Key Takeaways

- Bulgaria's Commercial Register, maintained by the Registration Agency under the Ministry of Justice, requires all commercial entities to complete registration before conducting any business operations.

- The OOD is Bulgaria's most commonly registered entity type, favored for its low capital threshold and straightforward management structure, while the EOOD serves the same legal framework for single founders.

- Foreign entities can establish a presence in Bulgaria through either a Branch Office or a Representative Office, neither of which constitutes a separate legal person under Bulgarian law.

- Among EU member states, Bulgaria operates one of the lowest flat corporate tax rates, making it a distinctive low-tax jurisdiction within the bloc for businesses registered under the Commercial Act.

Introduction to Entity Types in Bulgaria

Bulgaria sits in southeastern Europe, bordered by Romania, Serbia, North Macedonia, Greece, and Turkey, with a Black Sea coastline to the east. It is an independent republic and a member of the European Union, which means company formation and ongoing compliance are governed within an EU regulatory framework.

Registration of legal entities falls under the jurisdiction of the Bulgarian Commercial Register and Register of Non-Profit Legal Entities, maintained by the Registration Agency under the Ministry of Justice. All commercial entities are required to register here before conducting business.

From a tax perspective, Bulgaria operates one of the lowest flat corporate tax rates in the EU, making it a notable low-tax jurisdiction within the bloc.

The types of business entities in Bulgaria available to both domestic and foreign investors include: the Joint Stock Company (AD), the Limited Liability Company (OOD), the Single-Member Limited Liability Company (EOOD), the General Partnership (SD), the Limited Partnership (KD), the Limited Partnership with Shares (KDA), the Branch Office, the Representative Office, and the Sole Trader (ET).

Each structure carries distinct liability rules, capital requirements, and governance obligations. This article examines each one in detail to help you determine which fits your operational and ownership requirements.

An Overview of Business Structures in Bulgaria

Bulgarian company law recognises several distinct entity types, each governed primarily by the Commerce Act (Targovski Zakon), first enacted in 1991 and amended numerous times since. The Registration Agency (Agentsiya po Vpisvaniyata), operating under the Ministry of Justice, maintains the Commercial Register through which all commercial entities are registered. Each structure carries different rules on liability, governance, and permitted activity.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Tax Treatment | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| AD | Joint Stock Company | Limited to shareholding | Corporate tax applies | Permitted | 1 shareholder | Registration Agency | Commerce Act |

| OOD | Limited Liability Company | Limited to contribution | Corporate tax applies | Permitted | 2 members | Registration Agency | Commerce Act |

| EOOD | Single-Member LLC | Limited to contribution | Corporate tax applies | Permitted | 1 member | Registration Agency | Commerce Act |

| SD | General Partnership | Unlimited, joint | Corporate tax applies | Permitted | 2 partners | Registration Agency | Commerce Act |

| KD | Limited Partnership | Mixed liability | Corporate tax applies | Permitted | 2 partners | Registration Agency | Commerce Act |

| KDA | Limited Partnership with Shares | Mixed liability | Corporate tax applies | Permitted | 2 partners | Registration Agency | Commerce Act |

| Branch Office | Non-legal-entity branch | Parent bears liability | Tax on local profit | Permitted | 1 parent company | Registration Agency | Commerce Act |

| Representative Office | Non-legal-entity presence | Parent bears liability | Not taxed on trade | No commercial activity | 1 parent company | Bulgarian Chamber of Commerce | Commerce Act |

| ET | Sole Trader | Unlimited, personal | Income tax applies | Permitted | 1 individual | Registration Agency | Commerce Act |

Each of these structures is examined in full in the sections below.

Joint Stock Company (Aktsionerno Druzhestvo – AD)

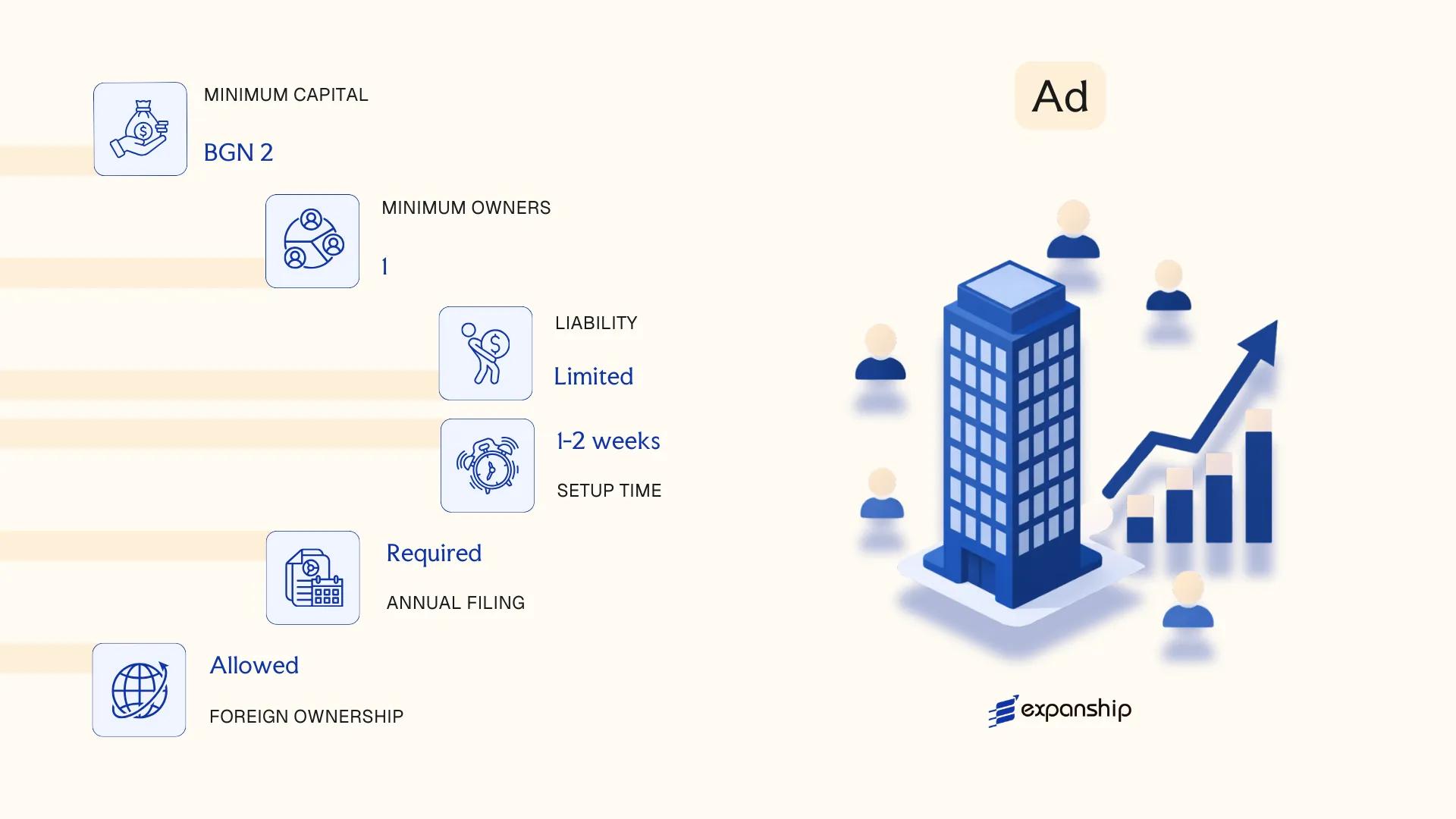

Governed by the Commerce Act of 1991 (Targovski Zakon), the joint stock company Bulgaria AD registration process establishes a capital-based entity with full legal personality, separate from its shareholders. Liability is limited to each shareholder's subscribed capital contribution.

Structured for larger commercial operations or entities intending to raise public or private capital, the Aktsionerno Druzhestvo issues transferable shares and may, under certain conditions, list on the Bulgarian Stock Exchange (BSE).

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Aktsionerno Druzhestvo (AD) | Separate legal entity; shareholders not liable for company debts |

| Members | Shareholders; Board of Directors or Supervisory Board + Management Board | Minimum 1 shareholder (no maximum); one-tier or two-tier board structure available |

| Capital | BGN 50,000 minimum (approx. EUR 25,000) | At least 25% of each share's nominal value must be paid upon registration; remainder within 2 years |

| Shares | Registered or bearer shares permitted | Bearer shares subject to disclosure requirements under AMLA regulations |

| Local Presence | Registered office address in Bulgaria required | No mandatory resident director, but a local address for official correspondence is obligatory |

| Privacy | Shareholders disclosed in the Commercial Register | Beneficial ownership registered with the Registry Agency under anti-money laundering obligations |

Focus Points

- Taxation: Corporate income tax at 10% flat rate; standard VAT rate of 20% with registration threshold of BGN 100,000; dividend withholding tax at 5% (reduced rates available under applicable double tax treaties); no stamp duty on share transfers.

- Annual Compliance: Mandatory annual financial statements audited by a registered auditor; filing with the Registry Agency; general meeting of shareholders required annually.

- Economic Substance: No formal substance test under Bulgarian law, though commercial reality and tax residency rules apply for treaty access purposes.

- Treaty Access: Bulgaria has over 60 active double tax treaties; AD entities qualify as residents for treaty purposes when management and control is exercised locally.

- Conversion: An AD may be converted into an OOD or other commercial entity through a statutory transformation procedure under the Commerce Act.

Sub-Types

Publicly Traded AD (Public AD)

A Public AD has made a public offering of shares or has more than 10,000 shareholders, bringing it under the supervision of the Financial Supervision Commission (FSC) and the requirements of the Public Offering of Securities Act. Ongoing disclosure, prospectus, and reporting obligations apply that do not affect a standard private AD.

Suited to institutional investors, joint ventures, and businesses anticipating equity financing, the AD offers structural flexibility through its dual-board option. The primary drawback is the relatively high minimum capital requirement and mandatory audit obligation, which increases administrative overhead compared to simpler Bulgarian entity forms.

The AD is most appropriate for larger businesses, investment holding structures, or entities planning to access capital markets or institutional investors.

Company Incorporation in Bulgaria

Incorporate a Joint Stock Company or other business entity in Bulgaria with end-to-end support from Expanship.

Limited Liability Company (Druzhestvo s Ogranichena Otgovornost – OOD)

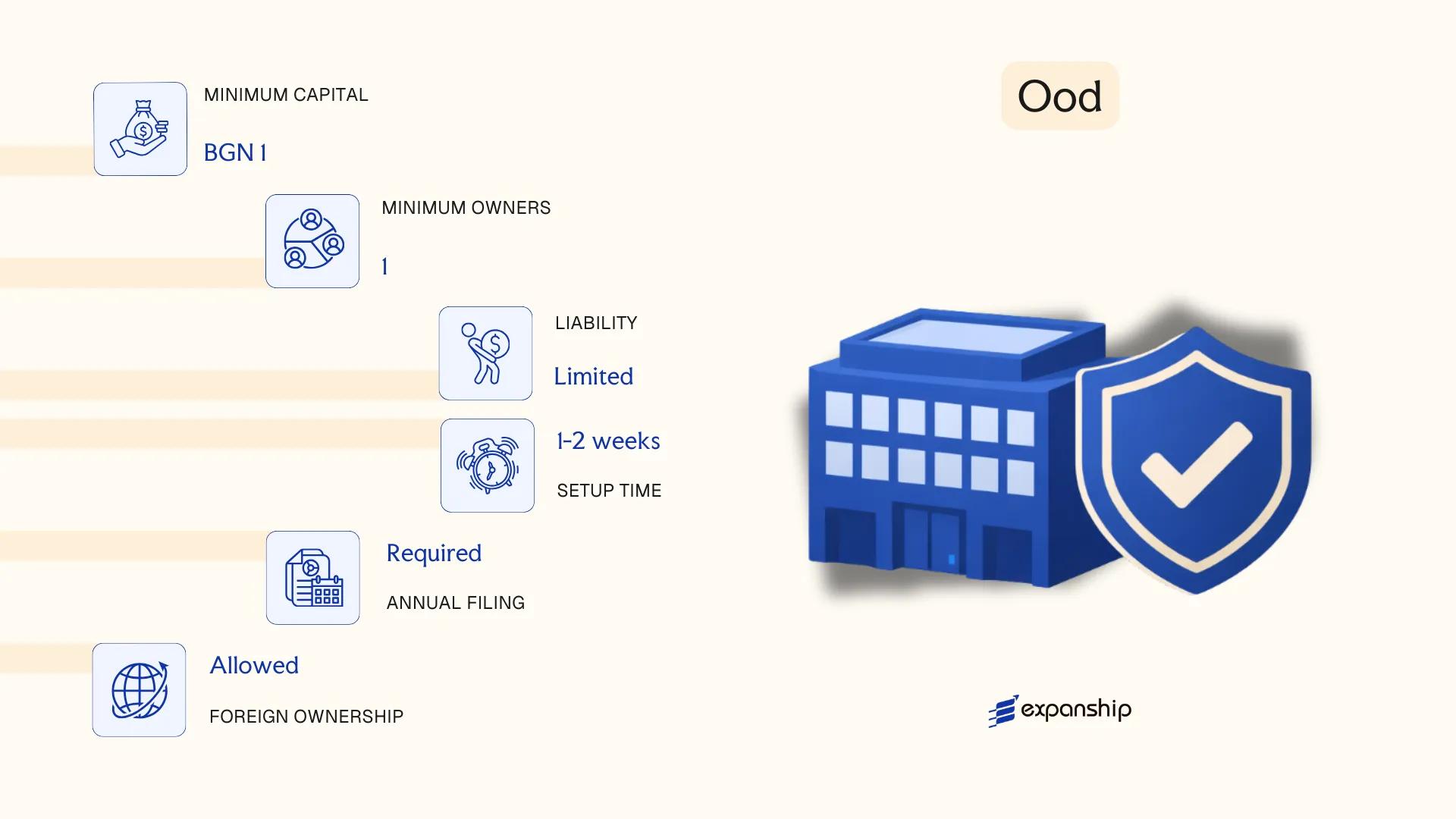

The limited liability company Bulgaria OOD is governed by the Commerce Act of 1991 (Targovski Zakon), which establishes it as a distinct legal entity separate from its members. Liability is confined to each member's capital contribution, meaning personal assets remain protected from business obligations.

Structurally, the OOD sits between a sole trader and a joint stock company — it carries corporate legal personality while permitting a relatively simple internal governance framework. Druzhestvo s Ogranichena Otgovornost registration is handled through the Bulgarian Commercial Register (Targovski Registar), maintained by the Registry Agency.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Company (OOD) | Separate legal personality; not publicly traded |

| Members | 2–50 members (individuals or legal entities) | Single-member variant is the EOOD; no upper limit on nationalities |

| Internal Roles | Manager (Upravitel); General Meeting of Members | Manager need not be a member; foreign nationals permitted |

| Registered Office | Physical address required in Bulgaria | Must be maintained throughout the company's existence |

| Share Capital | Minimum BGN 2 (approx. EUR 1); no maximum | Capital divided into shares (not freely transferable like AD shares) |

| Privacy | Member names filed in the Commercial Register | Register is publicly accessible |

Focus Points

- Taxation: Subject to 10% corporate income tax; standard VAT rate of 20% applies once registration threshold is met; withholding tax of 5% applies to dividends distributed to non-residents; no stamp duty on share transfers.

- Annual Compliance: Annual financial statements must be filed with the Commercial Register; audit obligation applies when statutory thresholds on revenue, assets, or headcount are exceeded.

- Economic Substance: No formal substance requirements under Bulgarian law, but tax residency determinations follow effective management and control principles.

- Treaty Access: Bulgaria's tax treaty network covers 70+ jurisdictions, making the OOD eligible for reduced withholding rates where applicable.

- Conversion: An OOD may be converted into an AD through a statutory transformation procedure under the Commerce Act.

Closing

The OOD suits trading operations, holding structures, and service-based businesses where controlled ownership and administrative simplicity are priorities. Its low capital threshold supports entry-level incorporation, though share transfer restrictions can limit investor flexibility compared to a share-based structure.

Small to mid-sized businesses, foreign investors entering the Bulgarian market through a locally incorporated entity, and holding structures requiring limited personal liability without public share issuance.

Single-Member Limited Liability Company (Edinolichno OOD – EOOD)

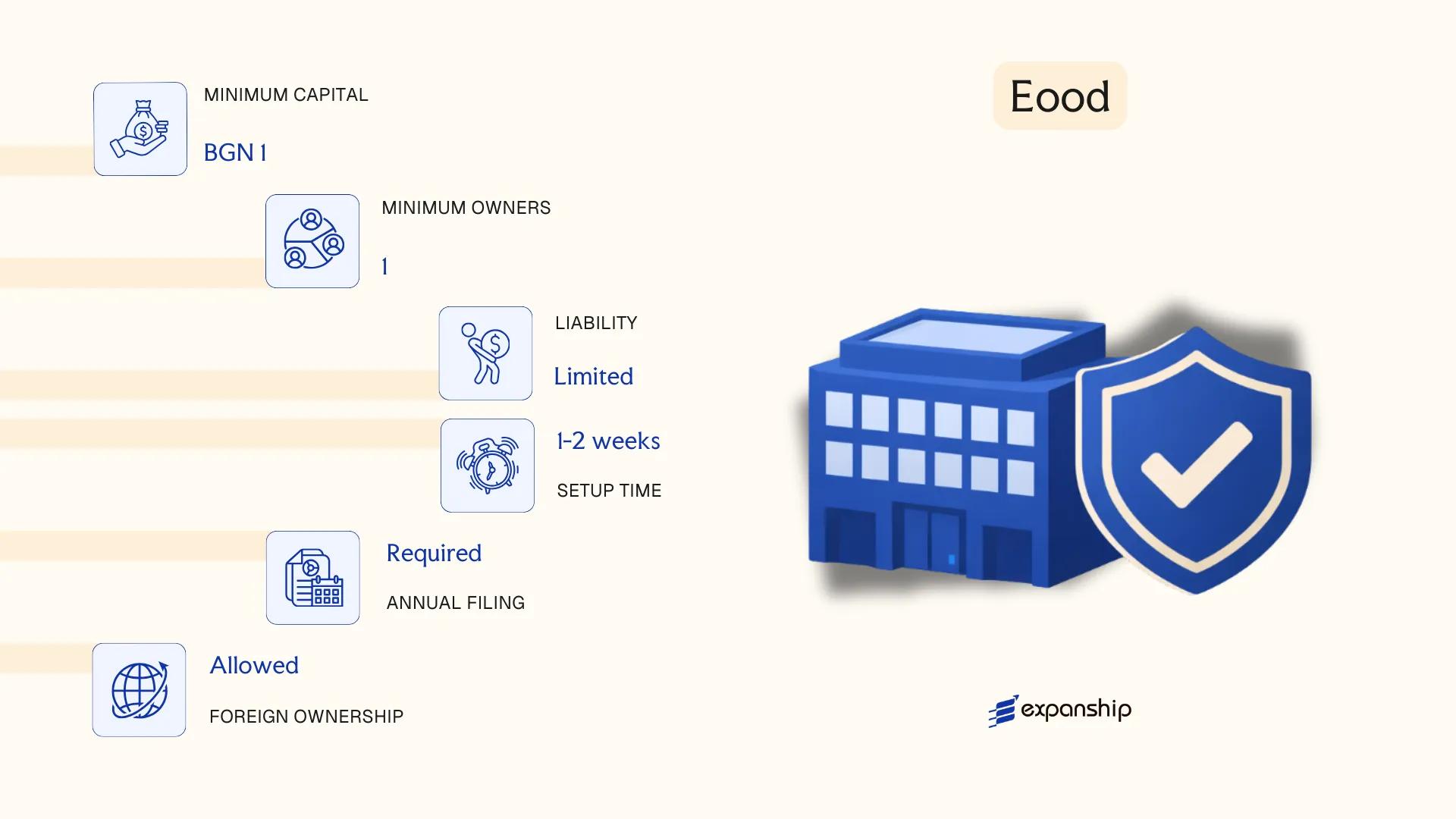

The single member LLC Bulgaria EOOD structure is governed by the Commerce Act of 1991 (Targovski Zakon), the same legislation that regulates the standard OOD. Structurally, the EOOD is a variant of the OOD in which a single individual or legal entity holds 100% of the capital.

As a separate legal person, it shields its sole owner from personal liability beyond the amount of their registered capital contribution. This hybrid character — combining the operational simplicity of a sole proprietorship with the liability protection of a limited liability entity — makes it a widely used form among small businesses and wholly-owned subsidiaries.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Company (Single-Member) | Registered under the Commerce Act 1991 |

| Members | 1 sole owner (individual or legal entity) | Owner acts as both shareholder and, typically, manager |

| Management | Manager (Upravitel) | Can be the owner or an appointed third party |

| Local Presence | Registered office address in Bulgaria required | No mandatory local resident director |

| Share Capital | Minimum BGN 2 (approx. EUR 1) | Must be fully paid up before registration |

| Privacy | Ownership details filed with the Commercial Register | Beneficial ownership also disclosed to the BULSTAT Register |

Focus Points

- Taxation: Subject to 10% corporate income tax; VAT registration is mandatory once annual turnover exceeds BGN 100,000; dividends distributed to non-resident owners are subject to 5% withholding tax under domestic law, reducible under applicable tax treaties.

- Annual Compliance: Annual financial statements must be filed with the Bulgarian Commercial Register; dormant companies still carry reporting obligations.

- Conversion: An EOOD can be converted to a standard OOD upon admitting additional shareholders, without dissolving the entity.

- Treaty Access: As a Bulgarian-resident legal entity, the EOOD can access Bulgaria's network of double taxation treaties, provided substance requirements are met.

- Restrictions: A single owner cannot simultaneously be the sole owner of another EOOD, under Article 156(2) of the Commerce Act.

Closing

The EOOD is suited to trading operations, holding structures, and wholly-owned subsidiaries where a single shareholder requires liability separation without the administrative overhead of a joint-stock entity. Its principal limitation is the restriction on sole ownership across multiple EOODs simultaneously, which can constrain certain multi-entity structuring approaches.

Freelancers, solo founders, and foreign investors establishing a wholly-owned subsidiary who require limited liability without multiple shareholders.

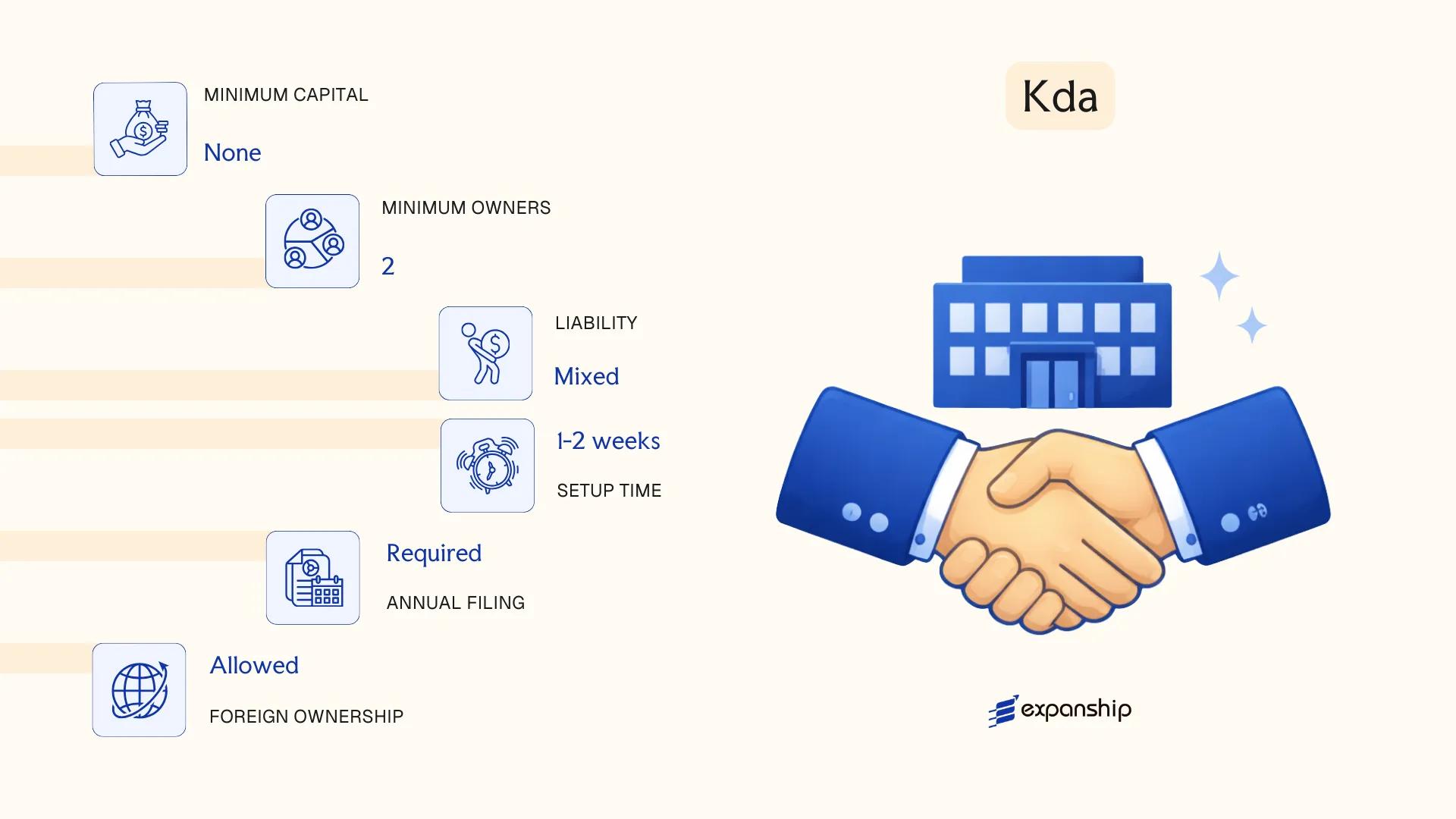

Partnerships in Bulgaria [General Partnership (Sabiratelno Druzhestvo – SD), Limited Partnership (Komanditno Druzhestvo – KD), Limited Partnership with Shares (Komanditno Druzhestvo s Aktsii – KDA)]

The three partnership types in Bulgaria — SD, KD, and KDA — are governed by the Commerce Act (Targovski Zakon) of 1991. All three possess separate legal personality upon registration with the Commercial Register at the Registry Agency, which distinguishes them from simple civil partnerships under the Obligations and Contracts Act.

Liability structures differ across these forms. In an SD, all partners bear unlimited joint and several liability for the firm's obligations. The KD introduces a two-tier membership model, separating unlimited general partners from limited partners whose exposure is capped at their capital contribution. The KDA extends this further by issuing shares to limited participants, combining partnership governance with share capital mechanics.

Key Characteristics

| Requirement | SD | KD | KDA |

|---|---|---|---|

| Legal Form | General Partnership | Limited Partnership | Limited Partnership with Shares |

| Partners | Unlimited partners only (min. 2) | Min. 1 general + 1 limited partner | Min. 1 general partner + shareholders for share capital portion |

| Liability | All partners: unlimited, joint and several | General partners: unlimited; Limited partners: capped at contribution | General partners: unlimited; Shareholders: limited to share value |

| Minimum Capital | None prescribed | None prescribed | Minimum share capital required (equivalent to AD requirements under Commerce Act) |

| Management | All general partners, unless restricted by articles | General partners only; limited partners excluded from management | General partners manage; shareholders participate via general meeting |

| Registered Office | Required in Bulgaria | Required in Bulgaria | Required in Bulgaria |

Focus Points

- Taxation: Partnerships are subject to 10% corporate income tax on profits; VAT registration is mandatory above the BGN 166,000 threshold; distributions may attract 5% withholding tax on dividends paid to non-resident partners.

- Annual compliance: All three forms must file annual financial statements with the Commercial Register; SD and KD have simplified accounting requirements relative to capital companies.

- Treaty access: Access to Bulgaria's double tax treaty network depends on the entity being treated as a tax resident; partnership classification can vary under foreign jurisdictions' domestic rules.

- Conversion: A KD may be converted into a KDA or an OOD under the Commerce Act transformation procedures, subject to creditor notification requirements.

- Restrictions: Limited partners in a KD who participate in management lose their limited liability protection under the Commerce Act.

Sub-Types

General Partnership (Sabiratelno Druzhestvo – SD)

The SD is the structurally simplest partnership form, with no capital minimum and full unlimited liability for every partner. It is typically used by small professional firms or family businesses where all participants are actively involved in operations.

Limited Partnership (Komanditno Druzhestvo – KD)

The KD separates passive investors (limited partners) from active managers (general partners), making it suitable for arrangements where capital contributors prefer defined exposure without operational responsibility.

Limited Partnership with Shares (Komanditno Druzhestvo s Aktsii – KDA)

The KDA is the least common of the three. Its share capital component brings it structurally closer to an AD, and it is occasionally used for investment vehicles where transferability of limited participation interests is commercially important.

Partnership structures suit professional services, family-owned trading businesses, and investment arrangements requiring a clear separation between active managers and passive capital contributors. The unlimited liability exposure of general partners is a material constraint that limits these forms in higher-risk commercial contexts.

Partnership forms in Bulgaria are best suited to closely-held businesses where all general partners are known individuals with direct operational involvement and a mutual acceptance of personal liability.

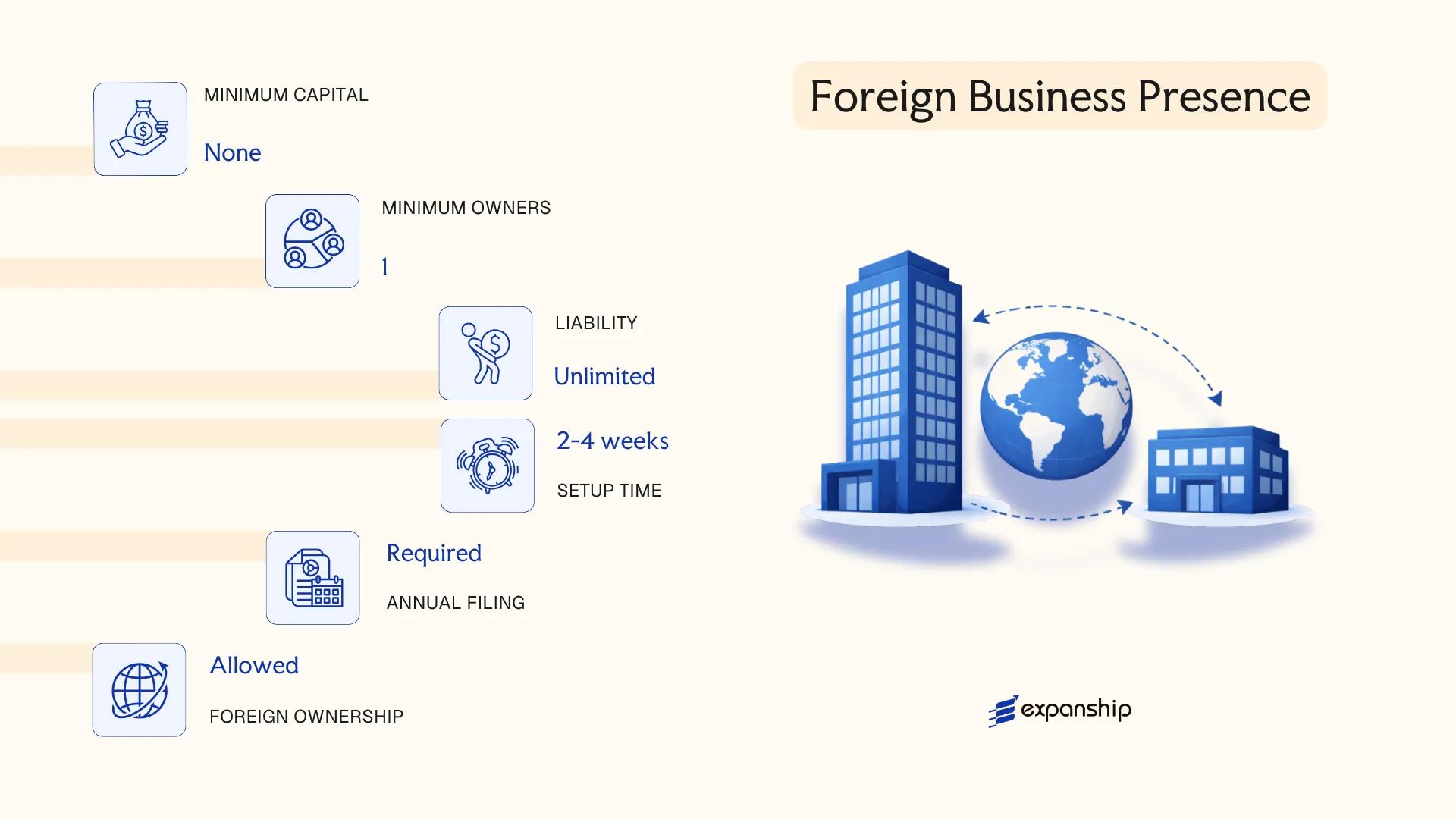

Foreign Business Presence in Bulgaria [Branch Office, Representative Office]

Establishing a foreign company branch office Bulgaria is governed primarily by the Commerce Act (Targovski Zakon), first enacted in 1991 and subsequently amended. Neither a branch office nor a representative office constitutes a separate legal entity — both are extensions of the parent company, which retains full liability for their activities. This distinction has direct consequences for contracting, taxation, and regulatory exposure.

Registration of both structures is handled through the Bulgarian Commercial Register (Targovski Registar), administered by the Registry Agency. A branch may conduct commercial activity directly, whereas a representative office is restricted to non-revenue-generating functions such as market research, promotional activities, and liaison work.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Personality | None — extension of parent | None — extension of parent |

| Commercial Activity | Permitted | Not permitted |

| Registration Body | Commercial Register (Registry Agency) | Bulgarian Chamber of Commerce and Industry (BCCI) |

| Local Representative | Mandatory — an authorised manager must be appointed | Mandatory — an authorised representative required |

| Registered Address | Required in Bulgaria | Required in Bulgaria |

| Capital Requirement | None prescribed | None prescribed |

| Liability | Parent company bears full liability | Parent company bears full liability |

Focus Points

- Taxation: Branch profits are subject to 10% corporate income tax on Bulgarian-sourced income; VAT registration is required if taxable turnover exceeds BGN 100,000; withholding tax may apply to profit remittances depending on the parent's home jurisdiction and applicable double tax treaties.

- Treaty Access: Access to Bulgaria's tax treaty network depends on the parent entity's tax residency; the branch itself does not qualify as a resident taxpayer.

- Annual Compliance: Branches must file annual financial statements with the Commercial Register; representative offices registered with the BCCI have separate annual re-registration requirements.

- Restrictions: A representative office cannot sign commercial contracts, invoice clients, or generate revenue — violations risk reclassification by the National Revenue Agency (NRA).

- Conversion: A branch can be converted into a locally incorporated entity, but this requires a new registration process rather than a statutory conversion procedure.

Closing

A branch office suits foreign firms testing the Bulgarian market or executing specific contracts without committing to full local incorporation, though the absence of liability separation between the branch and the parent remains a structural exposure. The representative office is appropriate only for preparatory or auxiliary functions.

A branch office is best suited for established foreign companies that need operational presence without incorporating locally; a representative office fits firms in an early market-entry or research phase only.

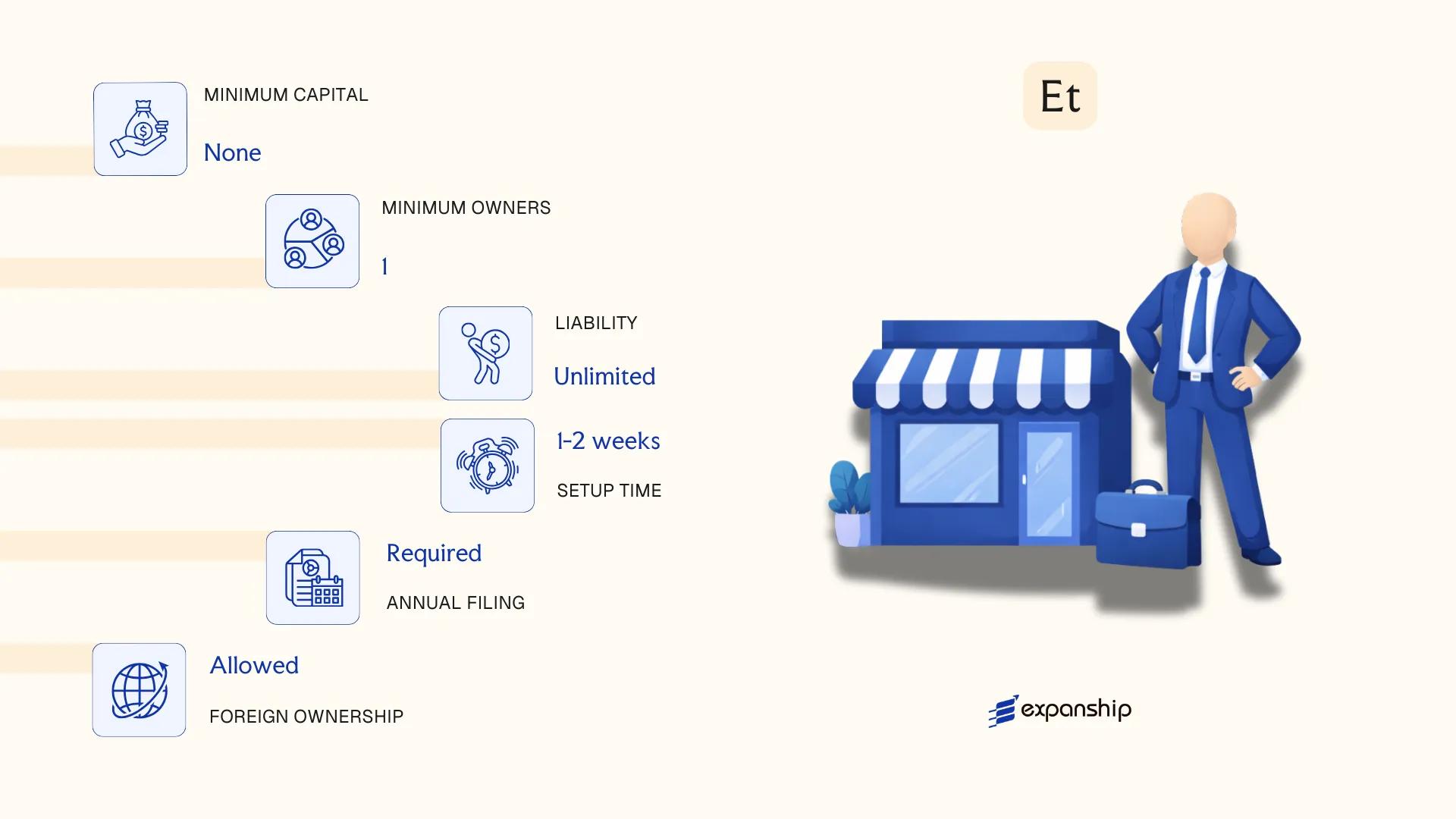

Sole Trader (Ednolichen Targovets – ET)

Sole trader registration Bulgaria ET is governed by the Commerce Act (Targovski Zakon) of 1991, specifically Part One, Chapter Two. Unlike the OOD or AD, the ET is not a separate legal entity — the individual and the business are legally the same person, meaning personal assets are fully exposed to business liabilities.

Registration is handled through the Commercial Register (Targovki registar) maintained by the Registry Agency. Any Bulgarian national or EU/EEA citizen with permanent residency may register as an ET; non-EEA nationals face restrictions under current rules.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole Trader (Ednolichen Targovets) | Not a separate legal entity; proprietor and business are legally identical |

| Proprietor | Single individual only | No minimum capital; no co-ownership permitted |

| Liability | Unlimited personal liability | All personal assets are at risk for business debts |

| Local Presence | Registered address in Bulgaria required | Must be a physical address; no virtual-only arrangements under the Commerce Act |

| Capital | No minimum capital requirement | No share structure exists |

| Privacy | Name of proprietor appears in the Commercial Register | Publicly searchable via the Registry Agency portal |

Focus Points

- Taxation: Subject to a flat 15% annual personal income tax on net profit (after a 60% standard expense deduction); VAT registration mandatory upon reaching the BGN 100,000 turnover threshold; no corporate tax applies.

- Social Security: Proprietors must make mandatory social and health insurance contributions regardless of profitability.

- Annual Compliance: Annual financial statements must be filed with the Registry Agency; dormant ETs with no activity may be eligible for simplified reporting.

- Conversion: An ET can be converted into an OOD or EOOD under the Commerce Act, but the process requires formal transformation proceedings and does not automatically transfer liabilities.

- Restrictions: Cannot be used for certain regulated activities (banking, insurance) that require a corporate structure with defined capital.

Closing

The ET suits individual traders, freelancers, and small-scale operators who need a low-cost, quickly registered structure for domestic commercial activity. The absence of minimum capital and simplified setup are practical advantages, but unlimited personal liability makes it unsuitable for any business carrying significant financial or legal risk.

Best suited for Bulgarian residents or EU/EEA nationals running a small, low-risk sole operation who want minimal administrative overhead and do not require liability separation.

How to Choose the Right Entity Type in Bulgaria

Knowing how to choose a company type in Bulgaria before you register prevents structural problems that are far more costly to correct after the fact.

Why Your Entity Choice Matters

The structure you select at registration has binding legal and financial consequences that persist for the life of the entity.

- Registering as a Branch Office when you intend to operate as an independent commercial entity means the parent company retains full liability for the branch's obligations under the Bulgarian Commerce Act — there is no liability shield.

- Choosing an OOD or EOOD when your activity falls under a licensed sector (banking, insurance, collective investment schemes) without meeting the minimum capital and regulatory requirements of the Financial Supervision Commission results in operating without a valid licence, exposing the entity to forced closure.

- Selecting a Representative Office, which cannot lawfully generate revenue, and then conducting commercial transactions through it constitutes a breach of its registered purpose and can trigger deregistration by the Registry Agency.

- Forming a Joint Stock Company (AD) for a single-owner consultancy imposes mandatory audited financial statements and a supervisory board structure, adding recurring compliance costs that a sole EOOD does not carry.

Key Factors to Consider

Before settling on a Bulgaria entity type, review each of the following against your specific situation:

- Business Activity: Active trading, passive asset holding, and regulated financial activity each point to structurally different entities under the Commerce Act.

- Ownership and Management: Single-person ownership suits an EOOD, while multi-party ventures with investor protections require an OOD or AD with a formal governance structure.

- Tax Objectives: If treaty access matters — for instance, to claim reduced withholding tax in counterpart states — you need a fully taxable resident entity, not a tax-exempt structure.

- Substance Capacity: If you cannot realistically maintain personnel, a registered address with operational activity, and management decisions inside the jurisdiction, the chosen structure must reflect that limitation.

- Privacy Requirements: The Commercial Register in Bulgaria is public; directors and shareholders of capital companies are disclosed, so nominee arrangements must be assessed separately for compliance with beneficial ownership reporting rules.

- Exit Strategy: Not all entity types in Bulgaria support redomiciliation or conversion; an OOD can be converted to an AD, but a Representative Office cannot be converted — it must be closed and a new entity formed.

Corporate Compliance Services in Bulgaria

Ongoing compliance support for Bulgarian companies, including annual filings, beneficial ownership reporting, and regulatory obligations under the Commerce Act.

Conclusion

Selecting the right structure is the first substantive decision in any incorporating a business in Bulgaria guide, and that choice carries consequences for liability, governance, and long-term operational flexibility. The OOD remains the most registered entity type in the country, favored for its low capital threshold and straightforward management structure. The EOOD serves the same framework but suits single founders operating without partners. For larger ventures requiring share transferability and public capital access, the AD applies. Partnerships — the SD and KD — fit closely held arrangements where personal liability is acceptable. Branch offices and representative offices extend foreign entities into Bulgarian territory without creating a separate legal person, each serving distinct operational purposes. The ET remains specific to individual traders operating under personal liability. Registered under the Commercial Act and administered through the Commercial Register at the Registry Agency, each structure carries defined legal standing.

How Expanship Can Assist You

Expanship's corporate services Bulgaria clients rely on cover the full formation cycle, from choosing between an OOD, EOOD, or AD to registering with the Bulgarian Commercial Register at the Registry Agency. Each entity type carries distinct filing requirements, capital thresholds, and ongoing compliance obligations — your setup should reflect your operational structure, not default to convention.

From initial document preparation through to post-incorporation obligations, here is what Expanship manages on your behalf:

- Document preparation and notarization for Registry Agency submission

- Registered address and local agent provision

- Government filing and liaison with the Bulgarian Commercial Register

- Post-incorporation compliance management, including annual reporting

- VAT registration support with the National Revenue Agency

- Banking introduction assistance for corporate account opening

To discuss your Bulgaria business incorporation, reach out to our team directly through Expanship Bulgaria.

Frequently Asked Questions (FAQ)

The OOD (Druzhestvo s Ogranichena Otgovornost) is the most frequently incorporated structure in Bulgaria. Its combination of limited liability, a low minimum capital requirement of BGN 2, and a single-tier management structure makes it the default choice for small and medium-sized enterprises.

A Branch Office is not a separate legal entity — it remains an extension of the foreign parent and is taxed only on locally generated income. An OOD is fully incorporated under Bulgarian law, carries its own legal personality, and is subject to the full scope of corporate compliance obligations under the Commerce Act.

Among registered structures, the EOOD (Edinolichno OOD) involves only one member, whose identity is recorded in the Commercial Register maintained by the Registry Agency. Nominee shareholder arrangements are legally permissible in Bulgaria, though nominee director services are subject to beneficial ownership disclosure requirements under the Measures Against Money Laundering Act.

Not all structures permit sole formation. The EOOD is specifically designed for single-member ownership, while an OOD requires at least two members. General Partnerships (SD) and Limited Partnerships (KD) each require a minimum of two partners by statute.

Foreign nationals face no restrictions on ownership or directorship in an OOD, EOOD, or AD. Bulgaria imposes no residency requirement on shareholders or directors, which makes these structures accessible for non-resident entrepreneurs without a Bulgarian co-founder.

The Commerce Act permits transformation between entity types, including conversion of an OOD into an AD. The process requires a resolution of the existing members or shareholders, re-registration with the Registry Agency, and compliance with the capital requirements applicable to the target structure.

The OOD, EOOD, AD, and KDA each hold separate legal personality from their owners. A Branch Office and a General Partnership (SD) do not — the parent company and general partners, respectively, retain direct legal liability for obligations incurred.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.