Key Takeaways

- Belgium's 2019 Code of Companies and Associations (WVV/CSA) governs all entity types, with the Besloten Vennootschap (BV) emerging as the most commonly registered structure due to its flexible capital requirements and simplified governance.

- All legal entities must be registered with the Crossroads Bank for Enterprises (CBE) and published in the Belgisch Staatsblad / Moniteur belge before any commercial activity can commence.

- The Naamloze Vennootschap (NV) is distinguished from the BV by its suitability for public capital markets and complex shareholder arrangements, making it the preferred structure for larger enterprises.

- Branch offices and representative offices allow foreign companies to establish a presence in Belgium without incorporating a separate legal entity under Belgian law.

Introduction to Entity Types in Belgium

Belgium is a federal state in Western Europe, bordered by the Netherlands, Germany, Luxembourg, and France. As a founding member of the European Union with Brussels serving as the de facto EU capital, the country sits at the center of European regulatory and commercial activity — a factor that directly shapes how types of business entities in Belgium are structured and governed.

Company registration falls under the authority of the Crossroads Bank for Enterprises (CBE), operated by the Federal Public Service Economy. All legal entities must be registered with the CBE and published in the Belgian Official Gazette (Belgisch Staatsblad / Moniteur belge) before commencing commercial activity.

Belgium operates a standard corporate tax regime, with participation exemptions and an extensive treaty network that affects how resident entities are taxed on foreign income.

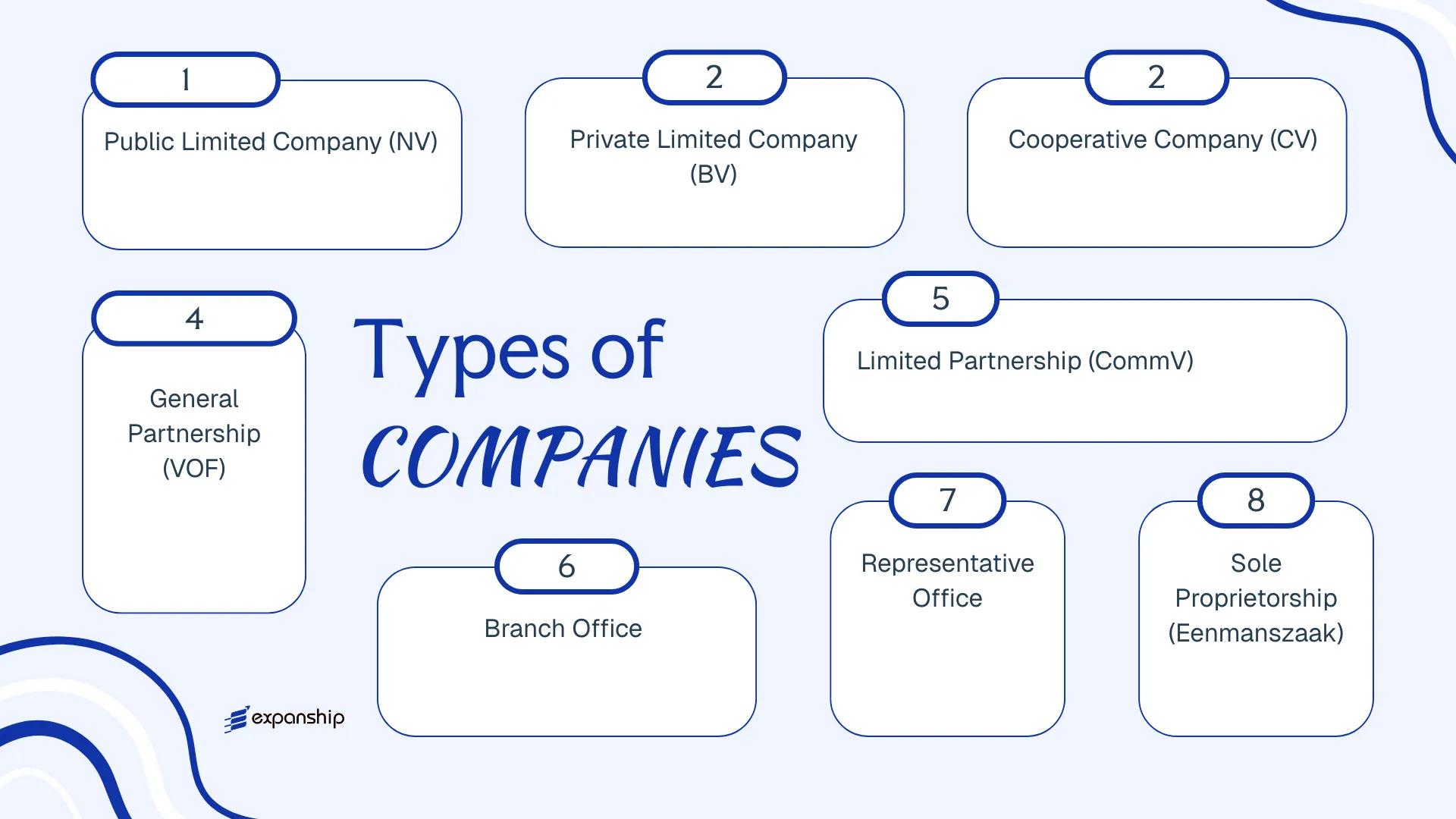

The following entity types are available to businesses operating in Belgium:

- Naamloze Vennootschap (NV)

- Besloten Vennootschap (BV)

- Coöperatieve Vennootschap (CV)

- Vennootschap onder Firma (VOF)

- Commanditaire Vennootschap (CommV)

- Branch Office

- Representative Office

- Eenmanszaak / Entreprise Individuelle

Each structure carries distinct liability, governance, and capital requirements under the Belgian Code of Companies and Associations (Wetboek van vennootschappen en verenigingen), which entered into force in 2019. This article examines each option in detail.

An Overview of Business Structures in Belgium

Belgian company law recognises several distinct entity types, each governed primarily by the Code of Companies and Associations (Wetboek van vennootschappen en verenigingen / Code des sociétés et des associations), which came into force on 1 May 2019. This legislation replaced the earlier Companies Code and consolidated the full Belgium business structures comparison framework under a single statute. Each form carries its own liability rules, capital requirements, and governance obligations.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Naamloze Vennootschap (NV) | Public limited company | Limited to capital | Corporate tax | Yes | 1 shareholder | Crossroads Bank for Enterprises (CBE) | CCA 2019 |

| Besloten Vennootschap (BV) | Private limited company | Limited to capital | Corporate tax | Yes | 1 shareholder | CBE | CCA 2019 |

| Coöperatieve Vennootschap (CV) | Cooperative company | Limited to capital | Corporate tax / exemptions possible | Yes | 3 shareholders | CBE | CCA 2019 |

| Vennootschap onder Firma (VOF) | General partnership | Unlimited, joint | Transparent / personal tax | Yes | 2 partners | CBE | CCA 2019 |

| Commanditaire Vennootschap (CommV) | Limited partnership | Mixed | Transparent / personal tax | Yes | 1 general + 1 limited | CBE | CCA 2019 |

| Branch Office | Foreign branch | Parent liability | Corporate tax on local profits | Yes | N/A | CBE | CCA 2019 |

| Representative Office | Non-trading presence | Parent liability | Generally non-taxable | No | N/A | CBE | N/A |

| Eenmanszaak | Sole proprietorship | Unlimited, personal | Personal income tax | Yes | 1 individual | CBE | N/A |

Each of these structures is examined in full in the sections below.

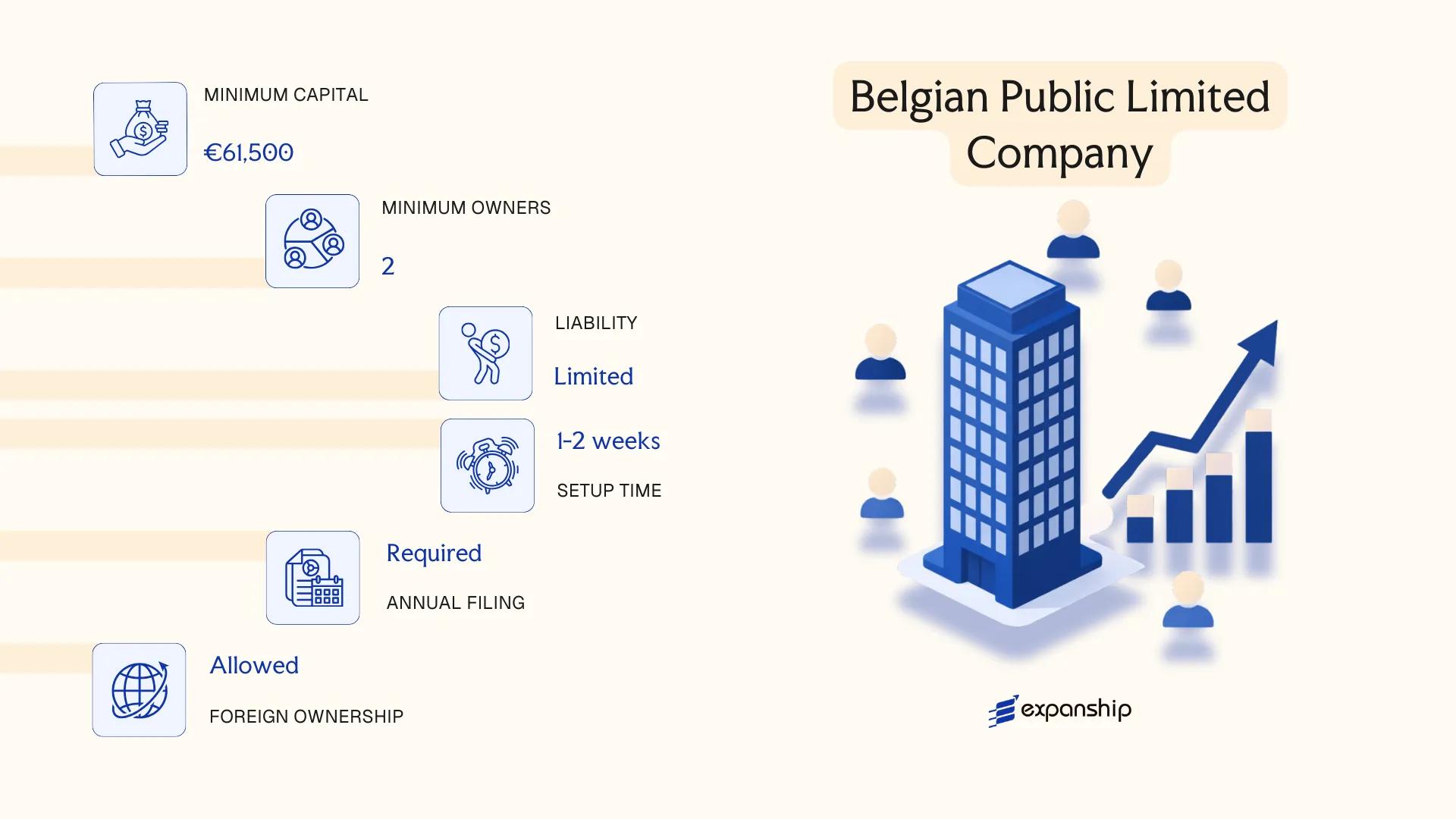

Naamloze Vennootschap (NV) — Belgian Public Limited Company

Governed by the Code des sociétés et des associations (CSA), enacted in 2019, the Naamloze Vennootschap (NV) is the primary vehicle for Naamloze Vennootschap NV Belgium formation at scale. It carries full separate legal personality, meaning the company itself bears rights and obligations distinct from its shareholders.

Shareholders' liability is limited to their capital contribution. The NV also functions as a hybrid structure in practice — it can be closely held or publicly listed, making it adaptable across ownership models without changing its fundamental legal form.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Naamloze Vennootschap (NV) | Société anonyme (SA) in French; registered via notarial deed at the Crossroads Bank for Enterprises (CBE) |

| Members | Shareholders (min. 1, no maximum) | Single-shareholder NV permitted; shareholders referred to as actionnaires in French documentation |

| Governance | Board of Directors or Sole Director | Minimum 1 director if single shareholder; otherwise minimum 3; a Supervisory Board is required for listed NVs under the dual-board model |

| Capital | EUR 61,500 minimum share capital | At least 25% of each share must be paid up at incorporation; fully paid up within 5 years |

| Local Presence | Registered office in Belgium | No mandatory resident director requirement, but a registered address is compulsory |

| Privacy | Shareholder register is not public | UBO register disclosure required under Belgian anti-money laundering legislation |

Focus Points

- Taxation: Subject to corporate income tax at 25% standard rate; reduced 20% rate applies on the first EUR 100,000 for qualifying SMEs; standard VAT registration required for trading activities; withholding tax of 30% applies to dividends, reducible under applicable tax treaties or the participation exemption regime.

- Annual Compliance: Annual accounts must be filed with the National Bank of Belgium (NBB); a statutory audit is mandatory once two of three size thresholds are exceeded.

- Treaty Access: Belgium maintains an extensive double tax treaty network; the NV qualifies as a resident entity for treaty purposes under standard residence tie-breaker rules.

- Economic Substance: No formal substance test is prescribed for domestic NVs, though transfer pricing rules apply to intra-group transactions with related parties.

- Conversion: An NV may be converted into a BV or CV by shareholder resolution, subject to notarial procedure and CBE re-registration.

Closing

The Belgian public limited company suits listed entities, large trading operations, joint ventures, and holding structures where capital markets access or institutional investment is anticipated. Its principal advantage is the ability to issue multiple share classes and bearer-equivalent instruments; its principal limitation is the EUR 61,500 minimum capital requirement, which places it above the threshold of most early-stage businesses.

The NV is most appropriate for businesses anticipating public listing, institutional shareholders, or cross-border investment structures requiring a capital-intensive, publicly recognised corporate form.

Company Incorporation in Belgium

Incorporate your NV or other Belgian entity with end-to-end support, from notarial deed preparation to CBE registration.

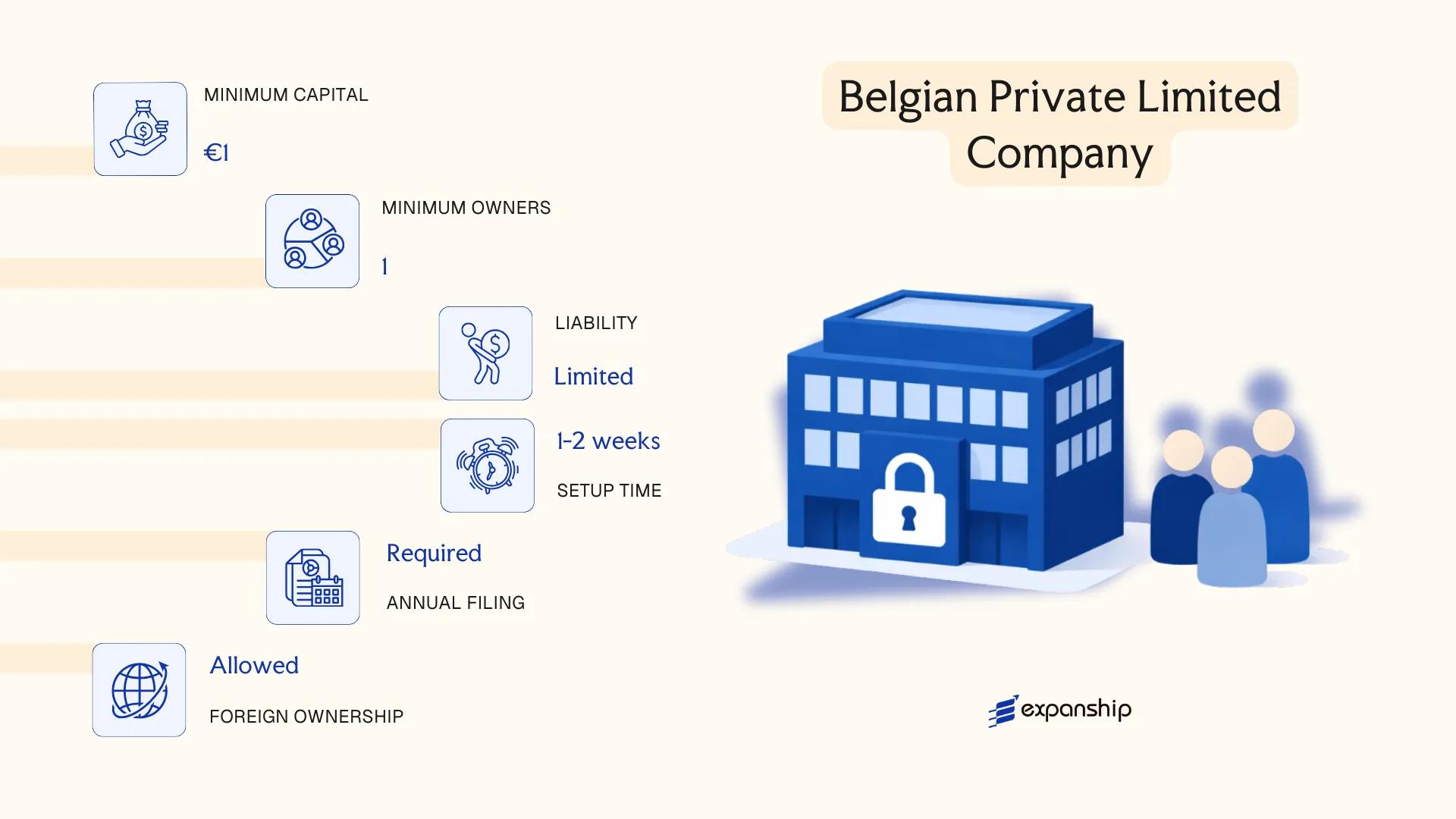

Besloten Vennootschap (BV) — Belgian Private Limited Company

Besloten Vennootschap BV Belgium registration is governed by the Companies and Associations Code (Wetboek van vennootschappen en verenigingen, WVV), which came into force on 1 May 2019. The reform fundamentally restructured this entity type, replacing the former BVBA and making the BV the default corporate form for private business activity in Belgium.

As a separate legal entity, the BV offers its shareholders full limited liability, capped at their subscribed contributions. Its hybrid character allows considerable flexibility in share transfer restrictions, voting arrangements, and profit distribution — all configurable through the articles of association.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Besloten Vennootschap (BV) | Private company with legal personality |

| Members | Shareholders: minimum 1, no maximum; Directors: minimum 1, no maximum | Single-member BV is permitted; no statutory cap on shareholders |

| Local Presence | Registered office in Belgium required | Must maintain a genuine Belgian address; virtual offices accepted in practice |

| Capital | No statutory minimum capital; adequate initial assets required | Founders must prepare a financial plan demonstrating sufficient funding |

| Share Transferability | Shares are restricted by default; transfer requires compliance with articles | Articles may loosen or tighten restrictions |

| Privacy | Shareholder register is internal; UBOs disclosed to the UBO Register | UBO Register is partially publicly accessible |

Focus Points

- Taxation: Subject to corporate income tax at 20% (reduced rate for qualifying SMEs on first €100,000 profit) or the standard 25% rate; standard VAT at 21% applies to taxable supplies; withholding tax of 30% on dividends, reducible under applicable tax treaties or the EU Parent-Subsidiary Directive.

- Annual Compliance: Annual accounts must be filed with the National Bank of Belgium (Nationale Bank van België); annual general meeting required; statutory auditor mandatory once two of three size thresholds are exceeded.

- Economic Substance: No formal substance regime, but the financial plan obligation at incorporation signals that genuine activity or adequate resourcing is expected.

- Treaty Access: Resident in Belgium for tax purposes and eligible for Belgium's extensive double tax treaty network (90+ treaties).

- Conversion: A BV may be converted into an NV or other recognised form through a statutory restructuring procedure under the WVV without dissolution.

Closing

The BV suits trading companies, SMEs, holding structures, and IP-holding vehicles where flexibility in governance and no minimum capital requirement are operationally useful. Its principal limitation is the financial plan obligation: an inadequate plan can expose founders to personal liability if the company becomes insolvent within three years of incorporation.

The BV is best suited for entrepreneurs, SMEs, and investors seeking a flexible, single-shareholder-capable structure without a mandatory minimum capital outlay.

Coöperatieve Vennootschap (CV) — Belgian Cooperative Company

Introduced under the Companies and Associations Code (Wetboek van vennootschappen en verenigingen, WVV) of 23 March 2019, the Coöperatieve Vennootschap CV Belgium setup is designed for enterprises built around a collective purpose rather than pure capital accumulation. The CV carries separate legal personality and offers limited liability to its members, while its structural flexibility sets it apart from conventional capital-based companies.

Unlike the NV or BV, the CV is explicitly reserved for entities pursuing a genuine cooperative objective — meaning the company must serve the economic or social needs of its members. This requirement is codified in the WVV and is assessed at incorporation.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Cooperative Company with legal personality | Separate legal entity; limited liability applies to members |

| Members | Minimum 3 founding members; no maximum | Members are referred to as "members" (leden), not shareholders |

| Governance | Board of directors or sole director | General assembly of members holds ultimate authority |

| Registered Office | Physical address in Belgium required | Cannot use a purely nominal address without substance |

| Share Capital | No statutory minimum | Capital is variable by design; shares are not freely transferable without consent |

| Privacy | Member register not publicly disclosed | Annual accounts filed with the National Bank of Belgium (NBB) are public |

Focus Points

- Taxation: Subject to standard corporate income tax at 25% (or 20% reduced rate for qualifying SMEs on the first €100,000); VAT obligations apply to commercial activities; dividend withholding tax at 30% applies, though the VVPRbis regime does not extend to CVs.

- Cooperative recognition: The CV may apply to the National Council for Cooperation (Nationale Raad voor de Coöperatie) for official recognition, which unlocks certain tax advantages including a deduction for distributed dividends to members.

- Annual compliance: Mandatory filing of annual accounts with the NBB; general assembly must be held at least once per year.

- Conversion: A CV can be converted to another legal form under the WVV, subject to member approval and notarial deed.

- Restrictions: The cooperative purpose must remain authentic; Belgian supervisory authorities can challenge structures that use the CV form without a genuine cooperative rationale.

Closing

The CV suits social enterprises, worker-owned businesses, and sector-specific cooperatives where member participation and shared purpose take precedence over investor returns. Its variable capital structure offers flexibility, though the mandatory cooperative purpose restricts its use as a general-purpose trading or holding vehicle.

The CV is most appropriate for businesses where members actively participate in the entity's activities and the structure genuinely serves collective economic or social objectives.

Partnerships in Belgium [Vennootschap onder Firma (VOF), Commanditaire Vennootschap (CommV)]

Belgian partnership law is governed by the Companies and Associations Code (Wetboek van vennootschappen en verenigingen, WVV), which entered into force on 1 May 2019. Both the Vennootschap onder Firma (VOF) and the Commanditaire Vennootschap (CommV) carry full legal personality under this code, meaning they can hold assets, enter contracts, and bear liabilities in their own name.

VOF CommV partnership Belgium formation procedures fall under the same WVV framework, though the two structures differ significantly in liability exposure. In a VOF, all partners bear unlimited joint and several liability for the firm's obligations. The CommV introduces a two-tier structure, separating general partners — who remain personally liable — from limited partners whose liability is capped at their contribution.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | VOF: General Partnership / CommV: Limited Partnership | Both have legal personality under WVV |

| Partners | VOF: minimum 2 general partners, no maximum / CommV: minimum 1 general + 1 limited partner | CommV limited partners may not manage the business |

| Capital | No statutory minimum; contributions in cash or kind | Capital amount agreed in the articles of association |

| Local Presence | Registered office required in Belgium | Address must appear in articles filed with the CBE |

| Registration | Filed with the Crossroads Bank for Enterprises (CBE) via a notarial or private deed | Published in the Belgian Official Gazette (Belgisch Staatsblad) |

| Privacy | Partner identities disclosed in public filings | Beneficial ownership registered with the UBO register |

Focus Points

- Taxation: Partnerships are generally taxed as pass-through entities by default; profits are attributed to partners and taxed at their applicable personal or corporate income tax rate, though a CommV may elect corporate income tax treatment; standard Belgian VAT (21%) applies to taxable supplies; withholding tax rules apply to any dividends distributed following a corporate tax election.

- Annual Compliance: Annual accounts must be filed with the National Bank of Belgium; a VOF with turnover below certain thresholds may qualify for a simplified micro-entity regime.

- Treaty Access: Pass-through treatment may limit direct access to Belgium's extensive double tax treaty network; a corporate tax election for the CommV can restore treaty eligibility.

- Conversion: Both structures can be converted into a BV or NV under the WVV without requiring dissolution, subject to compliance with restructuring formalities.

- Restrictions: Limited partners in a CommV who perform management acts risk losing their limited liability status under WVV provisions.

Sub-Types

Gewone Commanditaire Vennootschap (CommV)

The standard limited partnership form, distinguishing between managing general partners and passive limited partners. It is commonly used for family investment structures and private equity vehicles where capital contributors seek liability protection without management responsibilities.

Commanditaire Vennootschap op Aandelen (CommVA)

The CommVA — a partnership limited by shares — divides the limited partners' contributions into transferable shares. This structure suits larger capital-raising arrangements where transferability of interests is operationally necessary, while retaining at least one general partner with unlimited liability.

Both partnership forms suit closely held trading businesses and family-owned enterprises seeking structural simplicity without the formality of a capital company. The absence of a minimum capital requirement lowers the barrier to formation, though unlimited liability for general partners remains a material constraint in higher-risk commercial activities.

VOF and CommV structures are best suited for small to medium-sized businesses, professional firms, or family enterprises where partners are comfortable with direct liability exposure or can segregate risk through the CommV's two-tier partner structure.

Foreign Business Presence in Belgium [Branch Office, Representative Office]

A foreign company branch office Belgium registration falls under the Companies and Associations Code (CAC), which came into force in May 2019. A branch office (bijkantoor in Dutch, succursale in French) has no separate legal personality — it is an extension of the parent company, which bears full liability for the branch's obligations.

Registration is handled through the Crossroads Bank for Enterprises (CBE), and the branch must be published in the Belgian Official Gazette (Belgisch Staatsblad). A representative office, by contrast, is not formally registered as a trading entity and is restricted to preparatory or auxiliary activities such as market research.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Personality | None (extension of parent) | None |

| Liability | Parent bears full liability | Parent bears full liability |

| Trading Activity | Permitted | Not permitted; auxiliary only |

| Local Representative | Mandatory — a permanent representative domiciled in Belgium must be appointed | Not formally required |

| Registered Address | Required in Belgium | Required in Belgium |

| Share Capital | None required at branch level | None required |

| Privacy | Parent company documents filed publicly with CBE | Minimal public disclosure |

Focus Points

- Taxation: Branch profits are subject to corporate income tax at the standard rate of 25%; VAT registration is required for taxable activities; withholding tax may apply to certain payments to the parent; no separate stamp duty on branch formation.

- Treaty Access: Belgium's extensive tax treaty network generally covers branch operations, though treaty benefits depend on the parent entity's jurisdiction and structure.

- Economic Substance: The permanent representative must be genuinely active; a purely administrative arrangement may not satisfy Belgian tax authorities.

- Annual Compliance: Branches must file the parent's annual accounts (translated if necessary) with the CBE each year, in addition to local tax returns.

- Conversion: A branch can be converted into a locally incorporated entity such as a BV, though this requires a full incorporation procedure.

Closing

A branch office suits foreign firms testing the Belgian market or executing contracts without committing to a separate incorporated entity, while a representative office is appropriate only for pre-commercial activities. The branch's key limitation is unlimited parental liability, with no liability ring-fencing at the local level.

A branch office is best suited for established foreign companies that need operational presence without the governance obligations of a standalone Belgian subsidiary.

Sole Proprietorship in Belgium [Eenmanszaak / Entreprise Individuelle]

The Eenmanszaak sole proprietorship Belgium is the simplest form of self-employment available under Belgian law. Unlike corporate entities governed by the Companies and Associations Code of 2019, this structure carries no separate legal personality — the proprietor and the business are legally one and the same.

Unlimited personal liability is the defining legal characteristic here. All debts incurred by the business are recoverable against the proprietor's private assets. One partial protection exists: under Belgian law, a sole trader may submit a declaration of imputability (verklaring van hoofdverblijfplaats) before a notary to shield the primary residence from professional creditors.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole Proprietorship (no separate legal personality) | Proprietor and business are legally identical |

| Members | Single natural person only | No minimum capital; no shareholders or directors |

| Local Presence | Registered address in Belgium required | Must register with the Crossroads Bank for Enterprises (CBE) |

| Capital | No minimum capital requirement | No statutory capital rules apply |

| Privacy | Proprietor's name is publicly linked to the business | No anonymity from public CBE records |

| Social Status | Must register as self-employed (zelfstandige) with a social insurance fund (sociaal verzekeringsfonds) | Mandatory before commencing activity |

Focus Points

- Taxation: Subject to Belgian personal income tax (PIT) at progressive rates up to 50%; VAT registration required if annual turnover exceeds the applicable threshold; no corporate tax applies; no withholding tax on profit distributions since no dividends are paid.

- Annual Compliance: Annual personal income tax return required; simplified accounting obligations apply for small sole traders under Article III.85 of the Code of Economic Law.

- Treaty Access: Does not benefit from corporate tax treaty provisions; applicable treaties are those covering individual residents.

- Conversion: A sole proprietorship can be converted into a BV or other corporate form, but the process requires a notarial act and transfer of assets.

- Restrictions: Non-EEA nationals must hold a valid professional card (beroepskaart) or equivalent permit before registering.

Closing

The Eenmanszaak suits freelancers, independent consultants, and micro-traders who require a low-cost, administratively light structure with no minimum capital outlay. The absence of formation costs and simplified bookkeeping are practical advantages, though unlimited personal liability remains a material exposure that limits its suitability as the business scales.

Self-employed individuals and sole traders in Belgium with low startup capital and limited liability exposure who intend to operate at small scale.

How to Choose the Right Entity Type in Belgium

Knowing how to choose a company type in Belgium requires more than comparing formation costs — the structure you register determines your liability exposure, tax treatment, governance obligations, and operational capacity.

Why Your Entity Choice Matters

Selecting the wrong structure carries concrete legal and financial consequences:

- A sole proprietorship or partnership exposes the owner to unlimited personal liability, which cannot be rectified without dissolution and re-registration under a separate legal entity.

- Forming a BV or NV when your activity is a single-person consultancy subjects you to annual filing obligations and potential statutory audit requirements that do not apply to a sole trader.

- Choosing a structure without legal personality — such as a VOF — means the entity cannot independently hold assets, enter contracts, or access Belgium's double tax treaty network in its own name.

- Registering a branch rather than a subsidiary creates joint liability exposure for the foreign parent, which a separate BV or NV would otherwise limit.

Key Factors to Consider

- Business Activity: Active trading, asset holding, and regulated sectors (such as banking or insurance) each fall under distinct authorization requirements governed by the Code of Companies and Associations (WVV/CSA).

- Liability Exposure: If personal asset protection is a priority, only entities with separate legal personality — BV, NV, CV — provide statutory limited liability.

- Ownership and Management: Single-founder operations suit the BV's flexible governance model; multi-party structures with external investors typically require the NV's formal board framework.

- Tax Objectives: Your eligibility for Belgium's notional interest deduction or participation exemption depends on the entity type and whether it qualifies as a resident taxpayer under Belgian corporate income tax rules.

- Substance Capacity: If you cannot maintain a genuine operational presence — registered office, decision-making, staffing — certain structures will face challenge under Belgian anti-abuse provisions.

- Exit Strategy: The WVV/CSA permits conversion between certain entity forms, but not all conversions are available; verifying this before formation avoids costly restructuring.

Compliance Services for Companies in Belgium

Ongoing compliance support for Belgian entities, including annual filing, statutory reporting, and regulatory obligations under the WVV/CSA.

Conclusion

Choosing the right structure is the central decision in any Belgium company formation, and this guide has outlined the options governed primarily by the Code of Companies and Associations (WVV/CSA), which came into force in 2019. The BV is now the most commonly registered entity, favored by SMEs and startups for its flexible capital rules and straightforward governance. The NV suits firms anticipating public capital markets or complex shareholder arrangements. Cooperatives under the CV form serve businesses with a genuine member-benefit purpose. Partnerships carry unlimited liability and fit closely-held, trust-based operations. Branch offices and representative offices extend foreign firms' presence without creating a separate legal person.

Regulatory direction in Belgium continues toward digital filings, UBO transparency, and alignment with EU anti-money laundering directives. For businesses assessing fit, Expanship's team works directly with these structures across Belgian formation and compliance mandates.

How Expanship Can Assist You

Expanship's Belgium company incorporation services cover every major entity type discussed in this guide — from registering a Besloten Vennootschap (BV) with the Crossroads Bank for Enterprises (CBE) to structuring a Naamloze Vennootschap (NV) that meets the Belgian Code of Companies and Associations requirements. Your corporate structure needs a solid foundation from day one.

Across the full incorporation and post-registration cycle, Expanship provides:

- Document preparation, notarization, and legalization

- Registered agent and registered office provision in Belgium

- Filing coordination with the CBE and relevant commercial courts

- Liaison with the Belgian Official Gazette (Belgisch Staatsblad) for mandatory publications

- Ongoing compliance management, including annual accounts and UBO register obligations

- Banking introduction assistance for your Belgian entity

Reach out to Expanship Belgium to discuss your specific requirements with our corporate services team.

Frequently Asked Questions (FAQ)

The Besloten Vennootschap (BV) is the most frequently incorporated entity following the 2019 CAC reform. Its removal of the minimum capital requirement and flexible share transfer restrictions make it accessible to a wide range of businesses, from startups to established SMEs.

Both structures are fully taxable under Belgian corporate income tax and hold equal rights to trade locally. The NV requires a minimum share capital of EUR 61,500 and a more formal governance structure, including a board of at least three directors in most configurations, whereas a BV can be formed with a single director and no statutory minimum capital, though adequate financial resources must be demonstrated through a financial plan submitted to a notary.

Among Belgian structures, the BV and NV both require disclosure of beneficial ownership in the UBO register, administered through the FPS Finance portal. Shareholder identity is recorded with the Crossroads Bank for Enterprises (CBE), so neither structure offers full anonymity. Nominee arrangements are legally permissible but do not override UBO reporting obligations.

A sole individual can incorporate a BV or NV, as both permit single-shareholder formation under the CAC. Partnerships such as the Vennootschap onder Firma (VOF) require at least two partners by definition, and a Commanditaire Vennootschap (CommV) requires one general and one limited partner.

All entity types, including the BV, NV, CV, and partnerships, are open to foreign nationals and non-resident companies without a requirement for local shareholding. A foreign founder does need a Belgian enterprise number from the CBE and, where applicable, a professional card if personally managing operations as a non-EEA national.

The CAC expressly allows conversion between entity types through a notarial deed, subject to shareholder approval and publication in the Belgian Official Gazette. A BV can be converted to an NV, for example, provided the NV's minimum capital threshold is met at the time of conversion.

The BV, NV, and CV each hold full legal personality separate from their members. General partnerships (VOF) also hold legal personality under Belgian law, though partners remain jointly and severally liable for the firm's obligations, which distinguishes them from the limited-liability structures.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.