Key Takeaways

- Argentina's corporate legal framework is governed primarily by the General Companies Law (Ley General de Sociedades, Law No. 19,550), which has structured entity formation since 1972.

- The Sociedad por Acciones Simplificada (SAS), introduced in 2017, has become the most registered business structure in Argentina due to its digital formation process through the AFIP and IGJ systems.

- Entity registration in the City of Buenos Aires falls under the jurisdiction of the Inspección General de Justicia (IGJ), with provincial equivalents operating in all other Argentine jurisdictions.

- Partnerships such as the Sociedad Colectiva and Sociedad en Comandita Simple carry unlimited liability for at least some partners, making them uncommon in modern Argentine commercial practice.

Introduction to Entity Types in Argentina

Argentina is a federal republic in South America, bordered by Chile, Bolivia, Paraguay, Brazil, and Uruguay. Selecting among the types of business entities in Argentina requires an understanding of both federal corporate law and the registration process administered at the provincial and national levels. The primary national body governing company formation is the Inspección General de Justicia (IGJ), which oversees entities registered in the City of Buenos Aires; provincial equivalents operate in other jurisdictions.

Argentine corporate law is codified principally in the General Companies Law (Ley General de Sociedades, Law No. 19,550), which has governed legal entity structures since 1972 and been amended several times since. The tax system operates on a residency and source-of-income basis, with corporate income tax applied to domestic and foreign-source earnings for resident entities.

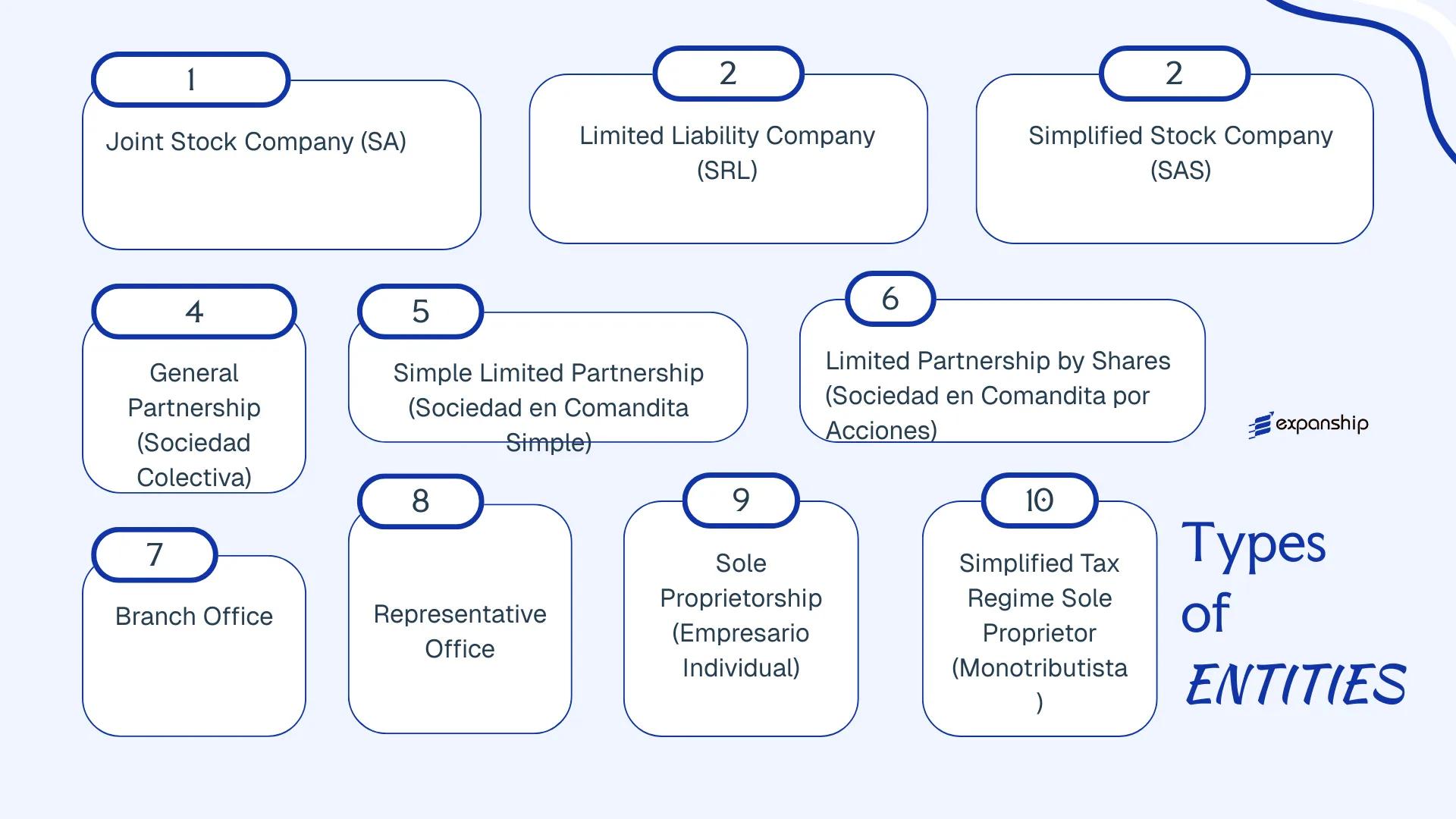

Available Argentine legal entity structures include the Sociedad Anónima (SA), Sociedad de Responsabilidad Limitada (SRL), Sociedad por Acciones Simplificada (SAS), Sociedad Colectiva, Sociedad en Comandita Simple, Sociedad en Comandita por Acciones, Branch Office, Representative Office, and sole proprietorship formats such as the Empresario Individual and Monotributista. Each of these business entity options in Argentina carries distinct formation requirements, liability implications, and administrative obligations, all of which are examined in the sections that follow.

An Overview of Business Structures in Argentina

Argentine company law offers several distinct entity types, each governed primarily by the General Companies Law (Ley General de Sociedades, Law No. 19,550) and supplemented by later legislation such as Law No. 27,349, which introduced the Sociedad por Acciones Simplificada in 2017. Each structure carries different rules on liability, governance, capital requirements, and permitted activities. The sections that follow examine each in detail.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Tax Status | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Sociedad Anónima (SA) | Corporation | Limited to shares | Taxable | Permitted | 2 shareholders | IGJ / Provincial Registry | Law No. 19,550 |

| Sociedad de Responsabilidad Limitada (SRL) | LLC | Limited to quota | Taxable | Permitted | 2 partners | IGJ / Provincial Registry | Law No. 19,550 |

| Sociedad por Acciones Simplificada (SAS) | Simplified corp | Limited to shares | Taxable | Permitted | 1 shareholder | IGJ / Provincial Registry | Law No. 27,349 |

| Sociedad Colectiva | General partnership | Unlimited, joint | Taxable | Permitted | 2 partners | IGJ / Provincial Registry | Law No. 19,550 |

| Sociedad en Comandita Simple | Limited partnership | Mixed liability | Taxable | Permitted | 2 partners | IGJ / Provincial Registry | Law No. 19,550 |

| Sociedad en Comandita por Acciones | Partnership by shares | Mixed liability | Taxable | Permitted | 2 partners | IGJ / Provincial Registry | Law No. 19,550 |

| Branch Office | Foreign branch | Parent liable | Taxable | Permitted | 1 foreign entity | IGJ / Provincial Registry | Law No. 19,550, Art. 118 |

| Representative Office | Non-trading presence | Parent liable | Limited scope | Not permitted | 1 foreign entity | IGJ / Provincial Registry | Law No. 19,550, Art. 118 |

| Empresario Individual | Sole proprietorship | Unlimited | Taxable | Permitted | 1 individual | AFIP / Provincial registry | Civil and Commercial Code |

| Monotributista | Simplified tax regime | Unlimited | Flat monthly tax | Permitted | 1 individual | AFIP | Law No. 24,977 |

Each of these structures is examined in full in the sections below.

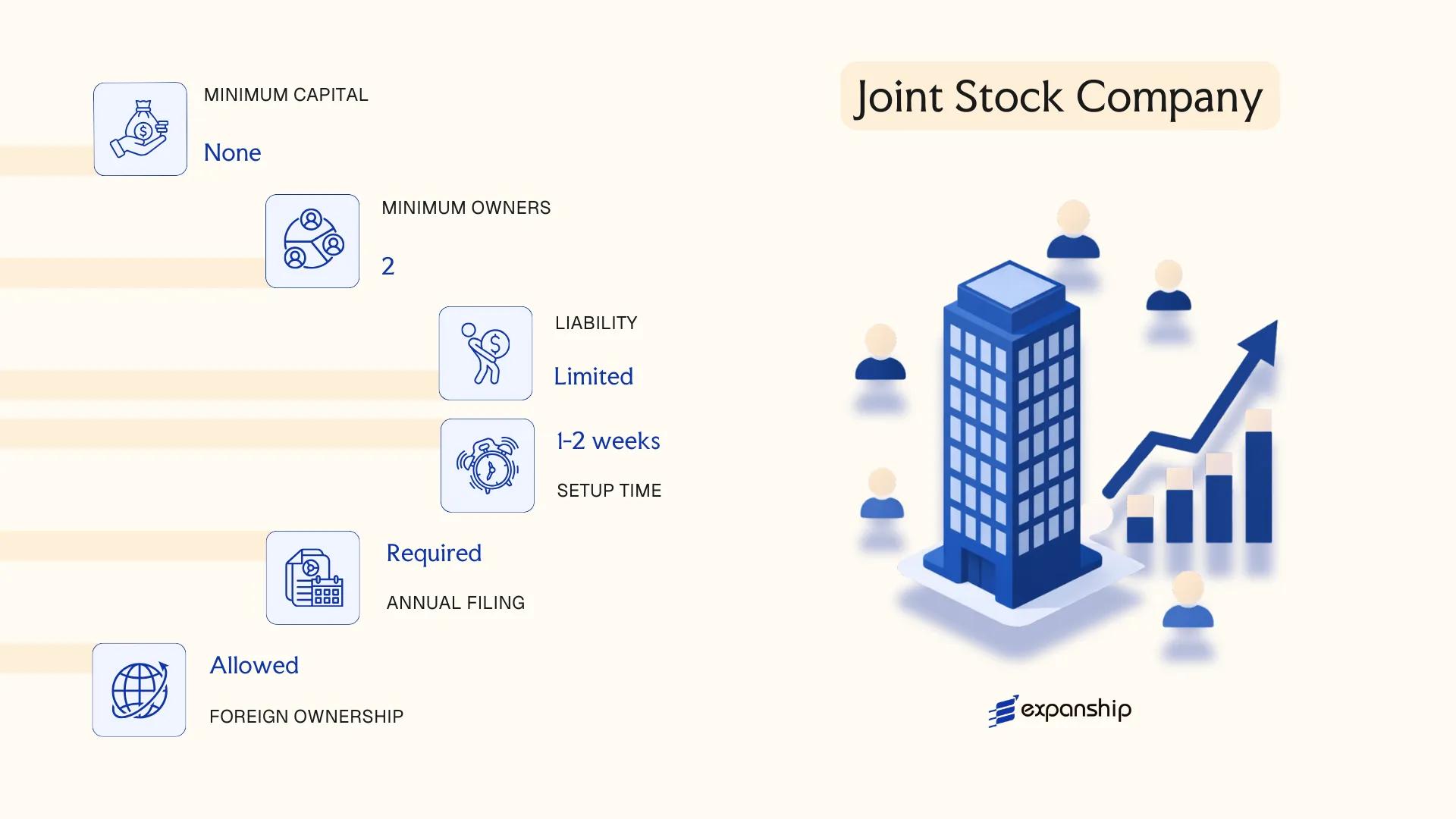

Sociedad Anónima (SA) — Joint Stock Company

Governed by the General Companies Law (Ley General de Sociedades, Law No. 19,550), the Sociedad Anónima Argentina formation process establishes an entity with full separate legal personality, meaning the company holds rights and obligations independently of its shareholders. Liability is capped at each shareholder's subscribed capital contribution.

Capital is divided into shares, which can be transferred without amending the corporate bylaws — a structural feature that makes this form common among larger businesses and those anticipating future investment rounds.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedad Anónima (SA) | Regulated under Law No. 19,550 |

| Members | Shareholders: minimum 2, no maximum | Shareholders may be individuals or legal entities, domestic or foreign |

| Governance | Board of Directors (at least 1 director); Statutory Auditor (Síndico) required when certain thresholds are met | A Supervisory Committee (Consejo de Vigilancia) is optional |

| Local Presence | Registered legal address in Argentina required | Must be maintained at all times |

| Capital | Minimum ARS 100,000 (subject to periodic adjustment by the IGJ); denominated in Argentine pesos | 25% must be paid in at incorporation; remainder within 2 years |

| Privacy | Shareholder names appear in public registry filings | Beneficial ownership disclosure requirements apply |

Focus Points

- Taxation: Subject to corporate income tax at 35% on net taxable income; VAT at 21% (standard rate); withholding taxes apply to dividends, interest, and royalties paid abroad; no federal stamp duty, though provincial stamp taxes may apply — see AFIP for current rates.

- Annual Compliance: Annual financial statements must be filed with the Inspección General de Justicia (IGJ) in Buenos Aires, or the equivalent provincial registry elsewhere; shareholders' meeting required annually.

- Economic Substance: No specific economic substance regime, but the IGJ scrutinises shell-like structures; directors must be locally reachable.

- Treaty Access: Argentina maintains a limited network of double taxation treaties; SA entities are generally eligible for treaty benefits where applicable.

- Conversion: An SA may be converted into another company type (including SRL or SAS) through a formal restructuring process under Law No. 19,550, requiring shareholder approval and registry re-registration.

Sub-Types

SA Cerrada (Closely Held SA)

A closely held SA does not make public offerings of its shares and operates under somewhat simplified governance requirements. It is the standard formation used by private businesses and family-owned enterprises.

SA Abierta (Publicly Traded SA)

This variant is authorised to offer shares to the public and falls under the additional supervision of the Comisión Nacional de Valores (CNV), Argentina's securities regulator. It carries stricter disclosure, audit, and governance obligations than its closely held counterpart.

When to Use an SA

The SA suits holding structures, medium-to-large trading operations, and businesses expecting external investment or eventual public listing. Share transferability without bylaw amendments is a practical advantage for equity transactions. The main limitation is administrative burden: mandatory annual audits, IGJ filings, and the Síndico requirement add recurring compliance costs that smaller operations may find disproportionate.

The SA is most appropriate for businesses with multiple investors, foreign parent companies establishing an Argentine subsidiary, or any operation where share transferability and institutional credibility are priorities.

Company Incorporation in Argentina

Incorporate a Sociedad Anónima or other Argentine entity with end-to-end support from registry filing to post-incorporation compliance.

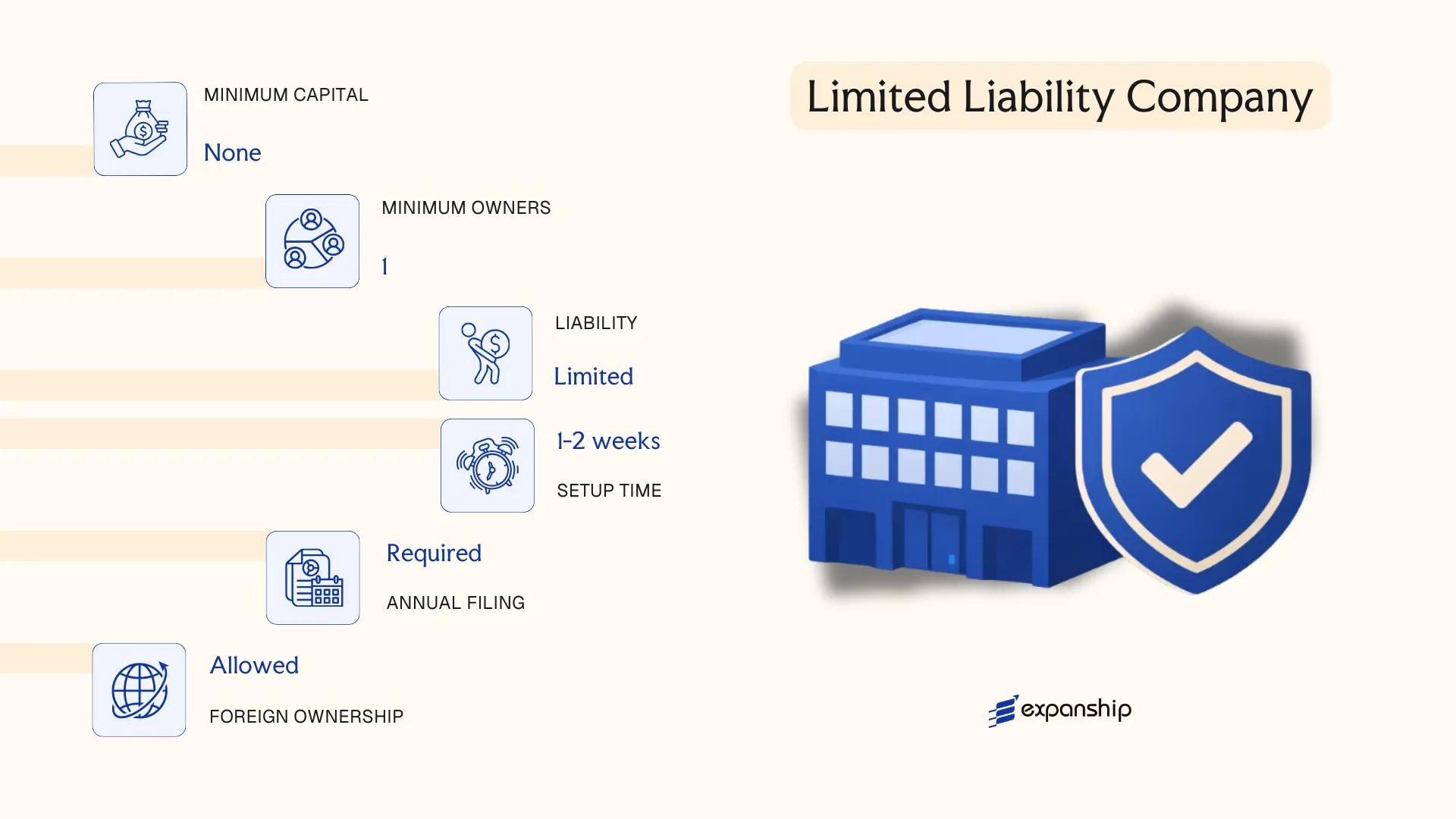

Sociedad de Responsabilidad Limitada (SRL) — Limited Liability Company

Governed by the General Companies Law (Ley General de Sociedades, Law 19,550), the Sociedad de Responsabilidad Limitada Argentina is a hybrid structure that blends the liability protection of a corporation with the operational flexibility typical of a partnership. The entity holds separate legal personality from its members, meaning the business can own assets, enter contracts, and incur obligations in its own name.

Membership interests are represented by quotas (cuotas) rather than shares, and liability is capped at each member's subscribed capital contribution. This structure suits closely held businesses where ownership transfer is intended to remain restricted.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedad de Responsabilidad Limitada (SRL) | Quota-based; not share-based |

| Members | 2–50 cuotistas (quota holders) | No single-member SRL permitted; capped at 50 |

| Management | One or more gerentes (managers) | Can be members or third parties; appointed in the bylaws |

| Registered Office | Local registered address required | Must be maintained with the IGJ (Buenos Aires) or relevant provincial registry |

| Capital | No statutory minimum; denominated in Argentine pesos | Quotas must be fully subscribed at formation; 25% paid-in at incorporation, remainder within 2 years |

| Privacy | Quota holders listed in public registry | Ownership information is publicly accessible |

Focus Points

- Taxation: Subject to corporate income tax at 35% on net taxable income; VAT applies at 21% on taxable supplies; dividend distributions to non-residents attract a 7% withholding tax (rising to 13% under certain conditions); no separate stamp duty at federal level, though provincial stamp taxes may apply on contracts.

- Annual Compliance: Financial statements must be filed annually with the Inspección General de Justicia (IGJ) or the relevant provincial registry; a statutory audit is not mandatory for SRLs below certain capital thresholds.

- Quota Transfer Restrictions: Quota transfers require consent procedures outlined in the bylaws and are subject to right-of-first-refusal provisions among existing members, making the SRL unsuitable for businesses anticipating frequent ownership changes.

- Treaty Access: As a tax-resident Argentine entity, the SRL can access Argentina's network of double taxation treaties, subject to applicable anti-abuse provisions.

- Conversion: An SRL may be converted into an SA or SAS through a formal restructuring process under Law 19,550, requiring member approval and re-registration.

Closing

The SRL is commonly used for small-to-medium trading operations, family-held businesses, and professional services firms where a tight membership structure is preferred. The quota-based ownership model provides effective transfer control, though the 50-member cap limits its suitability as the business scales or requires broader investor participation.

The SRL is most appropriate for closely held SMEs and family businesses seeking limited liability without the administrative overhead associated with a full SA structure.

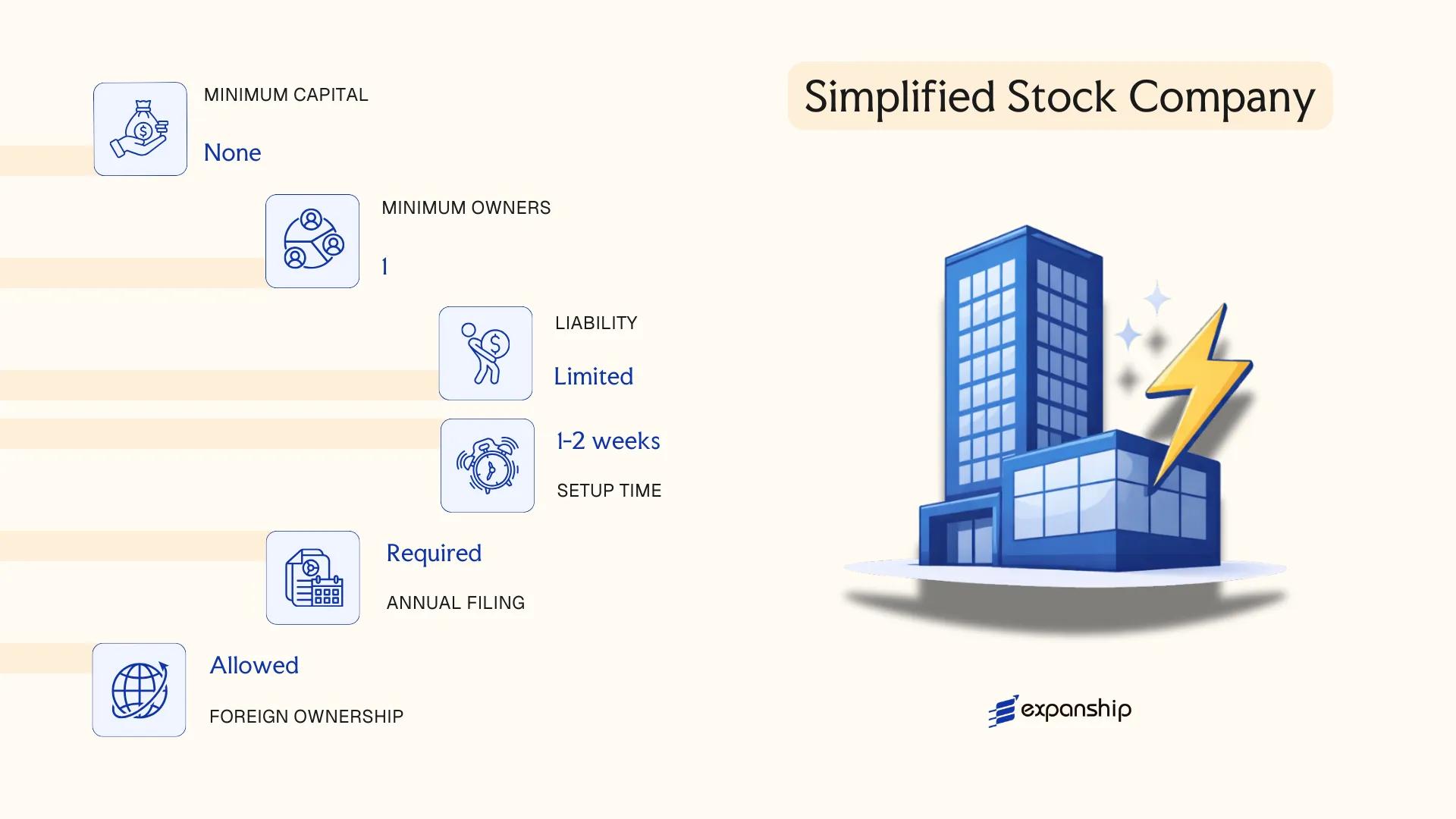

Sociedad por Acciones Simplificada (SAS) — Simplified Stock Company

Introduced under Law 27,349 of 2017, the Sociedad por Acciones Simplificada Argentina represents a significant departure from traditional incorporation frameworks. It carries separate legal personality and grants shareholders limited liability, while its hybrid structure borrows elements from both share-based companies and simplified foreign equivalents.

Registration occurs entirely online through the Argentine business registry system, making Argentina SAS online registration considerably faster than conventional routes. Incorporation can be completed within 24 hours in many jurisdictions, though timelines vary by province.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Share-based company with simplified governance | Governed by Law 27,349 |

| Members | Shareholders; minimum 1, maximum no statutory cap | Cannot be used by entities listed under public offering regimes |

| Directors | Minimum 1 director; no nationality or residency requirement | Director can be a shareholder |

| Local Presence | Registered address in Argentina required | No mandatory resident director, but a local fiscal address is needed |

| Capital | Minimum capital equivalent to 2x the minimum wage at time of incorporation; denominated in Argentine pesos | No paid-up requirement at formation beyond statutory minimum |

| Privacy | Shareholder and director information filed with registry; not publicly searchable in all provinces | Beneficial ownership disclosure required under anti-money-laundering regulations |

Focus Points

- Taxation: Subject to corporate income tax at the standard rate (currently 35%), VAT at 21%, and withholding taxes on dividends paid to non-residents; no special tax concessions apply by virtue of the SAS structure alone.

- Annual Compliance: Annual financial statements must be filed; auditor requirements depend on company size and capital thresholds set by the relevant provincial registry.

- Restrictions: Cannot be incorporated by another SAS or by entities subject to public capital markets regulation; intended for small to mid-sized private ventures.

- Conversion: May be converted into an SA or SRL through a formal restructuring process without dissolution, subject to registry approval.

- Treaty Access: As a domestic Argentine entity, the SAS qualifies for Argentina's double tax treaty network, subject to standard beneficial ownership and anti-abuse provisions.

Closing

The SAS suits early-stage ventures, technology businesses, and foreign investors seeking a low-friction entry point into the Argentine market for trading or service operations. Its primary advantage is speed of formation; its key limitation is the restriction on public capital raising, which prevents access to equity markets.

The SAS is most appropriate for small to mid-sized privately held businesses and foreign entrepreneurs seeking a fast, cost-effective Argentine corporate vehicle without complex governance requirements.

Partnerships in Argentina [Sociedad Colectiva, Sociedad en Comandita Simple, Sociedad en Comandita por Acciones]

Partnership structures in Argentina occupy a distinct space under the Ley General de Sociedades No. 19,550 (General Companies Law), which governs all commercial entities. Unlike capital-based structures, partnerships can expose partners to personal liability, and the degree of that exposure varies by structure. All three forms discussed here carry separate legal personality under Argentine law, meaning the entity can contract, hold assets, and incur obligations in its own name.

Registration of any Argentine partnership requires filing with the Inspección General de Justicia (IGJ) in the City of Buenos Aires, or with the equivalent provincial registry elsewhere in the country.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedad Colectiva (SC), Sociedad en Comandita Simple (SCS), Sociedad en Comandita por Acciones (SCA) | Three distinct structures under LGS 19,550 |

| Partners | Socios (SC/SCS); Socios Comanditados and Socios Comanditarios (SCS/SCA) | SC: minimum 2 partners, no maximum; SCS: at least 1 managing partner + 1 limited partner; SCA: at least 1 general partner + shareholders |

| Liability | SC: unlimited for all partners; SCS: unlimited for comanditados, limited for comanditarios; SCA: same split as SCS | Unlimited liability attaches jointly and severally to managing partners |

| Capital | No statutory minimum for SC or SCS; SCA must issue shares for comanditario contributions | Contributions can be in cash or in kind; SCA shares are freely transferable |

| Local Presence | Registered address required in the province of incorporation; a legal representative domiciled in Argentina is mandatory | IGJ requires a domicilio legal for service of process |

| Privacy | Partner names appear in the public commercial registry | No confidentiality mechanism available for any partnership form |

Focus Points

- Taxation: All three structures are subject to corporate income tax at the standard rate (currently 35%), VAT at 21%, and applicable withholding taxes on profit distributions to foreign partners; stamp duty applies at the provincial level on the constitutive deed.

- Annual Compliance: Annual financial statements must be filed with the IGJ; SC and SCS face lighter disclosure requirements than SCA, which is subject to rules closer to those of public companies.

- Economic Substance: No dedicated substance regime applies specifically to partnerships, but managing partners must be domiciled in Argentina for the entity to operate validly.

- Conversion: LGS 19,550 permits transformation of any of these structures into another company type without dissolution, provided partners comply with prescribed formalities.

- Restrictions: Foreign nationals may be partners, but at least one locally domiciled representative must be designated for legal and regulatory correspondence.

Sub-Types

Sociedad Colectiva (SC)

All partners bear unlimited, joint, and several liability for the firm's obligations. This structure is used almost exclusively by small professional or family-run businesses where partners have full mutual trust and no separation of liability is sought.

Sociedad en Comandita Simple (SCS)

The Argentina Sociedad en Comandita splits membership into two classes: comanditados, who manage the business and carry unlimited liability, and comanditarios, whose liability is capped at their capital contribution. Comanditarios may not participate in management without forfeiting their limited liability protection.

Sociedad en Comandita por Acciones (SCA)

Structurally similar to the SCS but the comanditario interest is divided into shares, allowing capital to be raised from a broader group. The SCA is subject to more stringent IGJ oversight and accounting obligations than the simpler partnership forms.

Partnerships under LGS 19,550 are most commonly used for family businesses, professional firms, or situations where a small group of known counterparties wishes to operate with a defined liability split without the formality of a joint-stock structure. The SCS and SCA offer useful flexibility in separating active management from passive investment, though unlimited liability for managing partners remains a material constraint on wider adoption.

These structures suit closely held family enterprises or professional partnerships where all active participants are Argentine residents willing to accept personal liability exposure.

Foreign Business Structures in Argentina [Branch Office, Representative Office]

Establishing a foreign company branch office Argentina requires registration under the General Companies Law (Ley General de Sociedades, Law No. 19,550). Under this framework, a branch (Sucursal) is not a separate legal entity — it remains an extension of the parent company, which retains full liability for its Argentine operations. A representative office, while also registered under the same law, operates under more restricted commercial parameters.

Both structures must register with the Inspección General de Justicia (IGJ) in Buenos Aires, or the relevant provincial registry elsewhere. Registration involves submitting authenticated copies of the parent company's constitutive documents, proof of legal existence in the home jurisdiction, and appointing a local legal representative.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Personality | None — extension of parent | None — extension of parent |

| Commercial Activity | Permitted | Not permitted; promotional only |

| Liability | Parent bears full liability | Parent bears full liability |

| Local Representative | Mandatory (resident individual) | Mandatory (resident individual) |

| Registered Address | Required in Argentina | Required in Argentina |

| Capital Assignment | Parent must assign capital; no statutory minimum | No capital assignment required |

Focus Points

- Taxation: Branch profits are subject to corporate income tax at 35%; VAT applies to taxable supplies; a remittance tax of 35% applies to profits transferred to the parent, though tax treaties may reduce this rate.

- Compliance: Annual financial statements must be filed with the IGJ; the branch must maintain local accounting records in Spanish.

- Treaty Access: Access to Argentina's double tax treaties depends on the parent company's residency; the branch itself holds no independent treaty status.

- Restrictions: A representative office cannot invoice clients, sign commercial contracts, or generate local revenue — any activity beyond promotion may trigger reclassification by the IGJ.

- Conversion: Converting a branch to a locally incorporated entity (such as an SA or SRL) requires a separate incorporation process; there is no automatic conversion mechanism under Law No. 19,550.

Sub-Types

Sucursal (Branch Office)

A Sucursal conducts active commercial or industrial operations in Argentina on behalf of the foreign parent. It can enter contracts, employ staff, and generate local revenue, but the parent remains directly liable for all obligations incurred.

Oficina de Representación (Representative Office)

This structure is limited to liaison, promotional, and market research activities. It cannot sign contracts that generate revenue, making it suitable only for foreign firms testing the market or coordinating with local partners before committing to full incorporation.

A branch is commonly used by foreign firms that need operational presence without establishing a separate local entity, though the parent's unlimited liability exposure is a material drawback for higher-risk activities. A representative office suits preliminary market entry but cannot sustain commercial operations.

A branch office is most appropriate for established foreign companies seeking direct operational control in Argentina; a representative office suits firms in an early-stage market assessment phase only.

Sole Proprietorship in Argentina [Empresario Individual, Monotributista]

Argentina's sole proprietorship structures operate outside the corporate framework established by the General Companies Law (Ley General de Sociedades, Law No. 19,550). Neither the Empresario Individual nor the Monotributista classification carries separate legal personality — the individual and the business remain a single legal subject, meaning personal assets are exposed to business liabilities without limitation.

Registration takes place through the Administración Federal de Ingresos Públicos (AFIP) for tax purposes, and through provincial commerce registries where applicable. The Monotributista regime, a simplified tax and social security system for self-employed individuals and small businesses, is the most commonly used sole proprietorship structure for Argentina self-employed business registration.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated sole proprietorship | No separate legal personality; owner bears unlimited personal liability |

| Owner Title | Proprietor / Autonomous Worker (Trabajador Autónomo) | Empresario Individual for general self-employed; Monotributista for simplified regime |

| Members | Single individual only | No partners or co-owners permitted under this structure |

| Local Presence | AFIP registration; provincial registry where required | Physical address in Argentina required for registration |

| Capital | No minimum capital requirement | No formal share capital; owner contributes operating funds directly |

| Revenue Cap (Monotributista) | Set by AFIP; adjusted periodically by resolution | Exceeding the cap triggers mandatory migration to the general tax regime |

Focus Points

- Taxation: Monotributistas pay a single fixed monthly contribution covering income tax, VAT, and social security; Autónomos under the general regime are subject to progressive income tax rates, VAT at 21%, and separate social security contributions.

- Annual Compliance: Monthly fixed payments to AFIP; annual income category recategorisation based on gross revenue and other activity indicators.

- Restrictions: Cannot employ more than a limited number of staff under the Monotributista regime; revenue thresholds and activity categories are strictly regulated by AFIP resolutions.

- Conversion: Upgrading to a corporate structure such as an SAS or SRL requires a separate incorporation process; assets and liabilities must be formally transferred.

Sub-Types

Monotributista

Designed for individuals whose annual gross income falls below AFIP-defined thresholds, this regime consolidates tax and social security obligations into a single monthly fixed payment. It is commonly used by freelancers, consultants, and small traders operating independently.

Autónomo (General Regime)

Self-employed individuals who exceed Monotributista thresholds, or who opt out voluntarily, register under the Autónomo category within the general AFIP tax regime. Obligations include progressive income tax, 21% VAT filings, and separate social security contributions calculated on a presumed income scale.

Closing

Sole proprietorships suit individual service providers, freelancers, and micro-businesses operating at low revenue volumes where administrative simplicity outweighs the need for liability protection. The primary limitation is unlimited personal liability, which leaves the owner's personal assets fully exposed to business obligations.

Best suited for individual professionals or micro-entrepreneurs with modest annual turnover who prioritise low administrative overhead over liability protection.

How to Choose the Right Entity Type in Argentina

Choosing the right company structure in Argentina determines your tax exposure, liability profile, and operational capacity before you ever conduct a transaction.

Why Your Entity Choice Matters

The structure you register has binding legal consequences that are difficult and costly to unwind.

- Registering a foreign branch under Article 118 of the General Companies Law (Ley General de Sociedades No. 19,550) when your activity qualifies as habitual local trade without proper registration can expose the parent entity to penalties and operational restrictions imposed by the Inspección General de Justicia (IGJ).

- Selecting an SA when a SAS would suffice for a single-person consultancy adds mandatory statutory audit requirements and higher annual compliance costs that are structurally unnecessary for low-complexity operations.

- Forming an SRL when your investors require freely transferable equity creates friction at every ownership transfer, since quota assignments require notarial deed and registration with the IGJ.

Key Factors to Consider

- Business Activity: Active trading, regulated sectors such as financial services, and passive asset-holding each correspond to different structural requirements under Ley 19,550.

- Ownership Structure: Single-owner operations may qualify for a SAS, while multi-party ventures requiring board governance point toward an SA.

- Tax Objectives: Your eligibility for Argentina's monotributo regime or the general income tax system depends on your chosen entity form and projected revenue.

- Substance Capacity: If you cannot maintain a local director or registered office in practice, certain structures will face compliance failures with the IGJ.

- Exit Strategy: Not all entity types permit redomiciliation or conversion without dissolution, which affects long-term planning for foreign investors.

Corporate Compliance Services in Argentina

Ongoing compliance support for Argentine companies, including IGJ filings, annual reporting, and statutory obligations.

Conclusion

Argentina's legal framework gives founders several distinct paths to incorporation, each governed by the General Companies Law (Ley General de Sociedades No. 19,550). Setting up a company in Argentina requires matching your structure to your operational goals. The SA suits larger enterprises requiring transferable share capital; the SRL works for closely held businesses with a defined partner group; the SAS, introduced in 2017, serves startups and small firms needing faster digital registration. Partnerships carry unlimited liability and remain uncommon in commercial practice. Branch offices and representative offices serve foreign entities with specific operational or liaison mandates.

The SAS has become the most registered structure in recent years, largely due to its simplified online formation process through the AFIP and IGJ systems.

Regulatory modernization is ongoing, with continued digitization of corporate filings pointing toward a more accessible registration environment for foreign investors. Expanship's team works directly within these frameworks to support your setup from entity selection through registration completion.

How Expanship Can Assist You

Expanship's Argentina company incorporation services cover the full scope of what this blog has addressed — from registering an SA or SRL with the Inspección General de Justicia (IGJ) to forming an SAS through the simplified digital registry. Your specific structure, ownership profile, and operational goals shape every step of that process, and our team works with each client accordingly.

From initial document preparation to post-incorporation obligations, Expanship handles the details so your business is properly established from day one:

- Document preparation, apostille, and legalization

- Registered agent and local registered address provision

- Filing with the IGJ or provincial public registries

- Post-incorporation compliance management, including annual filings

- Banking introduction assistance for corporate account setup

Ready to move forward? Reach out to Expanship Argentina to discuss your setup.

Frequently Asked Questions (FAQ)

The Sociedad de Responsabilidad Limitada (SRL) is the most frequently registered structure, particularly among small and medium-sized enterprises. Its simplified governance requirements and capped member liability make it practical for locally operating businesses with a limited number of partners.

A Branch Office is not a separate legal entity — it remains an extension of its foreign parent and carries the parent's full liability exposure. An SRL, by contrast, is incorporated under Argentine law as a distinct legal person, giving it independent contractual capacity and limiting member liability to their contributed capital. From a tax standpoint, both are subject to Argentine corporate income tax on locally sourced income, but the Branch triggers additional scrutiny under transfer pricing rules when transacting with its parent.

The Sociedad Anónima (SA) offers the highest degree of structural privacy among Argentine entity types. Bearer shares were eliminated under Argentine law, but nominee shareholders are legally permissible, and beneficial ownership disclosure requirements apply primarily through the Unidad de Información Financiera (UIF) rather than through public registries.

No. The Sociedad por Acciones Simplificada (SAS) is the only structure formally designed for single-person incorporation under Law 27,349. An SRL requires a minimum of two and a maximum of fifty quota-holders, while an SA requires at least two shareholders under the General Companies Law (Law 19,550).

Foreigners may incorporate an SRL, SA, or SAS without residency requirements, provided they comply with registration formalities before the Inspección General de Justicia (IGJ) in Buenos Aires or the equivalent provincial registry. A Branch Office requires the foreign parent to register locally and appoint a legal representative domiciled in Argentina. The SAS has become a preferred entry point for non-resident founders due to its digital registration process.

Argentine law permits the transformation of one company type into another without dissolution, as regulated under Section 74 of Law 19,550. An SRL can be converted into an SA, and an SA into an SRL, subject to creditor notification procedures and re-registration with the relevant commercial registry.

The Monotributista regime imposes the lightest administrative burden, requiring only a single unified tax filing that replaces VAT and income tax obligations below a set revenue ceiling. For formally incorporated entities, the SAS has the lightest annual compliance footprint among registered company types, with fewer mandatory assembly and audit requirements than the SA.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.