Key Takeaways

- Bosnia and Herzegovina's dual-entity federal structure means company registration procedures can differ depending on whether a business incorporates under the Federation of Bosnia and Herzegovina, Republika Srpska (overseen by APIF), or the Brčko District.

- The Društvo s Ograničenom Odgovornošću (D.O.O.) is the most commonly registered entity in Bosnia and Herzegovina, favored by small and medium-sized businesses for its lower capital requirements and simplified governance structure.

- Foreign companies seeking a presence in Bosnia and Herzegovina without establishing a separate legal entity can operate through either a branch office or a representative office, each carrying distinct operational limitations.

- Ongoing EU accession efforts are gradually aligning Bosnia and Herzegovina's regulatory framework with European standards, with implications for compliance obligations affecting all registered business structures over time.

Introduction to Entity Types in Bosnia and Herzegovina

Bosnia and Herzegovina is a sovereign state in southeastern Europe, bordered by Croatia, Serbia, and Montenegro, with a narrow coastal strip on the Adriatic Sea. The country operates under a complex federal structure, divided into two main entities — the Federation of Bosnia and Herzegovina and Republika Srpska — along with the Brčko District, each maintaining its own legal and administrative framework.

Company registration is administered through the relevant cantonal or entity-level courts, with oversight from bodies such as the Agency for Intermediary, IT and Financial Services (APIF) in Republika Srpska and equivalent authorities in the Federation. This jurisdictional split means that business entity types in Bosnia and Herzegovina, while broadly defined by federal commercial law, may differ slightly in registration procedure depending on where the company is registered.

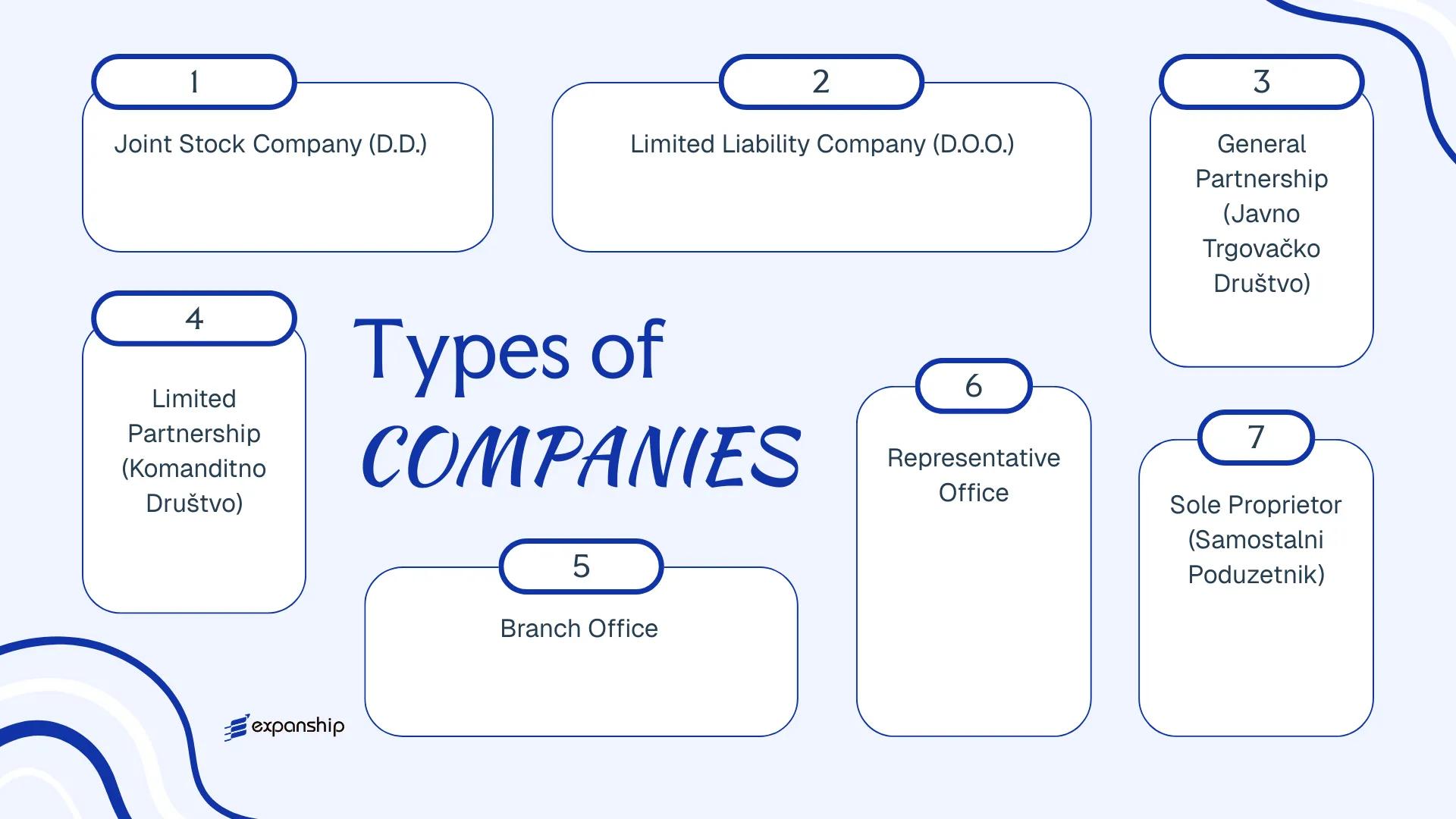

The general tax posture is low-rate, with a flat corporate income tax applied nationally. Available corporate forms include the Dioničko Društvo (D.D.), Društvo s Ograničenom Odgovornošću (D.O.O.), Javno Trgovačko Društvo, Komanditno Društvo, branch offices, representative offices, and the Samostalni Poduzetnik. Each structure carries distinct liability, capital, and governance implications that this article examines in turn.

An Overview of Business Structures in Bosnia and Herzegovina

Bosnia and Herzegovina recognises several distinct entity types under its corporate legal framework, primarily governed by the Law on Enterprises (Zakon o preduzećima), with parallel legislation at the entity level across the Federation of Bosnia and Herzegovina (FBiH) and Republika Srpska (RS). Registration and oversight fall under the competence of the relevant entity-level courts and, where applicable, the Brcko District authorities. Each business structure carries different implications for liability, governance, and operational scope.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Dioničko Društvo (D.D.) | Joint Stock Company | Limited to share capital | Taxed | Yes | 1 founder | Entity-level court registry | Law on Enterprises (FBiH / RS) |

| Društvo s Ograničenom Odgovornošću (D.O.O.) | Limited Liability Company | Limited to capital contribution | Taxed | Yes | 1 member | Entity-level court registry | Law on Enterprises (FBiH / RS) |

| Javno Trgovačko Društvo | General Partnership | Unlimited, joint | Taxed | Yes | 2 partners | Entity-level court registry | Law on Enterprises (FBiH / RS) |

| Komanditno Društvo | Limited Partnership | Mixed (general / limited) | Taxed | Yes | 2 partners | Entity-level court registry | Law on Enterprises (FBiH / RS) |

| Branch Office | Non-legal entity | Parent company liable | Taxed on local income | Yes | N/A (parent required) | Entity-level court registry | Law on Enterprises (FBiH / RS) |

| Representative Office | Non-legal entity | Parent company liable | Generally exempt | No (liaison only) | N/A (parent required) | Entity-level court registry | Law on Enterprises (FBiH / RS) |

| Samostalni Poduzetnik | Sole Proprietorship | Unlimited, personal | Taxed | Yes | 1 individual | Municipal / entity registry | Law on Enterprises (FBiH / RS) |

Each of these structures is examined in full in the sections below.

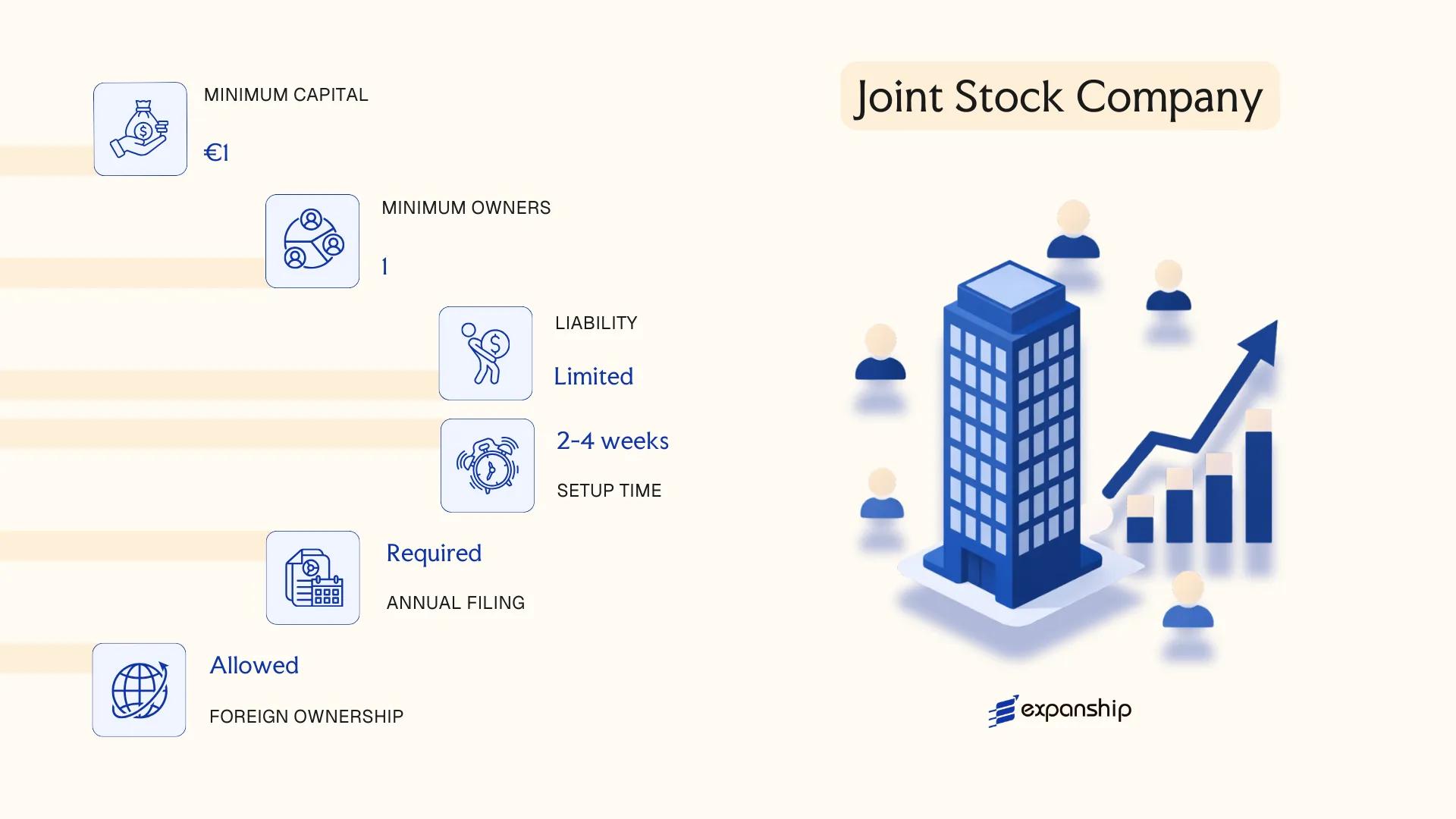

Dioničko Društvo (D.D.) — Joint Stock Company

The Dioničko Društvo DD joint stock company Bosnia is governed by the Law on Companies of the Federation of Bosnia and Herzegovina (FBiH) or its counterpart in Republika Srpska, depending on the entity in which the firm is registered. This structure carries separate legal personality, meaning the company's obligations are distinct from those of its shareholders.

Liability is limited to each shareholder's subscribed capital contribution. The D.D. is the only business form in BiH that can issue publicly traded shares, making it structurally suited to large-scale capital raising and institutional investment.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Dioničko Društvo (D.D.) | Recognized in both FBiH and Republika Srpska |

| Members | Shareholders; minimum 1 founder | No statutory maximum on shareholders; founder may be a natural or legal person |

| Management | Supervisory Board + Management Board (two-tier) | Supervisory Board oversees Management Board; both required for larger entities |

| Local Presence | Registered seat in the relevant entity (FBiH or RS) | Physical registered address required; no mandatory local director rule, but local registered address is obligatory |

| Share Capital | Minimum BAM 50,000 (approx. EUR 25,000); paid-up at registration | Shares may be ordinary or preference; public D.D. subject to Securities Commission oversight |

| Privacy | Shareholder register is maintained; beneficial ownership disclosure required | Registers accessible to authorities; not fully public in all cantons |

Focus Points

- Taxation: Corporate income tax is levied at 10% flat rate, one of the lower rates in the region; VAT applies at 17% where turnover exceeds the registration threshold; withholding tax on dividends, interest, and royalties paid to non-residents is generally 5–10% depending on applicable double taxation treaty.

- Annual Compliance: Mandatory financial statement submission, annual shareholders' assembly, and audit requirements apply once the entity meets prescribed size thresholds.

- Treaty Access: BiH has an active network of double taxation agreements; a D.D. with genuine substance qualifies for treaty benefits, though substance requirements are assessed case by case.

- Conversion: A D.D. may be converted into a D.O.O. or another recognized form through a formal restructuring procedure under company law, subject to creditor notification.

- Securities Regulation: A publicly listed D.D. falls under the jurisdiction of the Securities Commission of the Federation of BiH (Komisija za vrijednosne papire FBiH) or its Republika Srpska equivalent, adding a regulatory layer absent in private structures.

Sub-Types

Zatvoreno Dioničko Društvo (Closed Joint Stock Company)

Shares are not offered to the public and transfers are subject to restrictions defined in the founding act. This form is used by private groups seeking the corporate structure of a D.D. without public market obligations.

Otvoreno Dioničko Društvo (Open Joint Stock Company)

Shares may be offered publicly and the entity is subject to continuous disclosure and Securities Commission supervision. Firms intending to list on the Sarajevo or Banja Luka Stock Exchange must adopt this form.

When to Use a D.D.

The D.D. suits businesses planning to raise capital from multiple investors or access public equity markets, as well as holding structures where share transferability matters. The primary advantage is unrestricted share issuance and the ability to attract institutional investors. The clear limitation is administrative burden: two-tier governance, mandatory audits, and, for open companies, ongoing securities regulation compliance significantly increase operating costs.

Best suited for large enterprises, joint ventures with multiple institutional shareholders, or businesses with a clear path to public listing in BiH.

Company Incorporation in Bosnia and Herzegovina

Expanship assists with D.D. formation across both FBiH and Republika Srpska, including registered address, document preparation, and regulatory filing.

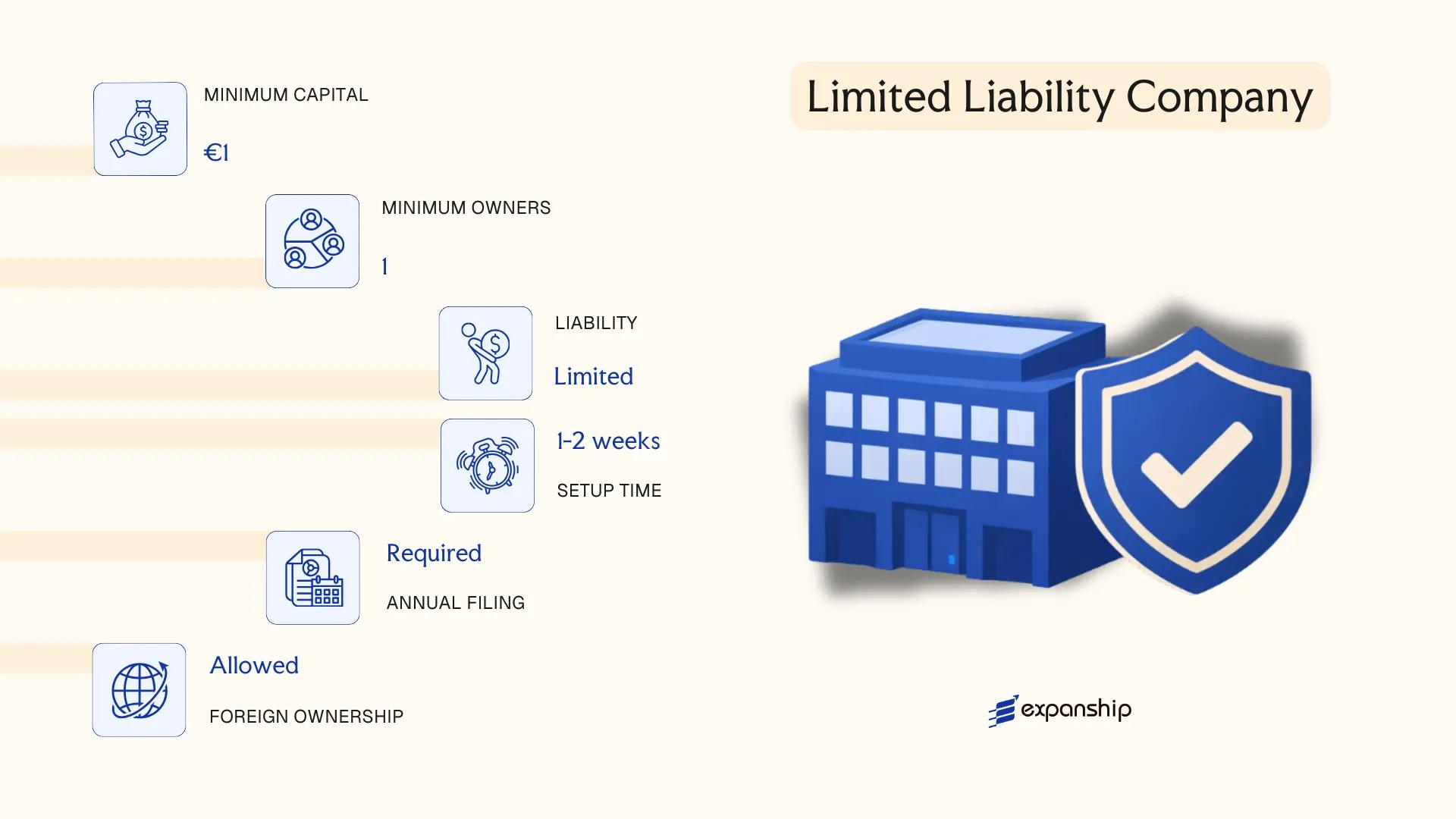

Društvo s Ograničenom Odgovornošću (D.O.O.) — Limited Liability Company

The Društvo s Ograničenom Odgovornošću DOO Bosnia is governed primarily by the Law on Business Companies, with parallel legislation enacted at the entity level across the Federation of Bosnia and Herzegovina and Republika Srpska. Registration is conducted through the relevant entity-level court registry, as no single federal commercial registry exists.

A D.O.O. carries separate legal personality, meaning the company holds rights and obligations independently of its members. Liability is confined to the amount of each member's capital contribution, making this a hybrid structure that combines corporate liability protection with relatively flexible internal governance.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Company | Separate legal personality; liability limited to subscribed capital |

| Members | 1 to 50 members | Members hold ownership interests (udjeli), not shares |

| Management | One or more managers (direktori) | No supervisory board required unless stipulated in the articles |

| Registered Office | Physical address within the relevant entity (FBiH or RS) | Virtual offices may not satisfy registration requirements |

| Minimum Capital | BAM 1,000 (approx. EUR 500) | Must be deposited prior to registration |

| Privacy | Member details filed in the court registry | Registry records are generally publicly accessible |

Focus Points

- Taxation: Corporate income tax applies at 10%; VAT registration is required once turnover exceeds BAM 50,000; withholding tax on dividends, interest, and royalties paid to non-residents is generally 5–10% depending on applicable treaties.

- Annual Compliance: Firms must submit audited or unaudited financial statements annually to the relevant tax authority and registry.

- Treaty Access: Bosnia and Herzegovina maintains a network of double tax treaties; a D.O.O. qualifies as a resident entity for treaty purposes.

- Restrictions: Member count is capped at 50; exceeding this threshold requires conversion to a D.D.

Closing

A D.O.O. suits trading operations, holding structures, and service businesses requiring limited liability without the administrative burden of a joint stock company. The low capital threshold eases entry, though the 50-member ceiling limits its use for businesses anticipating broad equity participation.

Small to mid-sized businesses, foreign investors establishing an operational subsidiary, and entrepreneurs seeking a straightforward liability-protected structure in Bosnia and Herzegovina.

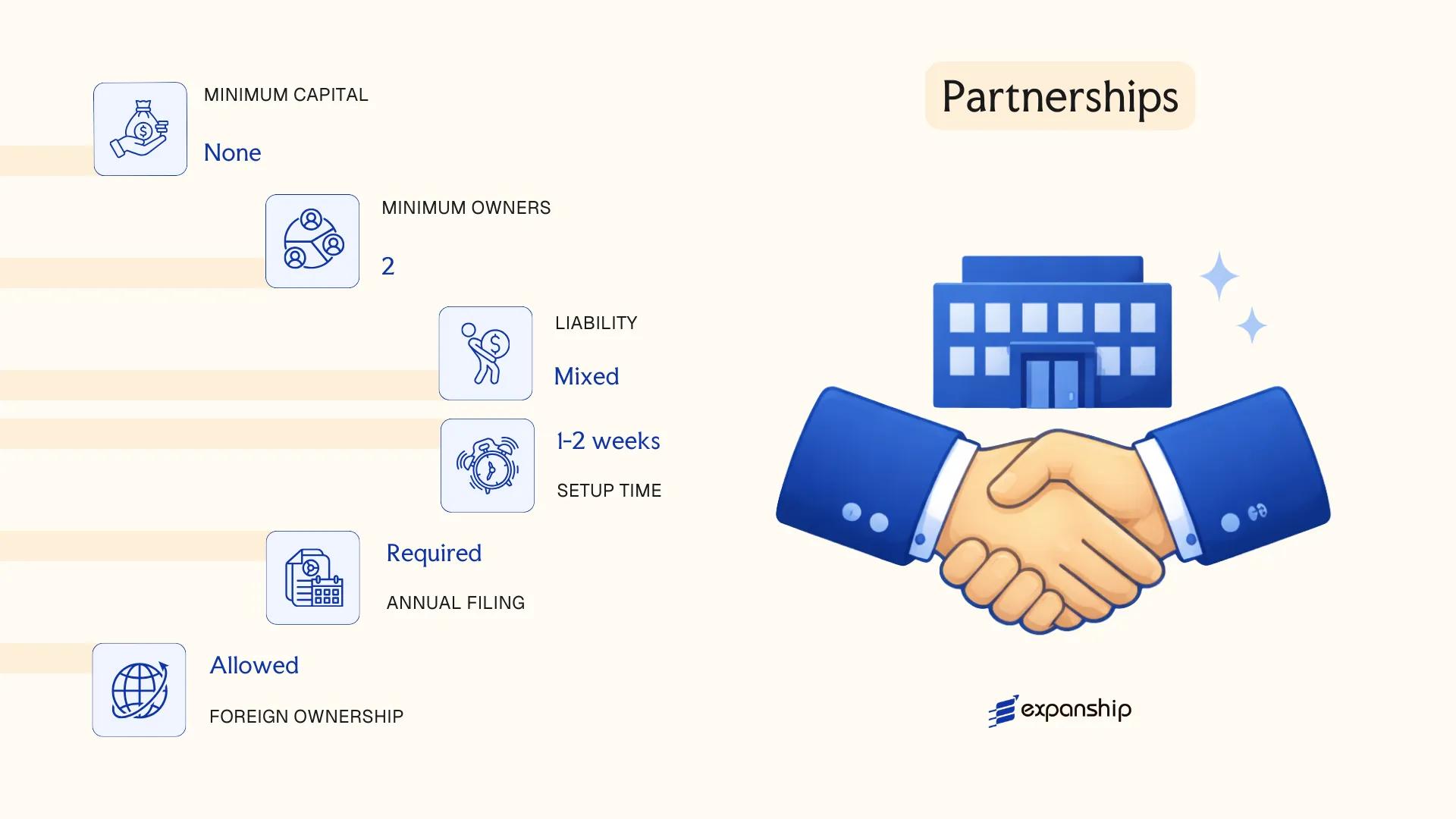

Partnerships in Bosnia and Herzegovina [Javno Trgovačko Društvo (General Partnership), Komanditno Društvo (Limited Partnership)]

Partnership company registration Bosnia Herzegovina falls under the Law on Companies of the Federation of Bosnia and Herzegovina (FBiH) and the corresponding Law on Companies of Republika Srpska, depending on the entity's registered location. Both frameworks recognise two distinct partnership structures: the Javno Trgovačko Društvo (JTD), or general partnership, and the Komanditno Društvo (KD), or limited partnership.

Unlike capital companies, neither structure requires a minimum share capital contribution at formation. Partners in a JTD bear unlimited joint and several liability for the firm's obligations, while a KD introduces a two-tier membership model that separates liability exposure between partner classes.

Key Characteristics

| Requirement | JTD (General Partnership) | KD (Limited Partnership) |

|---|---|---|

| Legal Form | Separate legal entity; unlimited liability for all partners | Separate legal entity; mixed liability structure |

| Members | Partners (minimum 2, no maximum; all bear unlimited liability) | General partners (min. 1, unlimited liability) + limited partners (min. 1, liability capped at contribution) |

| Local Presence | Registered office required in the relevant entity (FBiH or RS) | Registered office required in the relevant entity (FBiH or RS) |

| Capital | No statutory minimum; contributions recorded in partnership agreement | No statutory minimum; limited partner's liability tied to agreed contribution amount |

| Privacy | Partner names appear in the business register (public record) | Both general and limited partner names are publicly registered |

Focus Points

- Taxation: Both structures are subject to the corporate income tax rate of 10% in FBiH and RS; partners may also face personal income tax on distributed profits, and the standard VAT rate of 17% applies to taxable supplies.

- Annual Compliance: Partnerships must file annual financial statements with the relevant entity-level tax authority and maintain accounting records in accordance with applicable accounting laws.

- Economic Substance: No formal economic substance regime applies, but a functional registered office and legitimate operational presence are required under registration rules.

- Conversion: Both JTD and KD can generally be converted into a capital company (D.O.O. or D.D.) through a formal restructuring procedure under the applicable Law on Companies.

- Restrictions: Foreign nationals may participate as partners, but at least one general partner in a KD bears unlimited personal liability, which requires careful consideration in cross-border structures.

Sub-Types

Javno Trgovačko Društvo (JTD) — General Partnership

All partners hold equal management rights by default and carry unlimited, joint liability for partnership debts. This structure suits small professional firms or family-owned businesses where trust between partners is established and formal capital separation is unnecessary.

Komanditno Društvo (KD) — Limited Partnership

The KD distinguishes between general partners, who manage the business and bear unlimited liability, and limited partners, whose liability is confined to their agreed contribution. This arrangement is commonly used where passive investors wish to participate in a venture without assuming full personal liability.

Closing

Both structures are most suited to small-scale domestic trading operations or professional service arrangements where the partners have a pre-existing relationship and formalised capital structures are not required. The absence of a minimum capital requirement lowers the barrier to formation, though unlimited liability for general partners represents a significant personal financial exposure.

Partnerships in Bosnia and Herzegovina are most appropriate for small domestic businesses or professional firms where two or more individuals seek a straightforward operational structure without the administrative overhead of a capital company.

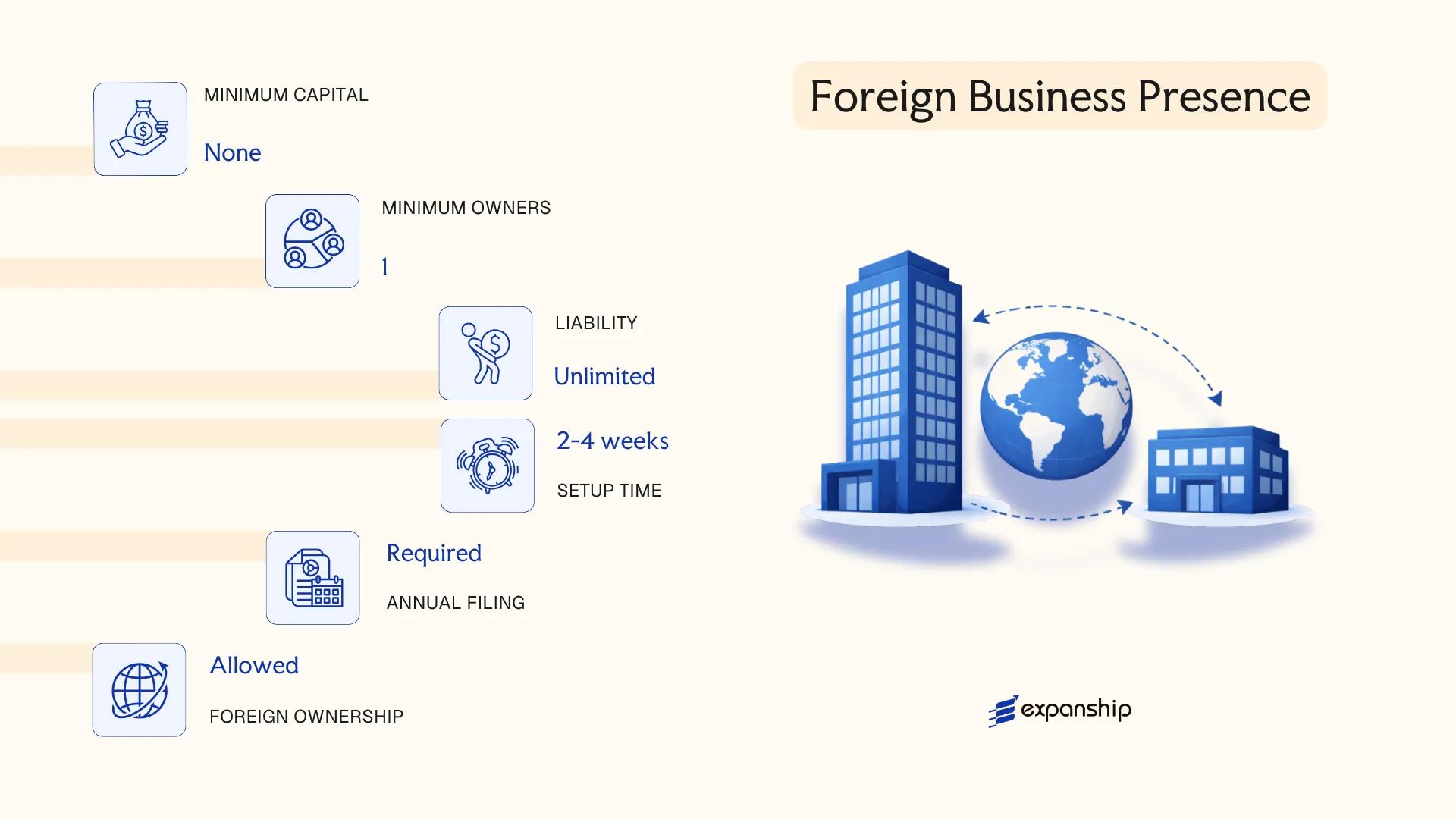

Foreign Business Presence in Bosnia and Herzegovina [Branch Office, Representative Office]

A foreign company branch office Bosnia Herzegovina operates under the Law on Registration of Business Entities, which governs how foreign firms establish a registered presence without forming a separate legal entity. A branch office is an extension of the parent company — it carries no independent legal personality and the parent bears full liability for its activities.

A representative office differs in scope. Registered under the same framework, it is restricted to non-commercial activities such as market research, liaison, and promotional work. Neither structure can issue shares or accumulate equity, but each provides a regulated path to operating on the ground before committing to full incorporation.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Personality | None — extension of parent | None — extension of parent |

| Commercial Activity | Permitted | Not permitted |

| Registration Body | Entity Registration Agency (APIF in FBiH; APRS in RS) | Entity Registration Agency (APIF in FBiH; APRS in RS) |

| Local Representative | Required (natural person resident in BiH) | Required (natural person resident in BiH) |

| Registered Address | Mandatory local address | Mandatory local address |

| Minimum Capital | No statutory minimum | No statutory minimum |

| Parent Liability | Unlimited | Unlimited |

Focus Points

- Taxation: Branch profits are subject to corporate income tax at 10%; VAT registration is required if turnover exceeds the statutory threshold; representative offices, being non-commercial, generally fall outside VAT and CIT scope but should confirm with the Tax Administration.

- Annual compliance: Both structures must file annual financial statements with the relevant entity-level registration agency.

- Treaty access: Access to Bosnia and Herzegovina's double tax treaties depends on the parent company's residence; the branch itself is not a treaty resident.

- Restrictions: A representative office cannot conclude commercial contracts, invoice clients, or generate revenue directly.

- Conversion: Neither structure can be converted directly into a D.O.O. or D.D. — a separate incorporation process is required.

Sub-Types

Branch Office (Podružnica)

Registered as a dependent unit of the foreign parent, a branch can conduct full trading operations, enter contracts, and employ staff locally. It is the appropriate structure when the foreign firm intends to generate revenue before committing to a subsidiary.

Representative Office (Predstavništvo)

Limited strictly to preparatory and auxiliary functions, this structure suits firms conducting due diligence, building supplier relationships, or assessing the market prior to a commercial commitment.

Closing

A branch office suits foreign firms that need an operational footprint quickly without the governance overhead of a subsidiary, while a representative office is appropriate for preliminary market engagement with no commercial transactions involved. The primary drawback of both is the absence of limited liability protection at the local level — the parent remains exposed for all obligations.

Both structures are best suited to established foreign companies testing or entering the Bosnian market before committing to a locally incorporated entity.

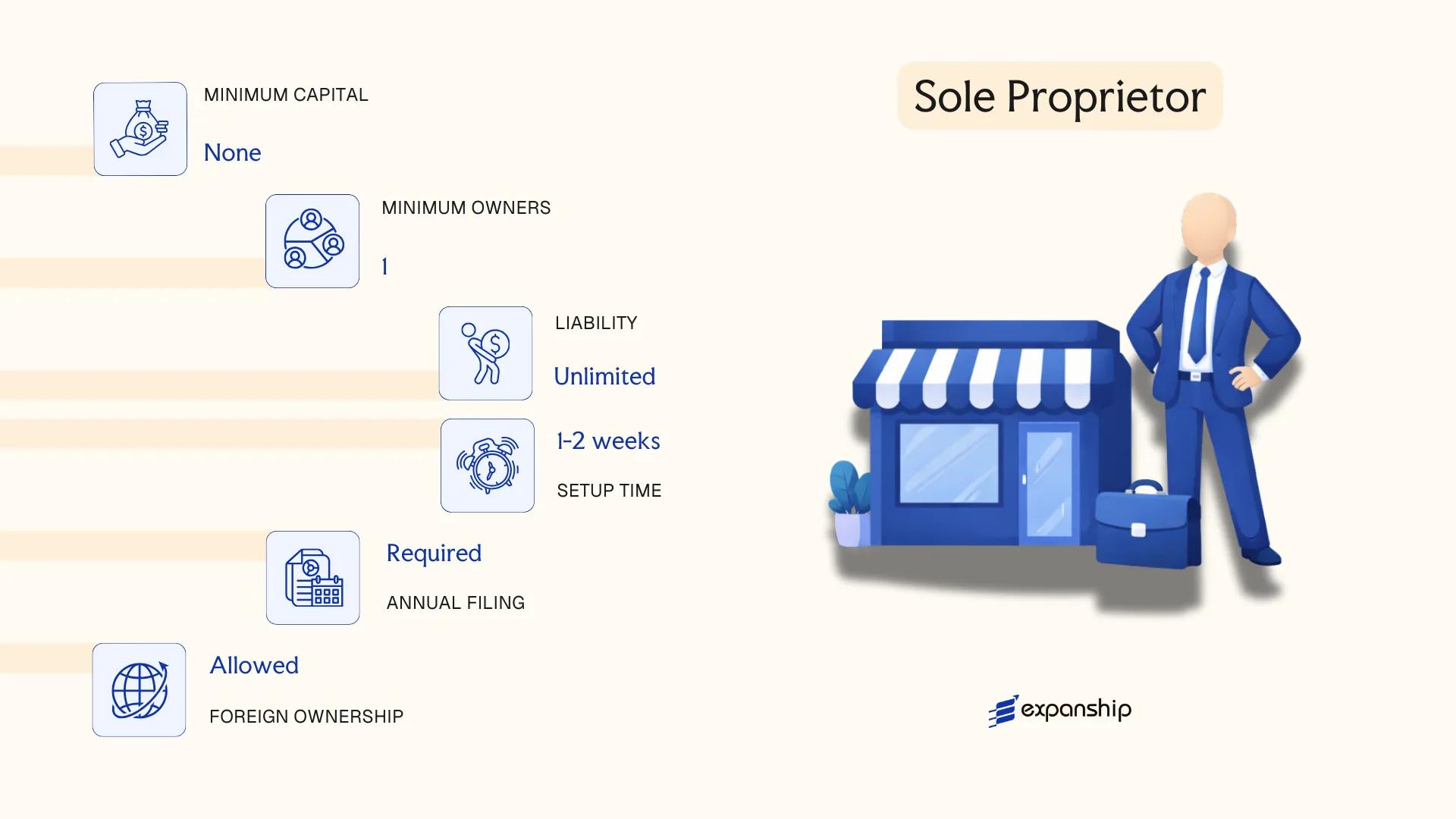

Sole Proprietor (Samostalni Poduzetnik)

Registered as a samostalni poduzetnik (sole proprietor Bosnia), this business form is the simplest structure available to individuals conducting commercial activity. Unlike a D.O.O. or D.D., a sole proprietorship does not create a separate legal entity — the individual and the business are legally one. Registration is handled through the relevant cantonal or entity-level court registry, depending on whether the proprietor operates in the Federation of Bosnia and Herzegovina, Republika Srpska, or Brčko District.

The governing framework differs across the two entities: in the Federation, the Law on Enterprises applies alongside cantonal regulations, while Republika Srpska maintains its own Law on Entrepreneurs. Self-employment registration in Bosnia Herzegovina is relatively straightforward, though the proprietor assumes unlimited personal liability for all business obligations.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole Proprietorship | No separate legal personality; owner and business are legally identical |

| Members | Single individual proprietor | No minimum capital requirement |

| Local Presence | Registered business address required | Must correspond to actual place of business |

| Liability | Unlimited personal liability | Personal assets are exposed to business creditors |

| Capital | No statutory minimum | No currency restriction imposed |

| Privacy | Owner's details publicly registered | Full transparency required in registry filings |

Focus Points

- Taxation: Subject to personal income tax on business profit; VAT registration mandatory once annual turnover exceeds the statutory threshold; no separate corporate tax applies.

- Annual Compliance: Annual financial reporting required; bookkeeping obligations apply under applicable accounting regulations.

- Conversion: Can be converted into a D.O.O. upon meeting registration requirements, though the process involves forming a new legal entity.

- Treaty Access: As an unincorporated individual business, access to double tax treaties may be limited compared to incorporated entities.

- Restrictions: Cannot issue shares or admit partners; unsuitable for businesses requiring external equity investment.

Closing

Sole trader BiH registration suits local service providers, freelancers, and small-scale traders operating with low capital requirements and limited organisational complexity. The primary advantage is minimal administrative overhead; the central drawback is unlimited personal liability, which exposes the proprietor's private assets to full business risk.

Best suited for resident individuals conducting low-risk, single-person commercial or professional activity within Bosnia and Herzegovina.

How to Choose the Right Entity Type in Bosnia and Herzegovina

Selecting how to choose a business entity type in Bosnia Herzegovina is not a procedural formality — the wrong choice produces concrete legal and financial consequences that are difficult to reverse.

Why Your Entity Choice Matters

- Operating through a foreign entity while conducting day-to-day commercial activity locally may constitute unlicensed business activity under the applicable cantonal or entity-level trade laws, exposing the firm to administrative penalties or forced deregistration.

- Registering a structure that lacks access to Bosnia and Herzegovina's double taxation agreements means withholding tax reductions available under those treaties cannot be claimed by counterpart parties.

- Choosing a D.D. when your business is a single-person consultancy imposes mandatory audit requirements and supervisory board obligations that generate annual costs disproportionate to the firm's size.

- Forming a general partnership without limiting liability locks all partners into unlimited personal exposure for business debts — an outcome that cannot be restructured without dissolving and re-registering the entity.

Key Factors to Consider

- Business Activity: Active trading, passive asset-holding, and regulated sectors such as banking or insurance each require a structurally distinct entity under BiH law.

- Ownership Structure: A sole owner generally favours a D.O.O., while multi-party arrangements with transferable capital interests point toward a D.D.

- Tax Objectives: Your need for treaty access, a specific tax rate, or VAT registration eligibility should be confirmed against the Law on Corporate Profit Tax before registration.

- Management Flexibility: Partnerships permit contractual management arrangements, whereas a D.D. mandates a defined board structure under the Companies Law of the Federation or Republika Srpska.

- Substance Capacity: If you cannot maintain a physical office and resident staff, a representative office — which is prohibited from generating revenue — may be the only compliant option.

- Exit Strategy: Not all BiH entity types permit redomiciliation or conversion; winding-up procedures vary in duration and cost depending on the structure chosen.

Compliance Services for Companies in Bosnia and Herzegovina

Ongoing compliance support for BiH-registered entities, covering annual filings, statutory reporting, and regulatory obligations across all three jurisdictions within the country.

Conclusion

Incorporating a company in Bosnia Herzegovina means selecting from a defined set of legal structures, each suited to a distinct operational profile. The D.O.O. is the most registered entity in the country, preferred by small and medium-sized businesses for its lower capital threshold and simpler governance. The D.D. suits larger enterprises requiring public capital access. General and limited partnerships serve closely held ventures where personal relationships underpin the business arrangement. Branch and representative offices give foreign firms a controlled entry point without establishing a separate legal entity. The Sole Proprietor structure fits individuals operating at minimal scale with direct personal liability.

Bosnia and Herzegovina continues to expand its network of bilateral investment and double taxation treaties, gradually broadening its appeal to foreign investors. Regulatory alignment with EU standards remains an ongoing process tied to the country's accession path, which will shape compliance obligations for registered businesses over time. Expanship's team works directly with this framework to assist clients through each stage of the setup process.

How Expanship Can Assist You

Expanship provides corporate services in Bosnia and Herzegovina across both the Federation BiH and Republika Srpska entities, covering every structure discussed in this guide — from a D.O.O. to a D.D. or branch office. Registration filings go through the relevant cantonal or entity-level court registries, and maintaining good standing requires ongoing engagement with the Tax Administration of the Federation of BiH or the RS Tax Administration, depending on where your business operates. Our company registration assistance in BiH accounts for these jurisdictional distinctions from the outset.

Our team handles the full incorporation cycle and what comes after it:

- Document preparation, notarization, and legalization

- Registered agent and registered office provision

- Filing and liaison with the competent court registry

- Post-incorporation compliance and annual reporting support

- Banking introduction assistance for local account opening

Reach out to Expanship Bosnia Herzegovina to discuss your entity setup requirements directly.

Frequently Asked Questions (FAQ)

The Društvo s Ograničenom Odgovornošću (D.O.O.) is the most frequently registered entity, largely because it requires a minimum share capital of 1,000 BAM and places no restriction on the number of shareholders. Its straightforward registration process under the Law on Enterprises makes it accessible to both domestic founders and foreign investors.

Both entity types can conduct business locally, but a Dioničko Društvo (D.D.) carries significantly heavier compliance obligations, including mandatory audits and a supervisory board once thresholds are met. The D.D. is structured for larger enterprises or those seeking public capital, while a D.O.O. suits closely held businesses with simpler governance needs.

A sole individual can form a D.O.O. or D.D., but general partnerships (Javno Trgovačko Društvo) and limited partnerships (Komanditno Društvo) each require a minimum of two partners by statute. A Sole Proprietor (Samostalni Poduzetnik) registration is also available to one person acting in their own name.

Foreign nationals may register a D.O.O., D.D., or establish a branch office without restrictions tied to citizenship. Bosnia and Herzegovina imposes no nationality requirement on shareholders or directors under the general company registration framework.

Conversion between entity types is generally permitted under the Law on Enterprises, with the D.O.O.-to-D.D. transition being the most procedurally documented path. The process requires a decision by the existing owners, updated founding documentation, and re-registration with the relevant entity registry.

A D.O.O., D.D., and both partnership forms hold separate legal personality upon registration. A Representative Office does not, as it remains an extension of the foreign parent company and cannot enter contracts or generate revenue in its own right.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.