Key Takeaways

- Bahrain imposes no corporate income tax on most commercial activities, making it a zero-tax jurisdiction for the majority of business structures outside specific regulated sectors.

- The With Limited Liability Company (WLL) is the most widely registered entity in Bahrain, offering liability protection without the capital requirements associated with a Bahraini Shareholding Company (BSC).

- Company registration and licensing in Bahrain are administered by the Ministry of Industry and Commerce (MOIC) through the Sijilat commercial registration platform, with financial services requiring additional Central Bank of Bahrain authorization.

- Foreign firms that wish to operate in Bahrain without generating local revenue may establish a representative office, while those executing contracts directly must register a branch office instead.

Introduction to Entity Types in Bahrain

Bahrain is an archipelago of approximately 40 islands situated in the Arabian Gulf, bordered by Saudi Arabia to the west and Qatar to the southeast. An independent constitutional monarchy, the country has developed a legal framework for commercial activity that draws from both civil law traditions and Gulf Cooperation Council standards.

Company registration and licensing fall under the authority of the Ministry of Industry and Commerce (MOIC), which administers the Sijilat commercial registration platform. Certain regulated activities — particularly in financial services — require additional licensing from the Central Bank of Bahrain.

Bahrain applies no corporate income tax on most commercial activities, making it a zero-tax jurisdiction for the majority of business types. Exceptions exist for specific sectors, but the general posture is one of minimal direct taxation.

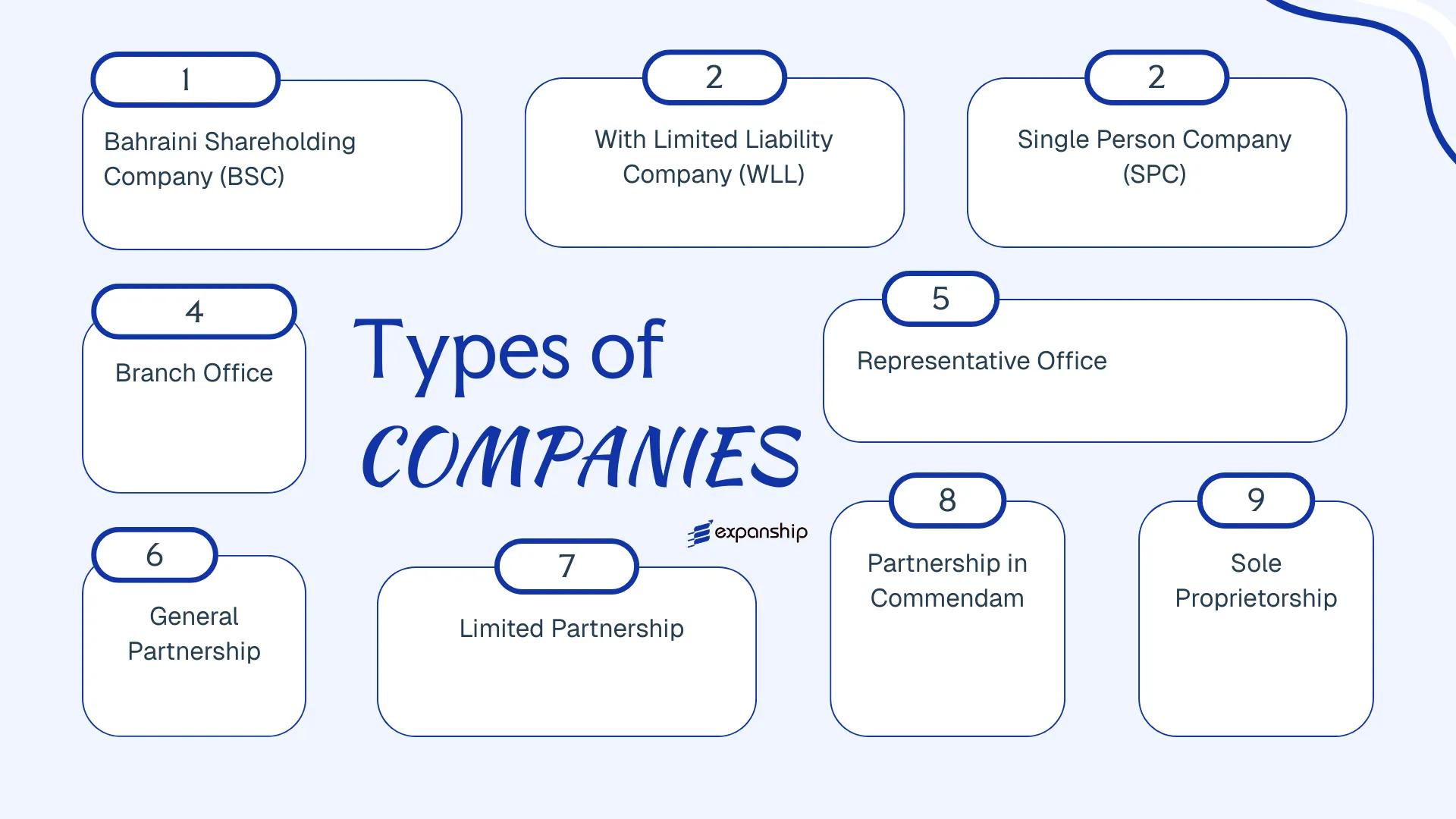

The types of business entities in Bahrain available to local and foreign investors include the Bahraini Shareholding Company (BSC), the With Limited Liability Company (WLL), the Single Person Company (SPC), the Branch Office, the Representative Office, the General Partnership, the Limited Partnership, the Partnership in Commendam, and the Sole Proprietorship. Each structure carries distinct rules on ownership, liability, and permitted activities — all of which this article examines in turn.

An Overview of Business Structures in Bahrain

Bahrain's company law framework provides several distinct entity types, each governed primarily by the Commercial Companies Law (Legislative Decree No. 21 of 2001) and its subsequent amendments. The Ministry of Industry and Commerce (MOIC), operating alongside the Bahrain Investors Centre, serves as the principal regulatory authority for company formation and ongoing compliance. Each structure carries different implications for ownership, liability, and permitted commercial activity.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Bahraini Shareholding Company (BSC) | Public / Closed corporation | Limited to shares | Subject to applicable taxes | Yes | 7 shareholders (public); 2 (closed) | MOIC / CBB (if regulated) | CCL Decree No. 21/2001 |

| With Limited Liability Company (WLL) | Private limited company | Limited to capital | Subject to applicable taxes | Yes | 2 shareholders | MOIC | CCL Decree No. 21/2001 |

| Single Person Company (SPC) | Sole-shareholder LLC | Limited to capital | Subject to applicable taxes | Yes | 1 shareholder | MOIC | CCL Decree No. 21/2001 |

| Branch Office | Extension of foreign entity | Parent bears full liability | Subject to applicable taxes | Restricted | N/A | MOIC | CCL Decree No. 21/2001 |

| Representative Office | Non-trading presence | Parent bears full liability | Generally exempt | No | N/A | MOIC | CCL Decree No. 21/2001 |

| General Partnership | Partnership | Unlimited, joint | Subject to applicable taxes | Yes | 2 partners | MOIC | CCL Decree No. 21/2001 |

| Limited Partnership | Partnership | Mixed (general/limited) | Subject to applicable taxes | Yes | 2 partners | MOIC | CCL Decree No. 21/2001 |

| Partnership in Commendam | Hybrid partnership | Mixed (general/limited) | Subject to applicable taxes | Yes | 2 partners | MOIC | CCL Decree No. 21/2001 |

| Sole Proprietorship | Individual trading entity | Unlimited personal | Subject to applicable taxes | Yes | 1 individual | MOIC | Commercial Registration Law |

Each of these structures is examined in full in the sections below.

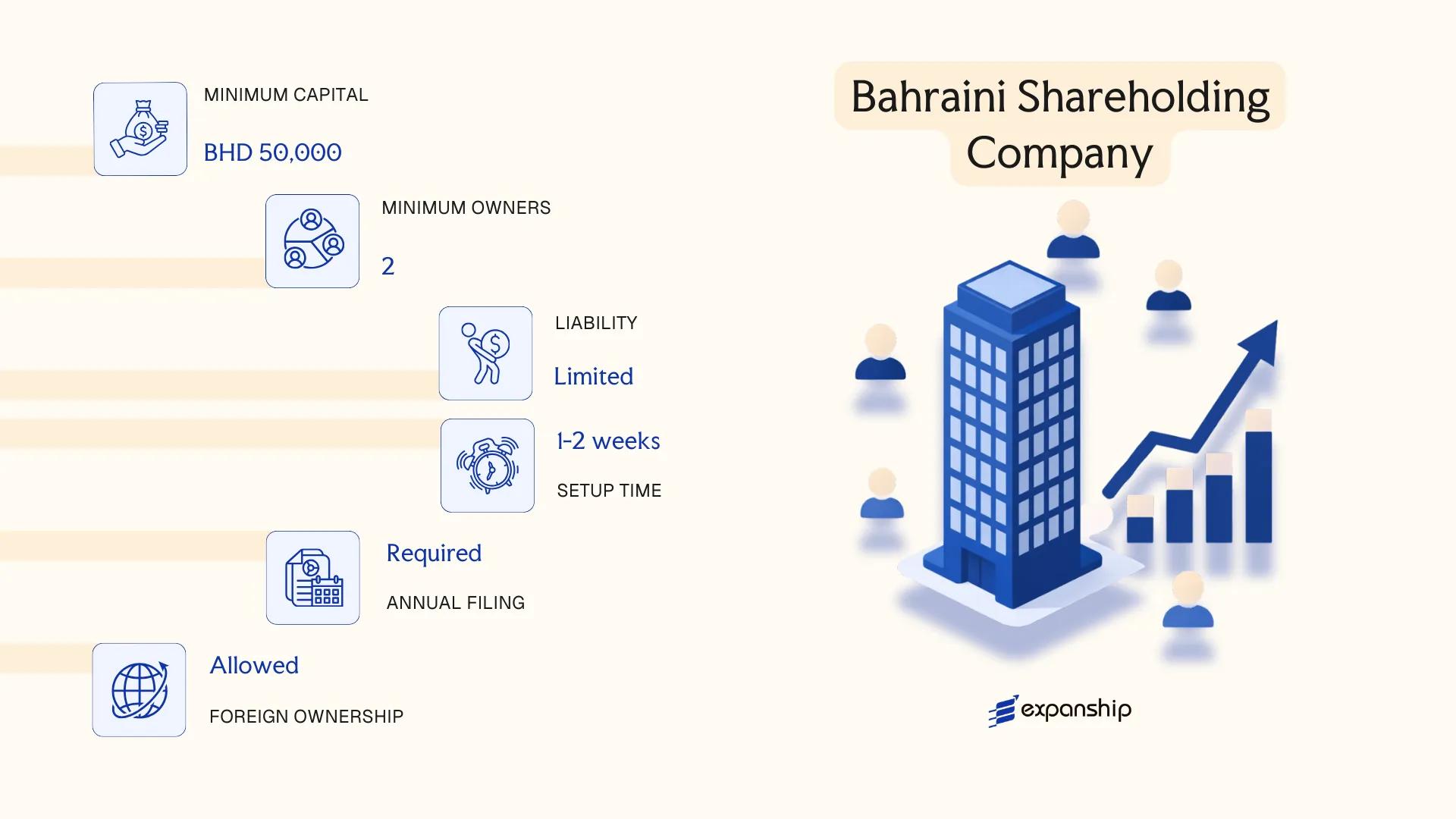

Bahraini Shareholding Company (BSC)

The Bahraini Shareholding Company (BSC) is governed by Legislative Decree No. 21 of 2001 (the Commercial Companies Law), along with its subsequent amendments. Meeting Bahrain BSC shareholding company requirements places you within a structure that carries full separate legal personality, with shareholder liability capped to the value of subscribed shares.

Capital is divided into freely transferable shares, making this the only Bahraini entity type capable of raising funds from the public through a stock exchange listing.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Shareholding Company (BSC) | Separate legal personality; shareholders not personally liable beyond share subscription |

| Governing Bodies | Board of Directors (minimum 3); General Assembly of Shareholders | Directors need not be shareholders; an audit committee is required for public BSCs |

| Shareholders | Minimum 2 (Private BSC); minimum 7 (Public BSC) | No maximum shareholder limit under the Commercial Companies Law |

| Local Presence | Registered office address within Bahrain required | Must maintain operational records locally; MOIC registration mandatory |

| Capital | BHD 250,000 minimum (Private BSC); BHD 1,000,000 minimum (Public BSC) | Capital denominated in Bahraini Dinar; public BSC capital must be fully subscribed at formation |

| Share Transferability | Shares freely transferable in principle | Private BSC constitutive documents may impose pre-emption rights or transfer restrictions |

Focus Points

- Taxation: No corporate income tax on most commercial activities; Bahrain VAT applies at 10% on applicable supplies; no withholding tax on dividends or interest; no stamp duty on share transfers. See National Bureau for Revenue for current VAT obligations.

- Economic Substance: BSCs conducting relevant activities as defined under Resolution No. 55 of 2018 must satisfy substance requirements, including adequate local expenditure and qualified personnel.

- Annual Compliance: Mandatory annual general assembly, audited financial statements filed with the Ministry of Industry and Commerce (MOIC), and renewal of commercial registration each year.

- Conversion: A private BSC may convert to a public BSC through a resolution passed by an extraordinary general assembly, subject to MOIC and Bahrain Bourse approvals where a listing is sought.

- Foreign Ownership: Up to 100% foreign ownership is permitted in most sectors, though certain regulated industries retain nationality requirements.

Sub-Types

Private Shareholding Company (BSC Closed)

Shares in a private BSC are not offered to the public and cannot be listed on the Bahrain Bourse. This structure is used by family-owned groups, joint ventures, and holding entities where capital pooling is required but public fundraising is not.

Public Shareholding Company (BSC Public)

A public BSC may list its shares on the Bahrain Bourse and offer securities to the general public, placing it under the additional regulatory oversight of the Central Bank of Bahrain for licensed activities and the MOIC for corporate governance requirements. This structure is typically used by banks, insurance firms, and large commercial enterprises.

Suitable For

The BSC suits large-scale commercial operations, regulated financial entities, and businesses anticipating future capital raising or public listing. The freely transferable share structure supports complex investor arrangements. The primary limitation is the high minimum capital threshold and the administrative burden of mandatory audits and board governance obligations, which make this structure disproportionate for small or single-investor businesses.

The BSC is best suited for established businesses, financial institutions, or investor groups requiring a scalable, institutionally recognised corporate structure with formal governance.

Company Incorporation in Bahrain

Set up your Bahraini Shareholding Company or other business structure with end-to-end support across registration, compliance, and licensing.

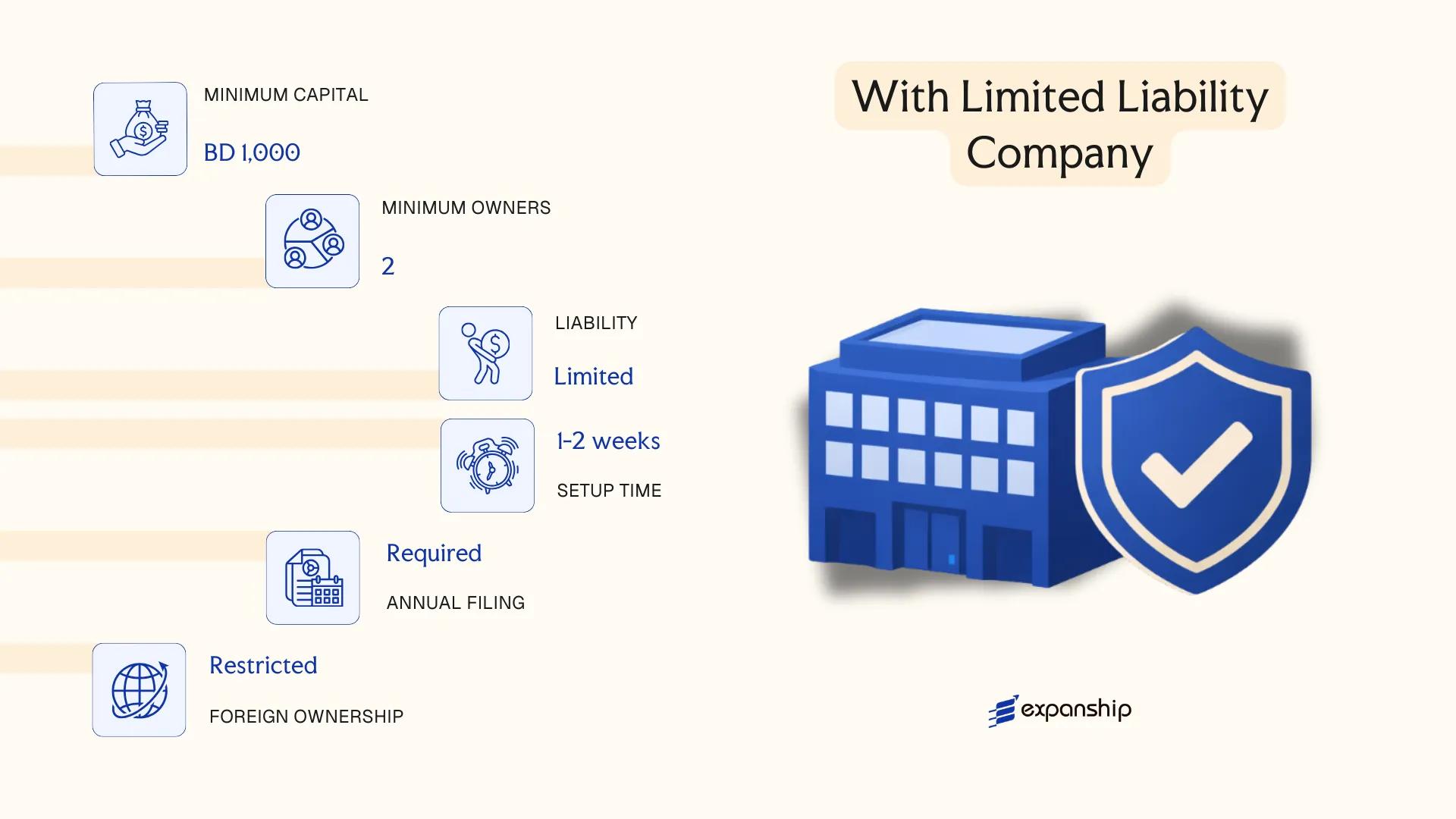

With Limited Liability Company (WLL)

Bahrain WLL company formation is governed by the Commercial Companies Law, Legislative Decree No. 21 of 2001, as amended. The With Limited Liability Company is a separate legal entity, meaning the business carries its own rights and obligations distinct from its members. Liability is confined to each member's capital contribution.

Structurally, the WLL sits between a private shareholding company and a simpler sole proprietorship. It does not issue shares to the public, and ownership is represented by quotas rather than tradeable shares.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | With Limited Liability Company (WLL) | Separate legal personality; liability limited to capital contribution |

| Members | 2 to 50 members | Referred to as members; no single-member WLL — use SPC for that |

| Foreign Ownership | Up to 100% in permitted sectors | Subject to MOIC approval and activity-specific restrictions |

| Local Presence | Registered office address in Bahrain required | Must maintain a physical or registered address; no mandatory local agent |

| Capital | BHD 20,000 minimum (general); higher thresholds for regulated activities | No public subscription; capital divided into quotas |

| Privacy | Member details filed with MOIC; not publicly searchable in full | Beneficial ownership registered with relevant authorities |

Focus Points

- Taxation: No corporate income tax for most commercial activities; 46% rate applies exclusively to oil, gas, and hydrocarbon companies; VAT at 10% applies; no withholding tax or stamp duty on standard transactions.

- Economic Substance: Bahrain does not impose economic substance requirements equivalent to those in certain offshore jurisdictions, though regulated activities may carry sector-specific presence obligations.

- Annual Compliance: Annual renewal of the Commercial Registration (CR) with the Ministry of Industry and Commerce (MOIC) is mandatory, along with updated financial records.

- Restrictions: Certain professional and regulated activities are excluded from the WLL structure and require alternative licensing arrangements.

- Conversion: A WLL may be converted to a Bahraini Shareholding Company (BSC) subject to meeting the applicable capital and membership thresholds under the Commercial Companies Law.

Closing

The WLL is commonly used for trading, services, and holding structures where public fundraising is not required and members prefer contained liability. A notable limitation is the 50-member cap, which restricts scalability for businesses anticipating broad equity participation.

The WLL structure suits small to mid-sized businesses, joint ventures, and foreign investors seeking a straightforward operational entity in Bahrain without the compliance burden of a public shareholding company.

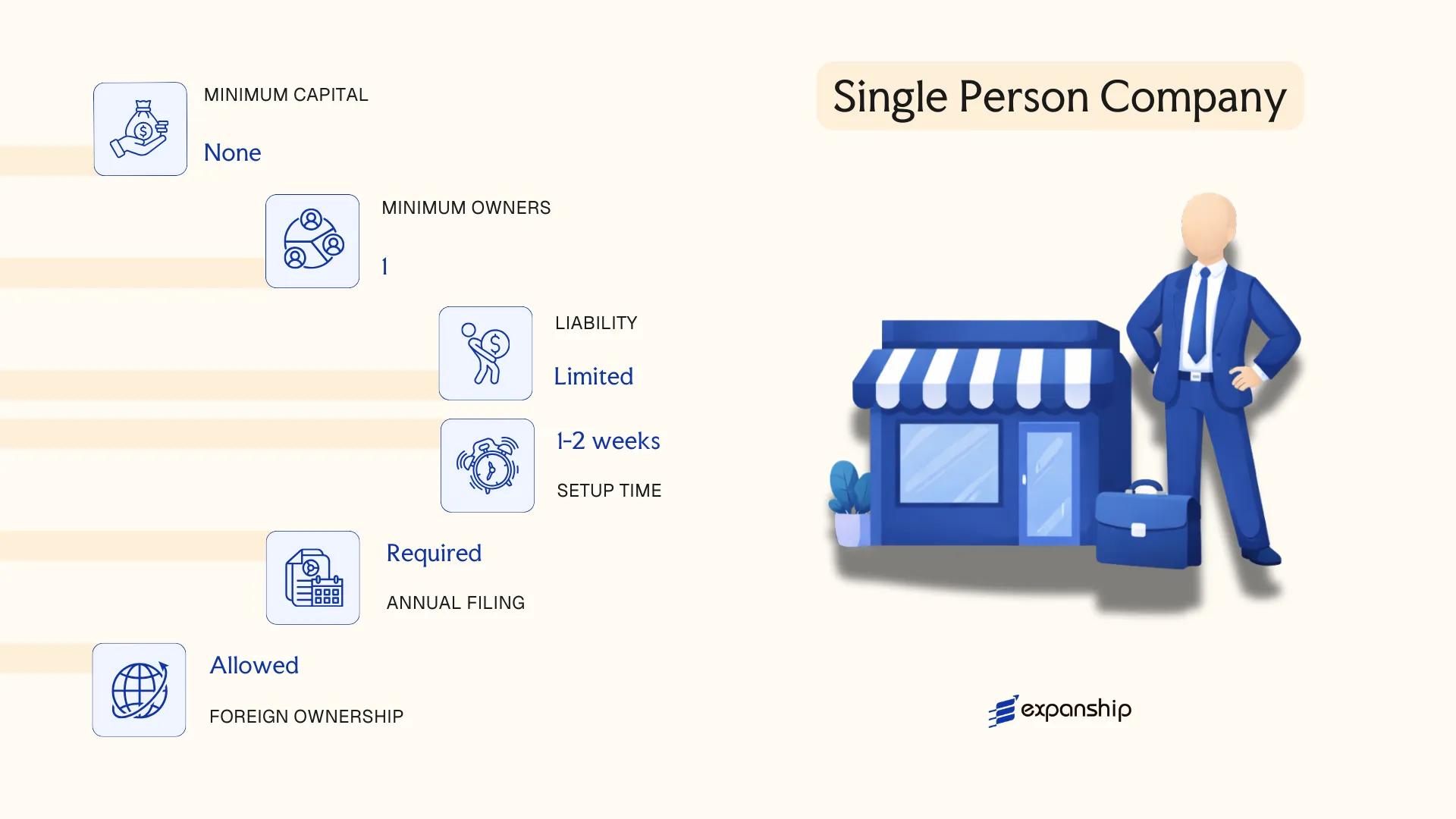

Single Person Company (SPC)

Bahrain Single Person Company registration is governed by the Commercial Companies Law (Legislative Decree No. 21 of 2001, as amended). The SPC is a distinct legal entity that separates the personal assets of its sole owner from the company's liabilities, providing full limited liability protection without requiring a second shareholder.

Structurally, this entity functions as a hybrid: it retains the corporate characteristics of a WLL but is owned entirely by one natural person or legal entity. The Ministry of Industry and Commerce (MOIC) oversees its incorporation and ongoing compliance.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability (Single Member) | Separate legal personality; owner not personally liable for company debts |

| Members | 1 sole owner (natural person or corporate entity) | No minimum additional shareholders required |

| Management | Manager(s) appointed by the owner | Owner may act as sole manager |

| Registered Office | Physical address in Bahrain mandatory | Virtual offices may not satisfy MOIC requirements |

| Share Capital | BHD 50 minimum (no paid-up requirement for most activities) | Certain licensed activities require higher capital |

| Privacy | Ownership details filed with MOIC; not publicly searchable by default | Beneficial ownership disclosures apply under AML regulations |

Focus Points

- Taxation: Subject to Bahrain's standard tax regime — no corporate income tax for most sectors (except oil and gas at 46%), no withholding tax, no capital gains tax; VAT at 10% applies to taxable supplies above the registration threshold.

- Economic Substance: Activities such as holding, financing, or IP may trigger Economic Substance Regulations obligations requiring adequate physical presence and local expenditure.

- Annual Compliance: Annual renewal of the Commercial Registration (CR) with MOIC is required, along with maintenance of statutory records and audited financials where applicable.

- Conversion: An SPC can be converted into a WLL or other corporate form if the owner wishes to admit additional shareholders at a later stage.

- Restrictions: A single natural person may generally register only one SPC; certain regulated activities (banking, insurance) require alternative structures.

Closing

The SPC suits solo founders, consultants, and holding structures where a single natural or legal person requires full operational control with corporate liability protection. The primary limitation is the restriction on admitting shareholders without first converting to another entity type.

The SPC is most appropriate for individual entrepreneurs and wholly owned subsidiaries seeking a straightforward corporate structure with limited liability under sole ownership.

Foreign Company Structures in Bahrain [Branch Office, Representative Office]

A foreign company branch office Bahrain registration is governed by the Commercial Companies Law (Legislative Decree No. 21 of 2001, as amended) and administered through the Ministry of Industry and Commerce (MOIC). Neither a branch nor a representative office constitutes a separate legal entity — both remain extensions of the parent company, which retains full legal and financial responsibility for their activities.

Registration is processed through MOIC's Sijilaat portal, and in most cases, foreign firms must obtain a Commercial Registration (CR) prior to commencing operations. Certain regulated activities require additional approvals from sector-specific authorities such as the Central Bank of Bahrain (CBB).

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Form | Extension of parent company; no separate legal personality | Extension of parent company; no separate legal personality |

| Permitted Activities | Revenue-generating commercial activities within approved scope | Non-commercial activities only (market research, liaison, promotion) |

| Management | Appointed local manager or authorised representative | Appointed liaison officer |

| Local Presence | Registered office address required; local agent may be required depending on activity | Registered office address required |

| Minimum Capital | No statutory minimum; parent company's capital backs the branch | None |

| Bahraini Ownership | 100% foreign ownership permitted in most sectors | 100% foreign ownership permitted |

| Privacy | Parent company details publicly disclosed via CR | Parent company details publicly disclosed |

Focus Points

- Taxation: Branches are subject to the same tax framework as locally incorporated entities — currently no corporate income tax for most sectors; VAT at 10% applies where the branch conducts taxable supplies; no withholding tax on remittances to the parent.

- Economic Substance: Branches conducting relevant activities may be subject to economic substance requirements under Bahrain's ES rules.

- Annual Compliance: Annual renewal of the Commercial Registration is required; audited financial statements of the parent may need to be filed with MOIC.

- Treaty Access: Access to Bahrain's double tax treaties is generally available to branches, though treaty eligibility depends on the specific treaty terms and the parent's residency.

- Restrictions: A representative office cannot invoice clients, sign commercial contracts, or generate revenue — any deviation risks reclassification or regulatory action.

Sub-Types

Branch Office

A branch office may conduct the same commercial activities as the parent company, subject to MOIC approval and any sector-specific licensing. It can enter into contracts, generate revenue, and employ staff directly.

Representative Office

A representative office is restricted to promotional and liaison functions on behalf of the parent. It cannot conduct revenue-generating activities, making it unsuitable for firms seeking operational presence.

Branches suit foreign firms that want direct operational presence without incorporating a new legal entity locally, though the parent assumes unlimited liability for all branch obligations — there is no liability ring-fencing between the two.

Foreign companies testing market entry or fulfilling a specific contract in Bahrain before committing to a locally incorporated entity.

Partnership Structures in Bahrain [General Partnership, Limited Partnership, Partnership in Commendam]

Partnership structures in Bahrain are governed by the Commercial Companies Law (Legislative Decree No. 21 of 2001, as amended). Three distinct forms exist under this framework: the general partnership, the limited partnership, and the partnership in commendam. Each carries different liability profiles, making the choice of structure consequential for the partners involved.

All three forms require registration with the Ministry of Industry and Commerce (MOIC) and must be listed in the Commercial Register. A partnership agreement defines the internal governance, profit distribution, and capital contributions — this document is central to the formation process.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Partnership (contractual entity) | Separate legal personality upon registration |

| Members | Partners (general or limited) | Minimum 2 partners; no statutory maximum |

| Local Presence | Registered address in Bahrain required | Physical office or registered agent address |

| Capital | BHD; no statutory minimum | Defined in the partnership agreement |

| Liability | Varies by partner class | General partners: unlimited; limited partners: capped at contribution |

| Privacy | Partnership agreement not fully public | Partner details disclosed in Commercial Register |

Focus Points

- Taxation: No corporate income tax on most activities; VAT applies at 10% where applicable; no withholding tax or stamp duty on profit distributions.

- Annual Compliance: Annual financial statements required; audit obligations depend on the partnership type and size.

- Foreign Ownership: General partnerships typically require Bahraini partner involvement; structures vary by licensed activity.

- Conversion: Partnerships may convert to other commercial entities through MOIC procedures, subject to partner consent.

- Treaty Access: Access to Bahrain's tax treaty network depends on residency status and the nature of income derived.

Sub-Types

General Partnership

Every partner holds unlimited joint and several liability for the firm's obligations. This structure suits small, trust-based businesses where all partners participate actively in management.

Limited Partnership

At least one general partner bears unlimited liability, while one or more limited partners are liable only to the extent of their capital contribution. Limited partners are restricted from participating in management.

Partnership in Commendam

A hybrid form where the managing partner (commendam manager) operates the business, and silent investors contribute capital without management rights. Their liability is confined to their invested capital, making this arrangement suited to investment-oriented structures where one party contributes expertise and another contributes funds.

Closing

Partnership structures are used primarily for professional services, family-owned trading operations, and joint ventures where partners prefer contractual flexibility over a corporate framework. The absence of a statutory minimum capital requirement is a practical advantage; however, unlimited liability for general partners poses a significant personal financial risk.

This structure is most appropriate for small businesses or professional firms where partners have an established relationship and require a flexible, low-cost formation with minimal regulatory overhead.

Sole Proprietorship

Sole proprietorship registration in Bahrain is governed by the Commercial Companies Law (Legislative Decree No. 21 of 2001) and administered through the Ministry of Industry and Commerce (MOIC) via the Sijilaat commercial registration portal. Unlike other business structures, a sole proprietorship does not constitute a separate legal entity from its owner — the individual and the business are legally one and the same.

This means the proprietor bears unlimited personal liability for all debts and obligations of the business. No liability shield separates personal assets from business exposure.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole Proprietorship (Unincorporated) | No separate legal personality from the owner |

| Member Designation | Proprietor | Single individual only |

| Ownership | 1 proprietor (minimum and maximum) | Must be a natural person; Bahraini nationals or eligible GCC nationals in most activities |

| Local Presence | Registered commercial address required | Must maintain a physical or registered business address in Bahrain |

| Capital | No statutory minimum capital | Capital declared at registration for record purposes only |

| Nationality Restriction | Generally restricted to Bahraini or GCC nationals | Foreign nationals face significant activity restrictions under current MOIC rules |

Focus Points

- Taxation: No corporate income tax applies; however, VAT at 10% applies if annual turnover exceeds the mandatory registration threshold of BHD 37,500.

- Annual Compliance: Commercial registration must be renewed annually through Sijilaat; failure to renew results in suspension of the CR.

- Economic Substance: Sole proprietorships are generally outside the scope of Bahrain's Economic Substance Regulations, which target specific regulated activities conducted by legal entities.

- Conversion: The structure can be converted to a more formal entity type, such as a WLL or SPC, through MOIC, though the process requires a new registration rather than a direct conversion.

- Restrictions: Foreign nationals are largely excluded from operating under this structure across most commercial activities.

Closing

A sole proprietorship suits small-scale, owner-operated trading or service businesses where administrative simplicity is prioritised over liability protection. The absence of a minimum capital requirement reduces the cost of entry, but unlimited personal liability remains a significant structural drawback for any business carrying financial or operational risk.

This structure is best suited for Bahraini or GCC national individuals operating low-risk, small-scale businesses who do not require a separate legal entity or external investors.

How to Choose the Right Entity Type in Bahrain

Selecting the wrong structure from the outset creates legal and financial consequences that can be difficult to unwind. Knowing how to choose a company structure in Bahrain requires evaluating your business model against the specific constraints and permissions each entity carries.

Why Your Entity Choice Matters

The structure you register determines your legal exposure, tax position, and operational permissions — choosing incorrectly has concrete outcomes:

- Registering a structure without the necessary commercial registration for local trading puts the business in breach of the Commercial Companies Law (Legislative Decree No. 21 of 2001), which can result in regulatory action or deregistration.

- Selecting a form that lacks a tax residency certificate — such as certain foreign branch arrangements — prevents your business from accessing Bahrain's bilateral tax treaties, blocking withholding tax reductions in counterpart jurisdictions.

- Forming a WLL when the intended purpose is asset holding or succession planning locks shareholders into annual general meeting obligations and equity transfer procedures that do not apply to trust or foundation arrangements.

- Choosing a structure that mandates audited financial statements for a single-person consultancy adds recurring compliance costs that an SPC operating under simplified reporting thresholds would not incur.

Key Factors to Consider

- Business Activity: Active trading, regulated operations (banking, insurance, capital markets), and passive asset holding each require a structurally distinct entity type under Bahraini law.

- Ownership Configuration: A sole operator points toward an SPC, while multi-party ventures with capital participation agreements are better served by a WLL or BSC.

- Local vs. Cross-Border Operations: Entities intended to transact with Bahraini residents must hold a valid commercial registration; purely offshore activity structures differ in their licensing pathway.

- Tax Treaty Access: If claiming withholding tax relief in a treaty partner country matters to your structure, confirm the entity type qualifies as a resident person under the relevant agreement.

- Regulatory Licensing: Certain activities require Central Bank of Bahrain or sector-specific authority approval, and the permitted entity types for those licenses are prescribed by regulation.

- Exit and Conversion: Not all entity types permit redomiciliation or conversion without dissolution; confirm the applicable procedure under the Companies Law before committing to a structure.

Corporate Compliance Services in Bahrain

Maintain good standing with Bahrain's regulatory requirements, from annual filings to statutory reporting obligations.

Conclusion

Incorporating a business in Bahrain requires matching the legal structure to your operational model, ownership constraints, and commercial objectives. The WLL remains the most widely registered entity, suited to small and mid-sized ventures where shareholders seek liability protection without the capital demands of a public structure. The BSC applies where public fundraising or large-scale institutional investment is required. For solo operators, the SPC provides a single-owner framework with limited liability. Foreign firms testing the market without generating local revenue typically establish a representative office, while those executing contracts directly opt for a branch. General and limited partnerships serve businesses built around professional or personal liability arrangements.

Bahrain's regulatory trajectory points toward continued alignment with international standards, reflected in its expanding tax treaty network and FATF compliance measures. Registration is administered through the Ministry of Industry and Commerce's Sijilaat portal, which has reduced processing timelines in recent years. Expanship's team works directly within this framework to structure and register entities across all permitted types.

How Expanship Can Assist You

Expanship's Bahrain company formation services cover the full registration process, from selecting between a WLL, BSC, SPC, or branch structure to satisfying the requirements of the Ministry of Industry and Commerce (MOIC) and the Bahrain Investors Center. Your business structure determines your foreign ownership rights, capital requirements, and ongoing filing obligations — all of which affect how your entity is registered and maintained.

From initial documentation through to post-incorporation compliance, our corporate services in Bahrain cover every operational stage:

- Preparation and legalization of incorporation documents

- Registered agent and registered office provision

- Government filing and liaison with the MOIC

- CR (Commercial Registration) renewal and compliance management

- Banking introduction assistance for corporate account opening

Get in touch with Expanship Bahrain to discuss your specific structure and requirements.

Frequently Asked Questions (FAQ)

The With Limited Liability Company (WLL) is the most frequently registered entity. Its combination of limited liability protection, relatively low capital requirements, and flexibility in ownership structure makes it the default choice for small and medium-sized businesses operating locally.

A WLL is suited to closely held businesses with a limited number of partners, whereas a BSC is designed for larger operations and is the only structure permitted to list shares on the Bahrain Bourse. BSCs carry heavier compliance obligations, including mandatory audits, and public disclosure requirements are more extensive. Both structures are subject to Bahrain's standard corporate tax framework, though neither faces corporate income tax at the national level under current law.

The Single Person Company (SPC) offers a concentrated ownership structure where a sole individual holds all shares, limiting the number of parties whose information appears in filings. Nominee arrangements are not a standard feature of Bahraini corporate law, so beneficial ownership disclosure to the Ministry of Industry and Commerce (MOIC) is required.

Not all structures permit sole formation. The SPC is specifically designed for individual ownership by one natural or legal person. General Partnerships and Limited Partnerships require a minimum of two partners, and a WLL requires between two and fifty shareholders under the Commercial Companies Law.

Foreign investors can register a WLL, BSC, SPC, or Branch Office, subject to sector-specific foreign ownership rules administered by the MOIC. Certain sectors require a local partner or impose ownership caps, while activities within the Bahrain International Investment Park or designated free zones may permit full foreign ownership without a local partner requirement.

Conversion between entity types is permitted under Bahraini company law, subject to MOIC approval and compliance with the applicable minimum capital and shareholder requirements of the target structure. A WLL, for example, can be converted to a BSC where the business grows to a scale that warrants public shareholding. The conversion process requires updated constitutional documents and re-registration.

The WLL, BSC, SPC, and both forms of Branch registration are treated as distinct legal persons. General Partnerships, by contrast, do not provide the same liability separation, and partners remain personally liable for the firm's obligations, which is a material distinction for risk allocation.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.