Key Takeaways

- Brunei's most commonly registered business structure is the Private Company Limited by Shares (Sendirian Berhad), governed by the Companies Act, Cap. 39 and administered by the Registry of Companies and Business Names (ROCBN).

- Foreign corporations seeking operational presence in Brunei without establishing a separate legal entity may do so through a branch office, which remains an extension of the parent company.

- Brunei's tax environment is characterized by a flat corporate income tax rate with no personal income tax and no capital gains tax, making entity selection consequential primarily for liability and compliance purposes rather than personal tax exposure.

- Partnership structures in Brunei are divided between general partnerships, which suit small collaborative ventures, and limited partnerships governed by the Limited Partnerships Order, which allow passive investors to participate without taking on management responsibilities.

Introduction to Entity Types in Brunei

Brunei Darussalam is a sovereign nation on the northern coast of Borneo in Southeast Asia, sharing the island with Malaysia and Indonesia. Its legal and corporate framework draws heavily from English common law, and company registration falls under the jurisdiction of the Registry of Companies and Business Names (ROCBN), operating under the Ministry of Finance and Economy.

Corporate income tax is levied at a flat rate, though the overall tax posture is relatively low by regional standards, with no personal income tax and no capital gains tax.

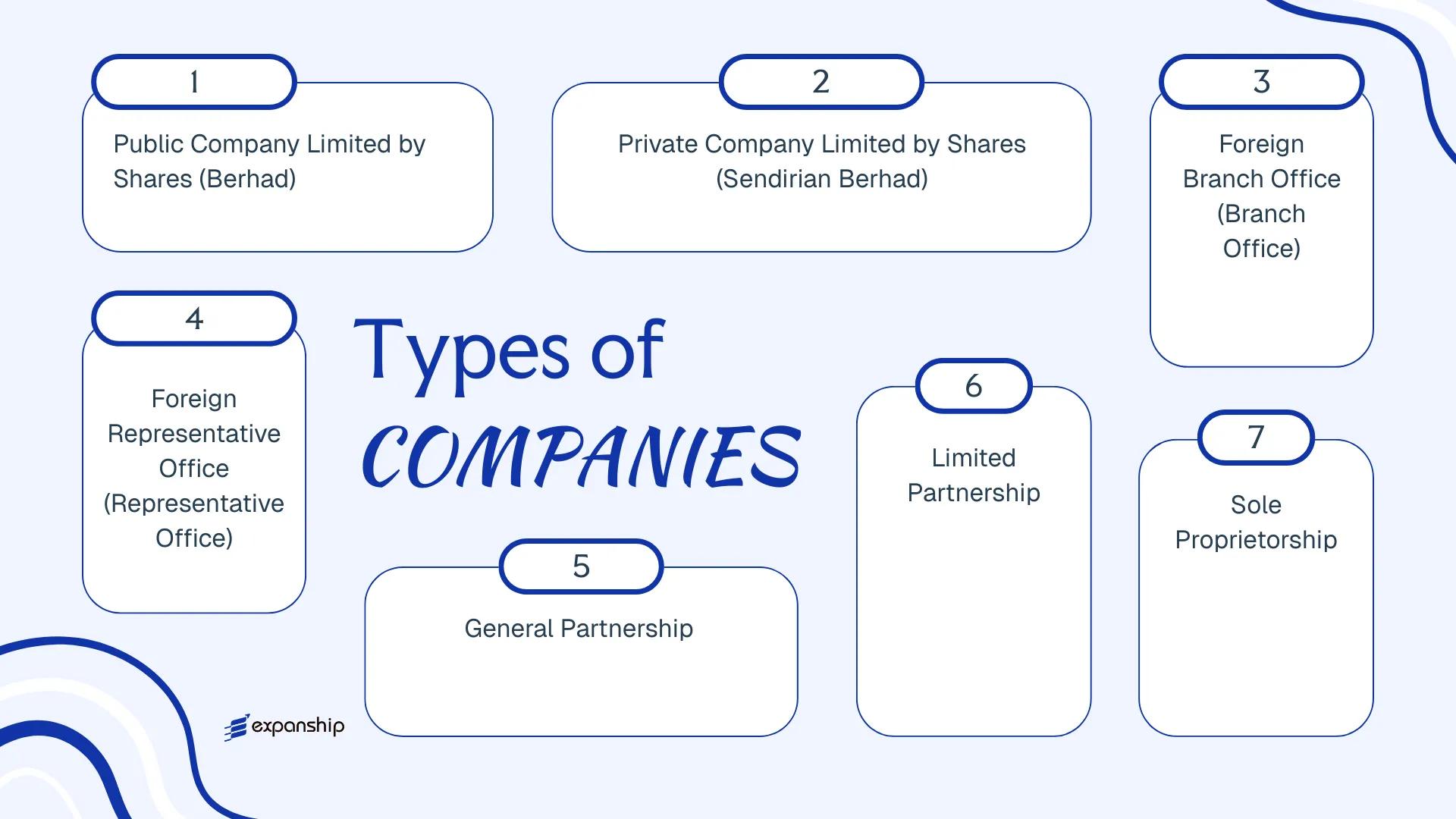

Several business structures in Brunei are available to both local and foreign investors. The types of business entities in Brunei recognized under statute include:

- Public Company Limited by Shares (Berhad)

- Private Company Limited by Shares (Sendirian Berhad)

- Branch Office

- Representative Office

- General Partnership

- Limited Partnership

- Sole Proprietorship

Each structure carries distinct liability, ownership, and compliance requirements. This article examines the legal basis, formation conditions, and operational parameters of each Brunei corporate entity option in turn.

An Overview of Business Structures in Brunei

Brunei's company law framework accommodates several distinct entity types, each governed primarily by the Companies Act, Cap. 39 and the Business Names Act, Cap. 92, with registration administered through the Registry of Companies and Business Names (ROCBN). An overview of business structures in Brunei shows that the available forms range from locally incorporated companies to foreign branch presences and unincorporated partnerships. Each structure carries different implications for liability, taxation, and operational scope.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Tax Status | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Public Company (Berhad) | Incorporated company | Limited to share capital | Taxable | Permitted | 2 shareholders | ROCBN | Companies Act, Cap. 39 |

| Private Company (Sdn. Bhd.) | Incorporated company | Limited to share capital | Taxable | Permitted | 1 shareholder | ROCBN | Companies Act, Cap. 39 |

| Branch Office | Extension of foreign entity | Unlimited (parent liable) | Taxable | Permitted | N/A | ROCBN | Companies Act, Cap. 39 |

| Representative Office | Non-trading presence | Unlimited (parent liable) | Generally exempt | Not permitted | N/A | ROCBN / MIPR | General approval framework |

| General Partnership | Unincorporated firm | Unlimited | Taxable | Permitted | 2 partners | ROCBN | Business Names Act, Cap. 92 |

| Limited Partnership | Unincorporated firm | Mixed (general/limited) | Taxable | Permitted | 2 partners | ROCBN | Business Names Act, Cap. 92 |

| Sole Proprietorship | Unincorporated business | Unlimited | Taxable | Permitted | 1 owner | ROCBN | Business Names Act, Cap. 92 |

Each of these structures is examined in full in the sections below.

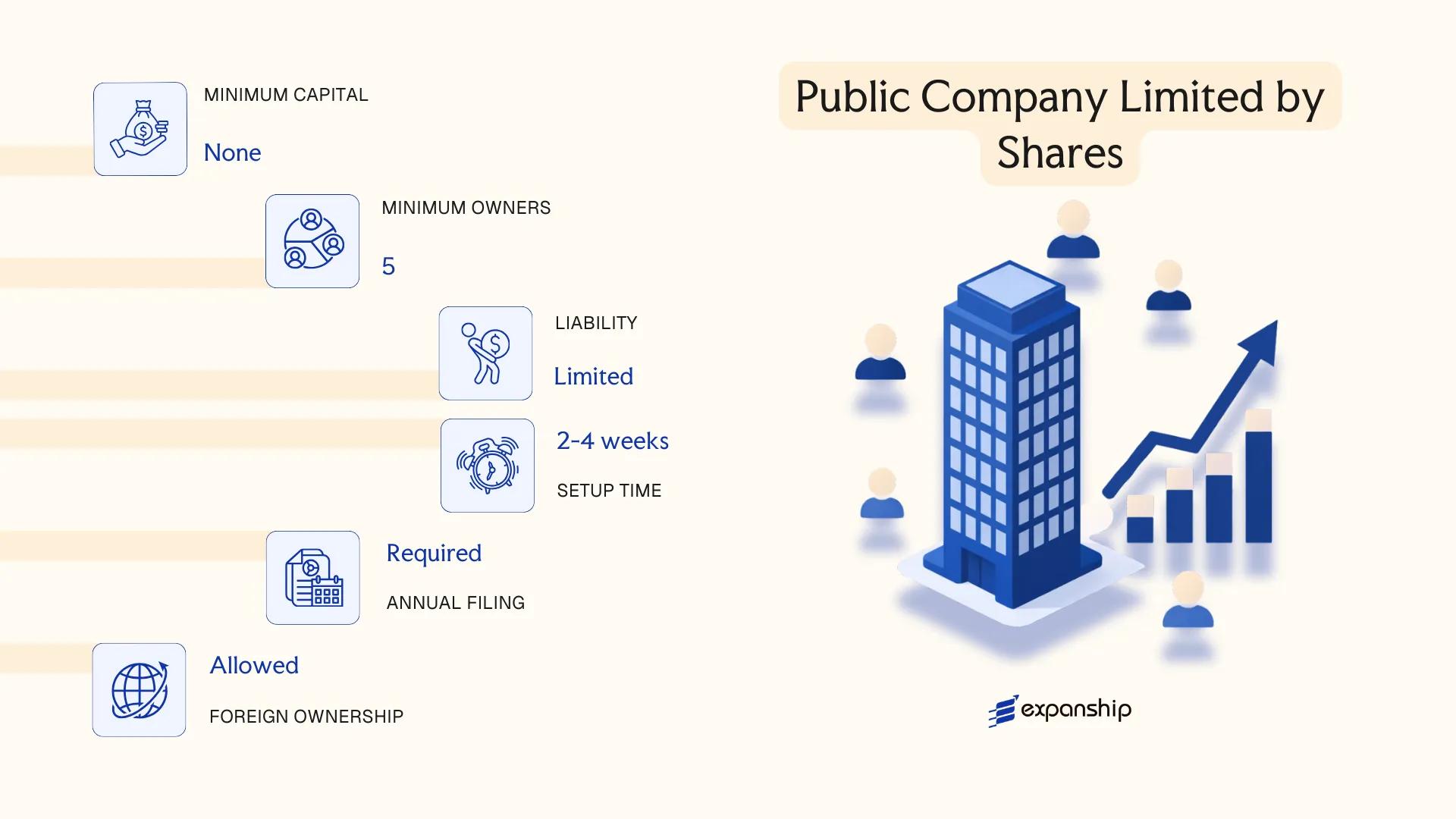

Public Company Limited by Shares (Berhad) Under the Companies Act, Cap. 39

Governed by the Companies Act, Cap. 39, a Brunei Berhad public company registration creates an entity with full separate legal personality, meaning the company can own assets, enter contracts, and incur liabilities independently of its shareholders. Liability of each shareholder is limited to the unpaid amount on their shares.

Unlike its private counterpart, a Berhad may offer shares to the public and, subject to meeting Brunei's listing requirements, apply for admission to the Autoriti Monetari Brunei Darussalam (AMBD)-regulated capital markets.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public company limited by shares | Incorporated under the Companies Act, Cap. 39 |

| Members | Shareholders (minimum 2, no maximum) | Directors: minimum 2; at least 1 must be ordinarily resident in Brunei |

| Local Presence | Registered office in Brunei required | A local company secretary must be appointed |

| Capital | No statutory minimum share capital (BND) | Shares must be denominated in Brunei dollars or a specified currency |

| Listing | May offer shares to the public | Subject to AMBD approval and applicable securities regulations |

| Privacy | Share register is publicly accessible | Directors and officers' details filed with the Registry of Companies |

Focus Points

- Taxation: Corporate income tax applies at a flat 18.5% on chargeable income; no capital gains tax, no VAT, and no withholding tax on dividends, though stamp duty applies to certain instruments.

- Annual Compliance: Audited financial statements required; annual general meetings (AGMs) must be held; annual returns filed with the Registry of Companies and Corporate Affairs (ROCCA).

- Economic Substance: Brunei has enacted substance requirements; entities deriving income from certain activities must demonstrate adequate local operations, staff, and expenditure.

- Treaty Access: Brunei maintains a limited but growing network of double taxation agreements, which a locally incorporated Berhad may access subject to treaty conditions.

- Conversion: A private Sendirian Berhad may re-register as a Berhad under the Companies Act, Cap. 39, provided it satisfies the requisite membership and compliance conditions.

Closing

A Berhad suits businesses seeking public capital-raising, large-scale commercial operations, or eventual stock exchange listing, though the associated disclosure obligations and governance requirements make it administratively demanding relative to a private structure.

This entity type is best suited for established enterprises planning to raise capital from the public or pursue a listing on a regulated exchange.

Company Incorporation in Brunei

Expanship assists with the end-to-end incorporation of Berhad and Sendirian Berhad companies under the Companies Act, Cap. 39.

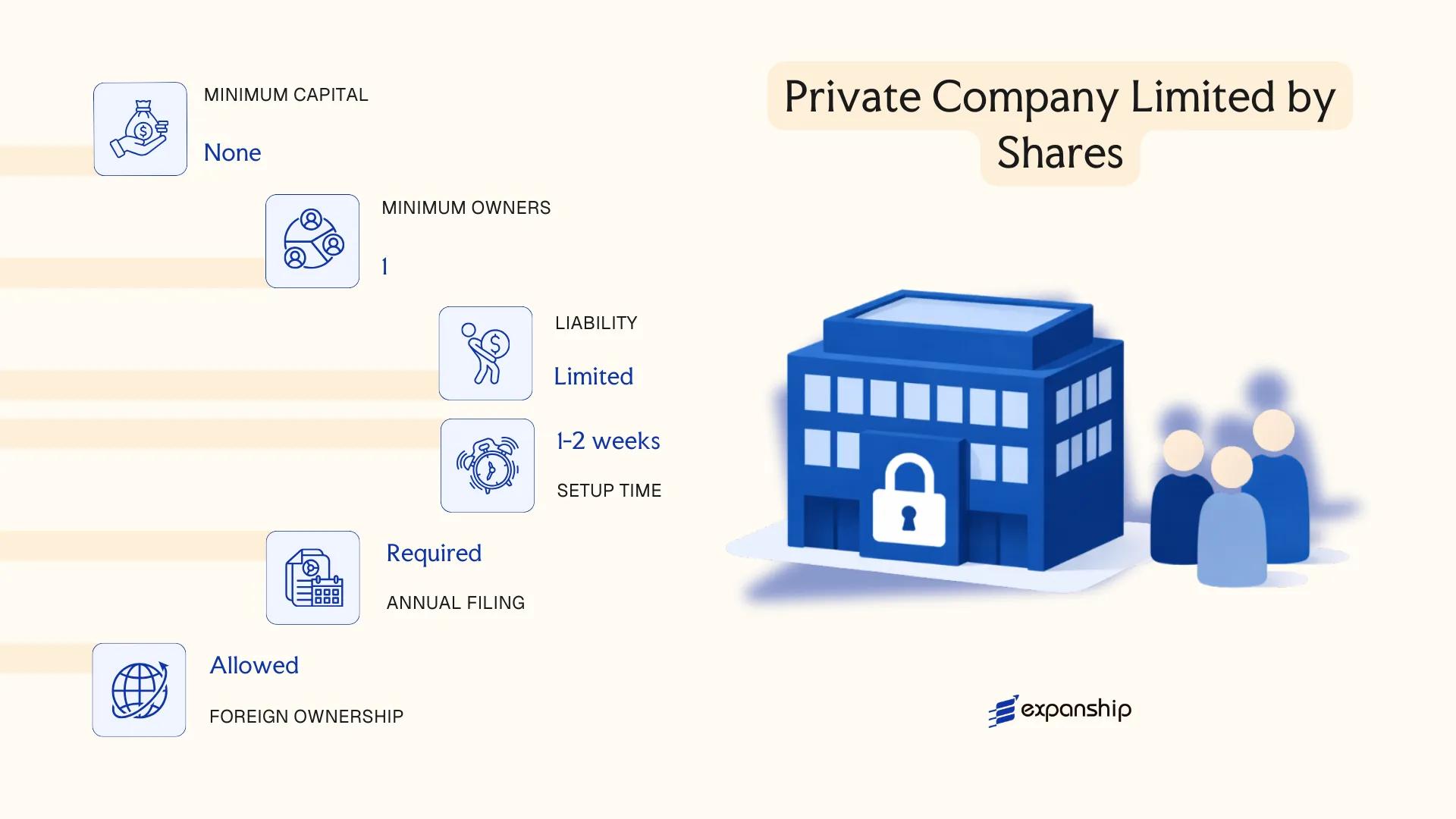

Private Company Limited by Shares (Sendirian Berhad) Under the Companies Act, Cap. 39

Brunei Sendirian Berhad company incorporation is governed by the Companies Act, Cap. 39, the same legislation that regulates public companies. The Sendirian Berhad (Sdn Bhd) structure carries separate legal personality, meaning the entity exists independently from its shareholders, and liability is capped at each member's unpaid share capital.

As a private limited company, the Sdn Bhd restricts the right to transfer shares and prohibits any invitation to the public to subscribe for shares or debentures. Registration is administered by the Registry of Companies and Business Names (ROCBN) under the Ministry of Finance and Economy.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private Company Limited by Shares | Suffix "Sdn Bhd" mandatory in company name |

| Members | Shareholders: min. 1, max. 50 | Corporate shareholders permitted; excludes employee share scheme holders |

| Directors | Min. 1 director; at least 1 must be ordinarily resident in Brunei | Residency condition applies to at least one director |

| Local Presence | Registered office address required in Brunei | Must be a physical address; PO Box alone not accepted |

| Share Capital | No statutory minimum; denominated in Brunei Dollar (BND) | Authorized and issued capital disclosed at incorporation |

| Privacy | Shareholder and director details filed with ROCBN | Register of members is not publicly searchable online |

Focus Points

- Taxation: Corporate income tax applies at a flat 18.5% on chargeable income; no VAT, no capital gains tax, no dividend withholding tax; stamp duty applies on certain instruments including share transfers.

- Economic Substance: Sdn Bhd entities conducting relevant activities may be subject to economic substance requirements under Brunei's domestic substance regulations.

- Annual Compliance: Annual returns and audited financial statements must be filed with ROCBN; audit exemptions are not broadly available for private companies.

- Treaty Access: Brunei's tax treaty network is limited; confirm treaty availability before relying on reduced withholding rates from counterpart jurisdictions.

- Conversion: An Sdn Bhd may convert to a public Berhad by passing the requisite resolutions and meeting public company thresholds under Cap. 39.

Closing

The private limited company Brunei Cap 39 structure suits trading operations, regional holding arrangements, and family-owned businesses where share transferability and public fundraising are not required. The liability shield is its primary structural advantage; the mandatory resident director and audit obligation add recurring compliance costs that should be factored into operational planning.

The Sdn Bhd is best suited for foreign investors and local entrepreneurs seeking a privately held, operationally active entity in Brunei with defined liability boundaries.

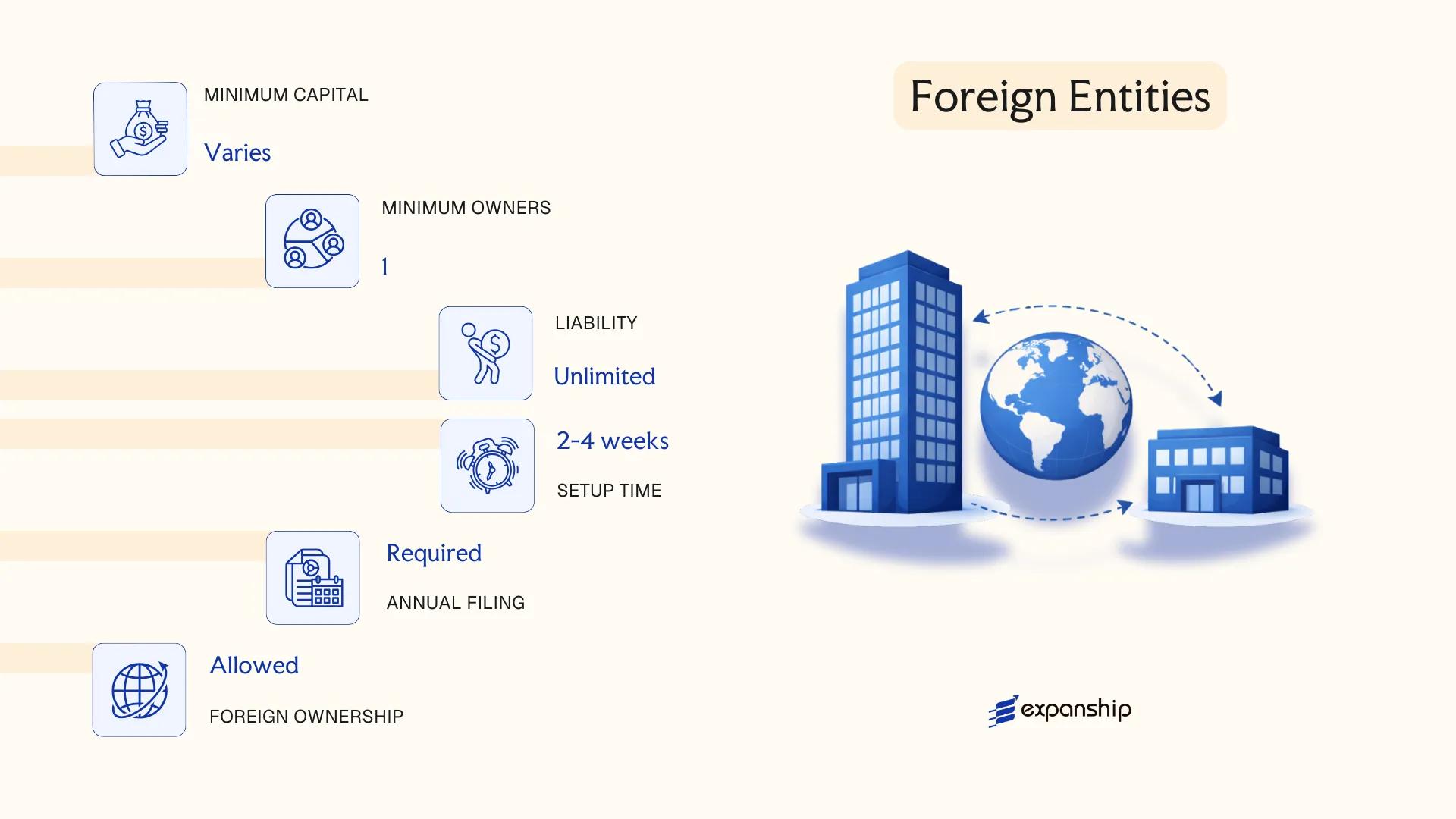

Foreign Entities in Brunei [Branch Office, Representative Office]

Foreign companies seeking a presence without incorporating a local subsidiary have two primary structural options: registering a foreign company branch office in Brunei or establishing a representative office. Both are governed under the Companies Act, Cap. 39, administered by the Registry of Companies and Business Names (ROCBN) under the Ministry of Finance and Economy.

A branch office is not a separate legal entity — it is an extension of the parent company, which retains full liability for the branch's obligations. A representative office operates under guidelines issued by the relevant ministry or authority, typically permitted only for liaison and promotional activities, not revenue-generating operations.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Form | Extension of foreign parent; no separate legal personality | Non-trading liaison office; no separate legal personality |

| Liability | Parent company bears full liability | Parent company bears full liability |

| Local Presence | Registered address in Brunei; local agent required | Registered address required |

| Permitted Activities | Commercial and trading activities | Liaison, market research, promotion only |

| Capital Requirement | No prescribed minimum | No prescribed minimum |

| Privacy | Parent company details publicly disclosed at ROCBN | Parent company details disclosed to relevant authority |

Focus Points

- Taxation: Branch profits are subject to corporate income tax at 18.5%; no GST or VAT currently applies; withholding tax applies to certain payments to non-residents.

- Economic Substance: No formal economic substance regime is currently imposed on branch offices, though physical presence requirements apply for registration.

- Annual Compliance: Branches must file annual returns and audited financial statements with ROCBN; representative offices have lighter filing obligations.

- Restrictions: Representative offices are prohibited from generating income, signing commercial contracts, or acting as an import/export agent.

- Conversion: A branch may be converted into a locally incorporated entity, though this requires a separate incorporation process under the Companies Act.

Closing

A branch office suits foreign firms that require operational presence for trading or service delivery without committing to full local incorporation, though the parent's unlimited exposure to branch liabilities is a material drawback. A representative office is appropriate only for pre-market entry or ongoing liaison functions where no revenue generation is anticipated.

Foreign companies testing the market or maintaining client relationships without transacting commercially are best served by a representative office; those requiring active operations should register a branch.

Partnerships in Brunei [General Partnership, Limited Partnership]

Partnerships are governed by the Partnership Act (Cap. 100) and the Limited Partnership Act (Cap. 101). A general partnership carries no separate legal personality — partners remain jointly and severally liable for business debts. Limited partnership registration Brunei follows a distinct statutory path under Cap. 101, which introduced a two-tier membership structure separating liability exposure between partner classes.

Registration for both forms is handled through the Registry of Companies and Business Names (ROCBN). Neither structure requires a minimum capital contribution, though both must register a principal place of business within the jurisdiction.

Key Characteristics

| Requirement | General Partnership | Limited Partnership |

|---|---|---|

| Governing Law | Partnership Act, Cap. 100 | Limited Partnership Act, Cap. 101 |

| Legal Personality | None | None |

| Members | Partners (min. 2, max. 20) | Min. 1 general partner + 1 limited partner; max. 20 total |

| Liability | Unlimited for all partners | Unlimited for general partners; capped at capital contribution for limited partners |

| Local Presence | Registered address in Brunei required | Registered address in Brunei required |

| Capital | No statutory minimum; BND denominated | No statutory minimum; limited partners' liability tied to contributed amount |

| Privacy | Partner details filed with ROCBN; publicly accessible | Same disclosure applies; general and limited partners listed on register |

Focus Points

- Taxation: Partnerships are generally treated as tax-transparent; individual partners are assessed on their share of income under personal tax rules, with corporate partners subject to corporate tax at 18.5% on their allocated profits.

- Annual Compliance: Annual renewal of registration with ROCBN is required; failure to renew can result in deregistration.

- Economic Substance: Partnerships engaged in certain prescribed activities may be subject to economic substance obligations under Brunei's substance regulations.

- Treaty Access: Neither partnership form qualifies as a resident entity for double tax treaty purposes in its own right; treaty benefits flow through to qualifying partners individually.

- Restrictions: General partners in a limited partnership cannot withdraw contributed capital in a manner that reduces the firm's ability to meet liabilities.

Sub-Types

General Partnership

All partners share management authority and bear unlimited personal liability. This structure suits small professional practices or family-operated trading businesses where partners accept equal exposure.

Limited Partnership

At least one general partner retains unlimited liability and management control, while limited partners contribute capital and remain passive. Limited partners who participate in management risk losing their liability protection under Cap. 101.

Closing

Partnerships suit joint ventures, professional services arrangements, and investment vehicles where pass-through tax treatment is preferable to corporate taxation, though the absence of separate legal personality means personal assets of general partners remain exposed to business creditors.

Limited partnerships are best suited to investment structures or fund arrangements where a clear separation between active management and passive capital contribution is required.

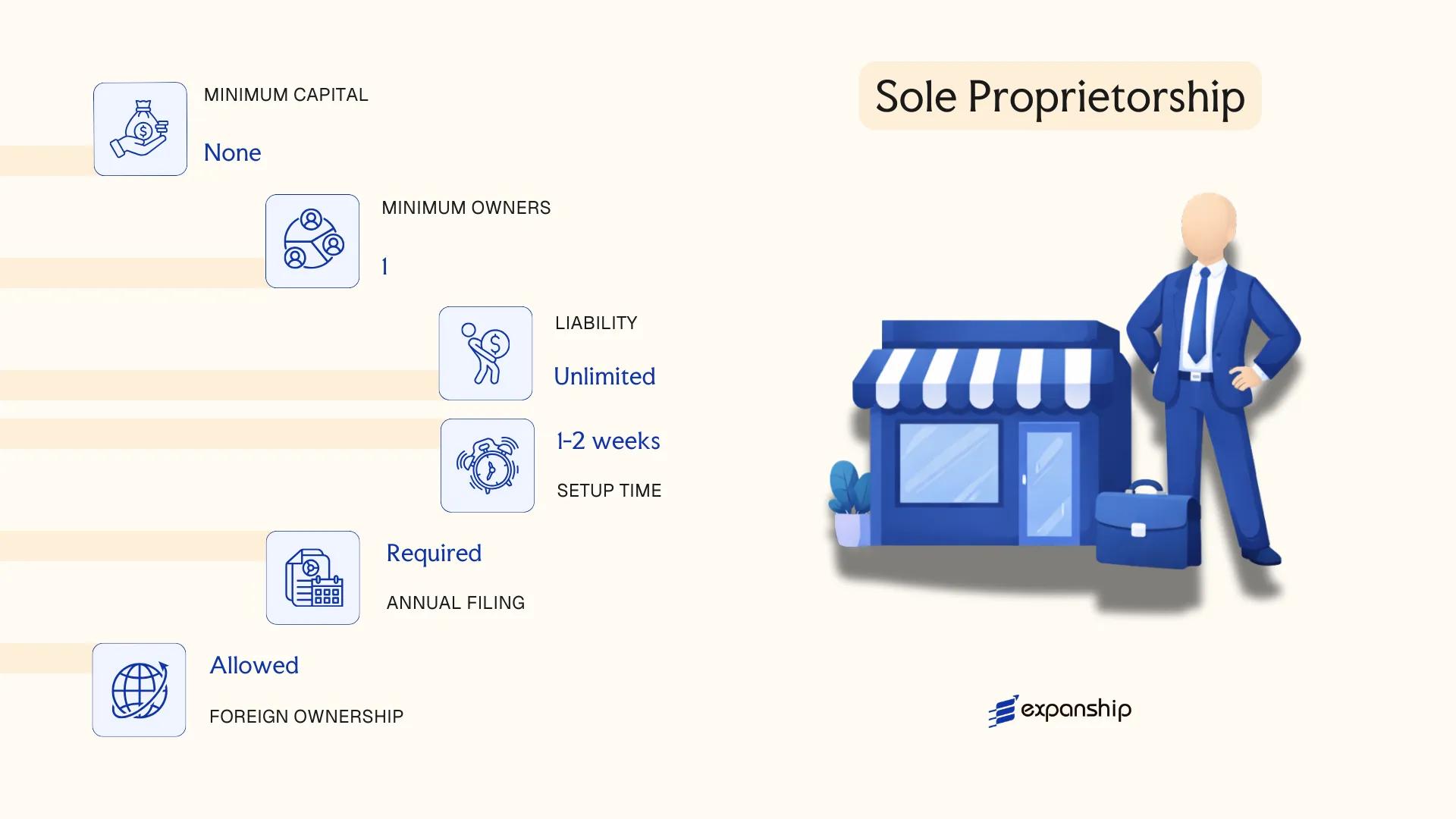

Sole Proprietorship Under the Business Names Act, Cap. 92

A sole proprietorship in Brunei is governed by the Business Names Act, Cap. 92, which requires any individual carrying on business under a name other than their own to register that name with the Registry of Business Names. Unlike a company incorporated under the Companies Act, Cap. 39, this structure carries no separate legal personality.

Because the business and the owner are legally the same, full personal liability attaches to all debts and obligations. Registration under the Business Names Act, Cap. 92 does not create a distinct legal entity — it records the trading name only.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated sole proprietorship | No separate legal personality from the owner |

| Referred To As | Proprietor | Single individual only; no partners or shareholders |

| Membership | 1 proprietor (minimum and maximum) | Must be an individual; corporations cannot register as sole proprietors |

| Local Presence | Registered business address required | Must maintain a local address on file with the Registry |

| Capital | No statutory minimum | Owner funds the business directly; no share capital structure |

| Privacy | Business name and owner details on public record | Registry records are accessible to the public |

Focus Points

- Taxation: Sole proprietors are taxed on business profits as personal income; Brunei currently imposes no personal income tax, making the effective tax burden on locally earned profits nil — though corporate tax, VAT, and withholding tax provisions do not apply to this structure.

- Annual Compliance: Registration must be renewed periodically with the Registry of Business Names; failure to renew can result in the registration lapsing.

- Economic Substance: No economic substance obligations apply, as this structure falls outside the scope of the economic substance framework targeting corporate entities.

- Conversion: A sole proprietorship can be wound up and a new company incorporated separately, but there is no direct statutory conversion mechanism into a company.

- Restrictions: Foreign nationals are generally not permitted to register a sole proprietorship; this structure is reserved for Brunei citizens and permanent residents.

Closing

A sole proprietorship suits small-scale, locally operated businesses with straightforward activities and a single owner who accepts full personal liability. The absence of personal income tax reduces the cost of operating in this form, but unlimited personal liability remains a significant structural constraint.

This structure is best suited for Bruneian citizens or permanent residents running low-risk, small-scale local businesses who require minimal administrative overhead.

How to Choose the Right Entity Type in Brunei

Selecting the correct corporate structure is a consequential decision, and understanding how to choose a business structure in Brunei requires looking beyond initial registration costs to the operational and legal implications that follow.

Why Your Entity Choice Matters

The structure you register shapes your tax position, reporting obligations, and legal exposure for the life of the business.

- Registering a branch office when you intend to conduct independent commercial activity locks you into the parent company's full liability and limits your ability to retain earnings locally as a separate legal entity.

- Choosing a structure without treaty access — such as an entity that does not qualify as a resident company under the Income Tax Act, Cap. 35 — means you cannot claim withholding tax reductions available under Brunei's double taxation agreements.

- Selecting an entity that requires audited financial statements when your business is a sole-person consultancy introduces recurring compliance costs that a sole proprietorship registered under the Business Names Act, Cap. 92 would not carry.

- Forming a private limited company when a partnership arrangement would suffice imposes annual filing obligations with the Registry of Companies and Business Names (ROCBN) that are disproportionate to the business scale.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors such as banking or insurance each point toward a distinct structure under Brunei's regulatory framework.

- Ownership and Management: A sole operator has little reason for a multi-director board structure, while a joint venture with foreign partners typically requires a private limited company to define equity and governance clearly.

- Tax Objectives: If access to Brunei's treaty network matters, confirm that your chosen entity qualifies as a tax-resident entity under the Income Tax Act, Cap. 35, rather than assuming residency by default.

- Local vs. External Operations: A representative office cannot generate revenue from local sources; if your business model involves billing Brunei-based clients directly, a registered company or branch is required.

- Substance Capacity: If you cannot realistically maintain a physical office and resident staff, confirm whether your entity type carries substance requirements before registering.

- Exit Strategy: Not all structures permit redomiciliation or straightforward conversion — verify winding-up and transfer procedures under the Companies Act, Cap. 39 before committing.

Corporate Compliance Services in Brunei

Annual filing, ROCBN obligations, and ongoing regulatory support for companies incorporated in Brunei.

Conclusion

This incorporating a company in Brunei guide has covered the full range of structures available under the Companies Act, Cap. 39, the Business Names Act, Cap. 92, and the Limited Partnerships Order. Each form of business carries a distinct profile: the Sendirian Berhad suits resident-controlled private ventures, while the Berhad serves firms pursuing public capital markets. Branch offices give foreign corporations direct operational presence without separate legal personality. A general partnership suits small collaborative ventures, and a limited partnership separates active management from passive investment. Sole proprietorships remain the entry point for individual traders.

The Sendirian Berhad is by far the most commonly registered structure. Regulatory oversight from the Registry of Companies and Business Names continues to evolve, with Brunei progressively refining its corporate governance framework. Your choice of entity will ultimately shape tax exposure, liability, and long-term operational flexibility.

How Expanship Can Assist You

Expanship's Brunei company incorporation services cover every entity structure discussed in this blog — from a Sendirian Berhad registered under the Companies Act, Cap. 39 to a sole proprietorship filed under the Business Names Act, Cap. 92. Our team works directly with the Registry of Companies and Business Names (ROCBN) on your behalf, handling filings, correspondence, and documentation from start to finish.

Across each engagement, the scope of our professional company formation Brunei services includes:

- Preparation and legalization of incorporation documents

- Registered agent and registered office provision

- Government filing and ROCBN liaison

- Post-incorporation compliance management, including annual returns

- Banking introduction assistance for your Brunei entity

Reach out through Expanship Brunei to discuss which structure fits your specific situation.

Frequently Asked Questions (FAQ)

The Private Company Limited by Shares, known as a Sendirian Berhad (Sdn Bhd), is the most widely registered structure. Its liability protection, flexible shareholding, and suitability for both local and foreign-owned businesses make it the default choice for most commercial activities.

A Branch Office is not a separate legal entity; it extends the liability and obligations of the foreign parent company. A Sdn Bhd, by contrast, is incorporated locally under Cap. 39, holds its own legal personality, and is subject to local corporate tax independently of any overseas parent.

Among registered structures, a Sdn Bhd with nominee shareholders provides the greatest degree of confidentiality. Beneficial ownership is not required to appear on publicly searchable registry filings, though ROCBN reporting obligations still apply. Nominee director and shareholder arrangements are permissible under Brunei law.

No. A Sdn Bhd requires a minimum of one director and one shareholder, so a sole individual can incorporate one. General and Limited Partnerships under the Business Names Act and the Limited Partnerships Act each require at least two partners, making single-person formation impossible for those structures.

Foreigners may incorporate a Sdn Bhd or register a Branch Office, though certain sectors require local participation under Brunei's foreign investment policies. A Representative Office is also available but is restricted to non-commercial activities and cannot generate revenue within the country.

Conversion from a Sole Proprietorship or Partnership into a Sdn Bhd is generally achievable through a new incorporation process rather than a formal statutory conversion. Direct re-registration of one corporate form into another is not broadly provided for under Cap. 39, so restructuring typically involves winding down the existing entity.

No. Sole Proprietorships, General Partnerships, and Branch Offices do not possess separate legal personality. The Sdn Bhd and the Public Company Limited by Shares (Berhad) are the primary structures that achieve full legal separation between the entity and its owners under Cap. 39.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.