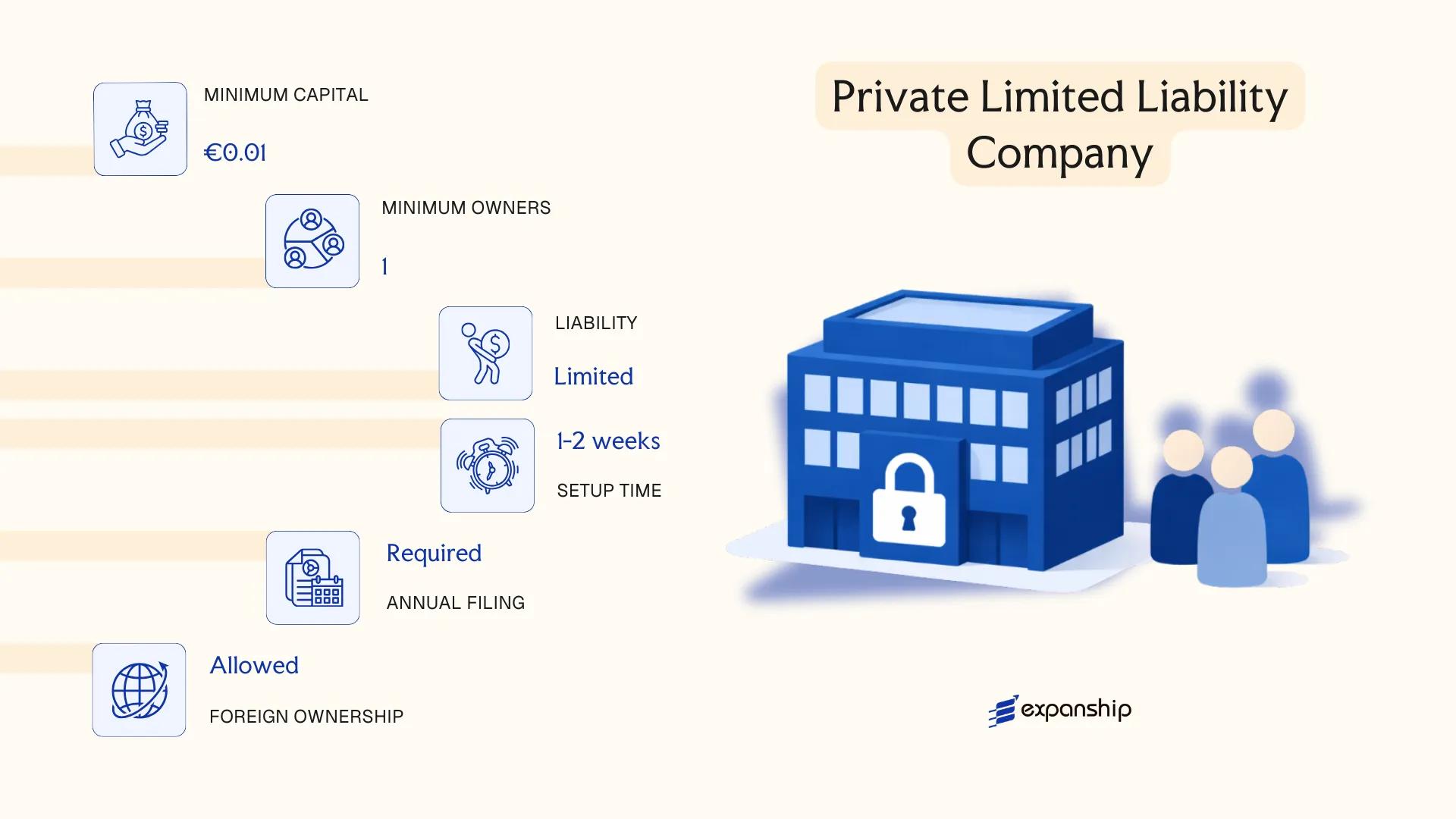

Besloten Vennootschap (BV) — Private Limited Liability Company

The Besloten Vennootschap BV Sint Eustatius Saba framework is governed by the Civil Code of the Caribbean Netherlands (Burgerlijk Wetboek BES), which came into effect on 1 January 2011 following the dissolution of the Netherlands Antilles. A BV holds a separate legal personality, meaning the entity bears its own rights and obligations independently of its shareholders.

Liability is limited to the capital contributed. This structure positions the BV as the standard closed private company form across the BES islands, suited to closely held ownership arrangements where shares are not publicly traded or freely transferable without restriction.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private limited liability company (BV) | Incorporated under Burgerlijk Wetboek BES |

| Members | Shareholders (min. 1, no maximum); Directors (min. 1) | Both shareholders and directors may be natural persons or legal entities |

| Local Presence | Registered office address required in BES | Registered agent not statutorily mandatory but standard practice |

| Share Capital | No statutory minimum capital requirement | Shares denominated in any currency; capital must be defined in articles |

| Share Transferability | Restricted; subject to approval or right of first refusal clauses | Transfer restrictions must be set out in the articles of association |

| Privacy | Shareholder register maintained internally; not fully public | UBO registration obligations apply under AML regulations |

Focus Points

- Taxation: Corporate profit tax applies at rates set under the BES fiscal regime; no VAT applies in BES, though a turnover tax (OB) may apply; dividend withholding tax and payroll taxes are relevant where distributions or staff are involved.

- Economic Substance: BES entities conducting relevant activities may be subject to economic substance requirements aligned with Dutch and international standards.

- Annual Compliance: Annual financial statements are required; filing obligations depend on entity size and activity classification under BES civil law.

- Conversion: A BV may be converted into an NV subject to meeting the applicable procedural requirements under the Burgerlijk Wetboek BES.

- Restrictions: Shares in a BV cannot be offered to the public; any public capital-raising activity requires conversion to an NV.

Closing

The BV is commonly used for trading operations, holding structures, and IP ownership by closely held groups seeking limited liability without public disclosure of share transfers. Its primary structural advantage is the ability to restrict share transferability through the articles, preserving ownership control. The main limitation is the prohibition on public share issuance, which constrains capital-raising options.

The BV is best suited for small to medium-sized privately held businesses, family-owned enterprises, and foreign investors establishing a controlled subsidiary in the Caribbean Netherlands.

Partnerships in Bonaire Sint Eustatius and Saba [Vennootschap Onder Firma (VOF), Commanditaire Vennootschap (CV)]

Two partnership forms operate within the BES islands under the civil and commercial law framework inherited from the Netherlands Antilles and subsequently aligned with Dutch statutory principles applicable to the Caribbean Netherlands. Neither the Vennootschap Onder Firma (VOF) nor the Commanditaire Vennootschap (CV) possesses separate legal personality, meaning all contractual obligations bind the partners directly rather than a distinct legal entity.

Registration of both forms is handled through the Kamer van Koophandel (Chamber of Commerce) of Bonaire. The VOF CV partnership Bonaire Sint Eustatius Saba structure suits smaller commercial operations and certain investment arrangements where pass-through taxation is preferred over corporate-level liability.

Key Characteristics

| Requirement | VOF Detail | CV Detail |

|---|---|---|

| Legal Form | General partnership; no separate legal personality | Limited partnership; no separate legal personality |

| Partners | General partners (vennoten); minimum 2, no maximum | At least 1 general partner (beherende vennoot) and 1 limited partner (commanditaire vennoot) |

| Liability | All partners bear unlimited joint and several liability | General partner: unlimited liability; limited partner: liability capped at capital contribution |

| Local Presence | Registered address in BES required; no mandatory local agent | Registered address in BES required |

| Capital | No statutory minimum; contributions defined by partnership agreement | No statutory minimum; limited partner's contribution documented in agreement |

| Privacy | Partnership deed registered; partner details held on public commercial register | Same as VOF; limited partner identity disclosed on registration |

Focus Points

- Taxation: Partnerships are fiscally transparent under BES tax rules; profits are attributed to and taxed at the partner level rather than the entity level, with no separate corporate income tax applied to the partnership itself; local income tax rates apply to resident partners, while non-resident partners are subject to withholding provisions on BES-sourced income.

- Economic Substance: Standard economic substance obligations under BES legislation apply only to specific relevant activities; pure holding or trading partnerships should verify whether their activities trigger substance requirements.

- Annual Compliance: Both forms must maintain accurate accounts and update the Chamber of Commerce register upon any change in partners or partnership terms.

- Treaty Access: BES entities generally fall outside the Netherlands tax treaty network, limiting access to reduced withholding tax rates on cross-border income flows.

Sub-Types

Vennootschap Onder Firma (VOF)

The VOF is a general partnership in which all partners actively participate in the business and carry unlimited liability for its obligations. It is typically used for small trading firms or professional practices where partners operate collectively.

Commanditaire Vennootschap (CV)

The CV introduces a two-tier partner structure: the general partner manages operations and bears unlimited liability, while the limited partner contributes capital without participating in management, preserving liability protection up to the amount contributed. This structure is commonly used for investment vehicles and family asset arrangements in the Vennootschap Onder Firma BES islands context.

When a Partnership May Apply

Partnerships in the Caribbean Netherlands suit operators who require structural simplicity and fiscal transparency, though the absence of limited liability for general partners remains a material constraint for higher-risk commercial activities.

VOF and CV structures work best for small commercial operations, professional collaborations, or capital-pooling arrangements where partners accept direct tax attribution and, in the CV's case, one party seeks passive investment exposure with capped liability.

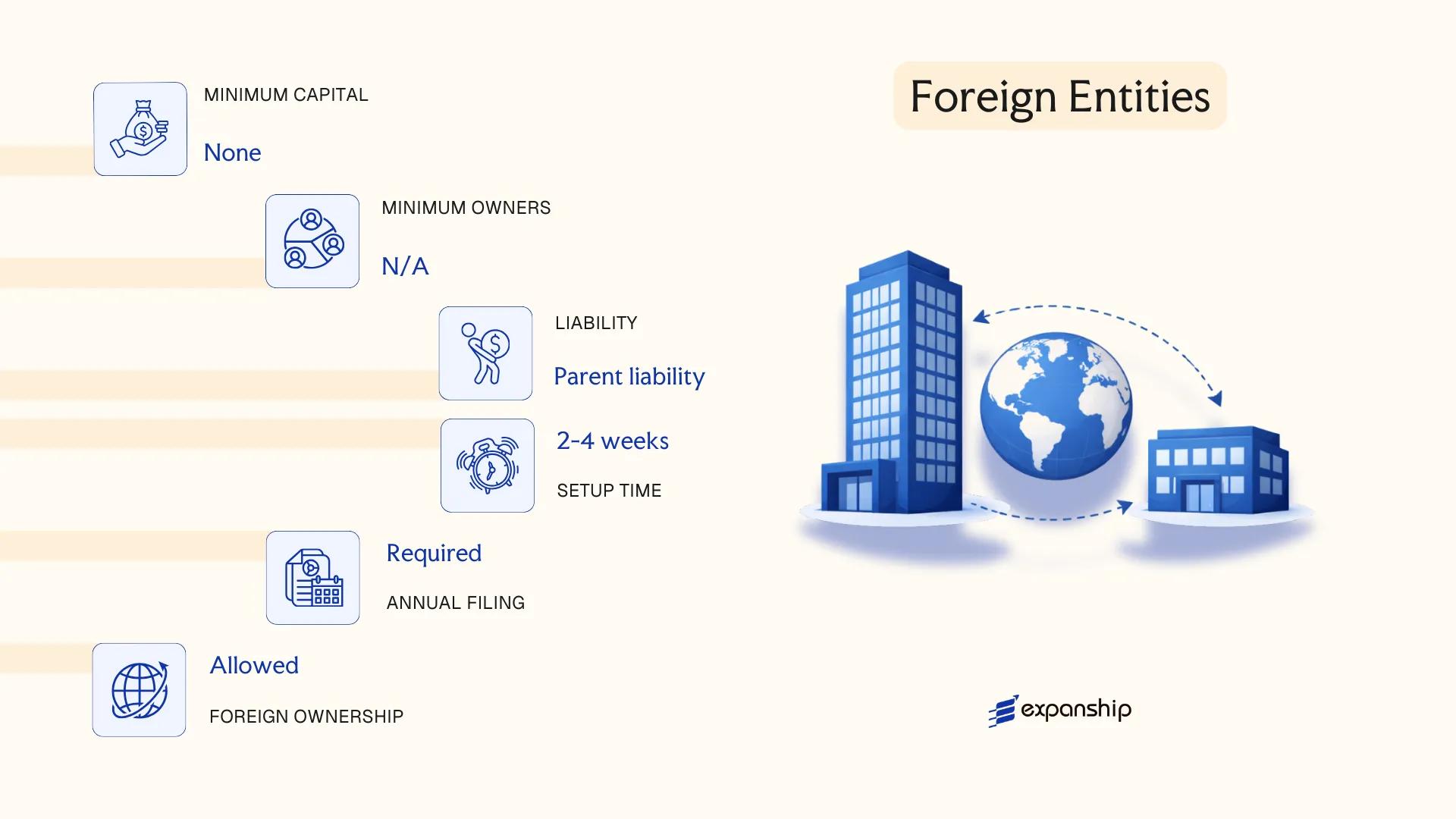

Foreign Entities in Bonaire Sint Eustatius and Saba [Branch Office, Representative Office]

Establishing a foreign branch office Bonaire Sint Eustatius Saba requires registration under the Civil Code of Bonaire, Sint Eustatius and Saba (BES Civil Code), which governs foreign entity operations across the three special municipalities. A branch office does not constitute a separate legal entity — it remains an extension of the parent company, which retains full liability for the branch's obligations.

Registration is handled through the Chamber of Commerce of Bonaire (Kamer van Koophandel), where the foreign firm must submit incorporation documents from its home jurisdiction, along with a local address. A representative office, by contrast, operates in a more limited capacity, restricted to promotional or liaison activities and excluded from generating direct revenue in the BES islands.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Branch or Representative Office | Neither constitutes a separate legal person; liability remains with the parent |

| Local Contact | Registered address in BES | A local representative or agent is required for correspondence |

| Capital | No minimum | Parent company capital applies |

| Registration Body | Chamber of Commerce, Bonaire | Home-country documents must be apostilled or notarised |

| Privacy | Parent entity details publicly filed | Beneficial ownership disclosure applies under BES AML regulations |

Focus Points

- Taxation: Branch profits are subject to the BES profit tax regime; no separate VAT system applies, but a turnover tax (ABB) may be applicable depending on activities.

- Economic Substance: Substance requirements under BES legislation may apply if the branch conducts relevant activities as defined by local economic substance rules.

- Annual Compliance: Annual financial reporting and Chamber of Commerce renewal obligations apply to registered branches.

- Treaty Access: Access to tax treaties depends on the parent company's jurisdiction; the BES islands have limited treaty coverage.

- Revenue Restrictions: Representative offices cannot invoice clients or conduct direct commercial transactions.

Sub-Types

Branch Office

A branch office can conduct full commercial operations in the BES islands on behalf of the parent company. It is used by foreign firms seeking an operational presence without incorporating a separate local entity.

Representative Office

A representative office is restricted to non-revenue-generating activities such as market research, liaison, or promotional work. It carries lower compliance obligations but cannot enter into commercial contracts independently.

Closing

Foreign companies use branch structures primarily for operational expansion into the Caribbean Netherlands market, with the key advantage being the absence of a separate incorporation process. The primary limitation is unrestricted parent liability for all branch obligations.

A branch office suits established foreign companies seeking direct market presence in the BES islands without creating a standalone local entity; a representative office fits firms conducting preliminary market activity only.

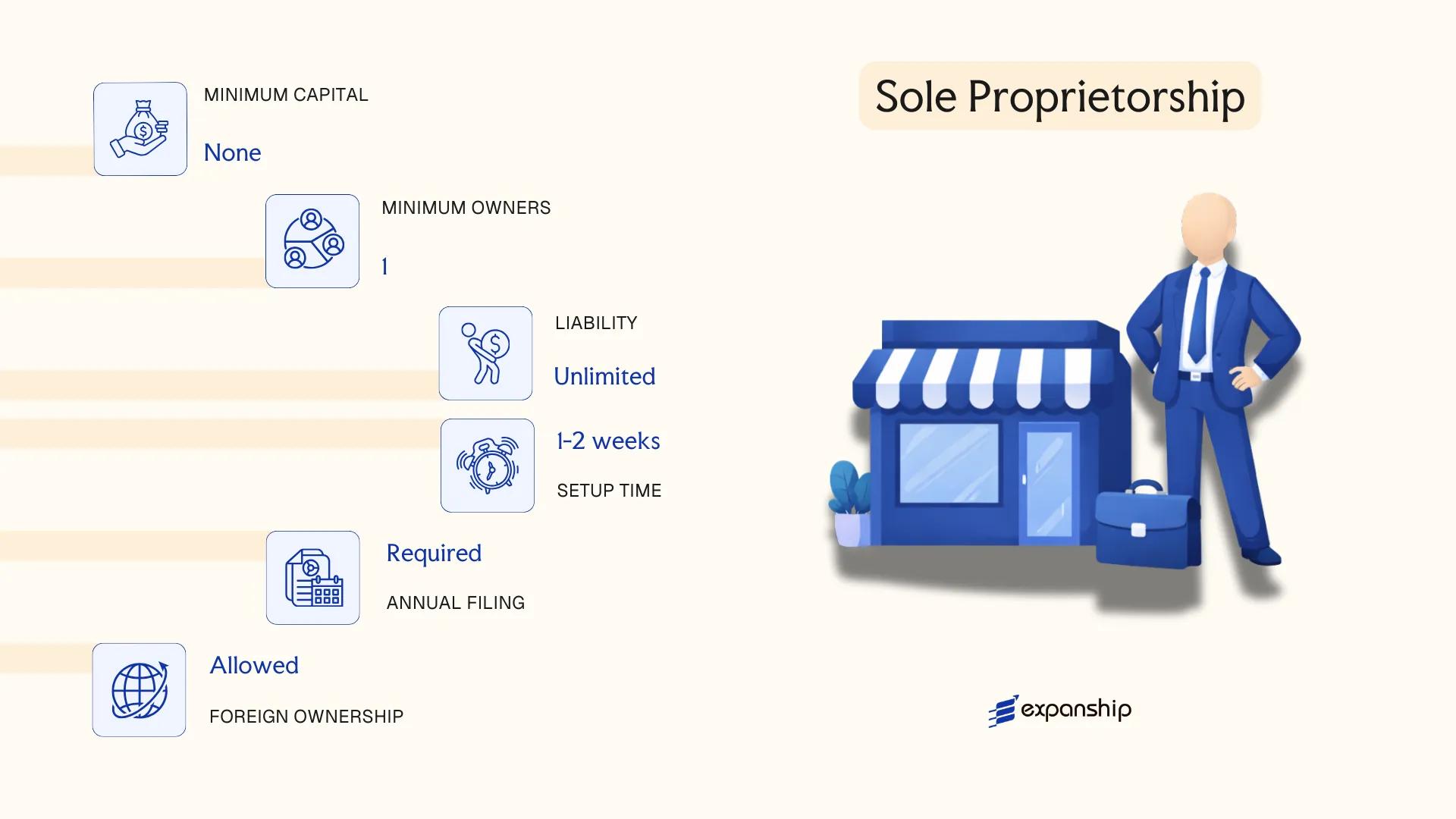

Sole Proprietorship (Eenmanszaak)

The Eenmanszaak sole proprietorship Bonaire registration process falls under the general commercial registration framework administered by the Chamber of Commerce of the Caribbean Netherlands (Kamer van Koophandel van Caribisch Nederland). This structure carries no separate legal personality, meaning the owner and the business are treated as a single entity under law. All assets and liabilities rest directly with the proprietor, without any liability shield.

Registration is straightforward by design. Self-employed individuals operating in the Caribbean Netherlands must register their sole proprietorship with the local Chamber of Commerce before commencing commercial activity. There is no minimum capital requirement, and the business income is taxed at the individual level rather than at an entity level.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole Proprietorship (Eenmanszaak) | No separate legal personality |

| Member Reference | Proprietor | Single natural person only |

| Ownership | 1 proprietor (maximum 1) | Legal entities cannot hold this form |

| Local Presence | Registered business address in BES islands | Chamber of Commerce registration required |

| Capital | No minimum; no prescribed currency | Fully at proprietor's discretion |

| Liability | Unlimited personal liability | Personal assets exposed to business creditors |

| Privacy | Owner name appears on public register | No shareholder register or confidentiality provisions |

Focus Points

- Taxation: Business profits are subject to income tax (inkomstenbelasting) at the proprietor level; there is no separate corporate tax, but turnover thresholds may trigger OB (Omzetbelasting, the BES islands' sales tax equivalent) obligations.

- Annual Compliance: Annual financial reporting requirements are minimal compared to corporate forms; however, tax filings with the Belastingdienst Caribisch Nederland (BCN) remain mandatory.

- Economic Substance: No economic substance obligations apply to this structure under the BES islands' substance rules, which target corporate entities.

- Conversion: Conversion to a BV or NV is possible but requires a new incorporation process rather than a statutory conversion procedure.

- Treaty Access: As a pass-through structure, the entity itself has no access to double tax treaties; any treaty benefits depend on the proprietor's personal tax residency.

Closing

A single-owner business Bonaire Sint Eustatius Saba operators frequently use the Eenmanszaak for local service provision, freelance activity, and small-scale trade where administrative simplicity outweighs the need for liability protection. The absence of a capital requirement and low setup costs make entry accessible, though unlimited personal liability remains a significant structural exposure for businesses with material financial risk.

This structure suits individual entrepreneurs and self-employed professionals conducting low-risk, locally focused activities with limited third-party liability exposure.

How to Choose the Right Entity Type in Bonaire Sint Eustatius and Saba

Choosing the right company type in Bonaire Sint Eustatius Saba determines not just how your business operates, but what obligations, costs, and risks attach to it from the moment of registration.

Why Your Entity Choice Matters

The structure you register under the Book 2 of the Civil Code BES has binding consequences.

- Registering as a branch of a foreign entity when you conduct substantive local trade may place you in breach of registration requirements, exposing the business to deregistration or administrative penalties.

- Selecting a tax-exempt structure when your counterparties require treaty-based withholding tax reductions means those reductions will be unavailable, since exempt entities fall outside the treaty network.

- Choosing a corporate structure when a foundation would serve asset protection or succession planning objectives binds you to annual shareholder obligations that foundations do not carry.

- Opting for an entity subject to mandatory audited financial statements when your firm is a single-person consultancy generates recurring professional costs that a simpler structure would avoid.

Key Factors to Consider

- Business Activity: Active trading, passive asset-holding, and regulated sectors such as banking or insurance each point toward a distinct legal structure under BES rules.

- Local vs. External Operations: Whether your firm transacts with BES residents or operates exclusively outside the islands affects which entity types are permissible and appropriate.

- Ownership and Management: A single-owner operation has different governance requirements than a multi-shareholder firm that needs a formal supervisory board.

- Tax Objectives: Your position on tax exemption, profit tax eligibility, or access to the Dutch tax treaty network should directly inform your NV vs BV Bonaire comparison.

- Substance Capacity: If you cannot maintain staff, office space, or local decision-making, you need a structure with lower or no substance thresholds to avoid reporting failures.

- Exit Strategy: Not all entity types permit redomiciliation or conversion; confirm at the outset which structures allow winding up or transformation without dissolving entirely.

Compliance Services for Companies in the Caribbean Netherlands

Maintain good standing across reporting, substance, and regulatory obligations in Bonaire, Sint Eustatius, and Saba.

Conclusion

Each entity structure available under the BES islands framework serves a distinct purpose. The NV suits firms seeking access to capital markets or broad shareholding arrangements, while the BV remains the most widely registered structure for private ventures due to its flexible governance and limited liability. Partnerships under the VOF and CV frameworks carry personal liability exposure that makes them less attractive for asset-holding purposes. Branch offices allow foreign companies to operate directly without creating a separate legal entity, and the Eenmanszaak fits individual operators running low-risk activities.

Registered in the highest numbers, the BV is the default choice for most private investors and holding structures across Bonaire Sint Eustatius and Saba. The jurisdiction continues to align with Dutch regulatory standards, and its standing within the Kingdom of the Netherlands provides a degree of institutional credibility that offshore alternatives often cannot match. Firms planning a company incorporation in Bonaire Sint Eustatius and Saba will find that entity selection directly determines compliance obligations, liability exposure, and tax treatment under applicable BES legislation.

How Expanship Can Assist You

Expanship company formation BES islands services are built around the specific legal and administrative realities of Bonaire, Sint Eustatius, and Saba as public bodies under Dutch law. From registering a Besloten Vennootschap to filing a branch office with the Kamer van Koophandel (Chamber of Commerce) for the Caribbean Netherlands, every step requires precise documentation and familiarity with local procedures.

Expanship handles the full scope of corporate services in Bonaire, Sint Eustatius, and Saba:

- Entity formation documents and notarial deed preparation

- Registered agent and local office address provision

- Filing and liaison with the Caribbean Netherlands Chamber of Commerce

- Post-incorporation compliance and annual reporting support

- Corporate document legalization and apostille coordination

- Banking introduction assistance for newly formed entities

Ready to set up your business in the BES islands? Reach out to Expanship BQ to discuss your requirements.

Frequently Asked Questions (FAQ)

The Besloten Vennootschap (BV) is the most frequently incorporated entity across the BES islands. Its combination of limited liability, flexible share transfer restrictions, and suitability for both small and medium-scale operations makes it the default choice for resident and non-resident entrepreneurs alike.

Both structures offer limited liability, but the NV permits public share issuance while the BV restricts share transferability by default. For tax purposes under the BES fiscal regime, treatment depends on the entity's activities and residency status rather than the legal form alone. The NV carries heavier disclosure and governance obligations, making the BV the more practical structure for private commercial operations.

The BV generally provides the greatest degree of confidentiality among standard BES entity types, as shareholder registers are not publicly accessible. Nominee arrangements are permissible under local practice, though ultimate beneficial ownership must be disclosed to the relevant authorities under applicable AML regulations. Directors are registered with the Kamer van Koophandel (Chamber of Commerce), so full anonymity at the directorship level is not available.

A sole proprietorship (Eenmanszaak) and a BV can each be established by one person. The NV formally requires at least one shareholder but is structurally designed for multiple investors. Partnerships, including the Vennootschap Onder Firma (VOF) and Commanditaire Vennootschap (CV), require a minimum of two partners by definition, so a single individual cannot form these alone.

Foreign nationals may incorporate a BV, NV, or register a branch of a foreign entity without a local residency requirement. Restrictions apply primarily to certain licensed activities, where local regulatory approvals may be required regardless of nationality. A branch office can be a practical entry point for foreign firms testing the market before committing to a fully incorporated subsidiary.

Conversion from a BV to an NV, or between other corporate forms, is possible under BES civil law through a formal legal continuation procedure. The process requires a notarial deed and updated registration with the Kamer van Koophandel. Conversion from a partnership to a corporate entity is also achievable, though it involves additional steps to transfer assets and liabilities.

The BV and NV both hold separate legal personality, meaning the entity itself bears rights and obligations distinct from its shareholders. A branch office does not constitute an independent legal entity; it remains an extension of its parent company. The VOF and sole proprietorship lack separate legal personality entirely, which is why partners and sole traders bear personal liability for business debts.

The sole proprietorship carries the lightest compliance burden, with no mandatory audit requirements or annual financial filings beyond standard tax reporting. By contrast, the NV is subject to the most extensive requirements, including formal board governance, financial reporting obligations, and in certain cases, statutory audit requirements. The BV sits between these two, with moderate obligations that scale with the size and nature of the business.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.