Key Takeaways

- Aruba maintains its own corporate legal framework under the Aruba Civil Code, separate from Dutch and Curaçaoan law, with the Kamer van Koophandel en Nijverheid Aruba administering the commercial register.

- The Vennootschap met Beperkte Aansprakelijkheid (VBA) is the most commonly chosen structure for both resident and non-resident businesses seeking private limited liability.

- Partnerships such as the Vennootschap onder Firma (VOF) and Commanditaire Vennootschap (CV) expose their principals to greater personal liability than incorporated structures like the NV or VBA.

- Aruba's territorial tax system means that foreign-sourced income may receive different treatment from locally generated profits depending on the entity structure used.

Introduction to Entity Types in Aruba

Aruba is a constituent country of the Kingdom of the Netherlands, situated in the southern Caribbean approximately 29 kilometres north of Venezuela. As a self-governing territory within the Kingdom, it maintains its own legal and commercial framework, operating under the Aruba Civil Code and related corporate legislation distinct from those of the Netherlands and Curaçao.

Company registration falls under the authority of the Kamer van Koophandel en Nijverheid Aruba (Chamber of Commerce and Industry Aruba), which maintains the commercial register and processes new entity formations. The territory applies a territorial tax system, meaning foreign-sourced income may be treated differently from locally generated profits depending on the structure used.

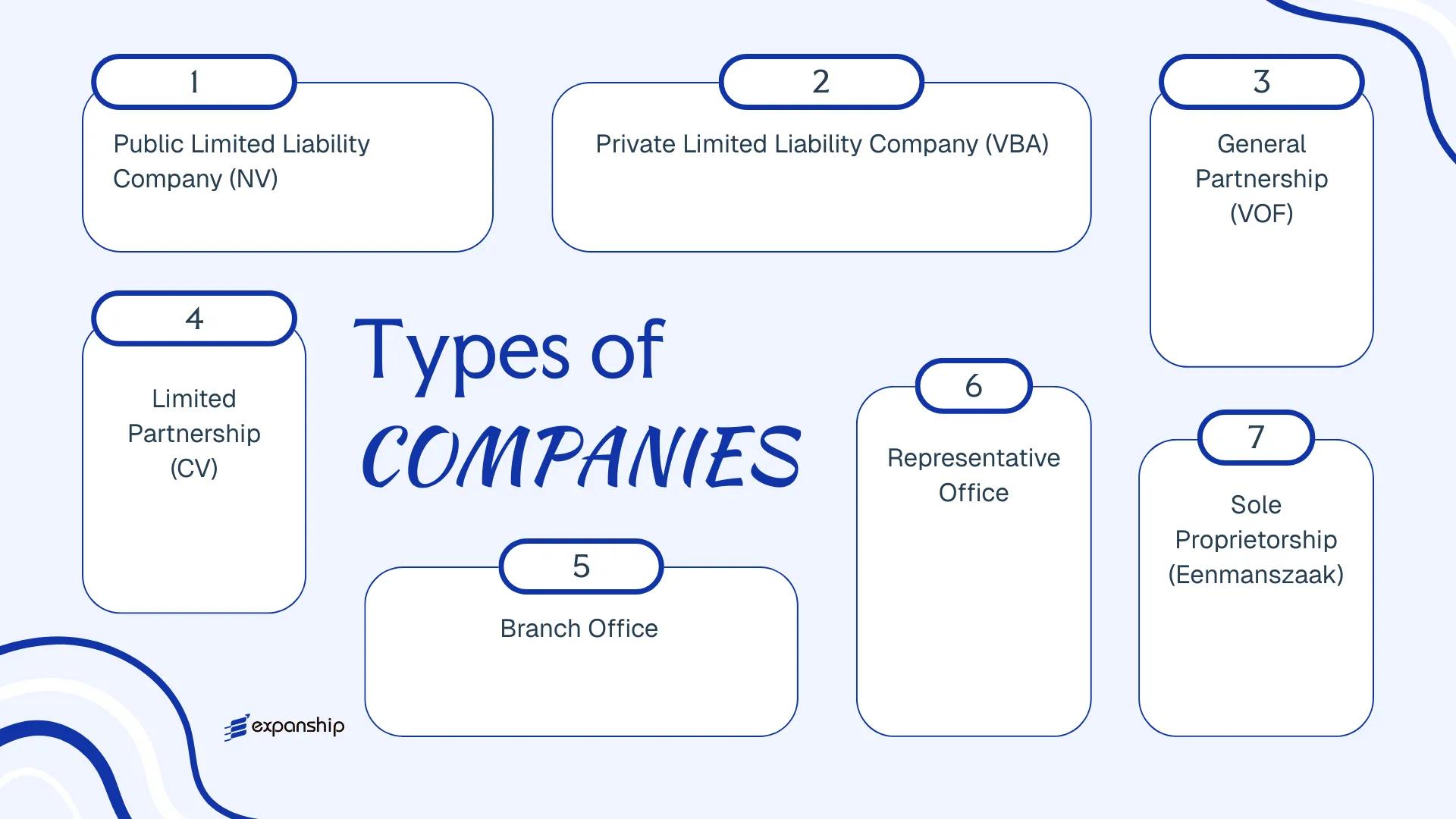

The types of business entities in Aruba available to local and foreign investors include the Naamloze Vennootschap (NV), the Vennootschap met Beperkte Aansprakelijkheid (VBA), the Vennootschap onder Firma (VOF), the Commanditaire Vennootschap (CV), the Eenmanszaak, the Branch Office, and the Representative Office. Each of these legal entity types carries distinct implications for liability, governance, and tax treatment. This article examines each structure in detail to help you identify which formation aligns with your operational and regulatory requirements.

An Overview of Business Structures in Aruba

Aruba's company law framework recognises several distinct entity types, each governed primarily by the Aruba Civil Code (Burgerlijk Wetboek van Aruba) and supplementary commercial legislation administered through the Aruba Chamber of Commerce and Industry (Kamer van Koophandel en Nijverheid). Every structure carries a different liability profile, capital requirement, and suitability for domestic versus international activity.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Naamloze Vennootschap (NV) | Public Limited Company | Limited to share capital | Taxed (profit tax) | Permitted | 1 shareholder | Chamber of Commerce | Civil Code Aruba |

| Vennootschap met Beperkte Aansprakelijkheid (VBA) | Private Limited Company | Limited to share capital | Taxed (profit tax) | Permitted | 1 shareholder | Chamber of Commerce | Civil Code Aruba |

| Vennootschap onder Firma (VOF) | General Partnership | Unlimited, joint | Taxed (income tax) | Permitted | 2 partners | Chamber of Commerce | Commercial Code |

| Commanditaire Vennootschap (CV) | Limited Partnership | Mixed (general/limited) | Taxed / Conditionally exempt | Permitted | 2 partners | Chamber of Commerce | Commercial Code |

| Branch Office | Foreign entity extension | Parent bears liability | Taxed on local profits | Permitted | N/A (parent entity) | Chamber of Commerce | Civil Code Aruba |

| Representative Office | Non-trading presence | Parent bears liability | Generally not taxed | Not permitted | N/A (parent entity) | Chamber of Commerce | Civil Code Aruba |

| Eenmanszaak | Sole Proprietorship | Unlimited, personal | Taxed (income tax) | Permitted | 1 owner | Chamber of Commerce | Commercial Code |

Each of these structures is examined in full in the sections below.

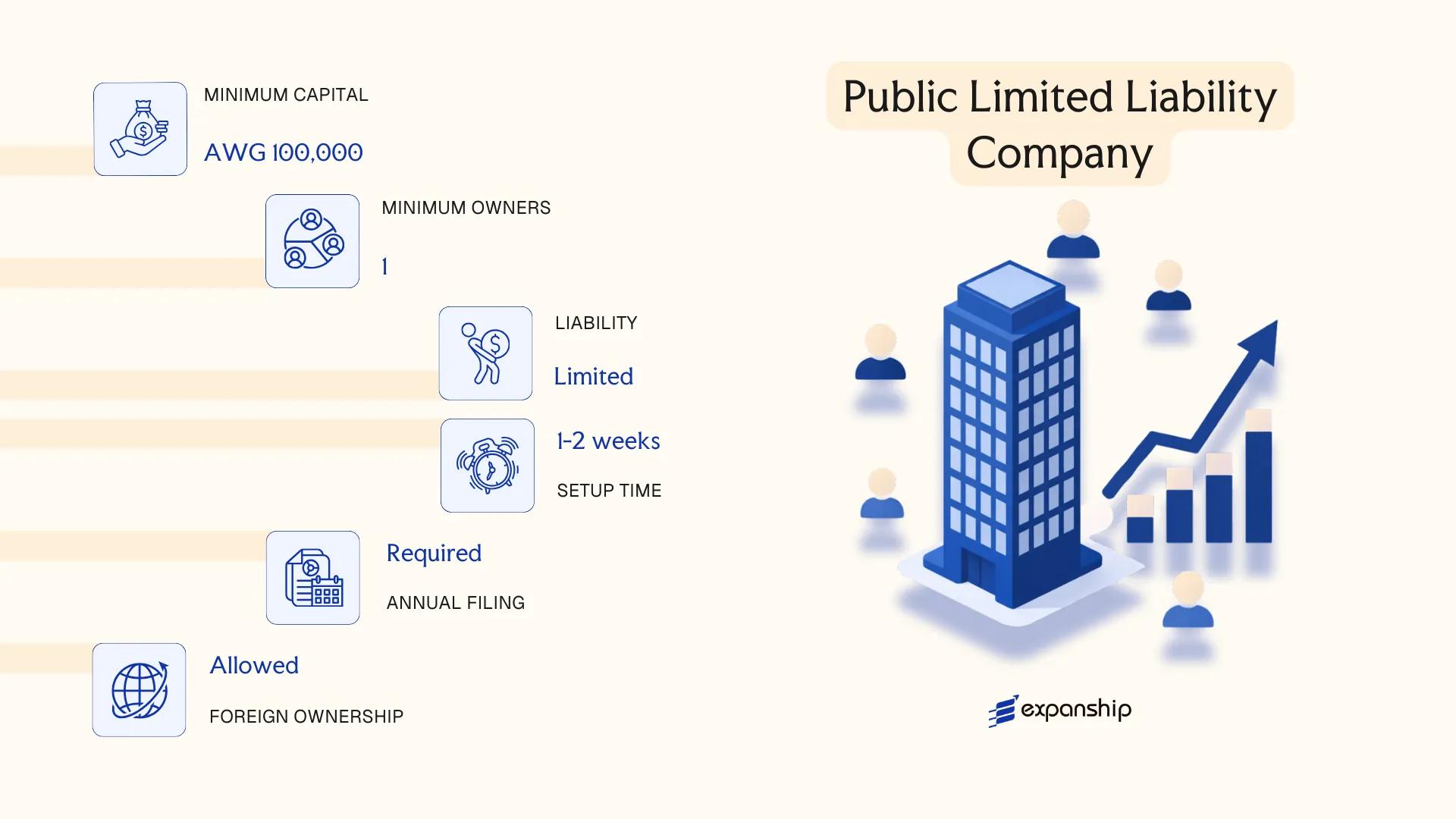

Naamloze Vennootschap (NV) — Public Limited Liability Company

Governed by the Civil Code of Aruba, the Naamloze Vennootschap is the foundational vehicle for Aruba NV company formation and has historically been the preferred structure for international holding and finance arrangements. The entity carries separate legal personality, meaning its assets and liabilities are legally distinct from those of its shareholders.

Shares in an NV are freely transferable by default, which distinguishes it structurally from its private counterpart and makes it suited to multi-investor or capital-market arrangements. Shareholder liability is confined to the amount unpaid on their shares.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Naamloze Vennootschap (NV) | Incorporated by notarial deed; legal personality arises upon registration with the Aruba Chamber of Commerce |

| Members | Shareholders; no statutory minimum shareholder count; shares may be held by a single legal or natural person | Bearer shares have been abolished; only registered shares are permitted |

| Directors | Minimum one director; no residency requirement under the Civil Code, though substance rules may apply in practice | Corporate directors are permissible |

| Local Presence | Registered office address in Aruba required; a licensed trust company commonly acts as registered agent | Physical office not mandated solely by incorporation rules |

| Capital | Minimum authorised capital of AWG 10,000; no statutory paid-up minimum at incorporation | AWG = Aruban Florin; capital must be stated in the articles of incorporation |

| Privacy | Shareholder register is maintained internally; not publicly filed | Director details are filed with the Chamber of Commerce |

Focus Points

- Taxation: NVs are subject to Aruban profit tax; the standard corporate income tax rate is 25%. Dividend withholding tax and no VAT regime applies — a turnover tax (BBO) applies instead. Review current rates at the Departamento di Impuesto.

- Economic Substance: Entities conducting relevant activities must meet substance requirements under Aruban economic substance legislation, including local management and qualified staff.

- Annual Compliance: Annual financial statements must be prepared; filing obligations with the Chamber of Commerce apply, including periodic fee payments.

- Treaty Access: Aruba has a separate tax arrangement within the Kingdom of the Netherlands (the BRK/BRNC), which governs inter-kingdom dividend and income flows rather than a standalone treaty network.

- Conversion: An NV may be converted into a VBA by shareholder resolution and notarial deed, subject to creditor protection procedures under the Civil Code.

Closing

The NV suits holding structures, intra-group finance vehicles, and businesses requiring freely transferable shares or multiple investor classes. Its primary advantage is structural flexibility for capital arrangements; the principal limitation is that maintaining economic substance compliance adds ongoing operational overhead for internationally managed entities.

The NV is most appropriate for internationally oriented businesses, investment holding companies, and structures involving multiple shareholders or planned capital distributions.

Company Incorporation in Aruba

Incorporate an NV or other entity type in Aruba with end-to-end support from registration through post-incorporation compliance.

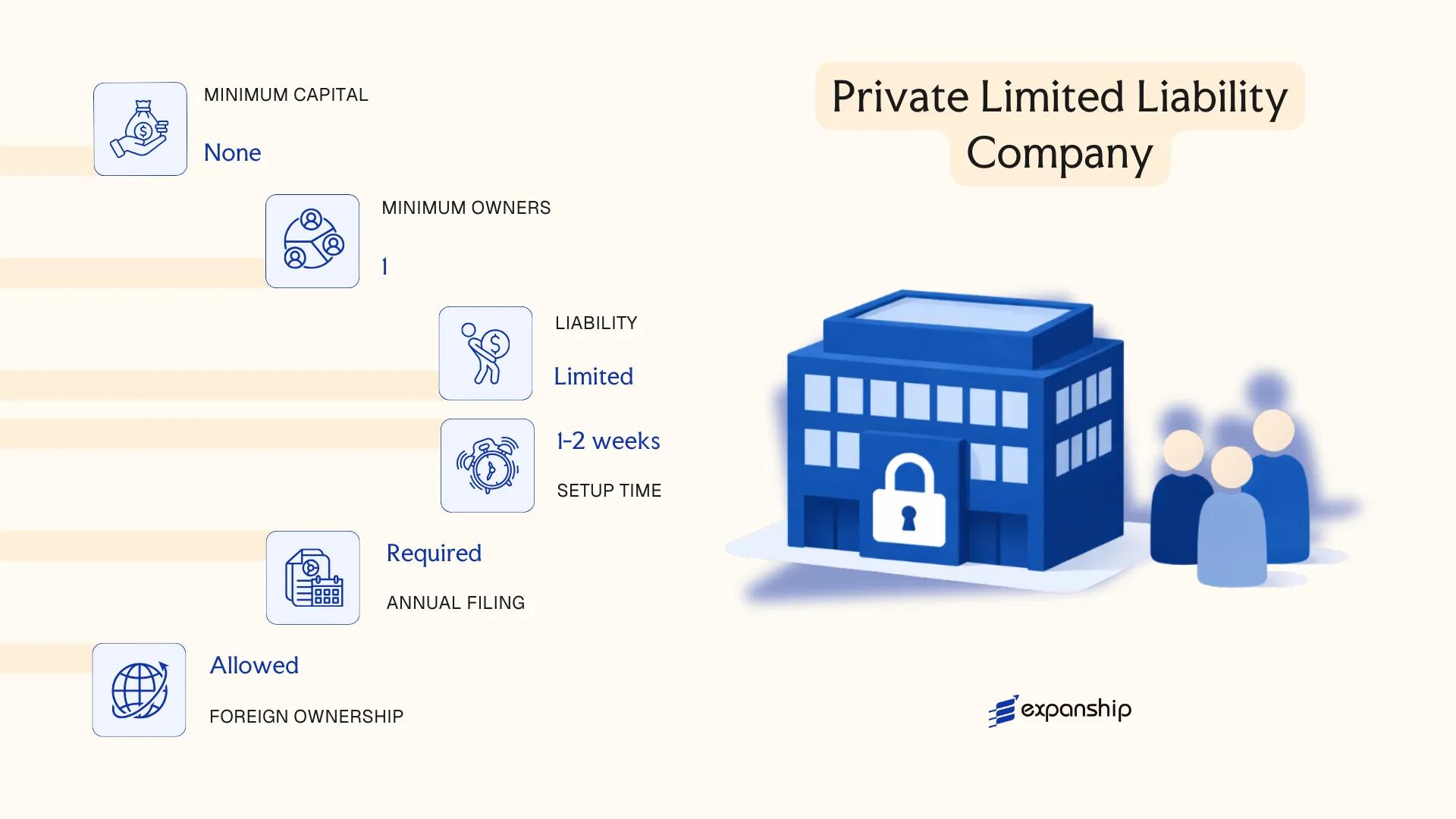

Vennootschap met Beperkte Aansprakelijkheid (VBA) — Private Limited Liability Company

The Aruba VBA private limited liability company is governed by the Landsverordening op de Vennootschap met Beperkte Aansprakelijkheid, enacted in 2009. It carries separate legal personality, meaning the entity itself holds rights and obligations distinct from those of its shareholders.

Liability is capped at each shareholder's capital contribution. The structure occupies a middle ground between a closely held private firm and a fully public vehicle, making it accessible without the disclosure requirements associated with publicly traded entities.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Vennootschap met Beperkte Aansprakelijkheid (VBA) | Separate legal personality; distinct from NV |

| Members | Shareholders and Directors; minimum 1 shareholder, no statutory maximum | Shareholders and directors may be the same person |

| Local Presence | Registered office in Aruba required; local registered agent recommended | No statutory requirement for a resident director |

| Share Capital | No mandatory minimum capital; shares may be issued in any currency | Capital structure is set in the articles of incorporation |

| Privacy | Shareholder register is maintained internally; not publicly filed | Beneficial ownership disclosure obligations apply under AML legislation |

Focus Points

- Taxation: Subject to Aruba profit tax; no separate capital gains tax regime; dividend withholding tax applies to distributions; no VAT at present, though turnover tax (BBO) applies at the entity level.

- Economic Substance: Entities engaged in relevant activities must demonstrate genuine substance in Aruba under the Country's economic substance framework.

- Annual Compliance: Annual financial statements must be prepared; filing obligations with the Aruba Chamber of Commerce (Kamer van Koophandel) apply.

- Treaty Access: Aruba maintains its own tax information exchange agreements (TIEAs); access to the Netherlands tax treaty network is not automatic for Aruba-incorporated entities.

- Conversion: A VBA may be converted into an NV subject to compliance with the applicable landsverordening governing that transition.

Closing

The VBA suits holding structures, trading operations, and family-owned businesses where shareholder identity need not be publicly disclosed. Its principal advantage is the absence of a minimum capital requirement; however, the economic substance obligations add an ongoing compliance layer that should not be underestimated for non-resident-managed structures.

The VBA is well-suited to small-to-medium private businesses and holding companies seeking limited liability without the formalities attached to a publicly oriented entity.

Partnerships [Vennootschap onder Firma (VOF), Commanditaire Vennootschap (CV)]

Aruba VOF and CV partnership structures are governed by the Wetboek van Koophandel (Commercial Code), which predates the island's separate Status Aparte in 1986 and continues to apply with local adaptations. Neither the VOF nor the CV holds separate legal personality, meaning the entity itself cannot own assets or enter contracts independent of its partners.

Liability exposure differs between the two forms. In a VOF, all partners bear unlimited joint and several liability for the firm's obligations. The CV introduces a distinction between general partners, who manage the business and carry unlimited liability, and limited (silent) partners, whose exposure is capped at their contributed capital provided they do not participate in management.

Key Characteristics

| Requirement | VOF | CV |

|---|---|---|

| Legal Personality | None | None |

| Partners | General partners (vennoten); minimum 2, no statutory maximum | General partners (beherende vennoten) minimum 1; limited partners (commanditaire vennoten) minimum 1; no statutory maximum |

| Liability | Unlimited, joint and several for all partners | Unlimited for general partners; limited to capital contribution for silent partners |

| Local Presence | Registered address in Aruba required; no mandatory local agent under current rules | Registered address in Aruba required |

| Capital | No minimum capital requirement; contributions can be cash, assets, or services | No minimum capital requirement; limited partner's contribution defines liability cap |

| Registration | Kamer van Koophandel en Nijverheid (Chamber of Commerce) registration required | Kamer van Koophandel en Nijverheid registration required |

Focus Points

- Taxation: Partnerships are fiscally transparent; profits flow to partners and are taxed at the individual or corporate level depending on partner status; no separate entity-level income tax applies, though turnover tax (BBO) obligations may apply to business activities.

- Economic Substance: Transparency structures are generally outside the scope of Aruba's economic substance requirements, which target specific regulated entity types.

- Annual Compliance: Partners must maintain registration with the Chamber of Commerce and file updates upon any change in partnership composition or structure.

- Treaty Access: As non-resident legal persons without separate legal personality, these structures typically cannot independently access double tax treaty benefits.

- Restrictions: Silent partners in a CV who actively participate in management lose their limited liability protection under the Commercial Code.

Sub-Types

Vennootschap onder Firma (VOF)

The VOF is the general partnership form, used for active trading or professional practices where all participants intend to take an operational role. Every partner is exposed to full personal liability, making this structure less suitable where liability insulation is a priority.

Commanditaire Vennootschap (CV)

The CV functions as a limited partnership, allowing passive investors to contribute capital without taking on management responsibility. This structure is commonly used for investment arrangements and family asset-holding purposes where operational control is concentrated in one or more general partners.

When to Use These Structures

Both forms suit smaller, operationally active businesses or domestic joint ventures where administrative simplicity outweighs the need for liability protection. The CV offers a degree of structural flexibility for capital-raising arrangements, but the unlimited liability carried by general partners remains a material constraint.

VOF and CV structures are most appropriate for small domestic businesses, professional partnerships, or family investment arrangements where the partners are prepared to accept personal liability exposure.

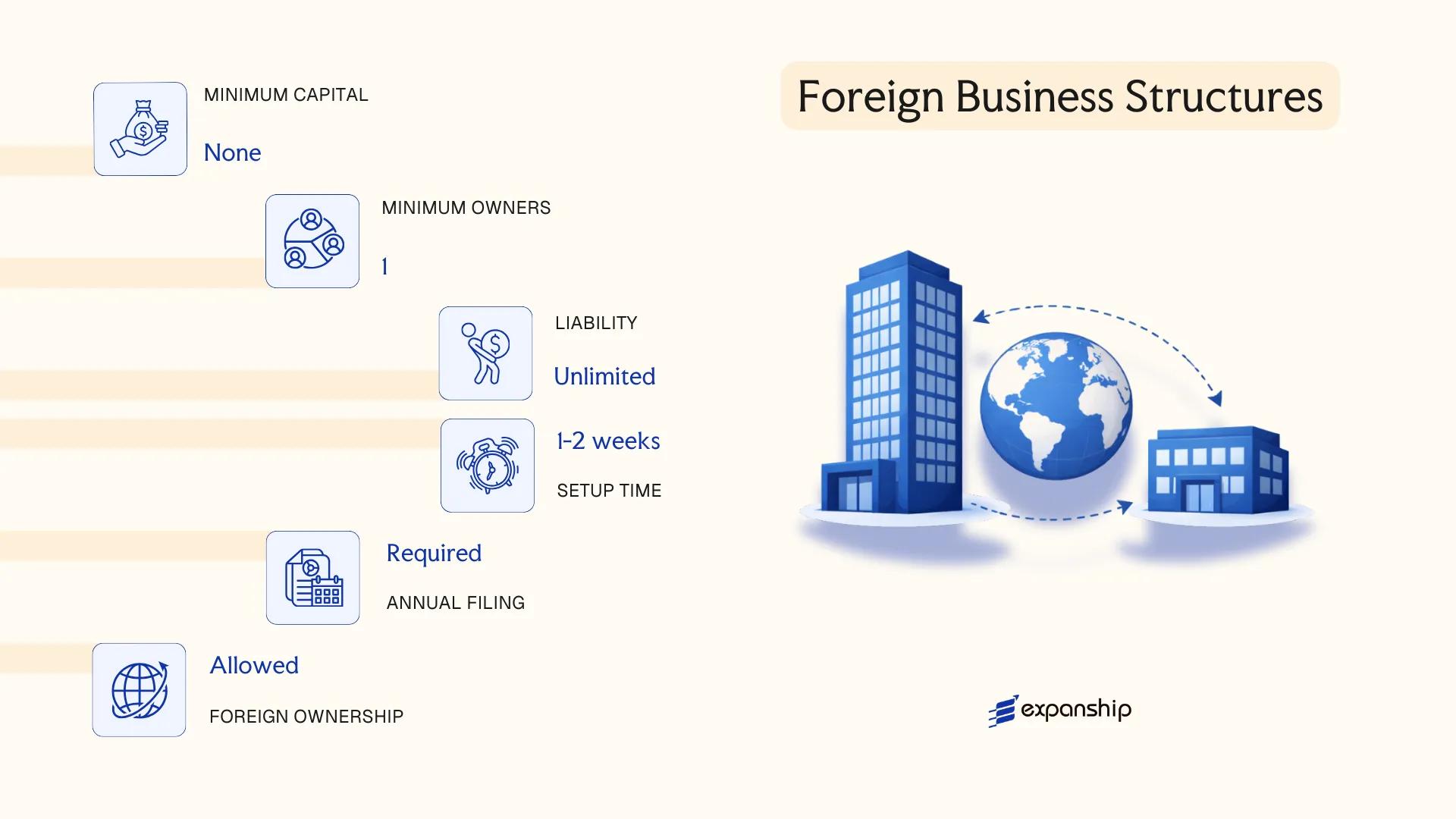

Foreign Business Structures [Branch Office, Representative Office]

To open a branch office in Aruba, a foreign company must register with the Chamber of Commerce (Kamer van Koophandel) under the Aruba Civil Code. A branch is not a separate legal entity — it remains an extension of the parent company, which bears full liability for the branch's obligations. No minimum capital requirement applies specifically to the branch itself, though the parent entity must already be validly incorporated in its home jurisdiction.

A representative office operates under similar registration requirements but is restricted to promotional and liaison activities. It cannot generate revenue or enter into commercial contracts in its own name.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Form | Extension of foreign parent; no separate legal personality | Extension of foreign parent; no separate legal personality |

| Liability | Parent company bears full liability | Parent company bears full liability |

| Local Presence | Registered address and local representative required | Registered address and local representative required |

| Permitted Activities | Full commercial operations | Promotional and liaison activities only |

| Capital Requirement | None specific to the branch | None |

| Privacy | Parent company details filed on public register | Parent company details filed on public register |

Focus Points

- Taxation: Subject to Aruba's corporate income tax on locally sourced profits; turnover tax (BBO) may apply to commercial transactions; no separate withholding tax treatment from the parent.

- Economic Substance: Activity conducted through a branch may trigger substance requirements depending on the nature of operations.

- Annual Compliance: Annual financial statements must be filed with the Chamber of Commerce; ongoing registration renewal required.

- Treaty Access: Access to tax treaties depends on the parent company's jurisdiction of incorporation, not the branch's registration.

- Activity Restrictions: Representative offices are prohibited from invoicing clients or concluding binding contracts locally.

Closing

A branch office suits foreign companies testing the Aruban market or managing regional operations without establishing a separate subsidiary, though the absence of liability separation between the branch and parent is a material structural risk.

Best suited for established foreign companies seeking a direct operational or market-entry presence without the administrative burden of incorporating a new local entity.

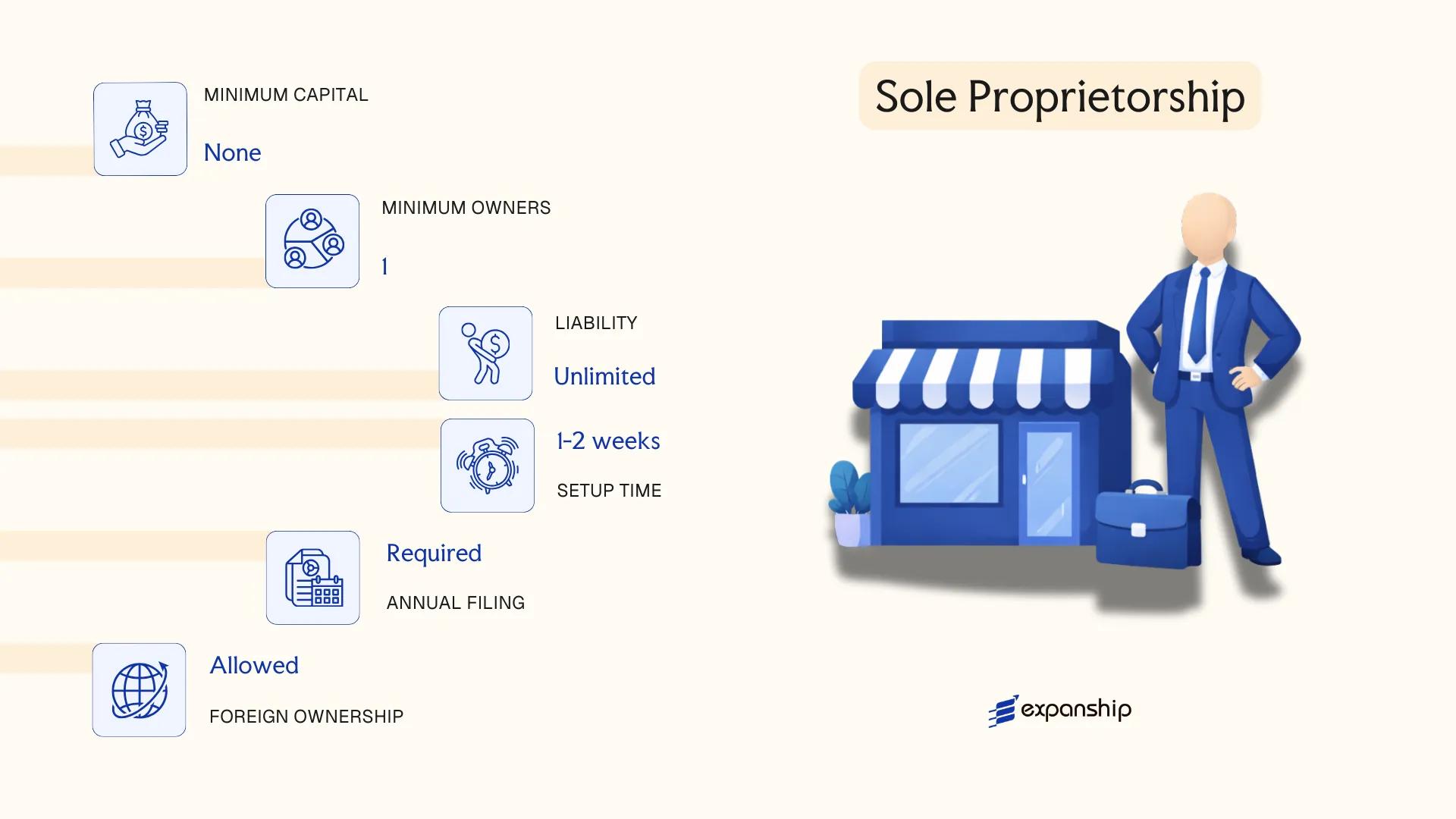

Sole Proprietorship [Eenmanszaak]

The Aruba Eenmanszaak sole proprietorship is the simplest business form available under Aruban law. It carries no separate legal personality — the proprietor and the business are treated as one and the same legal entity, meaning personal assets are directly exposed to business liabilities.

Registration is handled through the Aruba Chamber of Commerce and Industry (Kamer van Koophandel), which maintains the Commercial Register. Unlike capital-based structures, no minimum capital contribution is required to establish this form.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole Proprietorship (Eenmanszaak) | No separate legal personality |

| Members | One proprietor only | Cannot have co-owners; proprietor bears full personal liability |

| Local Presence | Registered business address in Aruba | Must be registered with the Chamber of Commerce |

| Capital | No statutory minimum | No paid-up capital requirement |

| Privacy | Proprietor's name appears on the Commercial Register | Limited privacy; publicly searchable |

Focus Points

- Taxation: Subject to personal income tax on business profits; no separate corporate tax filing; turnover tax (BBO) may apply depending on activity and revenue thresholds.

- Annual Compliance: Annual renewal of Chamber of Commerce registration is required to remain in good standing.

- Economic Substance: No substance requirements apply to this structure.

- Restrictions: Non-residents and foreign nationals may face eligibility constraints tied to residency or work permit status.

- Conversion: Can be converted into a VBA or NV, though this requires a formal incorporation process rather than a simple administrative filing.

Closing

This structure suits locally operating self-employed individuals and small-scale sole trader registration in Aruba where administrative simplicity outweighs the need for liability protection. The absence of minimum capital is a practical advantage, but unlimited personal liability remains a significant structural drawback for any business carrying financial or legal risk.

The Eenmanszaak is best suited for resident individuals operating as freelancers or small local traders who do not require liability separation.

How to Choose the Right Entity Type in Aruba

Selecting how to choose the right company structure in Aruba requires more than a cost comparison — the decision has direct legal, tax, and operational consequences that are difficult to reverse once a firm is registered.

Why Your Entity Choice Matters

An incorrect structure can produce concrete, costly outcomes:

- Registering an offshore entity while conducting local trade in Aruba places the business in breach of applicable commercial regulations, which can result in deregistration or administrative penalties.

- Choosing a tax-exempt entity when your business requires access to tax treaty benefits means withholding tax reductions in counterpart countries will not be available to you.

- Selecting a structure that carries mandatory audited financial statement requirements for a single-person consultancy creates recurring compliance costs that serve no regulatory purpose for that business model.

- Forming a standard company when a foundation would better serve asset protection or estate planning locks the structure into annual shareholder obligations that foundations do not carry.

Key Factors to Consider

- Business Activity: Passive asset-holding, active trading, and regulated sectors such as banking or insurance each point toward a distinct legal structure under Aruban law.

- Local vs. Offshore Operations: Transacting with Aruban residents requires a locally registered entity; purely offshore activity may permit lighter structures.

- Ownership and Management: Single-owner operations and multi-party arrangements have different governance requirements across entity types.

- Tax Objectives: Whether you require full exemption, a specific tax regime, or treaty eligibility determines which entity qualifies.

- Substance Capacity: If maintaining local employees, office space, and in-jurisdiction decision-making is not feasible for your business, the chosen structure must align with applicable substance thresholds.

- Exit Strategy: Redomiciliation, conversion, and voluntary winding-up procedures vary by entity type under Aruban corporate legislation.

Compliance Services for Companies in Aruba

Ongoing compliance support for Aruban entities, including annual filings, regulatory reporting, and substance requirements.

Conclusion

Aruba offers a defined set of legal structures, each suited to a distinct type of business activity. This incorporating a company in Aruba guide has covered the principal options available under local law. The NV suits larger enterprises requiring public capital access, while the VBA serves as the default for privately held companies with limited liability. Partnerships such as the VOF and CV fit smaller ventures where principals accept greater personal exposure. Branch offices and representative offices address foreign firms extending operations without forming a separate legal entity. The Eenmanszaak remains the simplest structure for individual traders.

Among registered entities, the VBA is the most commonly formed structure for both resident and non-resident businesses. Aruba's continued engagement with international tax transparency standards and its treaty network signal a regulatory direction aligned with OECD norms. Professional guidance through the registration process with the Aruba Chamber of Commerce reduces exposure to procedural delays and compliance gaps.

How Expanship Can Assist You

Expanship provides corporate services for Aruba company formation across the full range of entity types discussed in this guide — from the NV and VBA to branches and partnerships. Our team works directly with the Aruba Chamber of Commerce and Industry (Kamer van Koophandel en Nijverheid) to manage registration filings, documentation requirements, and post-incorporation obligations on your behalf.

From initial structuring to ongoing compliance, here is what our Aruba incorporation services cover:

- Preparation and legalization of incorporation documents

- Registered agent and registered office provision in Aruba

- Filing coordination with the Chamber of Commerce and relevant government authorities

- Post-incorporation compliance management, including annual reporting obligations

- Corporate secretarial support

- Banking introduction assistance for newly registered entities

Your business timeline and structure determine which of these services you will need. Expanship Aruba is available to discuss your specific situation.

Frequently Asked Questions (FAQ)

The Naamloze Vennootschap (NV) remains the most frequently incorporated structure, largely because it accommodates both resident and non-resident shareholders and supports a wide range of commercial activities. Its share capital flexibility and established legal framework under the Aruban Civil Code contribute to its broad adoption.

Both structures offer limited liability, but the VBA restricts share transferability and is generally used for closely held, domestically oriented businesses. The NV, by contrast, allows freely transferable shares and is more commonly used for international holding or investment purposes, though both structures are subject to Aruban corporate income tax.

The NV does not require shareholder details to appear in public-facing registry filings, making it the more privacy-oriented option between the two limited liability structures. Nominee shareholder arrangements are legally permissible, though ultimate beneficial ownership information must still be disclosed to the relevant authorities under Aruban AML regulations.

A sole proprietorship and an NV or VBA can each be formed by one individual. Partnerships — specifically the Vennootschap onder Firma (VOF) and Commanditaire Vennootschap (CV) — require a minimum of two partners, so single founders cannot use those structures.

Foreign nationals may form an NV or VBA without a residency requirement, and a branch office of a foreign entity may also be registered through the Aruba Chamber of Commerce. Certain regulated activities may require additional licensing from the Centrale Bank van Aruba, depending on the sector.

Aruban law permits the conversion of a VBA into an NV and vice versa through a formal legal process involving notarial deed amendment and re-registration with the Chamber of Commerce. Conversion between corporate entities and partnership structures is not a straightforward statutory process and typically requires dissolution and re-incorporation.

The NV, VBA, and registered branch office each carry distinct legal standing. Partnerships such as the VOF and CV do not possess full separate legal personality in the same sense — partners retain personal liability exposure, particularly in the VOF where all partners are jointly and severally liable.

Expanship's corporate services team works directly with the registration and compliance requirements described above, providing structured support across each stage of the incorporation process.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.