Key Takeaways

- Austria's Firmenbuch, administered through the federal court system, serves as the legally binding commercial register where all entity registrations take effect from the date of entry.

- The GmbH is Austria's most commonly registered entity, offering limited liability protection with manageable capital requirements suited to small and mid-sized businesses.

- Foreign companies can establish a presence in Austria without full incorporation through either a Zweigniederlassung (branch) or a Repräsentanzbüro (representative office), each carrying distinct regulatory obligations.

- Austria's available legal forms span incorporated structures such as the AG, GmbH, and SE, as well as unincorporated forms including the OG, KG, and Stille Gesellschaft, with each carrying specific implications for liability, governance, and taxation.

Introduction to Entity Types in Austria

Austria is a landlocked republic in Central Europe, sharing borders with Germany, Switzerland, Liechtenstein, Italy, Slovenia, Hungary, Slovakia, and the Czech Republic. As a member of the European Union and the Eurozone, it operates under a standard corporate tax framework with a territorial dimension, making it relevant for businesses seeking a regulated, treaty-connected European base.

Company registration and ongoing compliance fall under the jurisdiction of the Firmenbuch, Austria's commercial register administered through the federal court system. Entries are publicly accessible and legally binding from the date of registration.

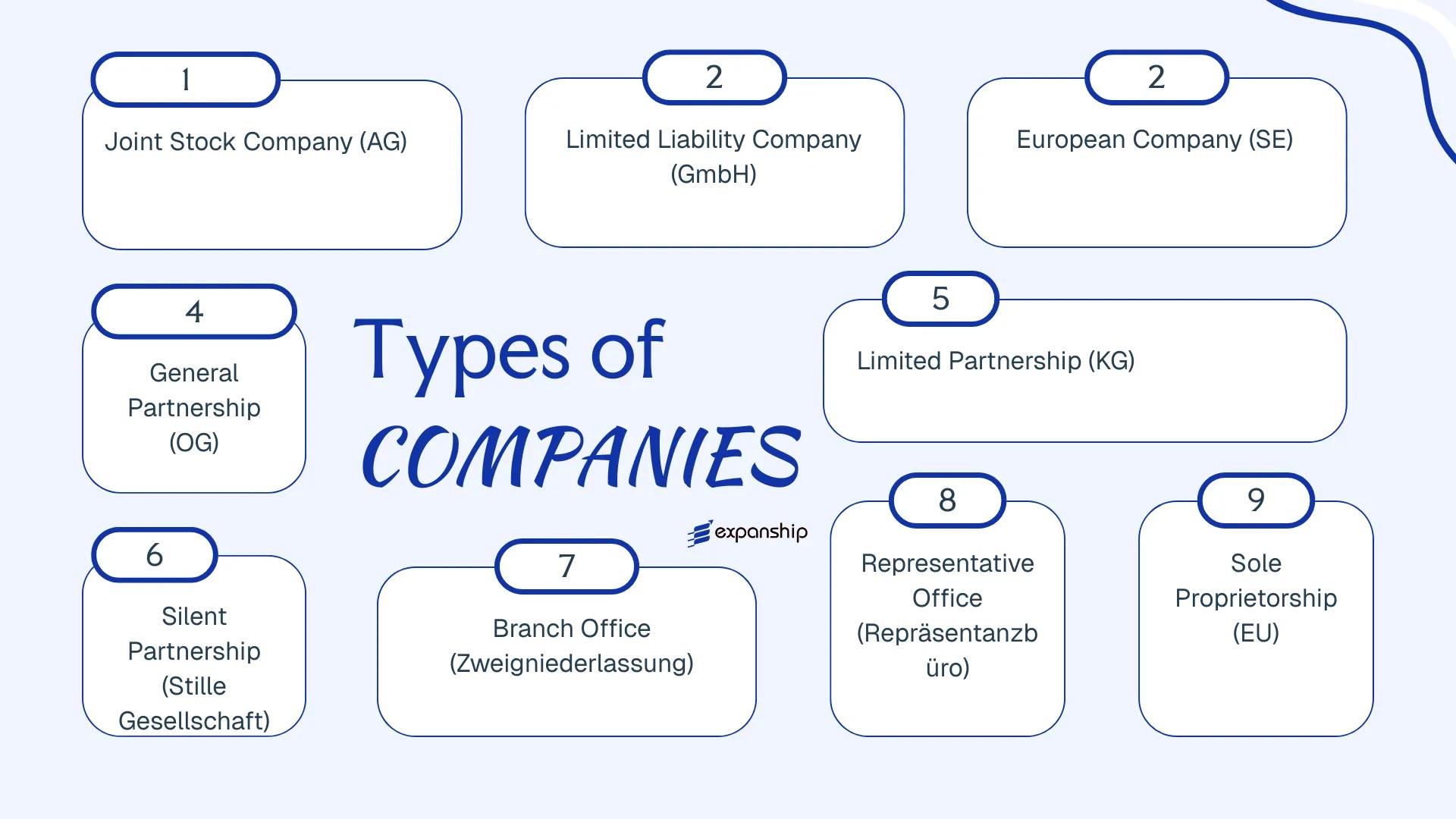

The types of business entities in Austria span both incorporated and unincorporated structures. Available legal forms include the Aktiengesellschaft (AG), Gesellschaft mit beschränkter Haftung (GmbH), Societas Europaea (SE), Offene Gesellschaft (OG), Kommanditgesellschaft (KG), Stille Gesellschaft, Zweigniederlassung, Repräsentanzbüro, and Eingetragener Unternehmer (EU). Each form carries distinct implications for liability, governance, minimum capital, and taxation. This article examines each structure in detail to help you determine which legal form fits your operational and compliance requirements.

An Overview of Business Structures in Austria

Austrian company law recognises several distinct entity types, each governed primarily by the Unternehmensgesetzbuch (UGB) and supplementary legislation such as the GmbH-Gesetz and the Aktiengesetz. The structural options range from sole proprietorships to European-level corporate forms, and each carries different implications for liability, taxation, and governance.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Aktiengesellschaft (AG) | Joint Stock Company | Limited to share capital | Taxed | Yes | 1 shareholder | Firmenbuch | Aktiengesetz 1965 |

| Gesellschaft mit beschränkter Haftung (GmbH) | Limited Liability Company | Limited to share capital | Taxed | Yes | 1 shareholder | Firmenbuch | GmbH-Gesetz |

| Societas Europaea (SE) | European Company | Limited to share capital | Taxed | Yes | 1 shareholder | Firmenbuch | SE-Verordnung (EC 2157/2001) |

| Offene Gesellschaft (OG) | General Partnership | Unlimited, joint and several | Taxed at partner level | Yes | 2 partners | Firmenbuch | UGB |

| Kommanditgesellschaft (KG) | Limited Partnership | Mixed | Taxed at partner level | Yes | 2 partners | Firmenbuch | UGB |

| Stille Gesellschaft | Silent Partnership | Limited to contribution | Taxed at partner level | Yes | 2 parties | Not registered | UGB |

| Zweigniederlassung | Branch Office | Parent bears liability | Taxed on local income | Yes | N/A | Firmenbuch | UGB |

| Repräsentanzbüro | Representative Office | Parent bears liability | Generally exempt | No | N/A | Wirtschaftskammer | UGB / Trade Law |

| Eingetragener Unternehmer (EU) | Sole Proprietorship | Unlimited personal liability | Taxed | Yes | 1 person | Firmenbuch | UGB |

Each of these structures is examined in full in the sections below.

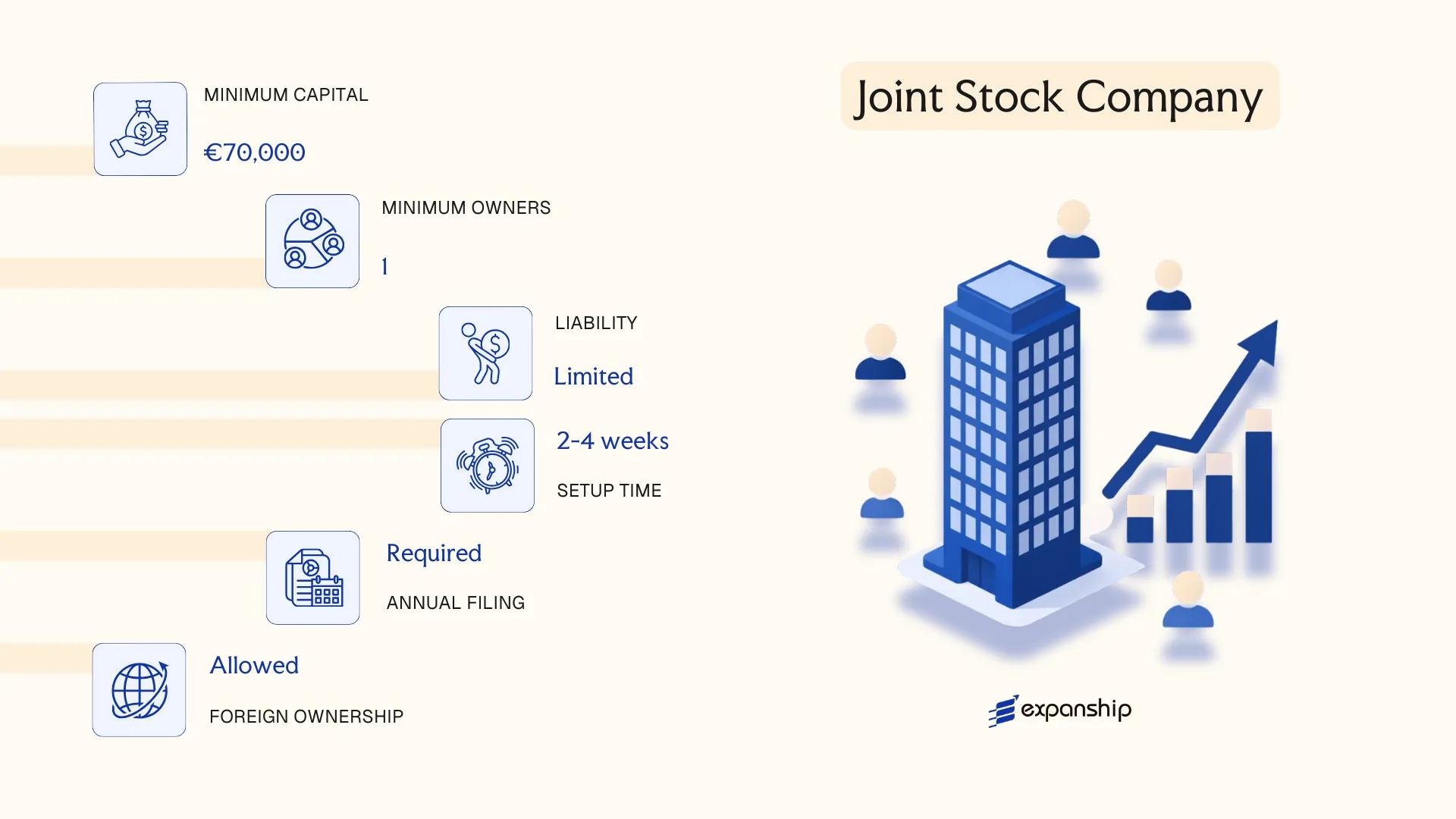

Aktiengesellschaft (AG) — Joint Stock Company

Aktiengesellschaft AG Austria formation is governed by the Aktiengesetz (AktG), enacted in 1965 and substantially amended over subsequent decades to align with EU corporate law directives. The AG carries separate legal personality, meaning the company's obligations are entirely distinct from those of its shareholders.

Shares in an AG are freely transferable by default, and the entity can be either publicly listed or privately held. This structural flexibility makes it a common vehicle for large enterprises, institutional investors, and businesses planning a future public offering.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Aktiengesellschaft (AG) | Governed by the Aktiengesetz (AktG) 1965 |

| Members | Shareholders (Aktionäre) | Minimum 1 shareholder; no maximum; shareholder identity not publicly disclosed for bearer shares if held via depository |

| Governing Bodies | Management Board (Vorstand) + Supervisory Board (Aufsichtsrat) | Supervisory Board mandatory; minimum 3 members; Vorstand manages day-to-day operations |

| Share Capital | EUR 70,000 minimum | At least 25% must be paid up at formation; shares can be registered (Namensaktien) or bearer (Inhaberaktien) |

| Local Presence | Registered office (Sitz) in Austria required | No mandatory local director, but Vorstand members are typically resident or accessible |

| Privacy | Shareholders not listed in the commercial register | Vorstand and Aufsichtsrat members are publicly registered in the Firmenbuch |

Focus Points

- Taxation: Subject to 23% corporate income tax; Austria's tax authority (Finanzamt) also applies 25% withholding tax on dividends, 20% VAT on standard supplies, and capital gains tax at the shareholder level; participation exemption may apply to qualifying dividend receipts.

- Annual Compliance: Annual financial statements must be audited and filed with the Firmenbuch; listed AGs follow additional disclosure obligations under the Börsegesetz.

- Economic Substance: No specific substance regime, but genuine management and control must align with Austrian tax residency claims.

- Treaty Access: Qualifies for benefits under Austria's extensive double taxation treaty network as a resident entity.

- Conversion: An AG can be converted into a GmbH or SE under the EU Cross-Border Conversion Directive as transposed into Austrian law.

Closing

The AG suits large-scale trading operations, holding structures, and businesses seeking access to capital markets, though its mandatory dual-board structure and EUR 70,000 minimum capital requirement make it administratively heavier than simpler corporate forms.

Best suited for large enterprises, institutional investors, or businesses with plans for a public listing or significant external investment rounds.

Company Incorporation in Austria

Incorporate your Austrian AG or other entity type with end-to-end support from Expanship.

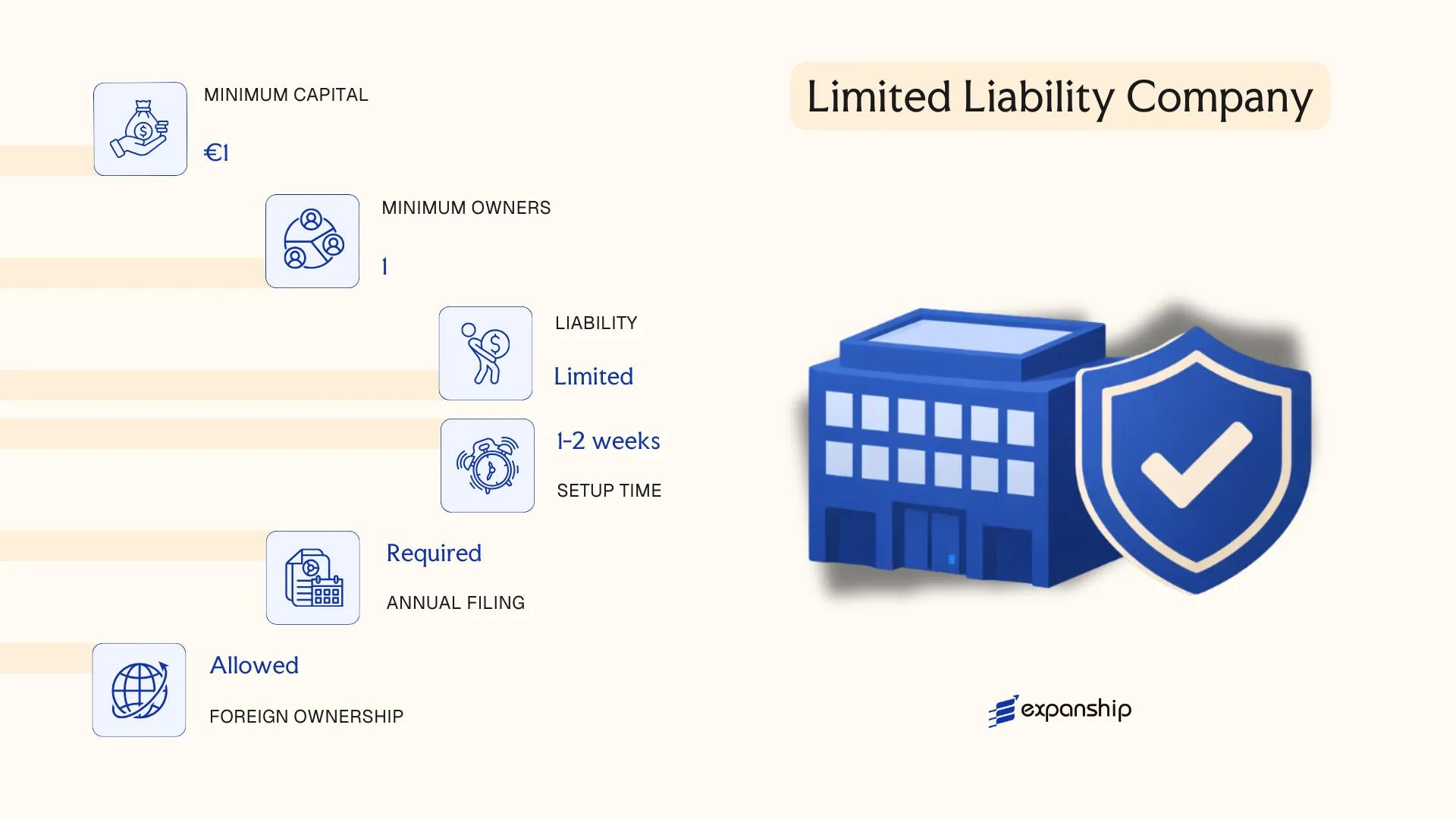

Gesellschaft mit beschränkter Haftung (GmbH) — Limited Liability Company

The GmbH Austria limited liability company is governed by the GmbH-Gesetz (GmbHG), enacted in 1906 and substantially amended over the decades. It holds separate legal personality, meaning the entity itself — not its shareholders — bears contractual obligations and liabilities.

Shareholders' exposure is capped at their respective capital contributions. This hybrid structure combines the liability protection of a corporation with the operational flexibility typically associated with smaller private firms, making it the most widely used commercial entity form in the country.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Gesellschaft mit beschränkter Haftung (GmbH) | Private limited liability company; not publicly traded |

| Members | 1–50 shareholders; managed by one or more Geschäftsführer (managing directors) | Shareholders and directors may be the same person; no nationality restriction |

| Local Presence | Registered office (Sitz) in Austria required; no mandatory resident director | A registered address must appear in the Firmenbuch |

| Share Capital | Minimum EUR 35,000; at least half must be paid up at incorporation | Cash or in-kind contributions permitted; Stammkapital term used in statute |

| Privacy | Shareholder and director details filed in the Firmenbuch (commercial register) | The register is publicly accessible |

Focus Points

- Taxation: Subject to 24% corporate income tax (KöSt) on worldwide profits; standard VAT rate of 20% applies; withholding tax of 27.5% on dividend distributions to non-residents, subject to applicable double tax treaty reductions; no stamp duty on share transfers.

- Annual Compliance: Annual financial statements must be filed with the Firmenbuch; audit required once the entity exceeds two of three statutory thresholds (turnover, balance sheet total, headcount).

- Economic Substance: No formal substance test under domestic law, though tax residency and transfer pricing rules require genuine management and control to be exercised from Austria.

- Treaty Access: Qualifies for Austria's extensive tax treaty network (90+ treaties) and EU directives, including the Parent-Subsidiary Directive.

- Conversion: A GmbH may be converted into an AG under the Umwandlungsgesetz without liquidation, subject to meeting the AG's minimum capital threshold.

Closing

The GmbH suits trading operations, holding structures, and IP-holding vehicles where limited liability and private ownership are priorities. Its principal constraint is the EUR 35,000 minimum capital requirement, which raises the initial cost of formation relative to some other jurisdictions.

The GmbH is best suited for small to mid-sized businesses, joint ventures, and foreign investors seeking a privately held Austrian operating or holding entity with clearly defined liability boundaries.

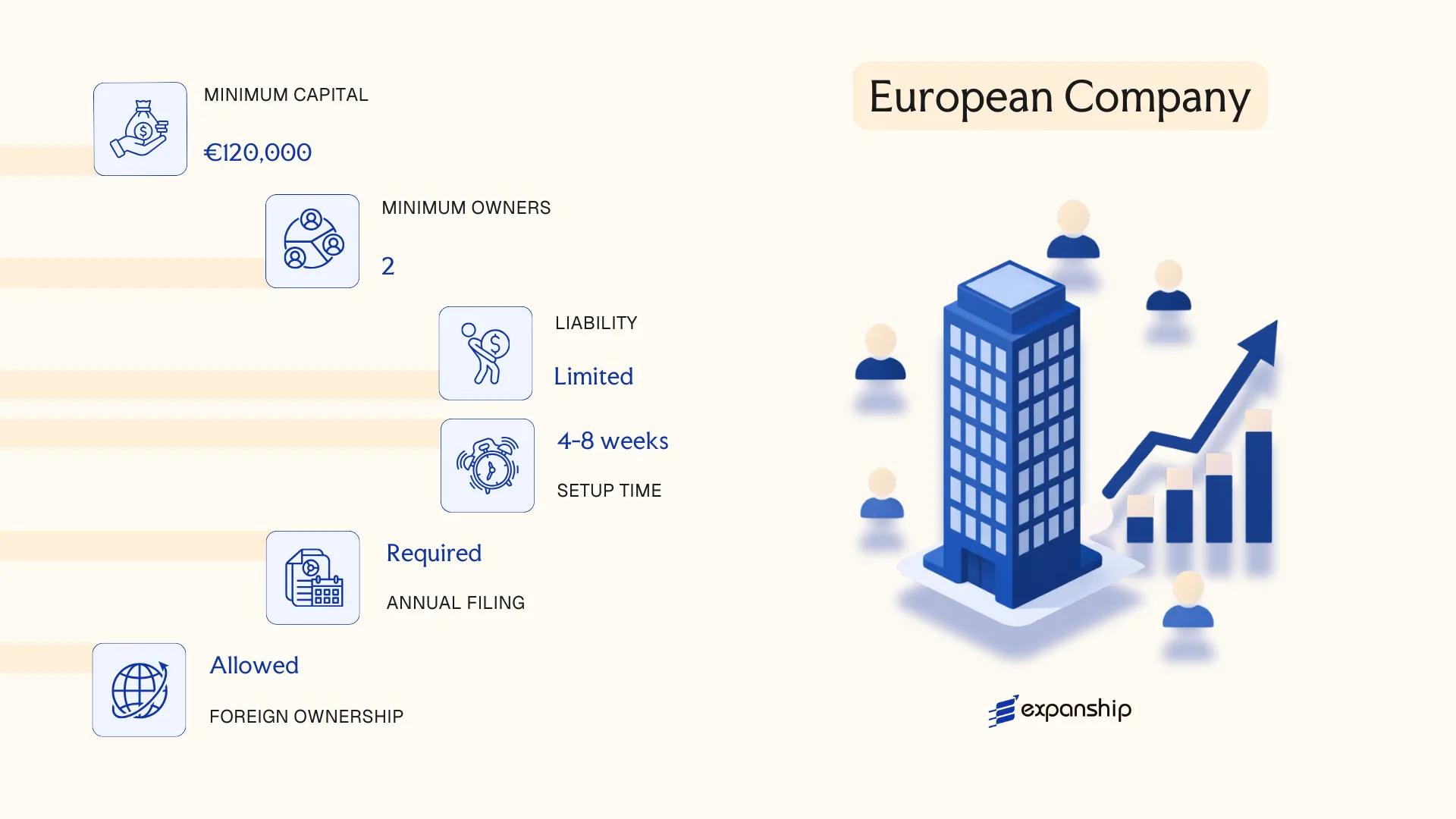

Societas Europaea (SE) — European Company

Societas Europaea SE registration Austria falls under Council Regulation (EC) No 2157/2001, supplemented by the Austrian SE-Gesetz (SEG), which implements the EU directive at the national level. The SE carries separate legal personality and offers shareholders limited liability, making its structural profile broadly comparable to an AG — the national joint stock company form it most closely mirrors.

Formation, however, follows distinctly supranational rules. SE formation Austria cross-border rules require that the entity arise through a prescribed EU-level procedure: merger of companies from at least two member states, formation of a holding SE, conversion of an existing AG, or establishment as a subsidiary SE. A purely domestic formation without a cross-border element is not permitted.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Societas Europaea (SE) | Governed by EC Reg. 2157/2001 and Austrian SEG |

| Members Referred As | Shareholders (Aktionäre); Directors (Vorstand / Aufsichtsrat or Administrative Board) | Two-tier or one-tier board structure available |

| Minimum Members | 1 shareholder (post-formation) | Cross-border element required at formation stage |

| Registered Office | Must be in Austria if incorporated here; must match place of real administration | Registered office and head office must coincide under EU rules |

| Share Capital | Minimum EUR 120,000 fully subscribed | Same minimum as the AG |

| Privacy | Shareholder register not publicly disclosed; board members filed with Firmenbuch | Beneficial ownership registered with WiEReG |

Focus Points

- Taxation: Subject to Austrian corporate income tax at 23% (as of 2024); VAT registration obligations apply in the standard manner; withholding tax on dividends generally 27.5%, reducible under applicable tax treaties or the EU Parent-Subsidiary Directive.

- Employee Involvement: SE formation triggers mandatory negotiation of employee involvement arrangements under the Austrian SE-Mitbestimmungsgesetz; this can extend the formation timeline significantly.

- Annual Compliance: Annual financial statements must be prepared and filed with the Firmenbuch; audit requirements apply as for an AG.

- Conversion: An SE registered in Austria may convert into an Austrian AG without dissolution or loss of legal personality, and vice versa.

- Seat Transfer: The SE's registered office may be transferred to another EU member state without dissolving the entity — a structural option unavailable to purely national company forms.

Closing

The SE suits multinational groups seeking a pan-European holding or operational vehicle with the flexibility to relocate the registered seat across the EU without restructuring. The seat-transfer facility is its principal structural advantage; the mandatory employee involvement process and the EUR 120,000 minimum capital requirement are practical constraints that make it less accessible for smaller businesses.

The SE is best suited for established multinational businesses or groups already operating across multiple EU member states that require a unified European legal structure with cross-border mobility.

Partnerships in Austria [Offene Gesellschaft (OG), Kommanditgesellschaft (KG), Stille Gesellschaft]

Austrian partnership structures in Austria OG KG are governed primarily by the Unternehmensgesetzbuch (UGB), which came into force in 2007, replacing the earlier Handelsgesetzbuch. The UGB regulates both the Offene Gesellschaft (OG) and the Kommanditgesellschaft (KG), while the Stille Gesellschaft operates as a contractual arrangement without separate legal personality.

Each structure differs in how liability is allocated among participants. The OG exposes all partners to unlimited joint liability, whereas the KG separates at least one general partner bearing unlimited liability from one or more limited partners whose exposure is capped at their registered capital contribution.

Key Characteristics

| Requirement | OG | KG | Stille Gesellschaft |

|---|---|---|---|

| Legal Form | General partnership; no separate legal personality | Limited partnership; no separate legal personality | Silent/contractual partnership; no legal personality |

| Members | Partners (Gesellschafter); minimum 2, no maximum | General partner (Komplementär) min. 1 + limited partner (Kommanditist) min. 1; no maximum | Proprietor (business owner) + silent partner (stiller Gesellschafter); minimum 2 |

| Local Presence | Registered office in Austria required; entry in Firmenbuch (commercial register) mandatory | Registered office in Austria required; entry in Firmenbuch mandatory | No registration required; governed by private contract |

| Capital | No statutory minimum capital | No statutory minimum; limited partner's contribution (Haftsumme) must be registered | No statutory minimum; contribution terms set contractually |

| Liability | All partners: unlimited, joint and several | Komplementär: unlimited; Kommanditist: limited to registered Haftsumme | Silent partner: limited to contribution; business owner: unlimited |

| Privacy | Partner names disclosed in Firmenbuch | Partner names and Haftsumme disclosed in Firmenbuch | Arrangement is private; not publicly disclosed |

Focus Points

- Taxation: OG and KG are fiscally transparent — profits pass through to partners and are taxed at the individual or corporate level depending on partner type; no entity-level corporate income tax applies. VAT registration obligations follow standard Austrian rules under the Umsatzsteuergesetz (UStG). The Stille Gesellschaft is similarly transparent, with the silent partner taxed on their profit share as passive income.

- Annual Compliance: OG and KG must file annual financial statements with the Firmenbuch if they meet size thresholds under the UGB; smaller partnerships have reduced obligations.

- Treaty Access: Pass-through treatment may complicate access to Austria's double tax treaty network, as treaty eligibility generally requires the income recipient to be a taxable entity.

- Conversion: Both OG and KG can be converted into a GmbH or AG under the Umwandlungsgesetz (UmwG) without full dissolution.

Sub-Types

GmbH & Co KG

A widely used hybrid where a GmbH acts as the sole Komplementär, effectively capping unlimited liability exposure. This structure is common for family businesses and real estate holdings where partners want limited liability at the general partner level without incorporating a full share-capital entity.

Atypische stille Gesellschaft

Distinguished from the standard Stille Gesellschaft by granting the silent partner participation in asset appreciation and losses, not only profits. This variant is frequently used in structured finance and employee participation arrangements.

Closing

Partnership structures suit professional service firms, family-owned trading operations, and real estate joint ventures where pass-through taxation is operationally preferable. The absence of minimum capital requirements reduces entry barriers, though unlimited liability for general partners remains a substantive structural risk that requires careful contractual planning.

OG and KG structures are best suited for domestic partnerships, family businesses, or professional firms where the partners accept personal liability or can mitigate it through a GmbH & Co KG arrangement.

Foreign Business Presence in Austria [Zweigniederlassung, Repräsentanzbüro]

Establishing a foreign company branch office Austria requires registration under the Austrian Commercial Code (Unternehmensgesetzbuch, UGB) and the Act on Business Licensing (Gewerbeordnung, GewO 1994). A branch (Zweigniederlassung) is not a separate legal entity — it remains an extension of the parent company, which retains full liability for its operations.

Registration for a Zweigniederlassung Austria registration is handled through the Austrian commercial court (Firmenbuch), which maintains the public register. The representative office (Repräsentanzbüro), by contrast, is not registered in the Firmenbuch and is restricted to auxiliary activities such as market research and liaison functions.

Key Characteristics

| Requirement | Zweigniederlassung (Branch) | Repräsentanzbüro (Rep Office) |

|---|---|---|

| Legal Personality | None — extension of parent | None — extension of parent |

| Registration | Firmenbuch (commercial register) | No formal registration required |

| Permitted Activities | Full commercial operations | Non-commercial, auxiliary only |

| Local Representative | Mandatory Austrian-resident representative | Not legally mandated |

| Capital Requirement | None separate from parent | None |

| Liability | Parent bears full liability | Parent bears full liability |

Focus Points

- Taxation: The branch is subject to Austrian corporate income tax (25% standard rate) on locally sourced profits; VAT registration is required if turnover thresholds are met; withholding tax may apply to profit remittances depending on applicable double tax treaties.

- Economic Substance: The branch must maintain a genuine operational presence; purely nominal offices risk reclassification.

- Annual Compliance: Branches must file annual financial statements in Austria, mirroring the parent's accounts where required by the Firmenbuch.

- Treaty Access: Access to Austria's tax treaty network depends on the parent entity's jurisdiction and treaty terms.

- Restrictions: The Repräsentanzbüro cannot invoice clients, generate revenue, or conclude contracts on behalf of the parent.

Closing

A branch suits foreign firms testing the Austrian market or executing contracts locally, though the absence of liability separation from the parent is a meaningful structural exposure. Opening a branch in Austria as a foreign company avoids the capitalisation requirements of a subsidiary but transfers full legal and financial risk to the parent entity.

Foreign companies seeking an operational presence in Austria without incorporating a separate subsidiary, provided the parent is comfortable bearing direct liability for local activities.

Eingetragener Unternehmer (EU) — Sole Proprietorship

The Eingetragener Unternehmer sole proprietorship Austria is the simplest form of business registration available to individuals operating commercially under Austrian law. Governed by the Unternehmensgesetzbuch (UGB), the commercial code that came into force in 2007, this structure carries no separate legal personality — the proprietor and the business are one and the same legal entity.

Because there is no liability shield, your personal assets are fully exposed to business creditors. Registration is mandatory once annual turnover exceeds EUR 700,000 (measured over two consecutive financial years), though voluntary registration is permitted below that threshold.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole Proprietorship (no separate legal personality) | Proprietor bears unlimited personal liability |

| Member Title | Proprietor (Einzelunternehmer) | Only one individual; no minimum capital contribution required |

| Registered Office | Business address in Austria required | Must be registerable with the Firmenbuch (commercial register) |

| Capital | No minimum capital requirement | No share structure; personal assets fund the business |

| Privacy | Name and address published in the Firmenbuch | Limited privacy; public register entries are freely searchable |

Focus Points

- Taxation: Subject to personal income tax (Einkommensteuer) at progressive rates up to 55%; VAT registration required once turnover exceeds EUR 35,000 annually; no corporate tax applies; no withholding tax on profit withdrawals as there are no dividends.

- Annual Compliance: Bookkeeping obligations depend on turnover thresholds under the UGB; above EUR 700,000, full double-entry accounting is required.

- Treaty Access: As a pass-through structure, treaty benefits apply at the individual proprietor level under Austria's bilateral tax treaty network.

- Conversion: Can be converted into a GmbH or other capital structure, though the process requires formal restructuring and new registration with the Firmenbuch.

Closing Remarks

This structure suits freelancers, tradespeople, and small-scale commercial operators who want a low-cost entry point without governance formalities. The absence of minimum capital is its clearest practical advantage; unlimited personal liability remains the defining constraint.

Resident individuals conducting low-risk, single-operator commercial activity who do not require a liability shield or external investor participation.

How to Choose the Right Entity Type in Austria

Knowing how to choose a company type in Austria requires more than comparing registration fees — the structural decision has legal, tax, and operational consequences that persist for the life of the business.

Why Your Entity Choice Matters

Choosing the wrong entity structure produces concrete, correctable-but-costly outcomes:

- Forming a GmbH when a branch (Zweigniederlassung) suffices for your operational model means bearing the full capital requirement of EUR 10,000 and ongoing annual filing obligations that branches are not subject to in the same form.

- Selecting an entity without qualifying as a tax resident can disqualify your business from accessing Austria's double taxation treaty network, preventing withholding tax reductions in counterpart countries.

- Registering a sole proprietorship (Eingetragener Unternehmer) when your activity requires a licensed trade under the Gewerbeordnung 1994 results in operating without valid authorization, which can lead to administrative penalties or forced cessation.

- Choosing an AG when a single-person consultancy is the actual model introduces mandatory supervisory board requirements and audit obligations that generate disproportionate annual compliance costs.

Key Factors to Consider

- Business Activity: Active trading, passive asset-holding, and regulated sectors such as banking or insurance each point toward a different permitted structure under Austrian commercial law.

- Ownership and Management: A sole founder with no co-investors may find the GmbH's flexible single-director structure more practical than the AG's mandatory two-tier governance model.

- Tax Objectives: Your need for full corporate tax residency, participation exemption eligibility, or access to the EU Parent-Subsidiary Directive will determine whether a capital company is required.

- Substance Capacity: If you cannot maintain genuine management and decision-making activity locally, the entity type chosen must still satisfy the economic substance expectations applied by Austrian tax authorities.

- Exit Strategy: Not all Austrian entity types permit redomiciliation or conversion without dissolution; the Societas Europaea offers cross-border seat transfer options that domestic entities do not.

- Privacy Requirements: Beneficial ownership data is disclosed to the Wirtschaftseigentümer Register (WiEReG) regardless of entity type, but the extent of public register disclosure varies by structure.

Compliance Services for Companies in Austria

Ongoing compliance support for Austrian entities, including annual filing, WiEReG reporting, and regulatory monitoring.

Conclusion

Austria offers a defined set of legal structures, each suited to a distinct operational and ownership profile. This setting up a company in Austria guide has covered the full spectrum: the GmbH remains the most registered entity in the country, favored by small and mid-sized firms for its manageable capital requirements and liability protection. The AG suits larger enterprises requiring access to capital markets. Partnerships such as the OG and KG serve businesses where personal involvement and shared liability align with the operating model. The SE addresses cross-border European structures, while the Zweigniederlassung and Repräsentanzbüro give foreign firms a regulated path to local presence without full incorporation.

Regulated by the Firmenbuch and overseen through established commercial law, Austria's corporate framework continues to attract international business, supported by a broad double taxation treaty network. Your choice of structure shapes everything from governance to tax treatment.

How Expanship Can Assist You

Austria company formation services through Expanship cover the full registration process, from selecting the right entity — a GmbH, AG, SE, or registered partnership — through to filing with the Firmenbuch, Austria's commercial register maintained by the regional courts. Every structure discussed in this guide carries distinct obligations, and Expanship's support is calibrated to those specifics rather than a generic process.

From the outset, your business receives hands-on assistance across each practical stage of incorporation and ongoing compliance.

- Document preparation and notarization support

- Registered office and local agent provision

- Firmenbuch filing and court liaison

- Post-incorporation compliance management

- Banking introduction assistance

- Ongoing registered agent services

Ready to move forward? Contact Expanship Austria to discuss your setup directly.

Frequently Asked Questions (FAQ)

The Gesellschaft mit beschränkter Haftung (GmbH) is the most frequently incorporated entity, primarily because it combines limited liability with relatively straightforward governance requirements. A minimum share capital of EUR 35,000 is required, and a single shareholder suffices for formation.

Both structures carry limited liability, but an AG is subject to considerably stricter regulatory obligations, including mandatory supervisory board requirements once certain employee or capital thresholds are met. For frequently asked questions about Austria GmbH setup, the key distinction is that the GmbH suits closely held businesses, whereas the AG is structured for entities seeking public capital markets access.

The Stille Gesellschaft provides the greatest degree of confidentiality, as the silent partner's involvement is not registered in the Firmenbuch (commercial register). Nominee arrangements are permissible in principle, though Austrian beneficial ownership disclosure rules under the Wirtschaftliche Eigentümer Registergesetz (WiEReG) still require ultimate beneficial owners to be registered in the WiEReG register.

A sole individual can form a GmbH, AG, or Eingetragener Unternehmer (EU). Partnerships such as the Offene Gesellschaft (OG) and Kommanditgesellschaft (KG) require a minimum of two partners by definition under the UGB. The Societas Europaea (SE) requires specific cross-border formation conditions and cannot be established domestically from scratch by one person.

Non-residents may establish a GmbH, AG, or SE without restrictions on nationality. Foreign nationals are permitted to serve as shareholders and, in most cases, as managing directors, though residency-based practical considerations around notarisation and bank account opening may apply. The Zweigniederlassung (branch) is also available to foreign companies seeking a registered presence without forming a separate legal entity.

Austrian law permits certain structural transformations (Umwandlung) under the Umwandlungsgesetz (UmwG), including conversion of a GmbH into an AG and vice versa. A sole proprietorship (EU) may also be converted into a capital company under applicable transformation provisions. Not all conversions are available between every entity type, so the specific path depends on the structures involved.

The GmbH, AG, and SE each hold full legal personality distinct from their shareholders. General partnerships (OG) and limited partnerships (KG) also have legal capacity under the UGB, meaning they can enter contracts and hold assets in their own name. The Stille Gesellschaft, by contrast, has no independent legal standing — it exists solely as a contractual arrangement between the silent partner and the active business.

The Eingetragener Unternehmer (EU) carries the lightest compliance burden, with no mandatory annual financial statements filed to the Firmenbuch for smaller operators and no minimum capital requirement. Austrian business entity questions about reduced reporting often point to the EU as the default answer for individual traders, though this structure offers no liability separation from the proprietor's personal assets.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.