Key Takeaways

- The Sociedade por Quotas is the most commonly registered entity in Angola, favored by small to mid-sized businesses for its relatively straightforward governance requirements under Lei das Sociedades Comerciais (Law No. 1/04).

- Angola operates a territorial tax system, meaning income sourced outside the country is generally not subject to domestic corporate tax.

- Company registration and commercial registry maintenance in Angola are administered through the Guichet Único do Empreendedor e da Empresa (GUE), which functions as the country's single-window incorporation body.

- Branch and representative offices allow foreign firms to operate in Angola without establishing a separate legal entity, making them suited for market-testing or contract fulfillment purposes.

Introduction to Entity Types in Angola

Angola is a sovereign nation located on the west coast of sub-Saharan Africa, bordered by the Democratic Republic of Congo to the north, Zambia to the east, and Namibia to the south. Company registration and ongoing compliance fall under the authority of the Guichet Único do Empreendedor e da Empresa (GUE), the single-window body that processes business incorporations and maintains the commercial registry. The country operates a territorial tax system, meaning income sourced outside Angola is generally not subject to domestic corporate tax.

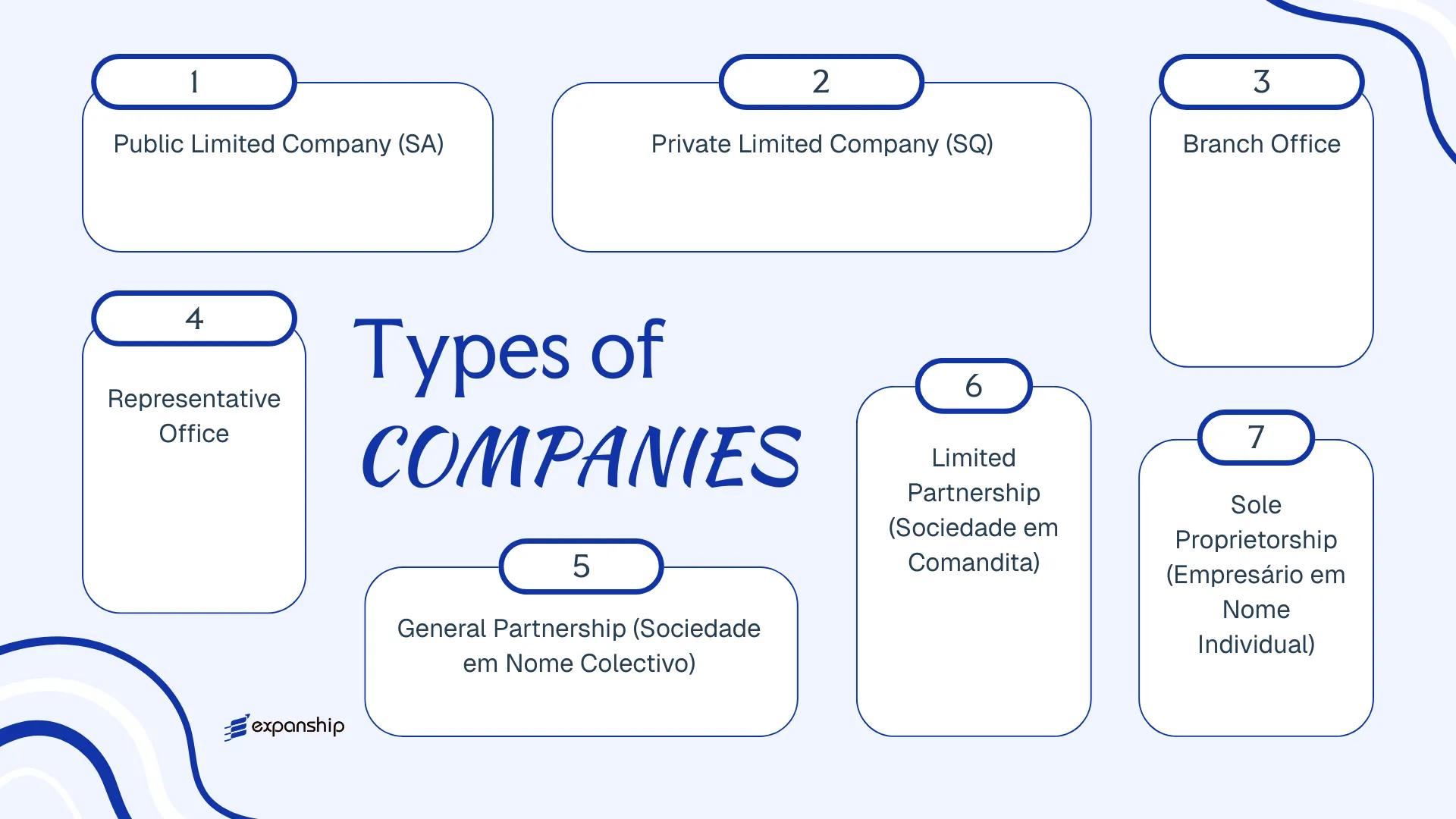

Several types of business entities in Angola are available to both local and foreign investors. These include the Sociedade Anónima, Sociedade por Quotas, Sociedade em Nome Colectivo, Sociedade em Comandita, Empresário em Nome Individual, branch offices, and representative offices. Each structure carries distinct liability, capital, and governance requirements under the Lei das Sociedades Comerciais (Law No. 1/04).

This article examines each of these Angola company types in detail — covering their legal requirements, ownership rules, and practical considerations for foreign businesses.

An Overview of Business Structures in Angola

Angola's company law framework recognises several distinct entity types, each governed primarily by the Lei das Sociedades Comerciais (Law No. 1/04 of 13 February 2004). This legislation establishes the legal foundations for how commercial entities are formed, capitalised, and operated within the country. Each structure carries different implications for liability, ownership, and operational scope.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Tax Status | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Sociedade Anónima (SA) | Public Limited Company | Limited to share capital | Taxable | Permitted | 1 shareholder | BODIVA / Commercial Registry | Law No. 1/04 |

| Sociedade por Quotas (SQ) | Private Limited Company | Limited to quota value | Taxable | Permitted | 1 member | Commercial Registry | Law No. 1/04 |

| Branch Office | Foreign branch | Parent bears liability | Taxable | Permitted | N/A | Commercial Registry | Law No. 1/04 |

| Representative Office | Liaison entity | Parent bears liability | Generally exempt | Not permitted | N/A | Commercial Registry | Law No. 1/04 |

| Sociedade em Nome Colectivo | General Partnership | Unlimited, joint | Taxable | Permitted | 2 partners | Commercial Registry | Law No. 1/04 |

| Sociedade em Comandita | Limited Partnership | Mixed liability | Taxable | Permitted | 2 partners | Commercial Registry | Law No. 1/04 |

| Empresário em Nome Individual | Sole Proprietorship | Unlimited, personal | Taxable | Permitted | 1 individual | Commercial Registry | Law No. 1/04 |

Each of these structures is examined in full in the sections below.

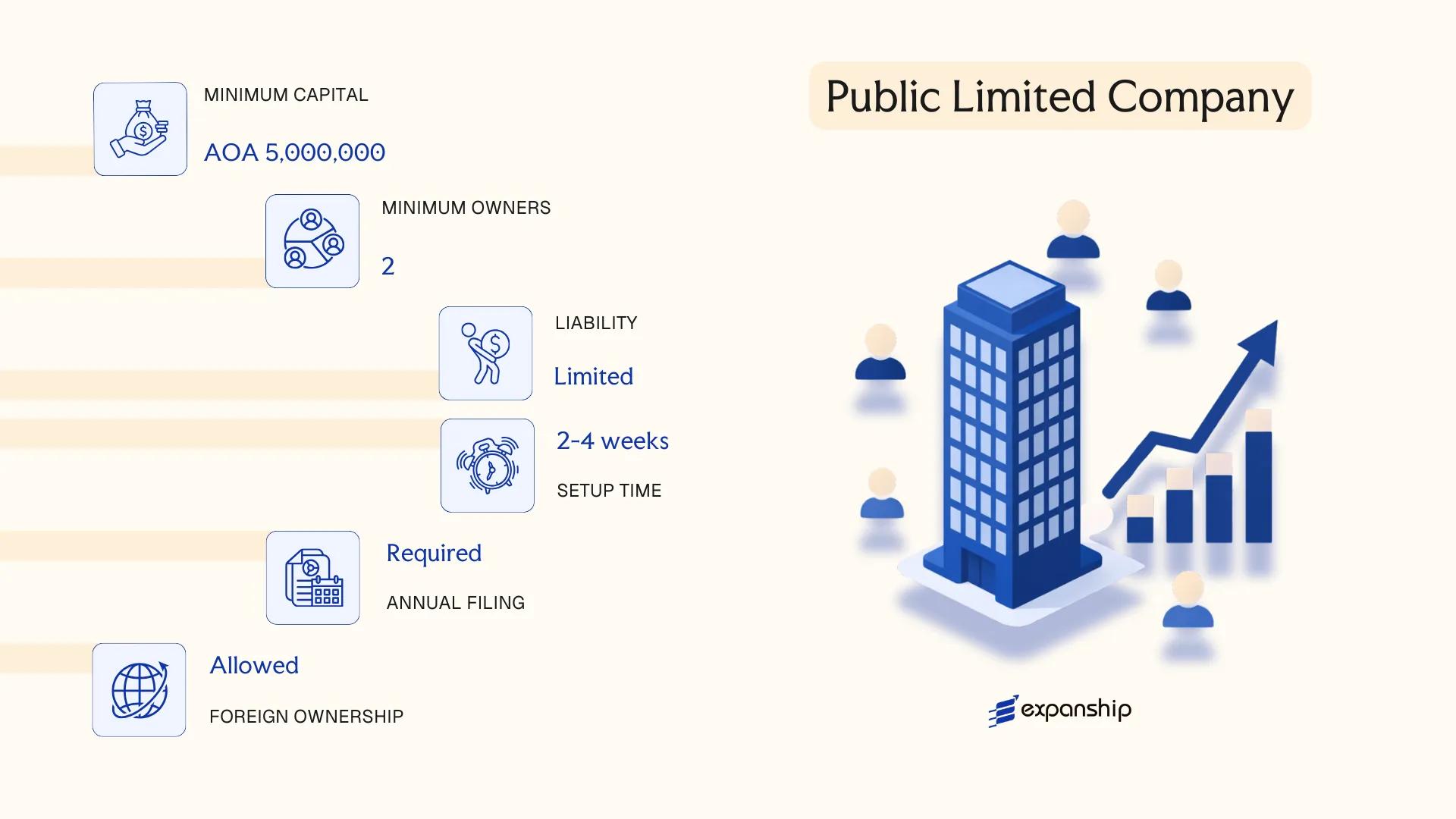

Sociedade Anónima (SA) — Public Limited Company

The Sociedade Anónima Angola structure is governed by the Lei das Sociedades Comerciais (Law No. 1/04 of 13 February 2004), which establishes its legal framework alongside subsequent amendments. The SA carries separate legal personality, meaning the company exists independently of its shareholders, whose liability is confined to their subscribed capital contributions.

Structurally, the SA functions as a joint stock company where capital is divided into shares that can, in principle, be transferred freely. This makes it the preferred structure for larger enterprises, foreign investors seeking scalability, and businesses that may eventually seek public financing.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedade Anónima (SA) | Joint stock company; shares represent ownership units |

| Members | Shareholders (Accionistas); minimum 3 | No statutory maximum; can include legal entities |

| Governance | Board of Directors (Conselho de Administração) + Fiscal Board (Conselho Fiscal) | Both bodies are mandatory for standard SAs |

| Local Presence | Registered office in Angola required | A physical registered address must be maintained |

| Share Capital | Minimum AOA 1,000,000 | Must be fully subscribed at incorporation; at least 30% paid up |

| Privacy | Shareholder register maintained; not fully public | Annual accounts filed with Conservatória do Registo Comercial |

Focus Points

- Taxation: Corporate income tax (IRC) applies at 25%, with VAT at 14%; dividends paid to non-residents are subject to withholding tax, and capital gains are generally taxed as ordinary income.

- Annual Compliance: Audited financial statements are required for SAs; accounts must be filed with the commercial registry and the Agência Geral do Comércio.

- Economic Substance: No formal substance regime equivalent to offshore jurisdictions exists, but genuine operational presence is expected to satisfy tax residency requirements.

- Treaty Access: Angola maintains a limited network of double taxation agreements; treaty benefits should be verified on a case-by-case basis.

- Conversion: An SA may be converted to a Sociedade por Quotas and vice versa, subject to shareholder approval and re-registration procedures.

Closing

The SA is suited to large-scale trading operations, holding structures with multiple investors, and businesses anticipating external financing or eventual public listing. Its principal advantage is unrestricted share transferability; the main drawback is the mandatory dual-governance structure, which increases administrative overhead and ongoing compliance costs.

Best suited for large enterprises, joint ventures with multiple shareholders, or foreign investors requiring a scalable corporate structure with freely transferable equity.

Company Incorporation in Angola

Incorporate an SA or other business entity in Angola with end-to-end support from registration through compliance.

Sociedade por Quotas (SQ) — Private Limited Company

The Sociedade por Quotas Angola SQ is governed by the Angolan Companies Act (Lei das Sociedades Comerciais, Law No. 1/04), which establishes it as a distinct legal entity separate from its members. Liability is capped at each member's subscribed quota, meaning personal assets are not exposed to business obligations.

Structurally, the SQ occupies a middle ground between a partnership and a fully public structure. This makes it a practical choice for closely held operations where ownership control and transferability need to remain within a defined group.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private limited company (quotas-based) | Quotas are not freely transferable without member consent |

| Members | Minimum 2, maximum not statutorily capped | Members hold quotas, not shares; referred to as "quotistas" |

| Management | One or more managers (gerentes) | Need not be members; board structure is optional |

| Local Presence | Registered office required in Angola | No statutory requirement for a resident company secretary |

| Capital | AOA minimum; no universally fixed statutory floor under general practice | Quota values must be defined in the articles of association |

| Privacy | Member details filed with the Conservatória do Registo Comercial | Public register; beneficial ownership disclosures apply |

Focus Points

- Taxation: Subject to Industrial Tax (Imposto Industrial) at 25% on net profits; VAT applies at 14%; withholding taxes apply to dividends, royalties, and services paid to non-residents at varying rates.

- Annual Compliance: Financial statements must be filed annually; auditing is mandatory once the entity exceeds statutory size thresholds.

- Economic Substance: No formal substance regime equivalent to offshore jurisdictions, but genuine local operational presence is expected for resident tax status.

- Quota Transfer Restrictions: Transfers to third parties outside the membership require prior consent from other quotistas under the articles or applicable law.

- Treaty Access: Angola has a limited double tax treaty network; access depends on the resident status of the entity and counterparty jurisdiction.

Closing

The SQ suits trading operations, joint ventures, and local subsidiary structures where ownership flexibility is secondary to liability protection. Its main advantage is the straightforward governance model relative to an SA; the principal limitation is that quota transfers are restricted, which can complicate exits or investor entry.

Best suited for foreign investors establishing a locally operating subsidiary or joint venture with Angolan partners who require defined ownership boundaries.

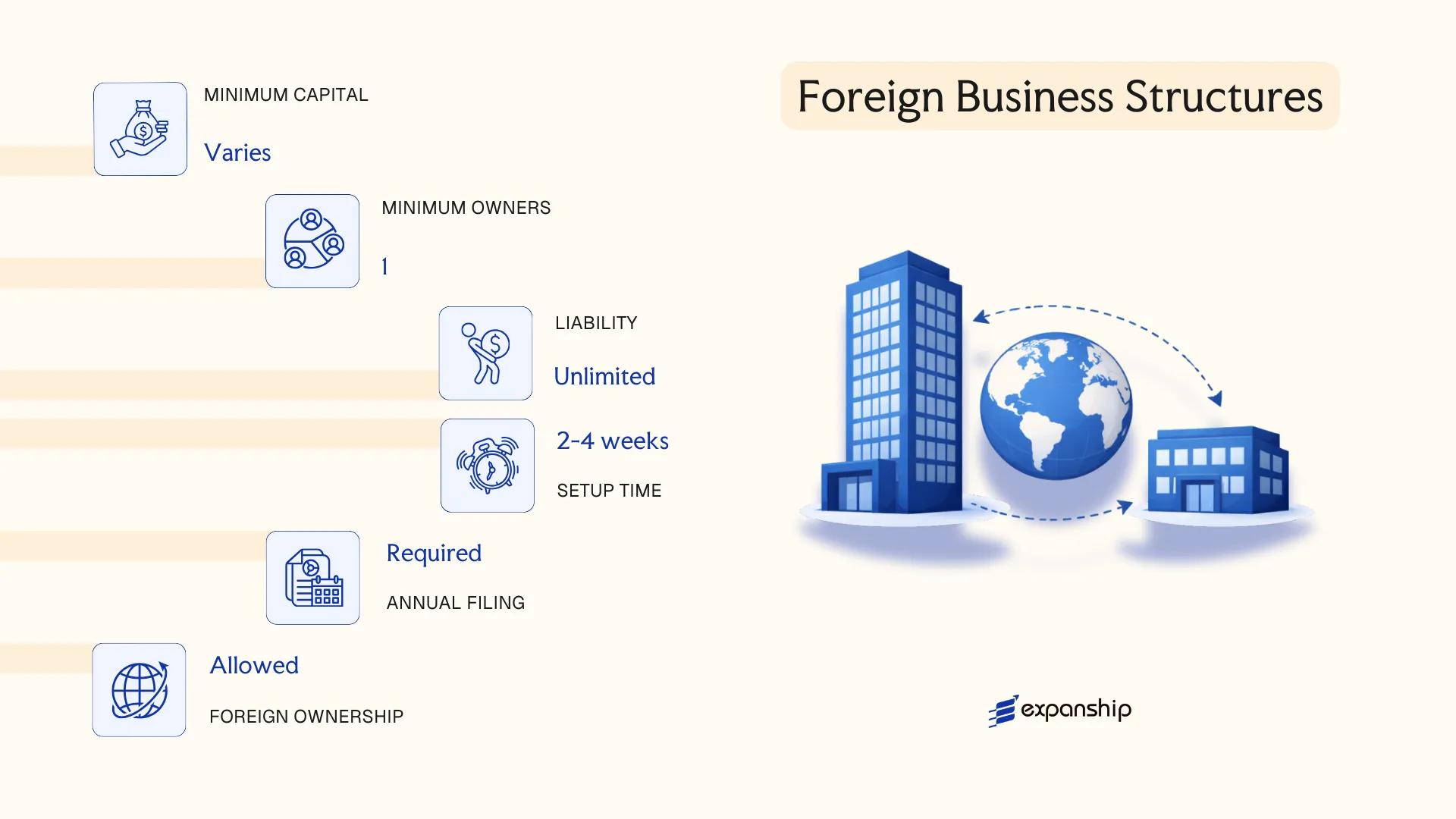

Foreign Business Structures in Angola [Branch Office, Representative Office]

Foreign company operations in Angola are governed primarily by the Private Investment Law (Law No. 10/18) and the Commercial Code, which together set out the conditions under which non-resident entities may establish a legal presence. Foreign branch office registration in Angola requires approval from the Agency for Private Investment and Export Promotion (AIPEX), and the process involves submitting documentation to the Guiché Único da Empresa (GUE), the single business registration window.

A branch has no separate legal personality from its parent — the foreign entity remains directly liable for all obligations incurred by the branch. A representative office, by contrast, is restricted to promotional and liaison activities and cannot engage in commercial transactions or generate local revenue.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Personality | None — extension of parent company | None — extension of parent company |

| Commercial Activity | Permitted | Not permitted; liaison only |

| Governing Members | Resident manager (mandatory) | Resident representative (mandatory) |

| Local Presence | Registered address in Angola required | Registered address required |

| Capital Requirement | Subject to minimum investment thresholds under Law No. 10/18 | No capital requirement |

| Liability | Parent bears full liability | Parent bears full liability |

Focus Points

- Taxation: Branches are subject to Industrial Tax (corporate income tax) at 25%, plus VAT at 14% on applicable supplies; withholding taxes apply to remittances to the parent entity.

- Economic Substance: A branch must maintain a genuine operational presence; a resident manager and physical office are required.

- Annual Compliance: Branches must file audited accounts locally and submit annual tax returns to the Administração Geral Tributária (AGT).

- Treaty Access: Angola has a limited tax treaty network; treaty benefits available to the parent may not automatically extend to the branch.

- Restrictions: Representative offices cannot invoice clients, hold bank accounts for commercial purposes, or repatriate profits.

Closing

A branch office suits foreign firms executing contracts or delivering services directly in the Angolan market, with the trade-off being full parental liability exposure. Representative offices are used primarily for market research, supplier coordination, or pre-investment activity where no revenue generation is intended.

A branch office is best suited for established foreign companies with confirmed commercial operations in Angola that require a formal, revenue-generating presence without incorporating a separate local entity.

Partnerships in Angola [General Partnership (Sociedade em Nome Colectivo), Limited Partnership (Sociedade em Comandita)]

Angolan partnership law is governed by the Lei das Sociedades Comerciais (Law No. 1/04 of 13 February 2004), which establishes the legal framework for both the Angola general partnership Sociedade em Nome Colectivo and the limited partnership Sociedade em Comandita. A general partnership carries unlimited joint and several liability for all partners, while a limited partnership introduces a two-tier liability structure separating active managers from passive investors.

Both forms possess separate legal personality upon registration with the Conservatória do Registo Comercial, meaning the entity can hold assets, enter contracts, and incur obligations in its own name.

Key Characteristics

| Requirement | Sociedade em Nome Colectivo | Sociedade em Comandita |

|---|---|---|

| Legal Form | General Partnership — unlimited liability for all partners | Limited Partnership — unlimited liability for general partners (sócios comanditados); limited liability for silent partners (sócios comanditários) |

| Members | Partners (sócios); minimum 2, no statutory maximum | Minimum 1 general partner + 1 limited partner; no statutory maximum |

| Liability | All partners: joint, several, and unlimited | General partners: unlimited; limited partners: capped at capital contribution |

| Local Presence | Registered office in Angola required | Registered office in Angola required |

| Capital | No statutory minimum prescribed under Law No. 1/04; contributions may be in cash or in kind | No statutory minimum; limited partners' liability tied to their declared contribution |

| Privacy | Partner names disclosed in public commercial registry | Both partner categories disclosed in public registry |

Focus Points

- Taxation: Partnerships are generally subject to Industrial Tax (Imposto Industrial) on business profits; VAT applies at the standard rate of 14% on taxable supplies; individual partners may also bear Personal Income Tax (IRT) obligations on distributed income; withholding tax may apply to certain payments made to non-resident partners.

- Annual Compliance: Entities must file annual accounts with the Conservatória do Registo Comercial and submit tax declarations to the Agência Geral Tributária.

- Restrictions: Foreign nationals serving as general partners face additional scrutiny under Angola's private investment regulations, including requirements under the Lei do Investimento Privado.

- Conversion: Law No. 1/04 permits conversion between commercial entity types through a formal amendment process, subject to creditor notification requirements.

- Treaty Access: Angola's limited double tax treaty network means treaty-based withholding tax relief is not broadly available for partnership income distributions.

Sub-Types

Sociedade em Nome Colectivo (General Partnership)

Every partner holds unlimited personal liability for the firm's debts, and management rights are ordinarily shared among all partners unless the articles of association restrict them. This structure is uncommon in practice and generally suits small, trust-based businesses where partners are closely related or known to one another.

Sociedade em Comandita (Limited Partnership)

The defining feature is the division between sócios comanditados (general partners bearing unlimited liability) and sócios comanditários (limited partners whose exposure does not exceed their capital contribution). This form can accommodate passive investors who wish to participate economically without taking on managerial responsibility or unlimited personal risk.

Closing

Partnership structures in Angola are used occasionally for professional services arrangements or family-owned trading businesses, but limited popularity relative to the Sociedade por Quotas reflects the burden of unlimited liability that general partners must accept. The two-tier liability structure of the Sociedade em Comandita offers a degree of investor protection, though the absence of a statutory capital minimum means creditor protections are weaker than in share-capital entities.

These structures are most appropriate for small, closely-held businesses or professional practices where all active participants are prepared to accept personal liability for the entity's obligations.

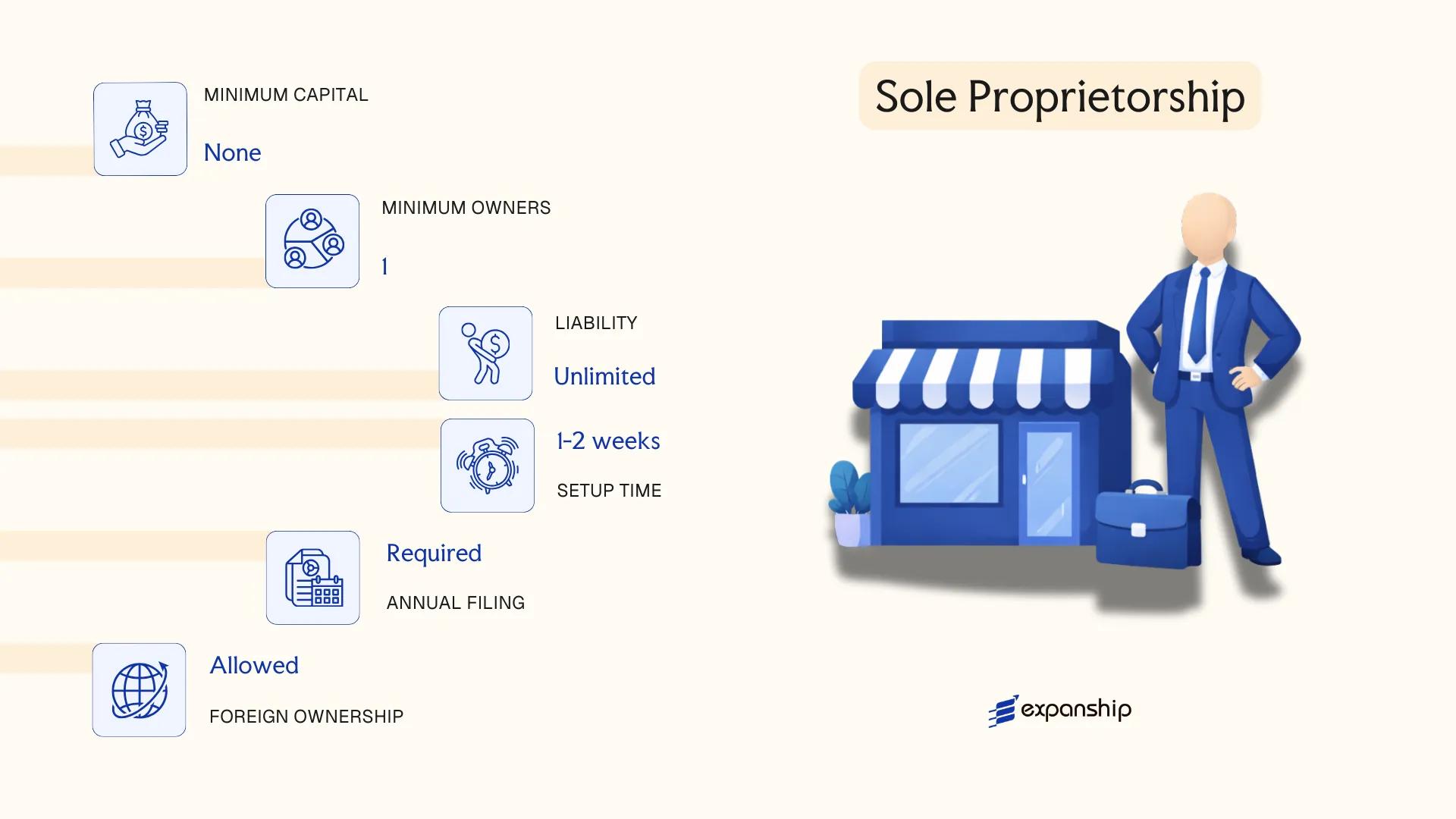

Sole Proprietorship (Empresário em Nome Individual)

The sole proprietorship Angola Empresário em Nome Individual is governed by the Companies Act (Lei das Sociedades Comerciais, Law No. 1/04) alongside supplementary provisions under the Commercial Registry Code. Unlike corporate forms, this structure does not create a separate legal personality — the business and its owner are treated as a single legal subject, meaning personal assets are exposed to all business liabilities without limitation.

Registration is handled through the Guichet Único do Empreendedor (GUE), the one-stop business registration centre administered by INAPEM. The proprietor must be a natural person, and the business operates under the owner's name or a registered trade name.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated sole proprietorship | No separate legal personality from the owner |

| Owner Reference | Proprietor (Empresário) | Single natural person only; no co-ownership permitted |

| Membership | 1 proprietor (minimum and maximum) | Legal entities cannot register as sole proprietors |

| Local Presence | Registered business address in Angola required | Must be a physical address; P.O. boxes not accepted |

| Capital | No statutory minimum capital in AOA | Capital is not formally subscribed or divided into shares |

| Liability | Unlimited personal liability | Personal assets are fully exposed to business debts |

| Privacy | Proprietor's name appears in public registry records | No structural separation between owner identity and business |

Focus Points

- Taxation: Subject to Industrial Tax (Imposto Industrial) under a simplified regime for small operators; VAT registration required once turnover thresholds are met; no withholding tax layer distinct from personal income obligations.

- Annual Compliance: Annual tax declarations must be filed with the Agência Geral Tributária (AGT); accounting records are required, though simplified bookkeeping may apply under the small taxpayer regime.

- Conversion: Can be converted into a Sociedade por Quotas, but the process requires a full new incorporation rather than a structural transformation of the existing registration.

- Treaty Access: As an unincorporated individual business, access to Angola's double tax agreements may be limited depending on treaty interpretation and residency status of the proprietor.

- Restrictions: Foreign nationals face significant barriers to registering as sole proprietors; this structure is effectively reserved for Angolan nationals or residents with qualifying status.

Closing

This structure suits micro-scale trading, freelance services, and early-stage individual entrepreneurs who operate domestically with low capital exposure. The primary advantage is administrative simplicity, but the absence of limited liability makes it unsuitable for activities carrying meaningful financial or legal risk.

Best suited for Angolan nationals operating small-scale, low-risk service or trade activities who do not require external investment or liability separation.

How to Choose the Right Entity Type in Angola

Selecting how to choose a business entity in Angola requires more than weighing registration costs — the structure you adopt governs your tax exposure, liability, operational permissions, and regulatory obligations from day one.

Why Your Entity Choice Matters

Choosing the wrong structure carries concrete legal and financial consequences:

- A foreign company conducting regular commercial activity through a representative office — which is legally restricted to liaison and promotional functions — operates in breach of the Private Investment Law and the Commercial Companies Law (Law No. 1/04), exposing the business to administrative penalties and forced cessation.

- Registering a branch rather than a locally incorporated entity can restrict your ability to bid on certain public procurement contracts, where Angolan law gives preference to domestically constituted companies.

- Selecting a structure that does not meet the minimum share capital thresholds set by the Instituto Nacional de Apoio às Micro, Pequenas e Médias Empresas (INAPEM) can disqualify your business from SME support programs and preferential financing schemes.

- Forming a Sociedade Anónima when your operation involves two or three shareholders adds mandatory audit, supervisory board, and public disclosure requirements that a Sociedade por Quotas does not impose at the same scale.

Key Factors to Consider

- Business Activity: Active trading, asset holding, and regulated sectors such as banking or insurance each require distinct structures under Angolan commercial law.

- Ownership Structure: A single-owner operation points toward an Empresário em Nome Individual or an SQ, while multi-investor arrangements may require the governance framework of an SA.

- Tax Objectives: Your eligibility for Industrial Tax, Investment Income Tax, or exemptions under the Private Investment Law depends directly on which entity type you register.

- Local vs. Foreign Operations: Entities intending to contract with Angolan residents or public bodies must be incorporated locally; a branch or representative office carries more restricted transactional capacity.

- Substance Capacity: If you cannot maintain a physical presence, staff, or local decision-making, certain entity types will expose you to non-compliance findings by the Agência Geral Tributária.

- Exit Strategy: Not all Angolan entity types permit straightforward conversion or redomiciliation — confirm whether your chosen structure supports the exit mechanism your investors may eventually require.

The full text of the Commercial Companies Law (Law No. 1/04) is available through the Angolan Ministry of Justice and Human Rights legal database.

Compliance Services for Companies in Angola

Ongoing compliance support for Angolan entities, covering statutory filings, tax obligations, and regulatory reporting requirements.

Conclusion

Selecting the right entity is one of the most consequential decisions in any Angola company incorporation summary. The Sociedade por Quotas is the most commonly registered structure in Angola, favored by small to mid-sized businesses for its relatively straightforward governance requirements. The Sociedade Anónima suits larger operations where share capital distribution across multiple investors is necessary. Branch and representative offices serve foreign firms testing the market or fulfilling contractual obligations without establishing a separate legal entity. General and limited partnerships remain less common, typically used in professional or family-held arrangements. Sole proprietorships carry unlimited liability, making them more appropriate for low-risk, small-scale activities.

Angola continues to develop its regulatory framework through the Agência Privada de Investimento e Promoção das Exportações (AIPEX) and incremental updates to the Private Investment Law, signaling a gradual effort to align corporate governance standards with international expectations. Your choice of structure will determine tax exposure, governance obligations, and operational flexibility from day one.

How Expanship Can Assist You

Expanship Angola company registration services are built around the specific requirements of Angolan corporate law, including the distinct obligations that apply to each entity form covered in this guide. From registering a Sociedade por Quotas with the Guichet Único do Empreendedor e da Empresa (GUEE) to establishing a branch of a foreign company, the process involves multi-step filings, notarized documentation, and coordination with the Agência de Investimento Privado e Promoção das Exportações de Angola (AIPEX) where applicable.

Expanship handles the full scope of incorporation and post-registration work on your behalf:

- Document preparation, notarization, and legalization

- Registered agent and legal address provision in Angola

- Government filing and liaison with GUEE and relevant public registries

- Post-incorporation compliance management, including annual obligations

- Corporate secretarial support

- Banking introduction assistance for newly incorporated entities

Get in touch with Expanship Angola to discuss your entity structure and next steps.

Frequently Asked Questions (FAQ)

The Sociedade por Quotas (SQ) is the most frequently registered structure, primarily because it requires fewer formalities than an SA and suits small to medium-sized businesses with a defined group of shareholders. Its lower minimum capital threshold and simpler governance framework make it the default choice for most market entrants.

A Branch Office has no separate legal personality and its parent company bears full liability for Angolan operations, whereas an SQ is a distinct legal entity with liability confined to its quota capital. Both are subject to Industrial Tax on locally sourced income, but an SQ generally carries greater compliance obligations, including annual accounts filed with the GARE registry.

Among available structures, the SA permits bearer-free registered shares and does not require public disclosure of beneficial ownership at the commercial registry level, though recent AML legislation has tightened disclosure obligations. Nominee arrangements are legally permissible but subject to regulatory scrutiny under Law No. 34/11 on money laundering prevention.

A sole proprietorship (Empresário em Nome Individual) requires only one natural person, and an SQ can be formed by a single quotaholder under the Companies Law (Lei das Sociedades Comerciais). Partnerships, by contrast, require at least two partners, and an SA mandates a minimum of five shareholders unless otherwise structured under specific statutory provisions.

Foreign investors may incorporate an SQ or SA, but doing so typically requires compliance with the Private Investment Law (Lei do Investimento Privado), which governs minimum investment thresholds and sector-specific restrictions. Certain industries, including media and defence, impose local participation requirements that affect the ownership structure available to non-residents.

Conversion between entity types is permitted under the Lei das Sociedades Comerciais, most commonly from an SQ to an SA as a business scales and seeks broader capital access. The process requires shareholder approval, amended articles of association, and re-registration with the Conservatória do Registo Comercial.

No. A General Partnership (Sociedade em Nome Colectivo) and a Branch Office do not possess separate legal personality, meaning partners or the parent entity remain directly liable. The SQ, SA, and Limited Partnership (Sociedade em Comandita) do hold separate legal personality under Angolan commercial law.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.