Key Takeaways

- The Private Company Limited by Shares under the Companies Act, Cap. 308 is the most commonly registered structure for both resident and foreign-owned operating businesses in Barbados.

- Company registration and administration in Barbados is governed by the Corporate Affairs and Intellectual Property Office (CAIPO), operating within a common law legal framework inherited from British colonial rule.

- The Society with Restricted Liability, governed by the Societies with Restricted Liability Act, Cap. 318B, provides pass-through tax treatment, making it a distinct option for joint venture arrangements.

- Entity selection in Barbados carries direct consequences for treaty access and compliance obligations under the Barbados Revenue Authority, given the jurisdiction's expanding network of double taxation treaties and tax information exchange agreements.

Introduction to Entity Types in Barbados

Barbados is an independent island nation in the southeastern Caribbean, situated east of Saint Vincent and the Grenadines and northeast of Trinidad and Tobago. As a sovereign state and former British colony, it operates a common law legal system and maintains a regulated corporate environment governed primarily by the Corporate Affairs and Intellectual Property Office (CAIPO), the body responsible for company registration and administration.

The types of business entities in Barbados span both domestic and international structures, reflecting the jurisdiction's position as a treaty-based, low-tax financial centre with an extensive network of double taxation agreements.

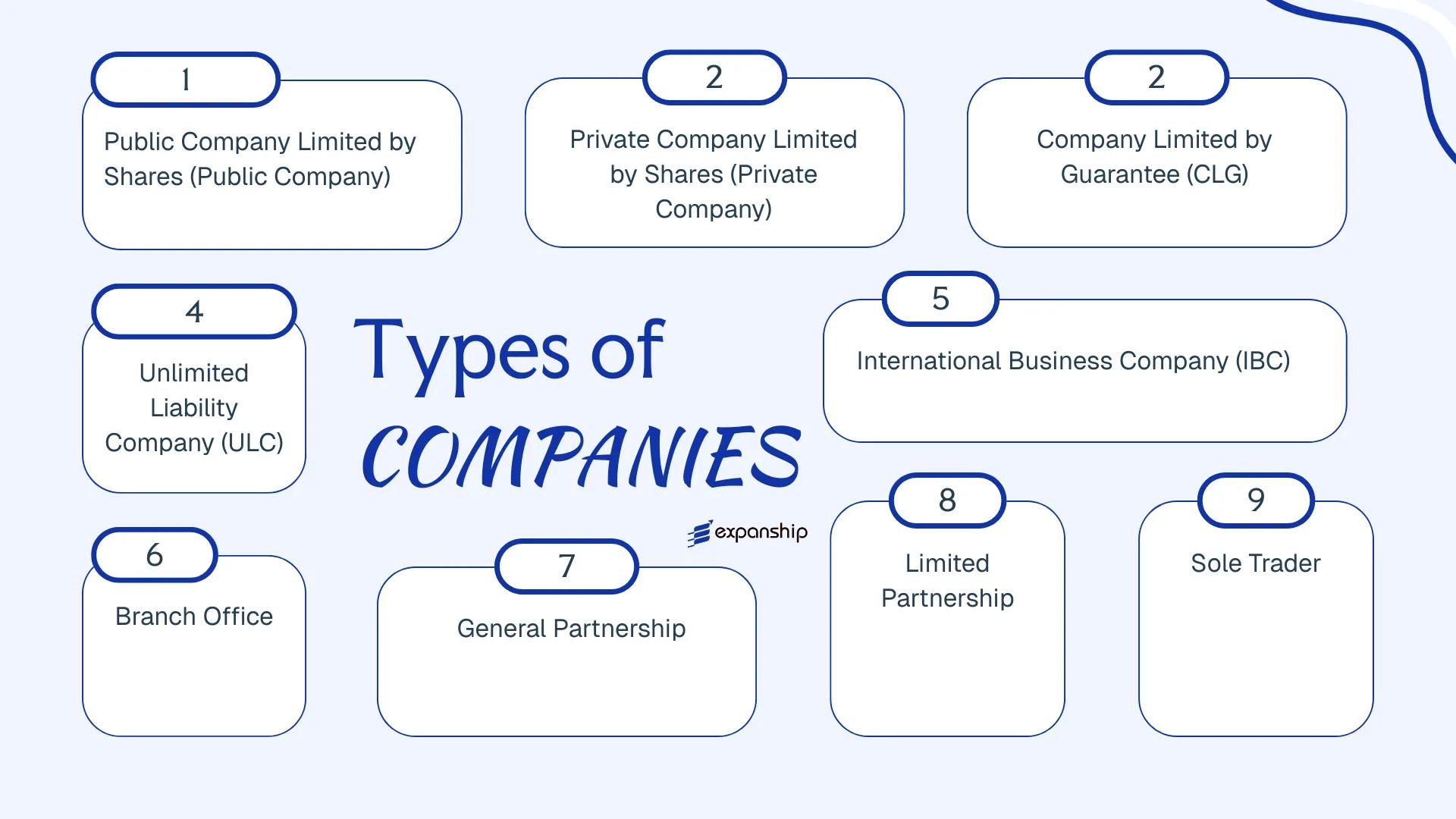

Available entity forms include the Public Company Limited by Shares, Private Company Limited by Shares, Company Limited by Guarantee, Unlimited Liability Company, Exempt Insurance Company, International Business Company, Society with Restricted Liability, Foreign Branch or External Company, General Partnership, Limited Partnership, and Sole Trader.

Each structure carries distinct legal characteristics, ownership rules, and regulatory obligations under instruments such as the Companies Act, Cap. 308 and the Societies with Restricted Liability Act, Cap. 318B. This article examines each entity type in turn, covering formation requirements, governance rules, and the considerations most relevant to your business objectives.

An Overview of Business Structures in Barbados

Barbados offers more than ten distinct legal forms for conducting business, governed primarily by the Companies Act, Cap. 308, alongside several specialist statutes including the Exempt Insurance Act, Cap. 308A, the Societies with Restricted Liability Act, Cap. 318B, and the International Business Companies Act. Each structure carries its own liability profile, tax treatment, and permitted activities.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Public Company | Corporation | Limited | Taxed | Yes | 1 shareholder | CAIPO | Companies Act, Cap. 308 |

| Private Company | Corporation | Limited | Taxed | Yes | 1 shareholder | CAIPO | Companies Act, Cap. 308 |

| Company Ltd by Guarantee | Corporation | Limited | Taxed | Yes | 1 member | CAIPO | Companies Act, Cap. 308 |

| Unlimited Liability Company | Corporation | Unlimited | Taxed | Yes | 1 shareholder | CAIPO | Companies Act, Cap. 308 |

| Exempt Insurance Company | Corporation | Limited | Exempt | Restricted | 1 shareholder | FSC | Exempt Insurance Act, Cap. 308A |

| International Business Company | Corporation | Limited | Exempt / Reduced | Restricted | 1 shareholder | CAIPO / FSC | IBC Act |

| Society with Restricted Liability | Hybrid entity | Limited | Varies | Yes | 2 members | CAIPO | SRL Act, Cap. 318B |

| External Company (Branch) | Branch / Non-resident | Varies | Taxed | Yes | N/A | CAIPO | Companies Act, Cap. 308 |

| General Partnership | Unincorporated | Unlimited | Taxed | Yes | 2 partners | CAIPO | Partnership Act |

| Limited Partnership | Unincorporated | Mixed | Taxed | Yes | 2 partners | CAIPO | Partnership Act |

| Sole Trader | Unincorporated | Unlimited | Taxed | Yes | 1 person | BRA | N/A |

Each of these structures is examined in full in the sections below.

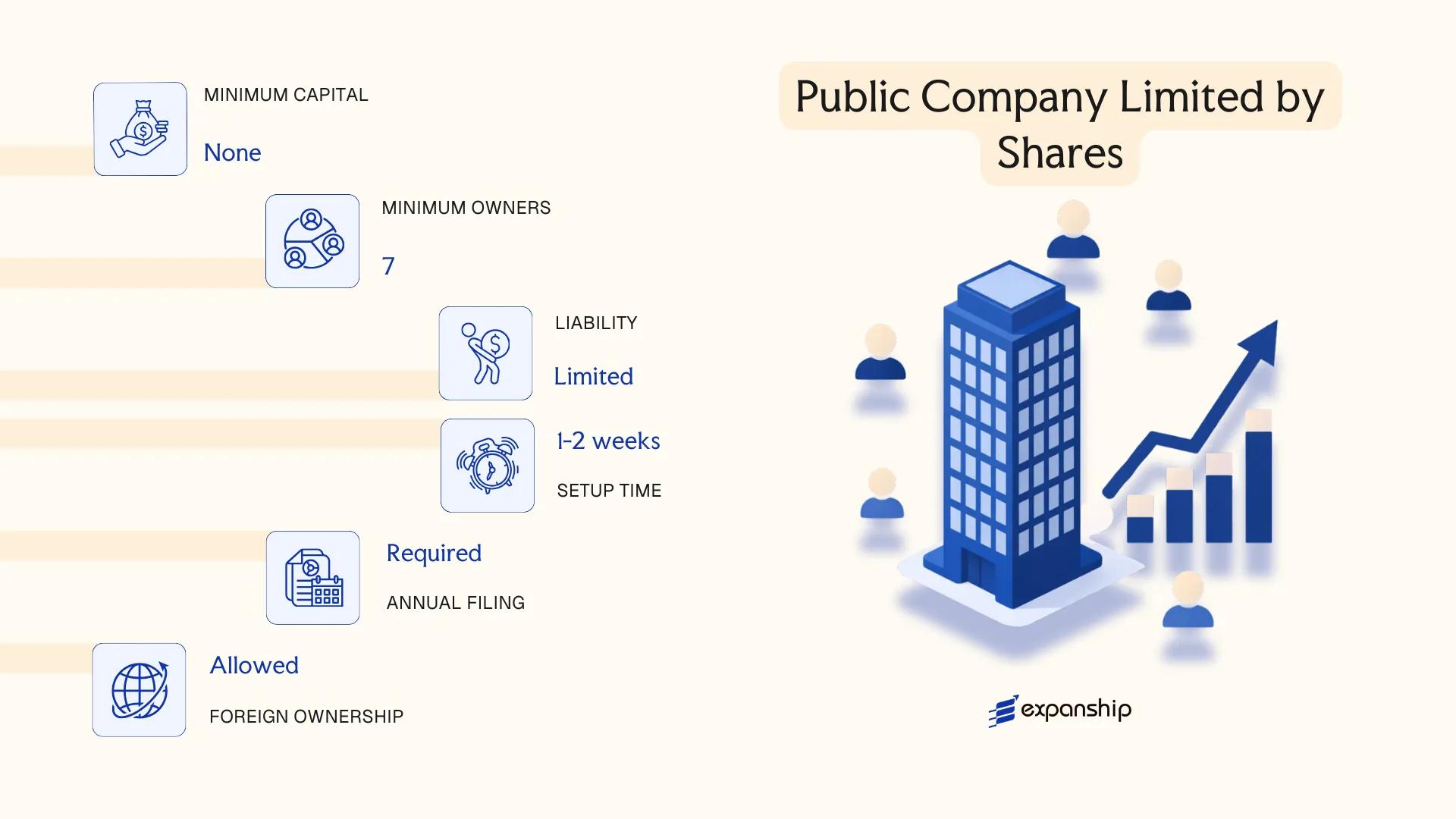

Public Company Limited by Shares under the Companies Act, Cap. 308

A Barbados public company limited by shares is incorporated under the Companies Act, Cap. 308 and carries full separate legal personality, meaning it can own assets, enter contracts, and incur liabilities in its own name. Shareholder liability is capped at the amount unpaid on their shares.

Unlike its private counterpart, this structure permits unrestricted share transfers and can offer securities to the public. Listing on the Barbados Stock Exchange is available to qualifying entities, making this form relevant for businesses seeking access to capital markets.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Company limited by shares | Separate legal personality; governed by the Companies Act, Cap. 308 |

| Members | Shareholders; no maximum | Minimum 1 shareholder; shares freely transferable |

| Directors | Minimum 3 directors required | At least one must be resident in Barbados |

| Local Presence | Registered office in Barbados; company secretary required | Registered agent not mandated but a local office address is obligatory |

| Capital | No statutory minimum share capital; denominated in any currency | Shares may be issued with or without par value |

| Privacy | Directors and shareholders on public record | Annual returns filed with the Corporate Affairs and Intellectual Property Office (CAIPO) are publicly accessible |

Focus Points

- Taxation: Subject to corporate income tax at the standard rate; Barbados Tax Authority administers VAT (17.5%), withholding taxes on dividends, interest, and royalties paid abroad, and stamp duty on share transfers.

- Economic Substance: Public companies conducting relevant activities must satisfy substance requirements under the Income Tax Act and associated regulations.

- Annual Compliance: Annual returns, audited financial statements, and shareholder meetings are mandatory; filings are made with CAIPO.

- Treaty Access: Barbados maintains a network of double taxation agreements; public companies resident in Barbados may access treaty benefits subject to beneficial ownership tests.

- Conversion: A public company may be converted to a private company by special resolution and amendment of its articles, subject to CAIPO approval.

Closing

This structure suits businesses planning to raise equity from the public, pursue a stock exchange listing, or operate at a scale requiring broad shareholder participation. The ability to issue shares freely is its principal advantage; the mandatory audit, minimum three-director requirement, and public disclosure of records represent meaningful compliance overhead for smaller operations.

Public companies limited by shares are most appropriate for larger enterprises seeking public capital or a Barbados Stock Exchange listing.

Company Incorporation in Barbados

Incorporate a public or private company in Barbados with end-to-end support from our corporate services team.

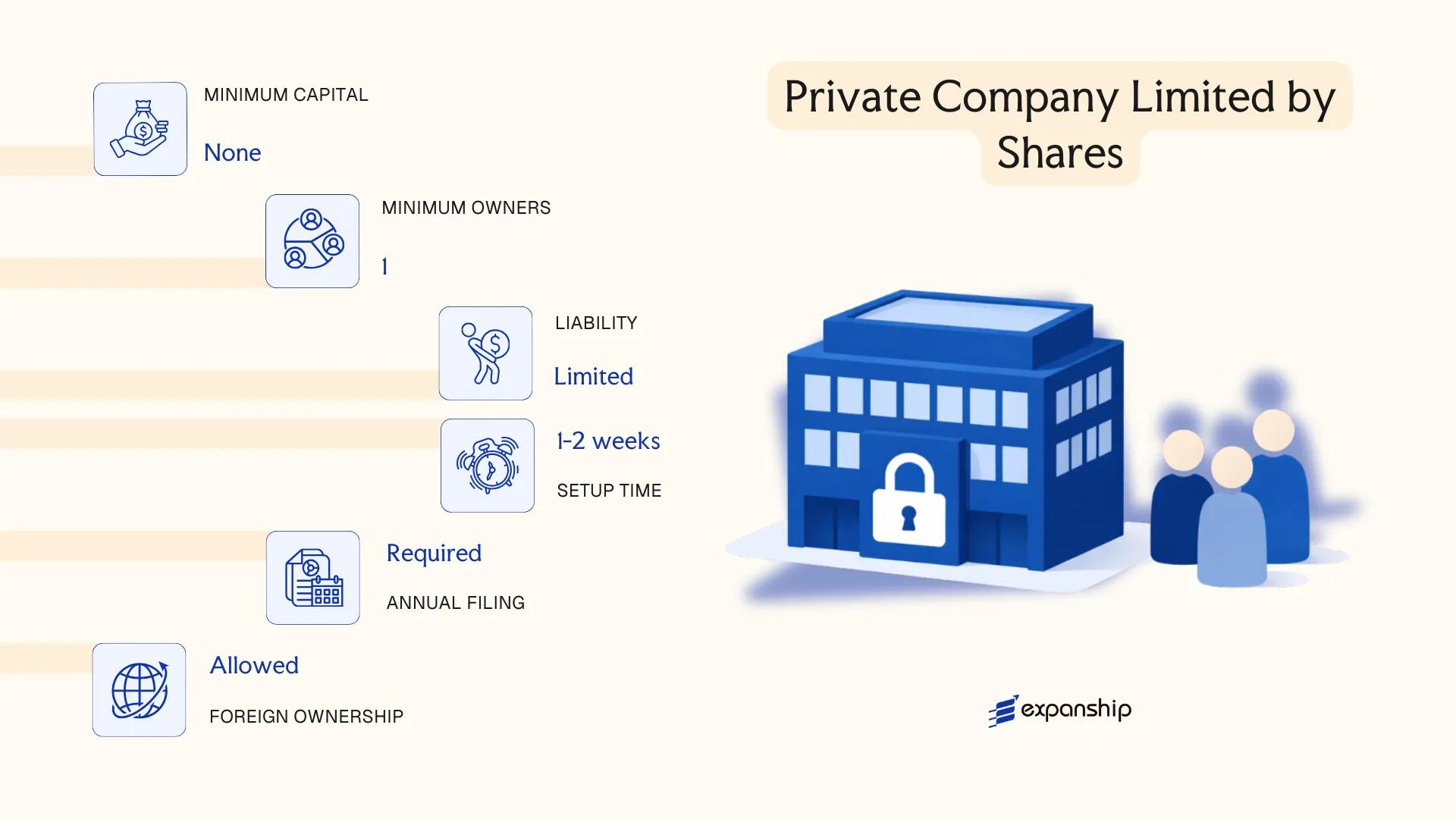

Private Company Limited by Shares under the Companies Act, Cap. 308

A Barbados private company limited by shares is incorporated under the Companies Act, Cap. 308 and holds a legal identity separate from its shareholders. Liability is confined to the amount unpaid on shares held.

Restrictions on share transfer distinguish this structure from its public counterpart. The entity cannot offer securities to the public, and its articles of incorporation must expressly limit the right to transfer shares.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Company limited by shares | Governed by Companies Act, Cap. 308 |

| Members | Shareholders; 1–50 | Directors minimum: 1; no maximum |

| Local Presence | Registered office in Barbados | No statutory requirement for a local director |

| Capital | No minimum share capital; denominated in any currency | Shares may be issued with or without par value |

| Privacy | Register of directors is public; shareholder register not publicly searchable | Beneficial ownership reported to CAIPO |

Focus Points

- Taxation: Subject to corporate income tax; rate varies by income type and residency status; VAT registration required if turnover exceeds the statutory threshold; withholding tax applies to dividends, interest, and royalties paid abroad.

- Economic Substance: Private companies engaged in relevant activities must satisfy substance requirements under the Income Tax Act amendments.

- Annual Compliance: Annual returns filed with the Corporate Affairs and Intellectual Property Office (CAIPO); audited financials may be required depending on size.

- Treaty Access: Resident companies may access Barbados's double taxation treaty network.

- Conversion: Can be converted to a public company by amending its articles and meeting the relevant threshold requirements under Cap. 308.

Closing

This structure suits trading operations, holding arrangements, joint ventures, and family-owned businesses where restricted share transferability is operationally practical. Its single-shareholder option provides flexibility, though the 50-member ceiling limits its use for broad investor participation.

Private companies limited by shares work best for closely held businesses, subsidiary operations, and entrepreneurs seeking a straightforward corporate vehicle with defined liability boundaries.

Company Limited by Guarantee under the Companies Act, Cap. 308

Governed by the Companies Act, Cap. 308, a company limited by guarantee in Barbados holds separate legal personality distinct from its members. Rather than issuing shares, this structure relies on members' undertakings to contribute a fixed sum to the company's assets if it is wound up.

Liability is capped at the amount each member guarantees, which is typically a nominal figure. This makes the non-profit company structure Barbados organisations favour particularly suited to associations, foundations, and similar bodies where capital accumulation is not the primary objective.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Incorporated entity under Companies Act, Cap. 308 | Separate legal personality; no share capital |

| Members | Minimum 1 member; no statutory maximum | Members are guarantors, not shareholders |

| Directors | Minimum 1 director required | No residency requirement under the Act |

| Local Presence | Registered office address in Barbados required | Must be maintained at all times |

| Guarantee Amount | Set in the memorandum; typically nominal (e.g., BBD 10–100) | Represents maximum liability per member on winding up |

| Privacy | Director and member details filed with the Corporate Affairs and Intellectual Property Office (CAIPO) | Public register accessible |

Focus Points

- Taxation: Generally exempt from corporate income tax if operating as a non-profit; VAT registration required if taxable supplies exceed the registration threshold; stamp duty may apply to certain instruments.

- Annual Compliance: Annual return must be filed with CAIPO; audited financial statements may be required depending on the entity's size and activities.

- Economic Substance: No economic substance obligations apply to entities not engaged in relevant activities under the Economic Substance legislation.

- Conversion: The Companies Act permits conversion to other company forms subject to member approval and regulatory filing, though this is uncommon for guarantee companies.

- Restrictions: Cannot distribute profits or assets to members during operation; any surplus must be applied toward the entity's stated objects.

Closing

To register a company limited by guarantee in Barbados, you would file a memorandum and articles of incorporation with CAIPO, specifying the guarantee amount and the entity's objects. This structure suits membership associations, regulatory bodies, charities, and professional organisations where profit distribution is prohibited and member liability must remain defined and limited.

A company limited by guarantee is most appropriate for non-profit organisations, industry associations, and foundations that require a formal corporate structure without share capital.

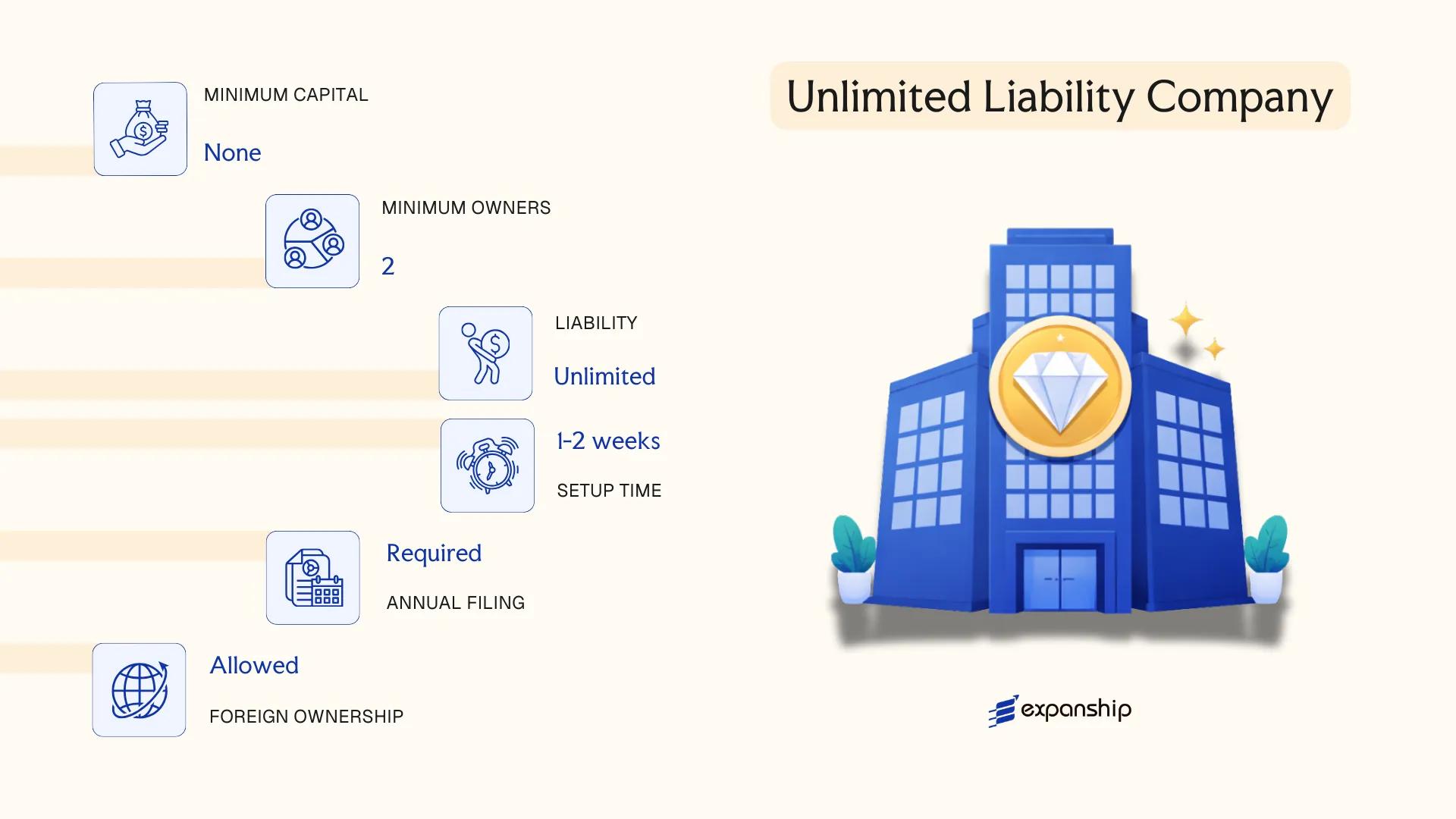

Unlimited Liability Company under the Companies Act, Cap. 308

An unlimited liability company (ULC) in Barbados is formed under the Companies Act, Cap. 308 and holds the status of a separate legal entity. Unlike other corporate forms under the same legislation, it does not limit the liability of its members — shareholders remain personally liable for the company's debts without a statutory cap.

Despite this exposure, the ULC structure is recognised in several treaty jurisdictions for specific tax planning arrangements, particularly where a pass-through tax treatment is sought in a foreign parent's home jurisdiction.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unlimited company with separate legal personality | Incorporated under Companies Act, Cap. 308 |

| Members | Shareholders; minimum 1, no statutory maximum | Members bear unlimited personal liability for company debts |

| Local Presence | Registered office in Barbados; registered agent required | Must maintain a physical registered address at all times |

| Capital | No minimum share capital; denominated in any currency | Shares may be par or no-par value |

| Privacy | Shareholder details filed with Corporate Affairs and Intellectual Property Office (CAIPO) | Limited public disclosure; beneficial ownership held on record |

Focus Points

- Taxation: Subject to Barbados corporate income tax at the standard rate; VAT registration required if turnover thresholds are met; withholding tax may apply to dividends, interest, and royalties paid to non-residents under domestic law, subject to treaty relief.

- Economic Substance: ULCs carrying out relevant activities must satisfy the economic substance requirements under the Income Tax Act as amended.

- Annual Compliance: Annual returns must be filed with CAIPO; financial statements and tax returns are required on an ongoing basis.

- Treaty Access: May access Barbados's network of double taxation agreements, subject to residency qualification and anti-avoidance provisions.

- Conversion: A ULC may be converted to a limited liability company under the Companies Act, subject to approval and re-registration with CAIPO.

Closing

The ULC structure is used primarily by groups seeking pass-through tax treatment in jurisdictions such as Canada or the United States, where the unlimited liability feature is the qualifying condition. The absence of liability protection is a direct structural drawback that requires careful consideration before adoption.

Best suited for multinational groups implementing cross-border tax structuring where a specific foreign jurisdiction requires an unlimited liability vehicle as a condition for transparent treatment.

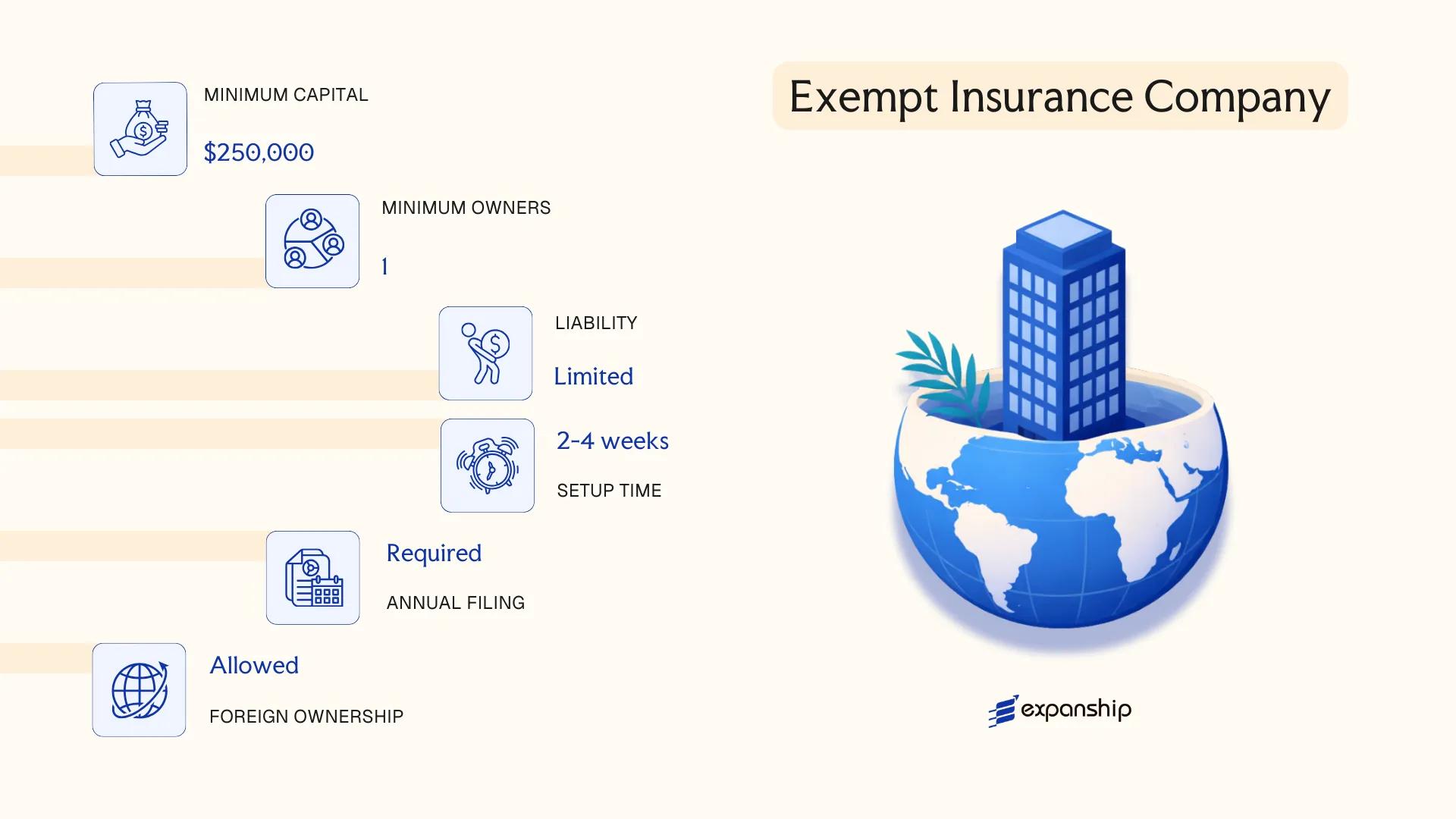

Exempt Insurance Company under the Exempt Insurance Act, Cap. 308A

Barbados exempt insurance company registration is governed by the Exempt Insurance Act, Cap. 308A, administered by the Financial Services Commission (FSC). The legislation provides a dedicated framework for insurance entities that underwrite risks outside Barbados, making this structure distinct from domestic insurance vehicles.

An exempt insurance company holds separate legal personality and benefits from limited liability. It is primarily used as a captive insurance vehicle, where a parent corporation insures its own group-related risks rather than underwriting third-party business.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Company incorporated or registered under Cap. 308A | Separate legal entity distinct from its parent |

| Members | Shareholders; minimum 1, no statutory maximum | Typically closely held by a parent group |

| Directors | Minimum 2 directors required | At least one must be a fit-and-proper resident of Barbados |

| Local Presence | Registered office and licensed insurance manager in Barbados | Insurance manager must be FSC-approved |

| Capital | Minimum paid-up capital prescribed by the FSC; denominated in any approved currency | Specific thresholds vary by class of licence |

| Privacy | Shareholder details not publicly filed | Beneficial ownership reported to FSC, not public register |

Focus Points

- Taxation: Exempt insurance companies are taxed at a reduced rate under a sliding scale regime; no withholding tax on dividends paid to non-residents.

- Economic Substance: Insurance activity and management must be conducted from within Barbados to satisfy FSC licensing conditions.

- Annual Compliance: Annual audited financial statements, actuarial reports where required, and licence renewal filings must be submitted to the FSC.

- Treaty Access: Barbados's tax treaty network may be accessible depending on the entity's residency status and the treaty's specific provisions.

- Restrictions: The entity may not underwrite risks of Barbados residents or domestic risks without separate authorisation.

Sub-Types

Class 1 Captive

A Class 1 licence is issued to a single-parent captive that insures only the risks of its own corporate group. It carries the lowest minimum capital requirements of the captive classes.

Class 2 Captive

A Class 2 licence permits the entity to insure group risks and a limited proportion of unrelated third-party risks. This structure suits groups that wish to generate modest premium income from outside their corporate family.

Class 3 and Class 4

Class 3 covers broader commercial captive arrangements, while Class 4 is reserved for large commercial insurers. Both carry higher capital and reporting obligations and are less commonly used in pure captive structures.

The exempt insurance company is used primarily by multinational groups managing internal risk financing and by professional captive managers establishing dedicated insurance cells. A key advantage is the regulatory framework's explicit recognition of captive structures, but the requirement for a locally licensed insurance manager represents an ongoing operational cost.

This structure is best suited for multinational corporations or financial groups seeking a regulated, tax-efficient vehicle for captive insurance arrangements within an internationally recognised jurisdiction.

International Business Company under the International Business Companies Act

Barbados International Business Company formation is governed by the International Business Companies Act, Cap. 77 (the "IBC Act"), which provides for a corporate structure designed primarily for cross-border commercial activity. The IBC is a body corporate with separate legal personality and limited liability for its shareholders, making it structurally similar to a standard company but with a regulatory framework oriented toward international operations.

Originally introduced to attract foreign investment, the IBC regime has undergone significant reform since Barbados committed to OECD and CARICOM transparency standards. New IBCs cannot be registered under the original concessionary tax regime; the structure now operates within the general corporate tax framework.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Body corporate (company limited by shares) | Separate legal personality; shareholders not liable for company debts |

| Members | Shareholders: minimum 1, no maximum | Directors: minimum 1, no nationality or residency requirement |

| Local Presence | Registered agent and registered office required in Barbados | Agent must be licensed under local law |

| Capital | No prescribed minimum share capital; denominated in any currency | Shares may be par value or no-par-value |

| Privacy | Beneficial ownership disclosed to the Corporate Affairs and Intellectual Property Office (CAIPO) | Not on public register; subject to competent authority access |

Focus Points

- Taxation: Subject to the standard corporate income tax rate (currently 5.5% on the first BBD 1 million, scaling up); no separate IBC concessionary rate; VAT, withholding tax, and stamp duty obligations apply under general law.

- Economic Substance: Must demonstrate adequate economic substance in Barbados if conducting a relevant activity, per the Companies (Economic Substance) Act.

- Annual Compliance: Annual filing with CAIPO required; annual return and financial statements must be maintained.

- Treaty Access: Barbados maintains a network of double taxation agreements; IBC access to treaty benefits depends on substance and residency conditions being met.

- Restrictions: Cannot carry on business with Barbados residents except as permitted by the IBC Act; certain regulated activities require additional licensing.

Closing

The IBC structure suits holding arrangements, international trading operations, and IP ownership where genuine economic activity can be demonstrated within the jurisdiction. Its integration into the standard tax regime removes the historic rate advantage, which is a material consideration for cost-sensitive structures.

Best suited for internationally active businesses that can satisfy economic substance requirements and wish to benefit from Barbados's tax treaty network.

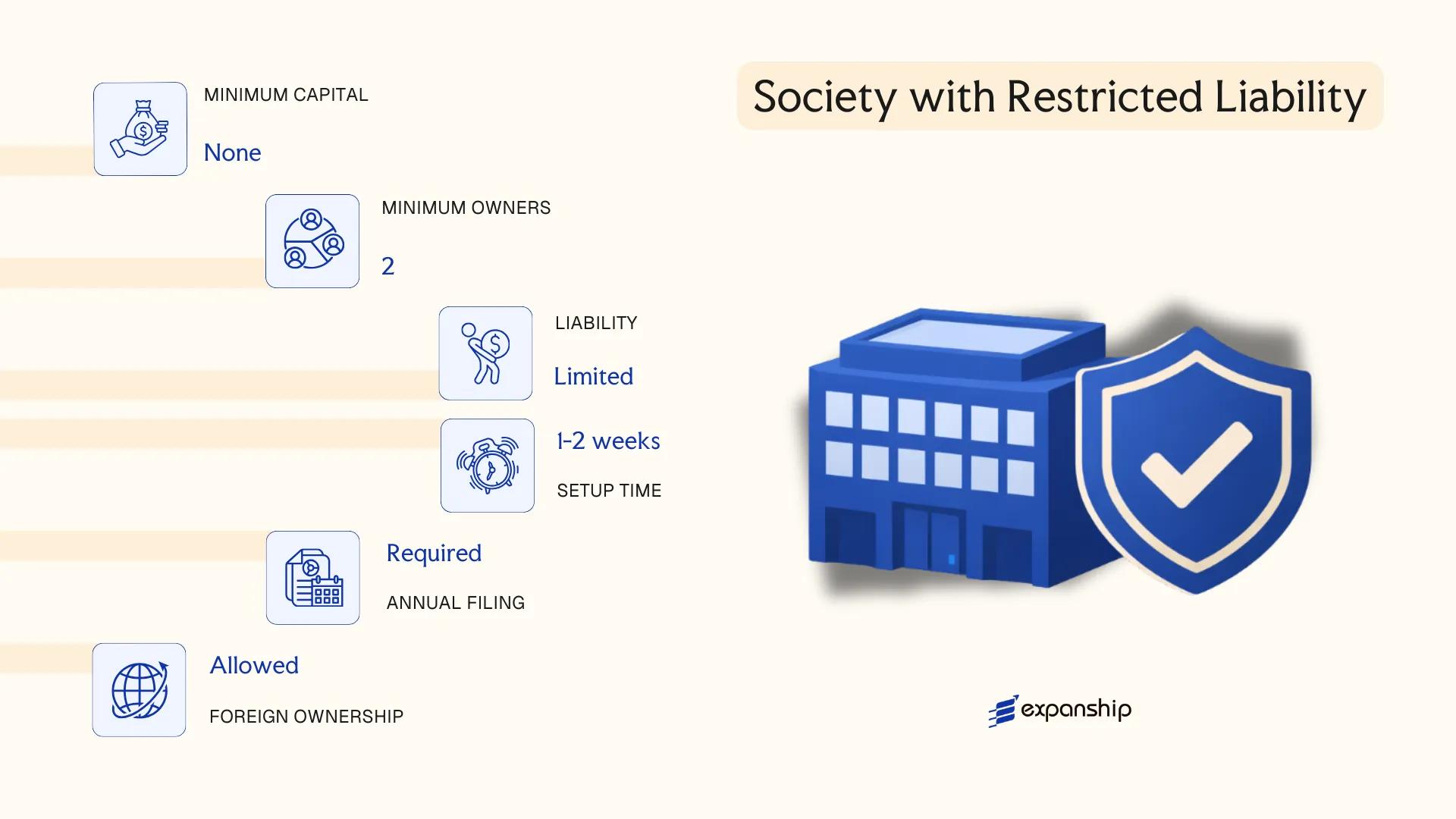

Society with Restricted Liability under the Societies with Restricted Liability Act, Cap. 318B

The Barbados Society with Restricted Liability (SRL) is governed by the Societies with Restricted Liability Act, Cap. 318B. Enacted to attract international business and investment structures, the legislation created a hybrid entity that combines characteristics of a partnership with the limited liability protections typically associated with a corporate form.

An SRL carries separate legal personality, meaning it can hold assets, enter contracts, and incur obligations in its own name. Members are not personally liable for the debts of the entity beyond their agreed contributions, which makes this structure functionally comparable to a limited liability company under civil law systems.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Hybrid entity (corporate/partnership) | Governed by Cap. 318B; not a company under the Companies Act |

| Members | Referred to as Members; minimum 1, no statutory maximum | At least one member must be identified in the Articles; members may be individuals or legal entities |

| Local Presence | Registered office and licensed registered agent required | Both must be maintained in Barbados throughout the entity's existence |

| Capital | No mandatory minimum capital; contributions may be in cash or in kind | Denominated in any currency; capital structure defined in the Articles of Society |

| Privacy | Members' details not publicly filed | Register of members held internally; beneficial ownership reported to the relevant authority |

Focus Points

- Taxation: SRLs are generally subject to corporate income tax; treaty access depends on residency and substance; withholding tax, VAT registration, and stamp duty obligations may apply depending on the nature of transactions conducted.

- Economic Substance: Entities conducting relevant activities must satisfy economic substance requirements under the Income Tax Act and related regulations.

- Annual Compliance: Annual returns and financial statements must be filed; the registered agent must be maintained at all times.

- Conversion: An SRL may be continued from or into a foreign jurisdiction if permitted by both the originating and receiving laws, subject to regulatory approval.

- Restrictions: SRLs may not offer shares to the public and are not listed on stock exchanges; their use for regulated financial activities requires separate licensing.

Closing

The SRL suits holding structures, joint ventures, and fund vehicles where members prefer a flexible governance framework over the rigid share-capital model of a standard company. Its key advantage is the ability to draft bespoke profit-sharing and management arrangements in the Articles of Society, though the relative unfamiliarity of the structure in some jurisdictions can complicate cross-border recognition and banking relationships.

The SRL is most appropriate for sophisticated investors and fund managers seeking a flexible, tax-efficient vehicle for holding assets or structuring multi-party investment arrangements.

Foreign Presence in Barbados [Branch Office, External Company Registration]

A foreign company seeking to operate in Barbados without incorporating a separate local entity can register as an external company under the Companies Act, Cap. 308. This route does not create a new legal person — the foreign entity remains the contracting party and retains full liability for obligations incurred locally.

Registration is handled through the Corporate Affairs and Intellectual Property Office (CAIPO). Once registered, the external company must maintain a registered office address and appoint a local agent authorised to accept service of process on its behalf.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Branch of a foreign corporation; no separate legal personality | The parent entity bears full liability for the branch's obligations |

| Governing Legislation | Companies Act, Cap. 308 (Part XIII) | Covers external company registration requirements |

| Local Presence | Registered office address; authorised local agent | Agent must be resident and authorised to accept service of process |

| Directors / Officers | No separate board required; parent company's directors govern | A local contact person must be designated |

| Share Capital | No separate capital requirement for the branch itself | Parent's capital structure applies |

| Privacy | Parent company's constitutional documents filed with CAIPO | These become part of the public record upon registration |

Focus Points

- Taxation: Branch profits are subject to corporate income tax at the standard rate; withholding tax may apply on remittances to the parent, and VAT registration is required if trading activity meets the threshold.

- Economic Substance: Branches conducting relevant activities must satisfy Barbados's economic substance requirements under the Income Tax Act (as amended) and related guidance.

- Annual Compliance: Audited or certified financial statements of the parent must be filed annually with CAIPO, along with any changes to directors or the registered agent.

- Treaty Access: Access to Barbados's double tax treaty network depends on the tax residency of the parent entity, not the branch registration alone.

- Restrictions: An external company cannot convert directly into a locally incorporated entity without a separate incorporation process.

Closing

Registering as an external company is a practical option for foreign businesses testing the local market or executing a defined project, but the absence of limited liability at the branch level means the parent entity is fully exposed to local claims.

Foreign corporations requiring a formal, registered presence for contract execution or regulatory compliance without committing to full local incorporation.

Partnerships in Barbados [General Partnership, Limited Partnership]

Governed by the Partnership Act, Cap. 312, partnerships in Barbados exist in two principal forms: the general partnership and the limited partnership. Unlike incorporated companies, a general partnership does not possess separate legal personality, meaning partners bear joint and several liability for the firm's obligations. Limited partnership registration Barbados follows a distinct statutory path, requiring formal registration with the Corporate Affairs and Intellectual Property Office (CAIPO) to achieve its hybrid structure.

A limited partnership must have at least one general partner with unlimited liability and at least one limited partner whose exposure is capped at their capital contribution. General partnerships, by contrast, involve no registration formality beyond any applicable business name filing.

Key Characteristics

| Requirement | General Partnership | Limited Partnership |

|---|---|---|

| Legal Personality | None | None |

| Members | Partners (min. 2, max. 20) | General partner(s) + limited partner(s); min. 2 total |

| Liability | Unlimited for all partners | Unlimited for general partners; limited for limited partners |

| Registration | Business name filing only | Formal registration with CAIPO required |

| Local Presence | No registered agent requirement | Registered office in Barbados required |

| Capital | No minimum; no prescribed currency | No statutory minimum |

| Privacy | Partnership agreement is private | Certificate of registration is public record |

Focus Points

- Taxation: Partnerships are fiscally transparent; profits are taxed in the hands of individual partners at applicable personal or corporate income tax rates, with no entity-level corporate tax. VAT registration obligations apply if taxable turnover thresholds are met.

- Economic Substance: General and limited partnerships engaged in relevant activities may attract substance requirements under the Income Tax Act amendments aligned with OECD standards.

- Annual Compliance: Limited partnerships must maintain their registered office and file any required renewals with CAIPO; general partnerships have minimal ongoing filing obligations.

- Treaty Access: Partners may access Barbados's tax treaty network depending on their own tax residency, not the partnership's status.

- Conversion: Barbados partnership law does not provide a straightforward statutory conversion mechanism to a corporate form; restructuring typically requires dissolution and fresh incorporation.

Sub-Types

General Partnership

All partners participate in management and carry unlimited personal liability. This structure suits professional service arrangements where principals intend to operate jointly without corporate formality.

Limited Partnership

One or more limited partners contribute capital and remain passive, while general partners manage day-to-day affairs. The limited partner's liability is confined to their agreed contribution, provided they do not participate in management.

When to Consider a Partnership

Partnerships suit joint ventures, professional practices, and investment arrangements where pass-through taxation is preferred over corporate-level tax. The absence of separate legal personality is a material drawback when entering contracts or holding assets in the firm's own name.

Barbados partnerships are most appropriate for two or more parties seeking a tax-transparent, low-formality structure for a defined commercial or investment purpose.

Sole Trader

Sole trader registration in Barbados does not create a separate legal entity. You and the business are legally the same person, meaning personal assets are fully exposed to business liabilities. There is no governing corporate statute equivalent to the Companies Act, Cap. 308; instead, the registration process falls under the Business Names Act, Cap. 317.

If you operate under your own legal name, formal registration may not be required. Trading under any other name, however, requires registration of that business name with the Corporate Affairs and Intellectual Property Office (CAIPO).

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated | No separate legal personality from the owner |

| Owner Reference | Sole Proprietor | Single individual; no concept of shareholders or directors |

| Liability | Unlimited personal liability | Personal assets at risk for all business debts |

| Registration Body | CAIPO | Required when trading under a name other than the proprietor's legal name |

| Local Presence | Physical address required | No registered agent requirement |

| Capital | No minimum | No statutory capital requirement |

Focus Points

- Taxation: Subject to personal income tax in Barbados; VAT registration is required once annual taxable supplies exceed the statutory threshold; no corporate tax applies.

- Annual Compliance: No annual return filing with CAIPO; income declared via personal tax return with the Barbados Revenue Authority.

- Conversion: Can convert to a company under the Companies Act, Cap. 308, though this requires full incorporation as a new entity.

- Treaty Access: Cannot access Barbados's double taxation agreements, which are available only to corporate entities.

- Restrictions: Cannot employ staff under a separate employer identity; contracts and obligations bind the proprietor personally.

Closing

A sole trader structure suits early-stage or low-risk domestic service providers where simplicity outweighs the need for liability protection. The absence of incorporation formalities reduces setup costs, though unlimited personal liability remains a material exposure.

Local freelancers, consultants, and micro-businesses operating with minimal financial risk and no immediate plans to scale or take on external liability.

How to Choose the Right Entity Type in Barbados

Selecting the wrong structure from the outset creates concrete legal, tax, and operational problems that can be difficult and costly to unwind.

Why Your Entity Choice Matters

- Registering an offshore entity such as an IBC while conducting trade with Barbados residents places the business in breach of the applicable act, which can result in penalties or striking off by the Registrar of Corporate Affairs.

- A tax-exempt entity cannot access Barbados's double taxation treaties. If your structure depends on reduced withholding tax rates in counterpart jurisdictions, exemption status defeats that purpose.

- Choosing a company structure when your objectives are estate planning or succession locks you into annual general meeting obligations and shareholder formalities that would not apply under alternative arrangements such as a trust or foundation.

- Selecting an entity that requires audited financial statements — such as a public company — for a single-person consultancy adds recurring professional fees that would not apply to a private company or sole trader structure.

Key Factors to Consider

- Business Activity: Passive asset holding, active trading, and regulated sectors such as insurance each fall under distinct statutes and point toward different structures.

- Local vs. Offshore Operations: Entities intended to transact with Barbados residents must be structured and licensed accordingly, as offshore vehicles are prohibited from doing so.

- Tax Objectives: Whether you require full tax exemption, access to the treaty network, or eligibility under the Income Tax Act, Cap. 73 determines which regime applies.

- Ownership and Management: A single-member operation may be served by a sole trader or SRL, while multi-party ventures requiring defined governance point toward a company under the Companies Act, Cap. 308.

- Substance Capacity: If you cannot realistically maintain employees, a registered office with genuine activity, or local decision-making, confirm whether your chosen entity type carries substance requirements under the Income Tax (Substance Requirements) (Amendment) Act, 2020.

- Exit Strategy: Not all structures permit redomiciliation or conversion; confirm whether the entity type allows those options before formation.

Compliance Services for Companies in Barbados

Ongoing corporate compliance support for Barbados-registered entities, including annual filings, registered agent services, and regulatory reporting.

Conclusion

Barbados company incorporation summary reflects a framework built across multiple statutes, each designed with a distinct commercial purpose. The private company limited by shares, incorporated under the Companies Act, Cap. 308, remains the most commonly registered structure for resident and foreign-owned operating businesses. The public company suits enterprises seeking public capital markets access, while the company limited by guarantee serves non-commercial or membership-based organisations. Unlimited liability companies are rare, suited to specific intra-group arrangements. The Society with Restricted Liability, governed by Cap. 318B, offers pass-through tax treatment for joint ventures. External company registration provides foreign firms a presence without a separate legal entity.

Barbados continues to expand its network of tax information exchange agreements and double taxation treaties, reinforcing its position as a mid-shore jurisdiction with substantive regulatory expectations. For businesses with cross-border structures, entity selection has direct consequences for treaty access and compliance obligations under the Barbados Revenue Authority.

How Expanship Can Assist You

Expanship's Barbados company formation services cover the full range of structures discussed in this guide — from private and public companies incorporated under the Companies Act, Cap. 308, to Societies with Restricted Liability and entities registered under specialist legislation. Your filing goes through the Corporate Affairs and Intellectual Property Office (CAIPO), and our team coordinates that process directly on your behalf.

From initial registration through to ongoing compliance, here is what Expanship handles for your business:

- Document preparation and notarization or apostille where required

- Registered agent and registered office provision in Barbados

- Government filings and liaison with CAIPO and relevant licensing authorities

- Post-incorporation compliance management, including annual returns

- Banking introduction assistance with local and international financial institutions

To discuss your specific requirements, contact Expanship Barbados directly and we will advise on the most appropriate path forward for your entity.

Frequently Asked Questions (FAQ)

The private company limited by shares, incorporated under the Companies Act, Cap. 308, remains the most frequently registered entity. Its flexible shareholding structure and relatively straightforward compliance requirements make it suitable for a broad range of commercial activities.

An IBC, governed by the International Business Companies Act, is restricted from trading with Barbados residents and historically attracted preferential tax treatment, while a private company under Cap. 308 can conduct business domestically and is subject to standard corporate tax rates. Compliance obligations also differ: IBCs face specific annual filing requirements with the Registrar of Corporate Affairs, whereas private companies operate under the broader Companies Act framework.

The Society with Restricted Liability, established under the Societies with Restricted Liability Act, Cap. 318B, provides a notable degree of privacy, as member details are not routinely exposed through public filings. Nominee arrangements are generally available under Barbadian practice, though ultimate beneficial ownership disclosure obligations apply under anti-money laundering legislation.

A sole individual can form a private company limited by shares, an unlimited liability company, and a company limited by guarantee under the Companies Act. General and limited partnerships, by contrast, require a minimum of two partners, and the Society with Restricted Liability requires at least two members under Cap. 318B.

Non-resident individuals and foreign corporations may incorporate or register across most entity types, including private companies, IBCs, and Societies with Restricted Liability, without a local shareholder requirement. Foreign nationals operating certain regulated structures, such as exempt insurance companies under the Exempt Insurance Act, Cap. 308A, must satisfy the Financial Services Commission's licensing criteria.

The Companies Act, Cap. 308 provides mechanisms for continuation and conversion, allowing a company to change its structure or migrate from a foreign jurisdiction into Barbados. Conversion between a private company and an unlimited liability company is permissible, subject to shareholder approval and filing with the Registrar of Corporate Affairs.

Companies incorporated under Cap. 308, IBCs, and Societies with Restricted Liability each hold legal personality distinct from their members. General partnerships do not, meaning partners bear personal liability for firm obligations without the protection of a corporate shield.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.