Key Takeaways

- The LLC is the most commonly registered entity type in American Samoa, favored for its combination of operational flexibility and pass-through tax treatment.

- Corporations, whether structured as C Corporations or S Corporations, are better suited to businesses requiring formal capital structures and shareholder-level limited liability protections under American Samoan law.

- General partnerships expose partners to unlimited personal liability, limiting their practical use to specific professional arrangements in the territory.

- Business registration and licensing in American Samoa falls under the Department of Commerce, operating within a tax regime that differs from the U.S. federal system and includes incentive structures administered by the American Samoa Economic Development Authority.

Introduction to Entity Types in American Samoa

Located in the South Pacific Ocean, American Samoa is an unincorporated territory of the United States situated approximately 2,600 miles southwest of Hawaii, within the Samoan island group. Its political status as a U.S. territory means federal law applies in certain areas, while the territory retains its own legislative framework governing local commercial activity.

Business registration falls under the jurisdiction of the American Samoa Government's Office of the Governor and its associated regulatory divisions, with the Department of Commerce playing a central role in business licensing and compliance. The territory operates under a tax regime that differs from the U.S. federal system, with qualified businesses potentially subject to reduced tax rates under local tax incentive structures administered by the American Samoa Economic Development Authority.

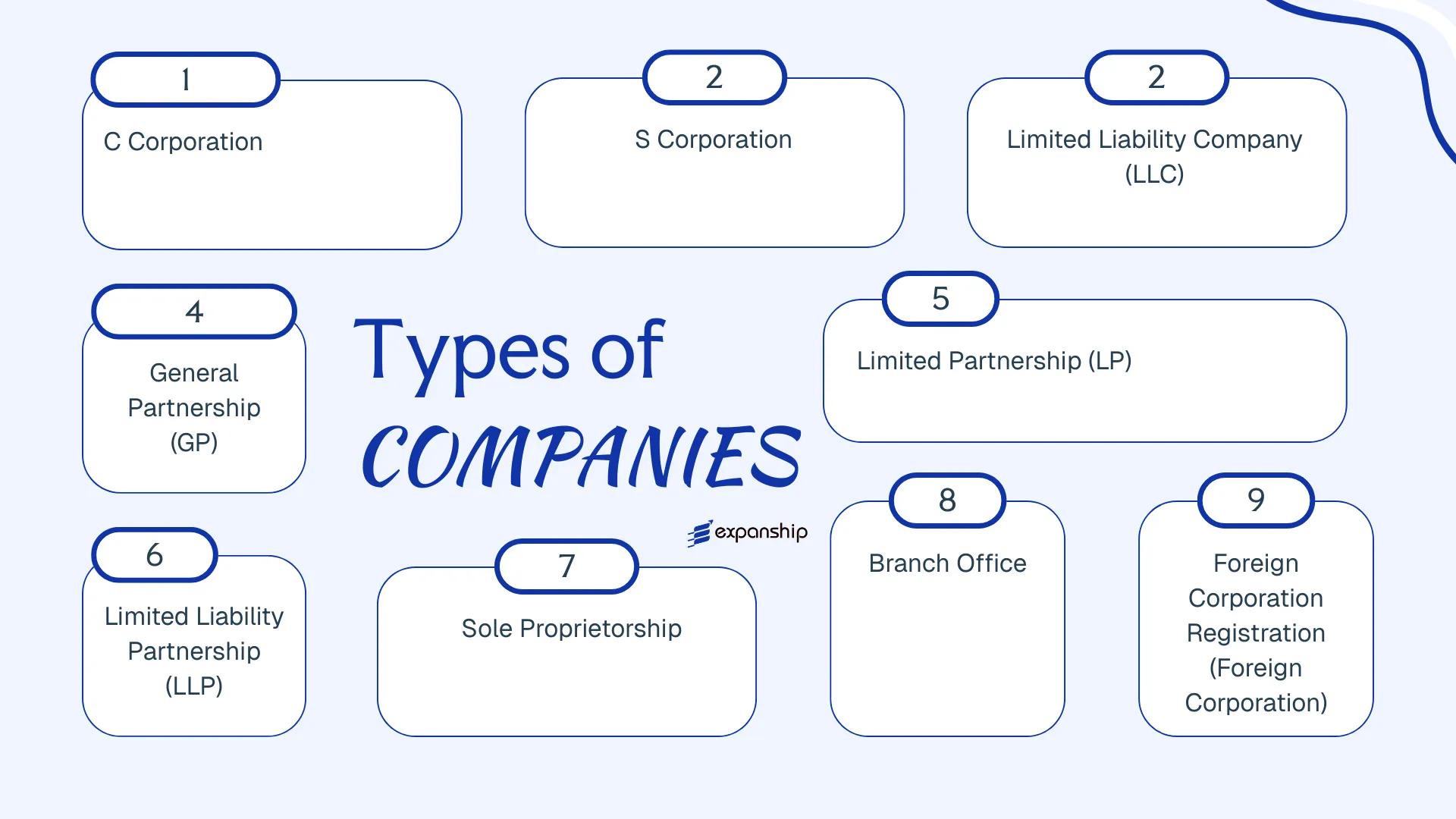

Several business entity types are available under American Samoan law, including the C Corporation, S Corporation, Limited Liability Company, General Partnership, Limited Partnership, Limited Liability Partnership, Sole Proprietorship, Branch Office, and Foreign Corporation. Each structure carries distinct implications for liability, governance, and taxation. This article examines each of these options in detail to help you determine which formation best suits your commercial objectives.

An Overview of Business Structures in American Samoa

American Samoa business structures overview encompasses several distinct entity types, each governed primarily by the American Samoa Code Annotated (ASCA) Title 27, which addresses business organizations and related commercial activity. The territory's framework accommodates both resident and foreign-owned enterprises through separate formation pathways. Each structure carries different implications for liability, taxation, and operational scope.

| Entity Type | Legal Form | Liability | Tax Treatment | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| C Corporation | Separate legal entity | Limited to investment | Subject to local tax | Permitted | 1 shareholder | ASG Office of the Governor | ASCA Title 27 |

| S Corporation | Pass-through entity | Limited to investment | Federal pass-through | Permitted | 1–100 shareholders | ASG / IRS rules apply | ASCA Title 27 |

| LLC | Hybrid legal entity | Members not liable | Flexible / pass-through | Permitted | 1 member | ASG Office of the Governor | ASCA Title 27 |

| General Partnership | Unincorporated firm | Unlimited personal | Pass-through | Permitted | 2 partners | ASG Office of the Governor | ASCA Title 27 |

| Limited Partnership | Unincorporated firm | Mixed (general/limited) | Pass-through | Permitted | 2 partners | ASG Office of the Governor | ASCA Title 27 |

| LLP | Registered partnership | Partners partially shielded | Pass-through | Permitted | 2 partners | ASG Office of the Governor | ASCA Title 27 |

| Sole Proprietorship | Unincorporated individual | Unlimited personal | Personal income tax | Permitted | 1 owner | ASG Business License Office | ASCA Title 27 |

| Branch Office | Extension of foreign entity | Parent bears liability | Subject to local tax | Permitted | N/A | ASG Office of the Governor | ASCA Title 27 |

| Foreign Corporation | Registered foreign entity | Limited to investment | Subject to local tax | Permitted | 1 shareholder | ASG Office of the Governor | ASCA Title 27 |

Each of these structures is examined in full in the sections below.

Corporation (C Corporation, S Corporation)

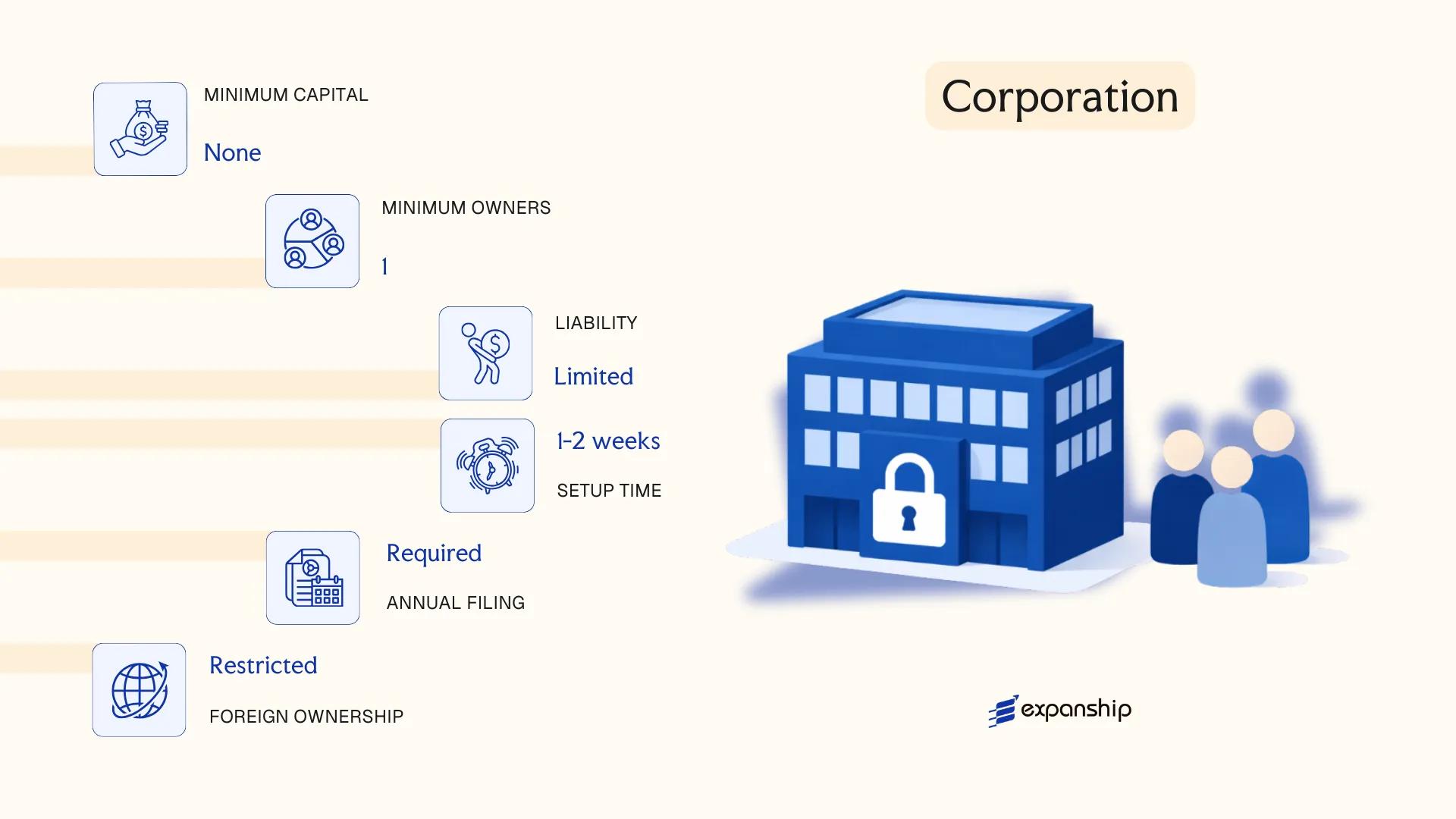

American Samoa corporation registration is governed by the American Samoa Code Annotated (ASCA), which provides the statutory framework for forming and operating corporations in the territory. A corporation is a separate legal entity, distinct from its shareholders, and confers limited liability on its members by default.

Corporations in the territory may be structured as either C corporations or S corporations, each carrying different tax treatment implications. Both forms share the same foundational corporate structure under territorial law but diverge primarily in how income is reported and taxed at the federal level.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Corporation | Separate legal personality; governed under ASCA |

| Members | Shareholders (directors, officers) | Minimum 1 shareholder; no statutory maximum |

| Local Presence | Registered agent required | Physical registered office address in American Samoa required |

| Capital | USD; no statutory minimum | Authorized capital stated in articles of incorporation |

| Privacy | Shareholder names filed with government | Directors and officers generally on public record |

Focus Points

- Taxation: C corporations are subject to American Samoa local income tax; S corporations pass income through to shareholders, avoiding entity-level federal tax, though territorial tax obligations still apply. No VAT or GST exists in the territory.

- Annual Compliance: Annual reports and renewal fees are required to maintain good standing with the American Samoa Government.

- Restrictions: S corporation eligibility requires shareholders to be U.S. citizens or resident aliens; non-resident alien shareholders disqualify the election.

- Conversion: A corporation may convert between C and S status subject to IRS eligibility rules; territorial filings are separate from federal elections.

Sub-Types

C Corporation

A C corporation in American Samoa is taxed as a standalone entity, with profits subject to taxation at both the corporate and, upon distribution, shareholder level. This structure is commonly used for businesses seeking investment capital or planning for eventual public offering.

S Corporation

An S corporation passes income, losses, and deductions directly to shareholders' personal tax returns, avoiding double taxation at the corporate level. It suits closely held businesses with a limited number of qualifying shareholders.

Use Cases and Considerations

Corporations suit trading operations, holding structures, and businesses requiring a recognized, liability-shielded form for institutional counterparties. The primary advantage is the clear separation of personal and business liability; the key limitation is the administrative burden of maintaining corporate formalities and dual-layer filing obligations.

This structure is best suited for businesses with multiple investors, growth ambitions, or those requiring a formal corporate identity for contracts and financing.

Company Incorporation in American Samoa

Limited Liability Company (LLC)

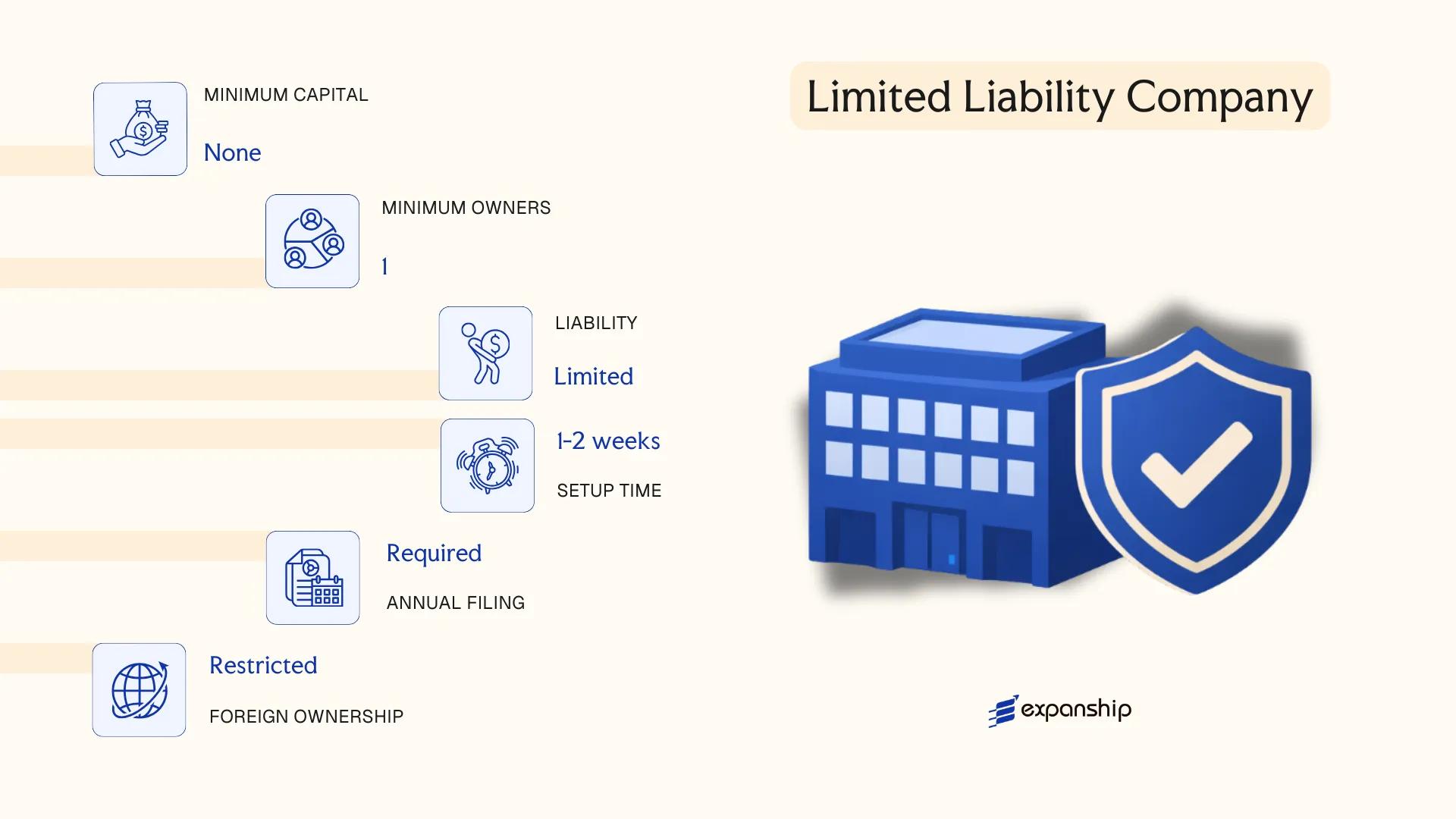

American Samoa LLC formation is governed by the American Samoa Limited Liability Company Act, which establishes the LLC as a distinct legal entity separate from its members. The structure combines the liability protection of a corporation with the pass-through flexibility typical of a partnership.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Separate legal entity | Members are not personally liable for company debts |

| Members | Referred to as Members | Minimum 1 member; no statutory maximum; members can be individuals or entities of any nationality |

| Management | Member-managed or Manager-managed | Managers need not be members |

| Local Presence | Registered Agent and Registered Office required | Must maintain a physical address in American Samoa |

| Capital | USD; no statutory minimum | Contributions may be cash, property, or services |

| Privacy | Member names not publicly disclosed on the register | Operating agreement is a private document |

Focus Points

- Taxation: LLCs are generally treated as pass-through entities for U.S. federal tax purposes; members report income on personal returns, though American Samoa applies its own territorial tax regime mirroring the U.S. Internal Revenue Code with local modifications.

- Annual Compliance: Annual report filings and maintenance of a registered agent are required to keep the entity in good standing.

- Economic Substance: No formal economic substance regime comparable to some offshore jurisdictions currently applies.

- Treaty Access: American Samoa is a U.S. territory but is not covered by U.S. tax treaties; treaty access is limited.

- Conversion: Conversion from an LLC to another entity type is permissible under local statute, subject to procedural requirements.

Closing

An LLC suits holding structures, small trading operations, and professional services where members prefer liability protection without corporate formality. The pass-through tax treatment is a practical advantage, though the territory's exclusion from U.S. tax treaty networks limits its utility for cross-border tax planning.

This structure suits entrepreneurs and small-to-mid-size businesses seeking liability protection with minimal administrative overhead, particularly those operating within the territory or under U.S. federal tax frameworks.

Partnerships [General Partnership, Limited Partnership, Limited Liability Partnership]

American Samoa partnership registration is governed by the Revised Uniform Partnership Act as adopted under local territorial law, alongside provisions in the American Samoa Code Annotated (ASCA). Partnerships in the territory are generally treated as pass-through entities, meaning profits and losses flow directly to the partners rather than being taxed at the entity level.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Partnership (GP, LP, or LLP) | LP and LLP offer greater liability protection than a GP |

| Members | Partners; no statutory maximum | GP requires minimum 2 general partners; LP requires at least 1 general and 1 limited partner |

| Local Presence | Registered agent and principal office in American Samoa | Required for service of process |

| Capital | USD; no prescribed minimum | Contributions defined by partnership agreement |

| Privacy | Partner details filed with registrar | Limited public disclosure requirements |

Focus Points

- Taxation: Partnerships are pass-through entities; partners are taxed individually on their share of income under American Samoa's territorial tax system, which mirrors the U.S. Internal Revenue Code with local modifications. No separate entity-level income tax, VAT, or withholding tax applies at the partnership level.

- Annual Compliance: Annual reports must be filed with the American Samoa Government's office; failure to file can result in administrative dissolution.

- Treaty Access: American Samoa is a U.S. territory but is not covered by U.S. tax treaties, limiting treaty-based benefits for foreign partners.

- Conversion: A general partnership may convert to an LP or LLP by filing the appropriate formation documents with the registrar, subject to partner consent.

- Restrictions: Foreign nationals may act as partners, though certain regulated industries require additional licensing approval.

Sub-Types

General Partnership (GP)

All partners bear unlimited personal liability for the firm's obligations. No formal registration is required to establish a general partnership in American Samoa, though filing a trade name or operating agreement is advisable.

Limited Partnership (LP)

American Samoa LP formation requirements include filing a certificate of limited partnership with the territorial registrar. Limited partners contribute capital and receive liability protection capped at their investment, while general partners retain full management authority and unlimited liability.

Limited Liability Partnership (LLP)

A limited liability partnership American Samoa structure requires registration with the territorial government and provides each partner with protection against liabilities arising from another partner's negligence or misconduct. It is commonly used by professional service firms.

When to Consider a Partnership

Partnerships suit joint ventures, professional services firms, and investment structures where pass-through taxation is a priority. The flexible internal governance is a clear advantage; however, general partners in a GP or LP remain personally exposed to the entity's debts.

Partnerships are best suited for two or more co-owners seeking pass-through taxation and operational flexibility, particularly in professional services or project-based ventures where formal corporate structure is unnecessary.

Sole Proprietorship

A sole proprietorship American Samoa setup is the simplest form of business registration available in the territory, operating without a separate legal personality — the owner and the business are treated as one and the same under applicable law. Registration requirements are administered through the American Samoa Government's Department of Commerce, which oversees business licensing for locally operating enterprises.

There is no distinct statute exclusively governing sole proprietorships; the structure is recognised under general business licensing and trade regulations applicable to self-employed individuals and sole traders. Because no legal separation exists between the owner and the business, the proprietor bears unlimited personal liability for all debts and obligations incurred.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated sole trader | No separate legal personality from the owner |

| Members | Single proprietor | One individual; no maximum or minimum beyond the single owner requirement |

| Local Presence | Business license required; no registered agent mandate for sole traders | Physical presence in the territory is generally expected for locally operating businesses |

| Capital | USD; no statutory minimum | American Samoa uses the US dollar; capital is at the proprietor's discretion |

| Privacy | Owner name typically appears on public license records | Limited privacy; business and owner identity are effectively the same |

Focus Points

- Taxation: Subject to US federal tax rules applicable to American Samoa residents and self-employed individuals; local gross revenue taxes may apply; no corporate tax layer exists since income passes directly to the proprietor.

- Annual Compliance: Business license renewal through the Department of Commerce is required annually.

- Economic Substance: No formal economic substance obligations apply to this structure.

- Treaty Access: Does not benefit from corporate-level tax treaty protections.

- Conversion: Can be converted to an LLC or corporation by registering a new entity and transferring business assets; no automatic conversion mechanism exists under local law.

Closing

A sole proprietorship suits locally based self-employed individuals and small-scale service providers who operate with low overhead and limited liability exposure. The primary advantage is minimal administrative burden; the key drawback is unlimited personal liability, which leaves the proprietor's personal assets fully exposed to business creditors.

Best suited for individual operators running small, low-risk local businesses who do not require liability protection or plan to seek external investment.

Foreign Business Entities [Branch Office, Foreign Corporation Registration]

Foreign company registration in American Samoa is governed by the American Samoa Code Annotated (ASCA), which requires overseas entities to formally qualify before conducting business within the territory. A branch office or registered foreign corporation does not create a separate legal entity — the parent company remains fully liable for all local operations, obligations, and liabilities incurred in the territory.

Qualification is administered through the American Samoa Government's Office of the Lieutenant Governor, which maintains the business registry. Your home-jurisdiction entity must submit certified copies of its formation documents, a certificate of good standing, and appoint a registered agent with a physical address in the territory.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Extension of foreign parent entity | No separate legal personality created |

| Members / Officers | Directors / Officers of parent company | Local representative or agent typically required |

| Local Presence | Registered agent with local address mandatory | Physical office may be required depending on business activity |

| Capital | No statutory minimum specified | Parent entity's capital structure applies |

| Privacy | Parent company documents become part of public registry filing | Beneficial ownership subject to local disclosure rules |

Focus Points

- Taxation: The branch is taxed on locally sourced income; American Samoa does not impose a separate federal US corporate tax, but local income tax rates apply, and no VAT or GST exists in the territory.

- Annual Compliance: Annual report filings and registered agent maintenance are required to preserve active status.

- Treaty Access: American Samoa is a US territory but is excluded from most US tax treaties, limiting treaty-based withholding relief.

- Restrictions: Certain regulated industries require additional licensing beyond standard foreign qualification.

- Liability: The parent entity bears unlimited liability for all branch obligations — there is no liability shield at the local level.

Sub-Types

Branch Office

A branch office operates as a direct extension of the foreign parent, conducting business under the parent's name and legal identity. This structure suits companies testing market presence before committing to a separately incorporated local entity.

Foreign Corporation Registration

A foreign corporation that wishes to establish a more defined operational presence may register as a qualified foreign corporation, maintaining the parent's legal structure while formally acknowledging the territory's jurisdiction over local activities. This path is typically used by firms with sustained trading or service operations in the territory.

Closing

Expanding business to American Samoa through a foreign entity qualification suits firms seeking operational presence without the administrative overhead of forming a new local company, though the absence of liability separation at the branch level is a significant structural drawback for higher-risk activities.

Foreign entity qualification is most appropriate for established companies with existing operations elsewhere that require a defined, short-to-medium-term presence in the territory.

How to Choose the Right Entity Type in American Samoa

Choosing the right business entity in American Samoa is a structural decision with direct legal, tax, and operational consequences — not merely an administrative formality.

Why Your Entity Choice Matters

The wrong structure can create compliance failures before your business generates a single dollar of revenue. Consider these concrete outcomes:

- Registering as a foreign corporation when you intend to conduct local commerce without completing registration under the American Samoa Code Annotated (A.S.C.A.) Title 30 can result in penalties or forced dissolution.

- Choosing an entity without the capacity to meet local substance requirements, where applicable, triggers reporting failures that may attract regulatory scrutiny from the American Samoa Government.

- Forming a corporation when a simpler structure would suffice locks your business into annual shareholder meeting obligations, board formalities, and statutory reporting costs that do not apply to an LLC or partnership.

- Selecting an entity structure incompatible with your exit strategy — such as one that does not permit redomiciliation or conversion — can make winding down or restructuring significantly more costly.

Key Factors to Consider

- Business Activity: Active trading, passive asset-holding, and regulated sectors each point toward a distinct entity structure under A.S.C.A. Title 30.

- Local vs. Offshore Operations: If your firm will transact with American Samoa residents, it must comply with domestic registration requirements rather than operate as a foreign entity.

- Ownership and Management: Single-owner operations generally suit an LLC or sole proprietorship, while multi-party arrangements with investor obligations push toward a corporation.

- Tax Objectives: American Samoa operates its own tax regime; whether your business qualifies for local incentives or exemptions depends partly on entity type.

- Privacy Requirements: Assess whether public disclosure of directors and shareholders is acceptable or whether nominee arrangements are necessary for your structure.

- Exit Strategy: Confirm whether your chosen entity type permits conversion, redomiciliation, or voluntary dissolution under the applicable provisions of A.S.C.A. Title 30 before formation.

Compliance Services for Companies in American Samoa

Maintain good standing and meet ongoing statutory obligations for your American Samoa entity.

Conclusion

Selecting the right structure is one of the more consequential early decisions in any American Samoa company formation guide. Corporations suit businesses seeking formal capital structures or those with shareholders requiring limited liability protections under local law. The LLC draws the most registrations in the territory, favored for its operational flexibility and pass-through tax treatment. General partnerships carry unlimited personal liability, making them less common outside professional arrangements. Limited partnerships serve capital-passive investors well, while LLPs address licensed professionals specifically. Sole proprietorships remain accessible but offer no liability separation.

Administered through the American Samoa Government's Department of Commerce, the territory's registration framework has remained relatively stable, though gradual alignment with federal compliance expectations continues to shape reporting obligations. Your entity choice will interact directly with that trajectory, particularly as federal oversight of territorial business activity becomes more defined.

How Expanship Can Assist You

Expanship's American Samoa incorporation services cover the full process of forming and maintaining a legal entity in the territory, from selecting the right structure under American Samoa's Revised Code to filing with the Office of the Treasurer, which serves as the registering authority for local businesses. Whether you are forming a domestic corporation, registering an LLC, or qualifying a foreign corporation to operate locally, your business will face specific documentation and compliance obligations that vary by entity type.

Expanship supports you at every stage of that process:

- Document preparation and notarization

- Registered agent and registered office provision in American Samoa

- Filing and liaison with the Office of the Treasurer

- Post-incorporation compliance and annual report management

- Banking introduction assistance

Reach out to Expanship American Samoa to discuss your incorporation requirements.

Frequently Asked Questions (FAQ)

The LLC is the most frequently formed entity in the territory. Its combination of pass-through taxation, limited liability protection, and relatively straightforward maintenance requirements makes it a practical choice for both resident and non-resident operators.

A corporation is subject to entity-level taxation and must observe stricter governance formalities, including a board of directors and annual meetings. An LLC avoids double taxation by passing income directly to members and carries fewer structural requirements under local law.

LLCs generally offer greater privacy than corporations, as member details are not always subject to full public disclosure. Nominee arrangements are available through registered agents operating in the territory.

A sole proprietorship and an LLC can be formed by a single individual. Partnerships, by definition, require at least two partners, so a solo founder cannot establish a general, limited, or limited liability partnership without an additional party.

Corporations and LLCs are accessible to foreign nationals under American Samoa's corporate framework. Foreign operators who do not wish to form a local entity may instead register as a foreign corporation or establish a branch office.

Conversion between entity types is generally permitted under corporate statutes, though the procedural requirements vary depending on the structures involved. An LLC converting to a corporation, for instance, must satisfy filing requirements with the relevant territorial authority.

Corporations and LLCs hold separate legal personality, meaning they can own assets, enter contracts, and incur liabilities in their own name. Sole proprietorships and general partnerships do not offer this separation, leaving owners personally exposed to business obligations.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.