Key Takeaways

- The Limited Liability Company is the dominant registration choice in Azerbaijan, governed by the Civil Code and the Law on Limited Liability Companies, making it the preferred structure for both foreign investors and domestic operators.

- Azerbaijan recognizes nine distinct business entity types, each with differentiated liability, governance, and capital requirements, all registered through the Ministry of Economy's State Register of Legal Entities.

- Branch offices and representative offices diverge fundamentally in function: branch offices carry the parent entity's legal identity and can conduct commercial activity, while representative offices are restricted to non-commercial operations.

- Open Joint Stock Companies, Closed Joint Stock Companies, and Additional Liability Companies serve narrower use cases — public capital access, closed investor groups, and extended personal liability respectively — compared to the more broadly applicable LLC structure.

Introduction to Entity Types in Azerbaijan

Located in the South Caucasus, Azerbaijan borders Russia, Georgia, Armenia, Iran, and the Caspian Sea — positioning it as a transit and trade corridor between Europe and Central Asia. It is an independent republic and a member of the Commonwealth of Independent States (CIS), with a mixed economy that has diversified beyond hydrocarbons in recent years.

Company registration falls under the jurisdiction of the Ministry of Economy of the Republic of Azerbaijan, which oversees the State Register of Legal Entities. All types of business entities in Azerbaijan must be registered through this body before commencing operations. The tax framework is treaty-based, with Azerbaijan maintaining a network of double taxation agreements alongside a standard corporate income tax rate applied to resident entities.

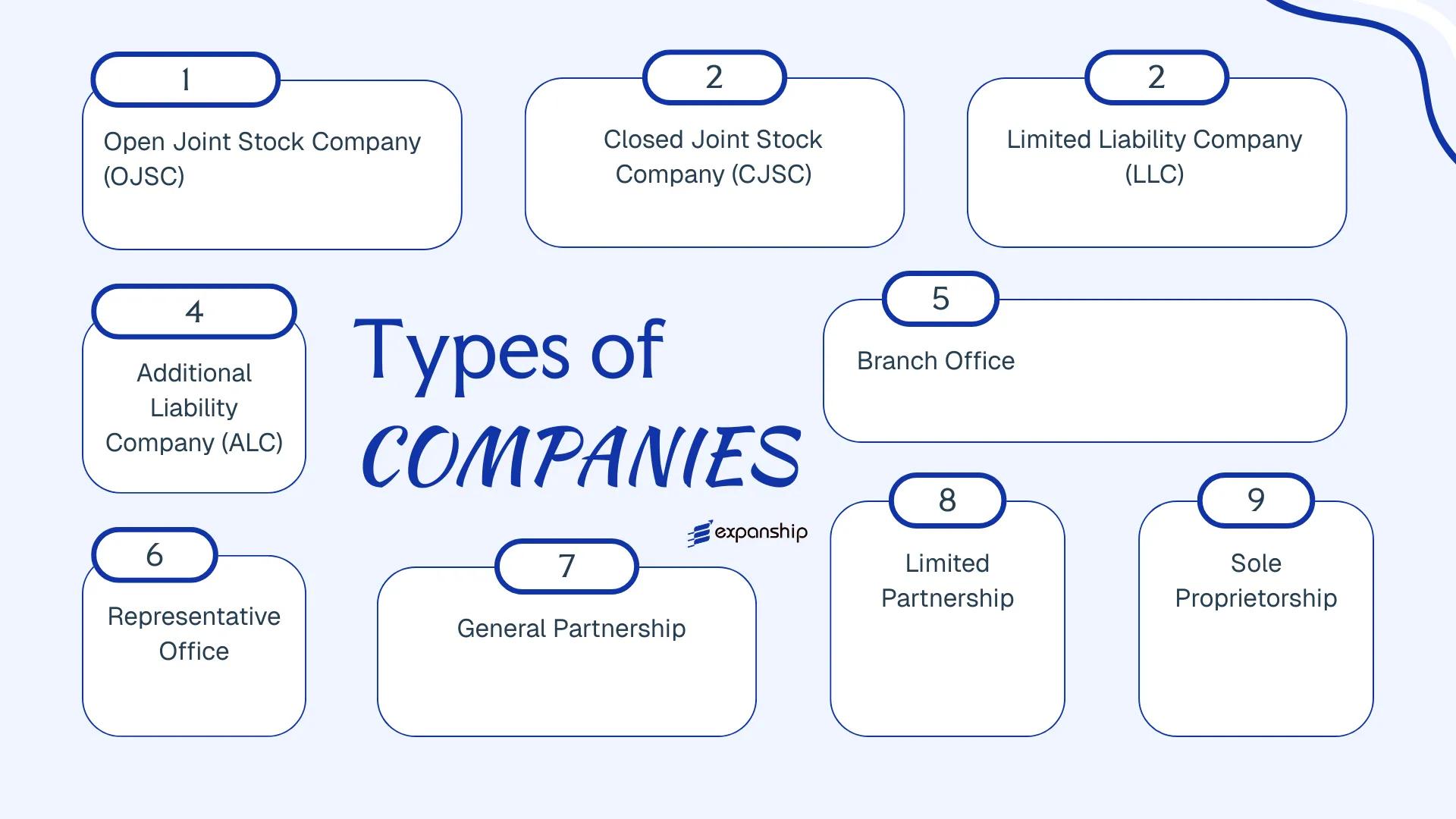

Azerbaijani legal entity types span a range of structures suited to both domestic operators and foreign investors. Available forms include the Open Joint Stock Company, Closed Joint Stock Company, Limited Liability Company, Additional Liability Company, General Partnership, Limited Partnership, Sole Proprietorship, Branch Office, and Representative Office. Each of these business structures in Azerbaijan carries distinct liability, governance, and capital requirements, all of which this article examines in detail.

An Overview of Business Structures in Azerbaijan

Azerbaijan business structure overview begins with the Civil Code of the Republic of Azerbaijan and the Law on Commercial Legal Entities (No. 560-IQ, 1996), which together define the recognised forms of business organisation available to both local and foreign investors. Seven distinct entity types fall under this framework, each designed to meet different ownership, liability, and operational requirements.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Tax Status | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Open Joint Stock Company (OJSC) | Corporate | Limited to shares | Taxable | Yes | 1 shareholder | Ministry of Justice | Law on Commercial Legal Entities |

| Closed Joint Stock Company (CJSC) | Corporate | Limited to shares | Taxable | Yes | 1–50 shareholders | Ministry of Justice | Law on Commercial Legal Entities |

| Limited Liability Company (LLC) | Corporate | Limited to contribution | Taxable | Yes | 1–50 members | Ministry of Justice | Law on Commercial Legal Entities |

| Additional Liability Company (ALC) | Corporate | Supplementary personal liability | Taxable | Yes | 1–50 members | Ministry of Justice | Law on Commercial Legal Entities |

| Branch Office | Non-legal entity | Parent company liable | Taxable | Yes | Parent company | Ministry of Justice | Civil Code |

| Representative Office | Non-legal entity | Parent company liable | Generally exempt | No | Parent company | Ministry of Justice | Civil Code |

| General Partnership | Unincorporated | Unlimited personal | Taxable | Yes | 2+ partners | Ministry of Justice | Civil Code |

| Limited Partnership | Unincorporated | Mixed | Taxable | Yes | 2+ partners | Ministry of Justice | Civil Code |

| Sole Proprietorship | Unincorporated | Unlimited personal | Taxable | Yes | 1 individual | State Tax Service | Tax Code |

Each of these structures is examined in full in the sections below.

Open Joint Stock Company (OJSC) in Azerbaijan

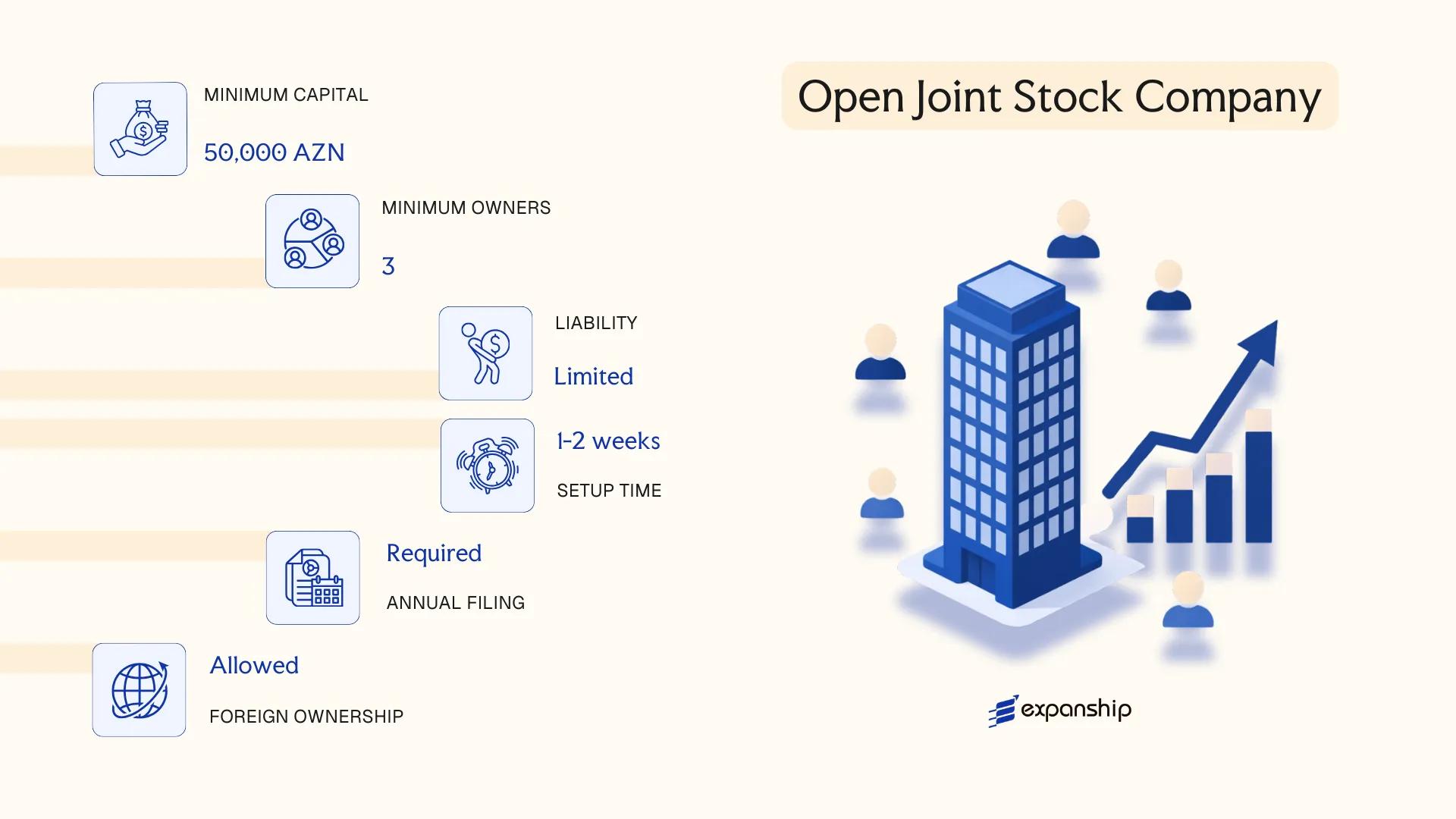

An Open Joint Stock Company — known locally as an açıq səhmdar cəmiyyəti (ASC) — is governed by the Civil Code of Azerbaijan Republic and the Law on Joint Stock Companies (No. 560-IQ, adopted in 1994, with subsequent amendments). The Open Joint Stock Company Azerbaijan ASC framework grants the entity separate legal personality, meaning it can hold assets, enter contracts, and incur liabilities in its own name.

Shareholders bear no personal liability beyond their capital contribution. Shares may be offered to the public and traded freely without shareholder consent, which distinguishes this structure from its closed counterpart.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Open Joint Stock Company (ASC) | Separate legal personality; limited liability |

| Members | Shareholders; minimum 2, no statutory maximum | Board of Directors and Supervisory Board required above certain thresholds |

| Local Presence | Registered legal address in Azerbaijan required | No mandatory resident director, but a local registered address is obligatory |

| Share Capital | Minimum AZN 4,000 (subject to regulatory revision) | Shares must be registered with the Azerbaijan Securities Market State Agency (ASMA) |

| Share Transferability | Freely transferable to any third party | No shareholder pre-emption rights apply on open-market transfers |

| Privacy | Shareholder register is publicly accessible | OJSC filings are subject to mandatory public disclosure |

Focus Points

- Taxation: Corporate profits taxed at 20%; VAT applies at 18% on taxable supplies; dividends paid to non-residents attract 10% withholding tax; stamp duty applies to certain capital transactions.

- Annual Compliance: Mandatory annual financial statements; public companies must undergo an independent audit each financial year.

- Treaty Access: Azerbaijan maintains a network of double taxation treaties, and an OJSC resident in Azerbaijan may access treaty benefits on qualifying income streams.

- Securities Regulation: Share issuances must be registered with ASMA; ongoing disclosure obligations apply under capital markets legislation.

- Conversion: An OJSC may be reorganised into a Closed Joint Stock Company or Limited Liability Company through a prescribed statutory process subject to shareholder resolution.

Closing

The OJSC structure suits businesses planning public capital raises, large-scale joint ventures, or listings on the Baku Stock Exchange. Its principal advantage is unrestricted share transferability; the corresponding drawback is the administrative burden of ongoing securities disclosure and mandatory audit requirements.

Best suited for large enterprises or ventures seeking access to public capital markets or broad investor participation.

Company Incorporation in Azerbaijan

Incorporate an Open Joint Stock Company or other business structure in Azerbaijan with end-to-end support from Expanship.

Closed Joint Stock Company (CJSC) in Azerbaijan

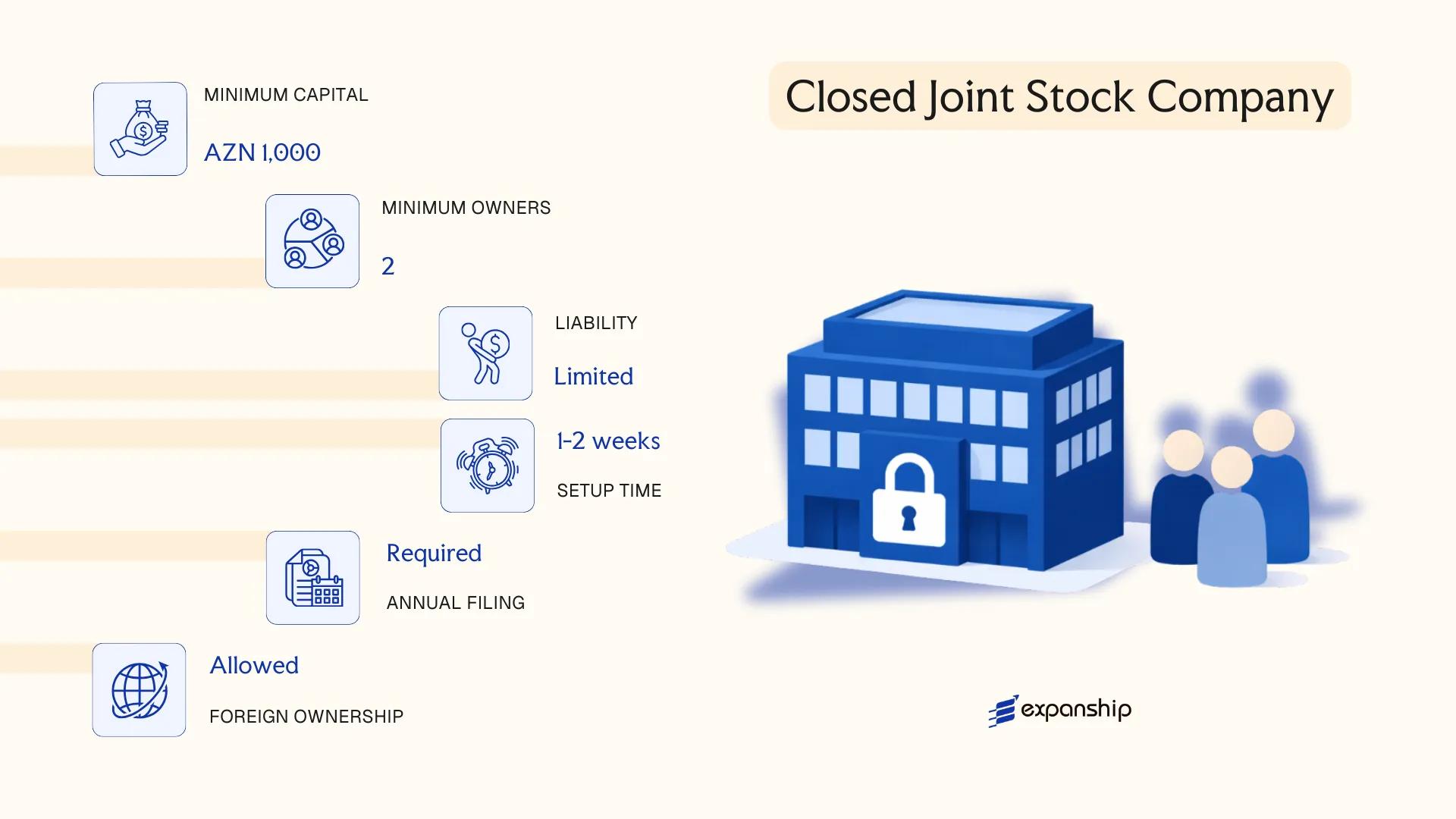

A Closed Joint Stock Company — known in Azerbaijani as qapalı səhmdar cəmiyyəti — is governed by the Civil Code of Azerbaijan and the Law on Joint Stock Companies (2003). Like its open counterpart, the Closed Joint Stock Company Azerbaijan QSC structure carries separate legal personality and limits shareholder liability to the value of their subscribed shares.

Shares in a CJSC cannot be offered to the public or traded on a stock exchange. Transfer of shares to third parties is restricted and typically subject to existing shareholders' pre-emptive rights, making this structure more suitable for closely held businesses where ownership control is a priority.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Closed Joint Stock Company (CJSC / QSC) | Shares not publicly tradeable |

| Members | Shareholders; 1–50 persons (natural or legal) | Exceeding 50 triggers mandatory conversion to OJSC |

| Local Presence | Registered legal address in Azerbaijan required | No mandatory resident director requirement under general rules |

| Capital | Minimum share capital: 2,000 AZN | Must be divided into shares of equal nominal value |

| Privacy | Shareholder register maintained internally; not fully public | State registration records are accessible |

Focus Points

- Taxation: Subject to 20% corporate profit tax; VAT applies at 18% on taxable turnover above the registration threshold; dividends paid to non-residents attract 10% withholding tax; stamp duty applies on certain transactions.

- Annual Compliance: Annual financial statements must be prepared; audit is mandatory where thresholds under Azerbaijani accounting law are met.

- Treaty Access: Resident entities may access Azerbaijan's network of double tax treaties, subject to beneficial ownership requirements.

- Share Transfer Restrictions: Pre-emptive rights of existing shareholders govern any proposed transfer to outside parties, requiring documented consent procedures.

- Conversion: A CJSC must convert to an OJSC if the shareholder count exceeds 50 or if shares are offered publicly.

Closing

A CJSC suits founders seeking a share-based corporate structure with controlled ownership — commonly used for joint ventures, family-held enterprises, and mid-sized trading or holding operations. The principal limitation is the 50-shareholder cap, which constrains future equity raises without a structural conversion.

Best suited for founders and investor groups that require a formal share capital structure while retaining close control over who holds equity in the business.

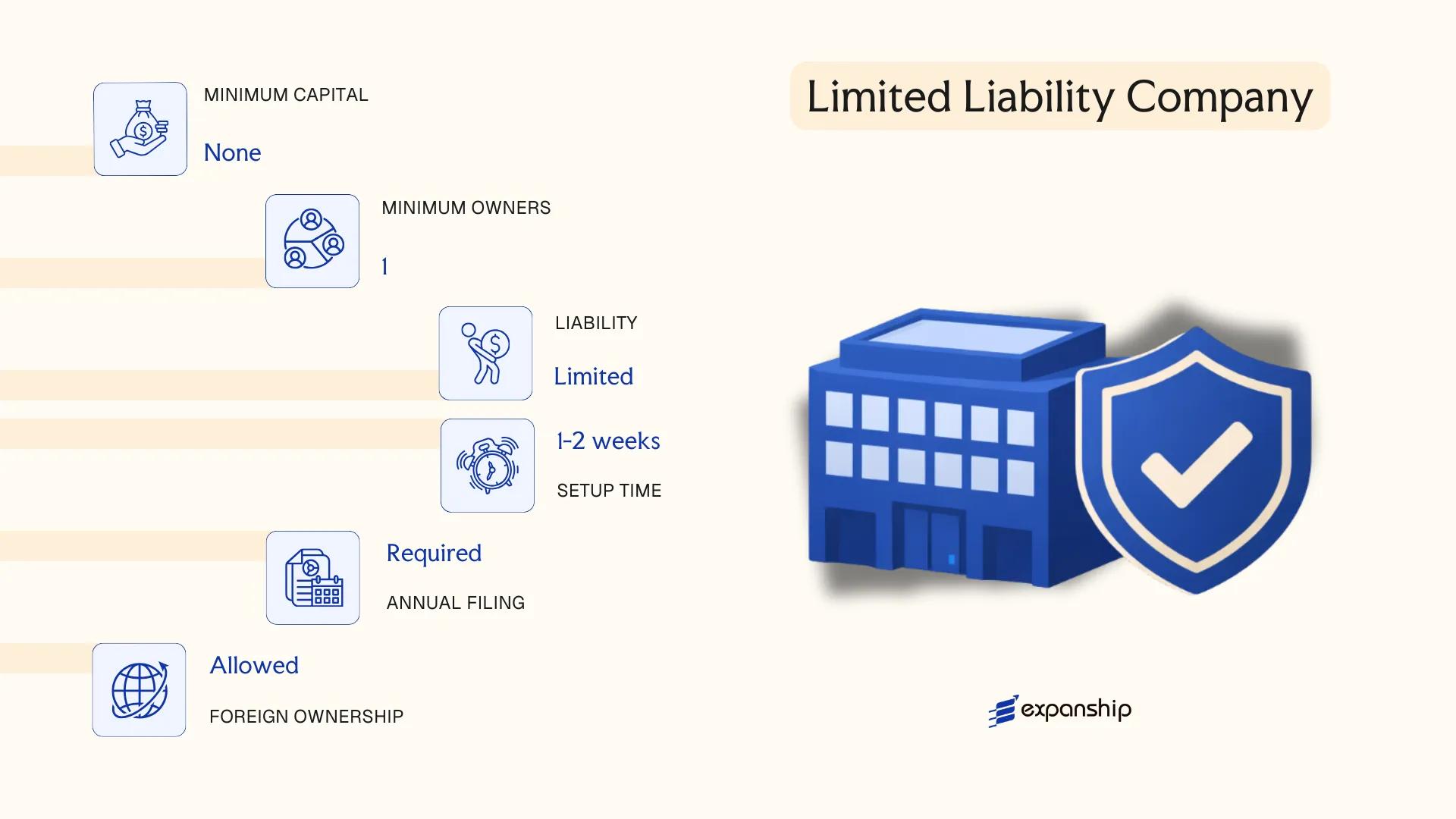

Limited Liability Company (LLC) in Azerbaijan

Governed by the Civil Code of Azerbaijan Republic and the Law on Limited Liability Companies (No. 324-IQ, 1998, as amended), the Limited Liability Company — known locally as a Məhdud Məsuliyyətli Cəmiyyət (MMC) — is the most widely used commercial structure in the country. A Limited Liability Company Azerbaijan MMC carries separate legal personality, meaning the entity can own assets, enter contracts, and incur obligations independently of its members.

Member liability is capped at each participant's contribution to the charter capital. This hybrid nature — combining corporate liability protection with a relatively simple governance structure — makes the MMC accessible to both domestic and foreign investors.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Company (MMC) | Separate legal entity; governed by Law No. 324-IQ |

| Members | 1–50 participants | Can be individuals or legal entities; foreign nationals permitted |

| Management | Director (Executive body) | Supervisory board optional; not mandatory for smaller firms |

| Local Presence | Registered legal address in Azerbaijan required | Physical office address; registered agent not a statutory requirement |

| Charter Capital | No statutory minimum since 2013 reforms | Denominated in AZN; contributions may be cash or in-kind |

| Privacy | Member details filed with the Ministry of Justice | Not publicly searchable via an open online registry |

Focus Points

- Taxation: Subject to 20% corporate profit tax; standard VAT rate of 18% applies above registration threshold; dividend withholding tax of 10% for non-residents; no stamp duty on share transfers as a general rule.

- Annual Compliance: Mandatory submission of financial statements; tax filings with the State Tax Service under the Ministry of Economy.

- Economic Substance: No formal substance regime, though genuine operational presence is expected for treaty benefits.

- Treaty Access: Azerbaijan MMC entities may access the country's double tax treaty network, subject to beneficial ownership conditions.

- Conversion: An MMC may be reorganised into a joint-stock company through a formal restructuring procedure under the Civil Code.

Closing

The MMC suits trading operations, holding structures, and service businesses where operational simplicity and liability protection are both required. Its principal limitation is the 50-participant cap, which constrains equity fundraising at scale.

Best suited for small-to-medium foreign-owned operating businesses or holding entities where full corporate formality is unnecessary.

Additional Liability Company (ALC) in Azerbaijan

The Additional Liability Company (ALC), known in Azerbaijani as əlavə məsuliyyətli cəmiyyət (ƏMC), is governed by the Civil Code of Azerbaijan Republic and the Law on Limited Liability Companies and Additional Liability Companies. It holds a separate legal personality, meaning the entity can enter contracts, own assets, and incur obligations in its own name.

Unlike a standard LLC, members of an ALC bear liability not only to the extent of their capital contributions but also for the company's obligations up to a defined multiple of their contributions — making it a hybrid structure that sits between limited and unlimited liability.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Additional Liability Company (ƏMC) | Separate legal personality; hybrid liability structure |

| Members | Referred to as participants; 1–50 | Exceeding 50 triggers mandatory reorganisation |

| Liability | Each participant liable beyond their contribution at a fixed multiple defined in the charter | Multiple is identical for all participants |

| Local Presence | Registered legal address in Azerbaijan required | No statutory requirement for a local resident director |

| Capital | Minimum share capital: AZN 100 (general principle) | Denominated in Azerbaijani Manat |

| Privacy | Participant details filed with the Ministry of Taxes | Not publicly indexed in a searchable register |

Focus Points

- Taxation: Subject to 20% corporate profit tax; standard VAT rate of 18% applies above the registration threshold; withholding tax on dividends paid to non-residents is generally 10%.

- Annual compliance: Annual financial statements must be submitted to the Ministry of Taxes; audit requirements depend on thresholds set under national accounting legislation.

- Economic substance: No dedicated economic substance regime analogous to offshore jurisdictions, but tax residency rules require genuine local management presence for treaty benefits.

- Treaty access: Azerbaijan's tax treaty network covers 60+ jurisdictions; ALC entities qualify as residents for treaty purposes provided substance criteria are met.

- Conversion: An ALC may be reorganised into an LLC, joint stock company, or other permitted form through a formal restructuring procedure under the Civil Code.

Closing

The ALC suits situations where participants want to signal enhanced financial commitment to counterparties — such as financial services intermediaries or contractual joint ventures — while retaining a corporate structure. The defined liability multiple provides predictability, but the exposure beyond contributed capital is a concrete drawback for risk-averse investors.

Best suited for businesses operating in sectors where counterparty confidence depends on demonstrated participant liability, such as financial intermediation or project-based ventures requiring guaranteed commitments.

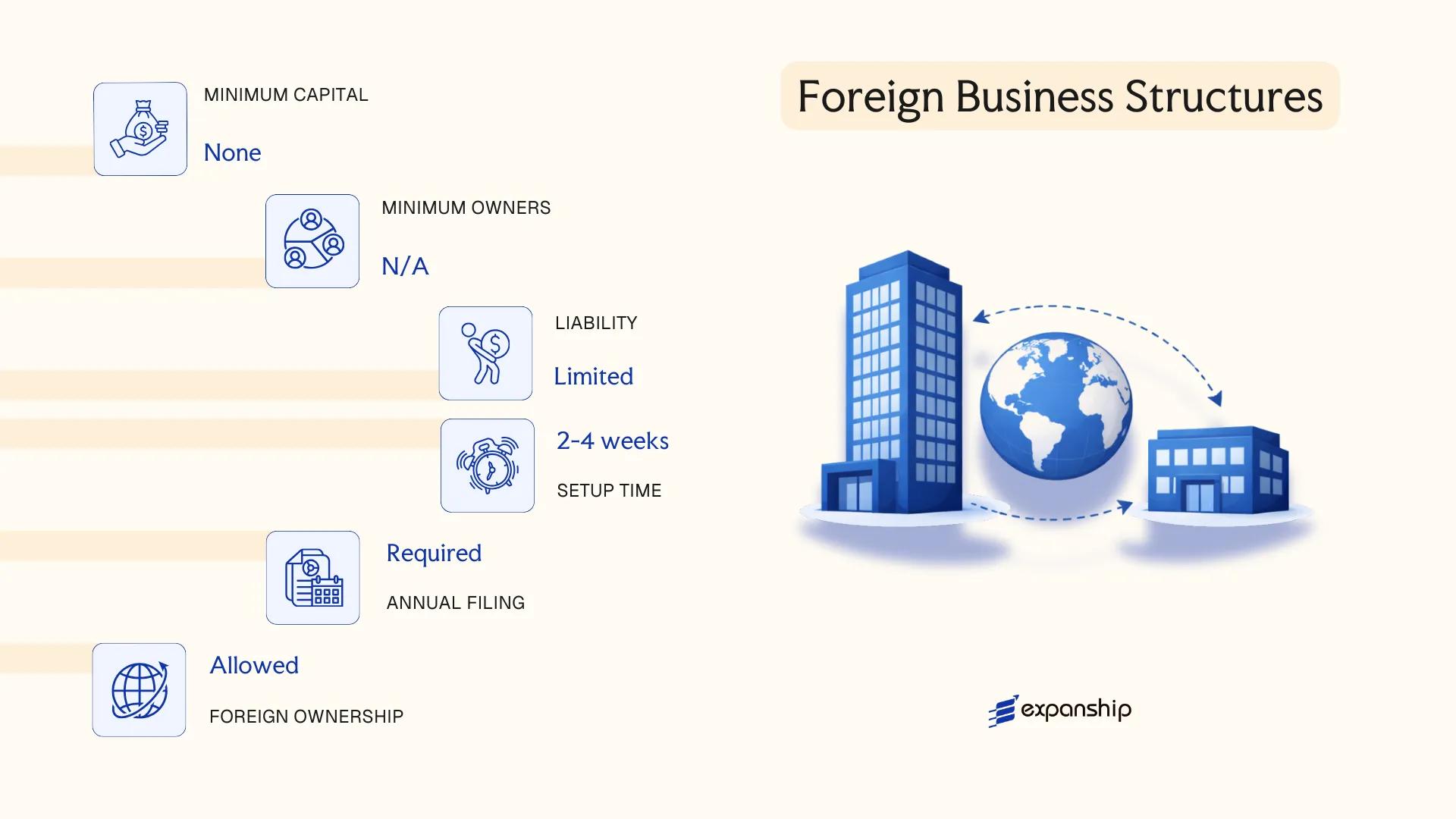

Foreign Business Structures in Azerbaijan [Branch Office, Representative Office]

Registering a foreign company branch office Azerbaijan operates under the Civil Code of the Republic of Azerbaijan and is further governed by the Law on State Registration and State Registry of Legal Entities. Neither a branch nor a representative office constitutes a separate legal entity — both remain extensions of the parent company, which retains full liability for their obligations.

Registration of both structures is handled by the Ministry of Economy of Azerbaijan. A branch may conduct commercial operations on behalf of the foreign parent, while a representative office is restricted to non-commercial activities such as market research, promotion, and liaison functions.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Form | Extension of foreign parent; no separate legal personality | Extension of foreign parent; no separate legal personality |

| Permitted Activities | Full commercial operations | Non-commercial only (liaison, promotion, research) |

| Head | Accredited representative / branch director | Accredited representative |

| Local Presence | Registered legal address in Azerbaijan required | Registered legal address required |

| Capital | No statutory minimum; parent bears liability | No statutory minimum |

| Registration Body | Ministry of Economy | Ministry of Economy |

| Privacy | Parent company details disclosed on public registry | Parent company details disclosed |

Focus Points

- Taxation: Branch profits are subject to corporate income tax at 20%; VAT at 18% applies to taxable supplies; withholding tax may apply to payments remitted to the parent depending on applicable double tax treaties.

- Economic Substance: No formal substance test is codified specifically for branches, but the branch must maintain an active, staffed local address.

- Annual Compliance: Branches must file annual tax returns and maintain accounting records in accordance with Azerbaijani legislation; representative offices have reduced but still mandatory reporting obligations.

- Treaty Access: Access to Azerbaijan's double tax treaty network depends on the parent's country of residence, not the branch's registration status.

- Restrictions: Representative offices cannot generate revenue or enter commercial contracts in their own right; any revenue-generating activity requires conversion to a branch or a locally incorporated entity.

Closing

Both structures suit foreign firms testing the market or supporting an existing client base without committing to full local incorporation. The branch offers operational flexibility for active business, while the representative office carries the limitation of being barred from direct commercial activity.

A branch office is best suited for foreign companies that need to conduct revenue-generating operations in Azerbaijan without establishing a separately incorporated local entity.

Partnerships in Azerbaijan [General Partnership, Limited Partnership]

Partnership structures in Azerbaijan are governed by the Civil Code of the Republic of Azerbaijan (1999) and the Law on Commercial Legal Entities. Partnership registration in Azerbaijan produces entities classified as commercial legal entities, yet the two recognised forms differ significantly in how liability is distributed among participants. Unlike capital-based structures such as LLCs or JSCs, partnerships are founded on the personal participation and mutual trust of their members.

Both forms require at least two founding members and are registered with the Ministry of Taxes of the Republic of Azerbaijan. Under Azerbaijani law, these entities do carry separate legal personality, though members' personal assets remain exposed to varying degrees depending on the form chosen.

Key Characteristics

| Requirement | General Partnership (Tam Ortaqlıq) | Limited Partnership (Kommandit Ortaqlıq) |

|---|---|---|

| Legal Form | Commercial legal entity with separate legal personality | Commercial legal entity with separate legal personality |

| Members | General partners (tam ortaqlar); minimum 2, no statutory maximum | At least 1 general partner + at least 1 limited partner (kommanditist); no statutory maximum |

| Liability | All partners bear unlimited, joint and several liability | General partners: unlimited liability; limited partners: liable only up to their capital contribution |

| Local Presence | Registered office address required in Azerbaijan | Registered office address required in Azerbaijan |

| Capital | No statutory minimum capital; denominated in Azerbaijani Manat (AZN) | No statutory minimum capital; denominated in AZN; limited partners' contributions define their exposure |

| Privacy | Partner names are disclosed in state registration records | General and limited partner names appear in registration documents |

Focus Points

- Taxation: Partnerships are treated as transparent or pass-through entities for Azerbaijani tax purposes; profits are attributed to and taxed at the partner level under the Tax Code of the Republic of Azerbaijan; VAT obligations apply if turnover thresholds are met; no separate entity-level corporate profit tax is levied on the partnership itself.

- Annual Compliance: Partners are required to submit financial statements and tax filings to the Ministry of Taxes; accounting records must be maintained in accordance with Azerbaijani accounting standards.

- Treaty Access: Because partnerships are not subject to corporate income tax at the entity level, access to Azerbaijan's double tax treaty network may be limited or unavailable for the partnership itself.

- Restrictions: Foreign nationals may participate as partners, but certain regulated sectors impose additional licensing or residency requirements on general partners.

- Conversion: Azerbaijani law permits conversion of a partnership into another commercial legal entity form, subject to statutory procedures and member consent.

Sub-Types

General Partnership (Tam Ortaqlıq)

All participants act as general partners and each bears unlimited personal liability for the obligations of the firm. This structure is most commonly used by small professional or family-owned businesses where all members are actively engaged in management.

Limited Partnership (Kommandit Ortaqlıq)

This form introduces a two-tier membership structure: general partners manage the business and carry unlimited liability, while limited partners (kommanditistlər) are passive investors whose exposure is capped at their contributed capital. The limited partnership is suited to arrangements where investors wish to participate financially without taking on management responsibilities or personal liability beyond their contribution.

Closing

Partnerships are primarily used for small-scale trading or professional service arrangements where the founding members prefer a less formalised corporate structure over a share-based entity. The absence of a minimum capital requirement is a practical entry point, though unlimited personal liability for general partners represents a significant financial exposure that makes these forms unsuitable for higher-risk commercial activities.

Partnerships suit small, closely-held businesses where all principals are known to each other and the scale of operations does not justify the administrative overhead of a share-based entity — particularly where limited partners seek passive investment with capped liability.

Sole Proprietorship in Azerbaijan

Sole proprietorship registration in Azerbaijan is governed by the Civil Code of the Republic of Azerbaijan and the Law on State Registration and State Registry of Legal Entities. Unlike the corporate forms covered elsewhere in this guide, a sole proprietorship — locally termed fərdi sahibkar (individual entrepreneur) — does not constitute a separate legal entity. The proprietor and the business are legally indistinguishable, meaning personal assets remain exposed to business liabilities.

Registration is handled through the Ministry of Economy's ASAN Xidmət (ASAN Service) centres or via the e-government portal. The process is comparatively straightforward, with registration typically completed within one business day upon submission of required documentation.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated individual enterprise | No separate legal personality from the owner |

| Proprietor | Single individual (fərdi sahibkar) | One proprietor only; no co-ownership structure |

| Local Presence | Registered address required | Must be a physical address within Azerbaijan |

| Capital | No statutory minimum | No paid-up capital requirement |

| Liability | Unlimited personal liability | Proprietor's personal assets are fully exposed |

| Privacy | Name appears in public registry | Registry records are accessible |

Focus Points

- Taxation: Subject to simplified tax regime if annual turnover falls below the statutory threshold; otherwise standard income tax applies at 14% on net profit, with VAT registration mandatory upon exceeding AZN 200,000 in annual turnover. Withholding tax obligations apply on applicable payments.

- Annual Compliance: Annual income declaration must be filed with the State Tax Service; bookkeeping obligations apply under the simplified or general regime.

- Conversion: A sole proprietorship can be converted into a legal entity (such as an LLC), though the process requires fresh registration rather than a structural transformation.

- Treaty Access: As an unincorporated individual, access to Azerbaijan's double tax treaties depends on the individual's residency status, not the business form itself.

- Restrictions: Foreign nationals face additional conditions when registering as individual entrepreneurs and should verify current eligibility requirements with the Ministry of Economy.

Closing

A sole proprietorship suits small-scale local trading, freelance service providers, and individual professionals seeking a low-cost operational structure with minimal administrative burden. The primary advantage is the absence of a minimum capital requirement and rapid registration; the principal drawback is unlimited personal liability, which exposes the proprietor's private assets to all business obligations.

Local individuals operating small-scale or single-person service businesses who prioritise low setup costs over liability protection.

How to Choose the Right Entity Type in Azerbaijan

Knowing how to choose a company type in Azerbaijan before registration prevents structural problems that are far more costly to correct after the fact.

Why Your Entity Choice Matters

The legal form you register has binding consequences on liability, tax treatment, reporting obligations, and operational capacity. Selecting the wrong structure can produce outcomes such as:

- Choosing a structure without access to Azerbaijan's double taxation treaty network means your foreign counterparts cannot claim withholding tax reductions on dividends, interest, or royalties paid to your entity.

- Registering a representative office when your actual activities constitute trading subjects the operation to penalties under the Civil Code of Azerbaijan, since representative offices are legally prohibited from conducting commercial transactions.

- Selecting an entity that requires annual audited financial statements when your firm operates as a single-person consultancy adds recurring compliance costs without regulatory benefit.

- Forming a joint stock company when a limited liability company would suffice locks you into mandatory board structures, share issuance procedures, and State Securities Commission disclosure requirements that do not apply to an LLC.

Key Factors to Consider

- Business Activity: Active trading, regulated sectors such as banking or insurance, and passive asset-holding each correspond to distinct permissible entity types under Azerbaijani law.

- Ownership Structure: A single founder can establish an LLC without a board, whereas multi-party arrangements with transferable equity may require a joint stock structure.

- Tax Objectives: If treaty access or a specific tax regime applies, the entity type must be eligible under the Tax Code of Azerbaijan.

- Substance Capacity: If you cannot maintain a physical presence or local decision-making, confirm whether your chosen structure triggers substance-related reporting obligations.

- Privacy Requirements: Shareholder and director information for OJSCs is subject to public disclosure through the State Securities Commission; LLCs offer comparatively more confidentiality.

- Exit Strategy: Confirm whether your chosen structure permits conversion, redomiciliation, or voluntary liquidation under the Law of the Republic of Azerbaijan on State Registration of Legal Entities and Individual Entrepreneurs before committing to it.

Compliance Services for Companies in Azerbaijan

Ongoing compliance support for Azerbaijani entities, covering annual filings, tax reporting, and regulatory obligations.

Conclusion

Reaching the right Azerbaijan company formation conclusion depends on matching your business objectives to the structural characteristics of each entity type.

The LLC dominates registrations under the Civil Code and the Law on Limited Liability Companies, making it the default choice for most foreign investors and domestic operators. OJSCs suit businesses requiring public capital access, while CJSCs serve smaller closed investor groups. The ALC introduces personal liability beyond share value, making it a less common but legally distinct option. Branch offices maintain the parent entity's legal identity, whereas representative offices are confined to non-commercial functions. General and limited partnerships retain unlimited or tiered liability structures. Sole proprietorships carry the lowest administrative burden but expose founders to personal liability.

Regulatory oversight by the State Tax Service and the Ministry of Economy continues to evolve, with Azerbaijan incrementally expanding its tax treaty network and refining its investment legal framework. Expanship monitors these developments to support accurate, jurisdiction-specific guidance.

How Expanship Can Assist You

Expanship company registration Azerbaijan services are built around the specific structures and obligations covered in this blog — from LLCs and OJSCs to branch and representative offices. Every entity type carries distinct filing requirements under Azerbaijani law, and the State Tax Service under the Ministry of Economy is your primary point of contact for registration and ongoing compliance. Knowing which structure fits your goals is only part of the process; executing it correctly matters just as much.

Expanship handles each stage of your Azerbaijan company setup from the initial documentation through to post-incorporation obligations.

- Document preparation, notarization, and apostille

- Registered agent and legal address provision

- Filing and liaison with the State Tax Service

- Post-incorporation compliance management

- Corporate bank account introduction assistance

- Ongoing statutory maintenance support

Ready to incorporate in Azerbaijan with Expanship? Reach out directly through our Expanship Azerbaijan contact page.

Frequently Asked Questions (FAQ)

The Limited Liability Company (LLC) is the most frequently registered entity. Its relatively low minimum capital threshold, capped member liability, and straightforward administrative structure make it the default choice for small to mid-sized businesses.

A Branch Office is not a separate legal entity — it carries the full liability of its parent company and cannot issue equity. An LLC, by contrast, has independent legal personality and limits member liability to their capital contributions. Compliance obligations also differ: branches must file under the parent's governance structure, while an LLC maintains its own statutory records locally.

The Closed Joint Stock Company (CJSC) restricts share transfers and does not offer securities to the public, limiting the scope of publicly accessible ownership information. Shareholder registers are maintained internally rather than published. Nominee arrangements are legally permissible in Azerbaijan, though their practical use varies by structure.

A sole proprietorship and an LLC can each be established by one individual. General Partnerships and Limited Partnerships require at least two participants by their legal definition. A CJSC or OJSC can technically have a single shareholder, though governance requirements differ between the two.

Foreign nationals may register an LLC, CJSC, OJSC, or Additional Liability Company (ALC) in Azerbaijan without a local partner requirement. Representative Offices and Branch Offices are also available to foreign firms operating under their parent entity. There is no general restriction on foreign ownership percentage in most commercial structures under Azerbaijani civil law.

Reorganisation between entity types — including transformation, merger, and division — is governed by the Civil Code of the Republic of Azerbaijan. An LLC may be restructured into a joint stock company through a formal transformation procedure. The process requires a shareholders' resolution, updated charter documentation, and re-registration with the State Register.

LLCs, ALCs, CJSCs, and OJSCs all hold separate legal personality under Azerbaijani law. A Branch Office does not — it acts as an extension of its foreign parent and carries no independent legal standing. Sole proprietorships also lack separate legal personality; the individual and the business are treated as one legal subject.

A sole proprietorship has the lightest ongoing compliance burden, with simplified tax reporting and no requirement to maintain separate statutory registers. However, unlimited personal liability remains a significant structural drawback for any business with meaningful financial exposure. LLCs carry more administrative obligations but provide the liability protection that most commercial operators require.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.