Key Takeaways

- The UAE's commercial company landscape is governed federally by the Ministry of Economy under Federal Decree-Law No. 32 of 2021, while individual emirates add a local licensing layer through their respective Departments of Economic Development.

- Among onshore structures, the Limited Liability Company is the most widely registered entity type, valued for its flexibility on ownership rules and liability treatment.

- Free zone entities — including the FZE, FZ-LLC, and FZC — operate under provisions separate from the mainland corporate tax regime introduced in 2023, making them particularly relevant for non-resident investors and export-oriented businesses.

- Civil companies remain the default structure for licensed professionals such as lawyers and accountants, while PJSCs and PrJSCs are reserved for capital-intensive operations or businesses with public fundraising requirements.

Introduction to Entity Types in United Arab Emirates

Located in the Arabian Peninsula, the United Arab Emirates shares borders with Saudi Arabia and Oman, with coastlines along both the Persian Gulf and the Gulf of Oman. A federation of seven emirates established in 1971, it operates as a sovereign state with a civil law framework that draws on both federal legislation and emirate-level regulation.

Understanding the types of business entities in UAE requires familiarity with the federal authority that oversees commercial registration: the Ministry of Economy, which administers the Commercial Companies Law (Federal Decree-Law No. 32 of 2021). Individual emirates also maintain their own Department of Economic Development offices, adding a local licensing layer to federal requirements.

From a tax standpoint, the UAE applies a territorial corporate tax regime introduced in 2023, with free zone entities operating under separate provisions.

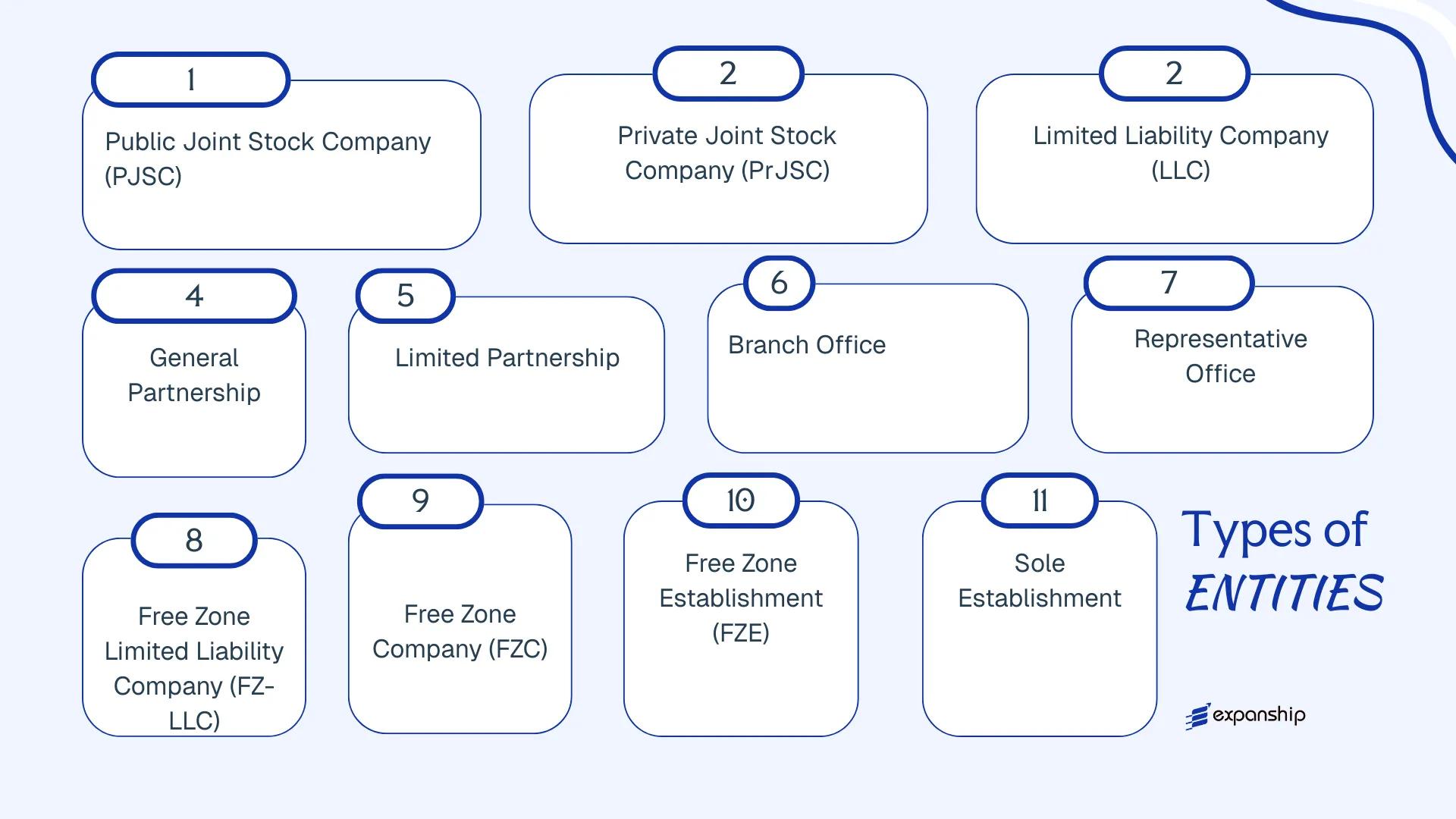

Available legal structures in United Arab Emirates include the Public Joint Stock Company, Private Joint Stock Company, Limited Liability Company, Civil Company, General Partnership, Limited Partnership, Branch Office, Representative Office, Sole Establishment, and a range of free zone-specific entities. Each structure carries distinct ownership rules, liability treatment, and regulatory obligations — this article examines each in detail.

An Overview of Business Structures in United Arab Emirates

Governed primarily by Federal Decree-Law No. 32 of 2021 on Commercial Companies, the UAE business structures overview spans a broad range of onshore, free zone, and foreign entity types. That law regulates most onshore commercial forms, while free zone entities fall under the individual regulations of each free zone authority. Each structure carries distinct ownership rules, liability parameters, and permitted activities.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Public Joint Stock Company (PJSC) | Corporate | Limited to shares | Taxed | Yes | 10 founders | SCA / MoEI | Fed. Decree-Law 32/2021 |

| Private Joint Stock Company (PrJSC) | Corporate | Limited to shares | Taxed | Yes | 3 shareholders | MoEI | Fed. Decree-Law 32/2021 |

| Limited Liability Company (LLC) | Corporate | Limited to shares | Taxed | Yes | 1–50 shareholders | MoEI | Fed. Decree-Law 32/2021 |

| Civil Company | Non-commercial | Unlimited | Taxed | Limited | 2+ partners | DoE (emirate-level) | Civil Transactions Law |

| General Partnership | Partnership | Unlimited | Taxed | Yes | 2+ partners | MoEI | Fed. Decree-Law 32/2021 |

| Limited Partnership | Partnership | Mixed | Taxed | Yes | 2+ partners | MoEI | Fed. Decree-Law 32/2021 |

| Branch Office | Branch | Parent liable | Taxed | Yes | Parent company | MoEI | Fed. Decree-Law 32/2021 |

| Representative Office | Branch | Parent liable | Exempt from trading | No | Parent company | MoEI | Fed. Decree-Law 32/2021 |

| Free Zone LLC (FZ-LLC) | Corporate | Limited | Taxed / Exempt | Free zone only | 1–50 shareholders | Respective FZRA | Free zone regulations |

| Free Zone Company (FZC) | Corporate | Limited | Taxed / Exempt | Free zone only | 2+ shareholders | Respective FZRA | Free zone regulations |

| Free Zone Establishment (FZE) | Corporate | Limited | Taxed / Exempt | Free zone only | 1 shareholder | Respective FZRA | Free zone regulations |

| Sole Establishment | Sole proprietorship | Unlimited | Taxed | Yes | 1 owner | DED (emirate-level) | Emirate-level commercial law |

Each of these structures is examined in full in the sections below.

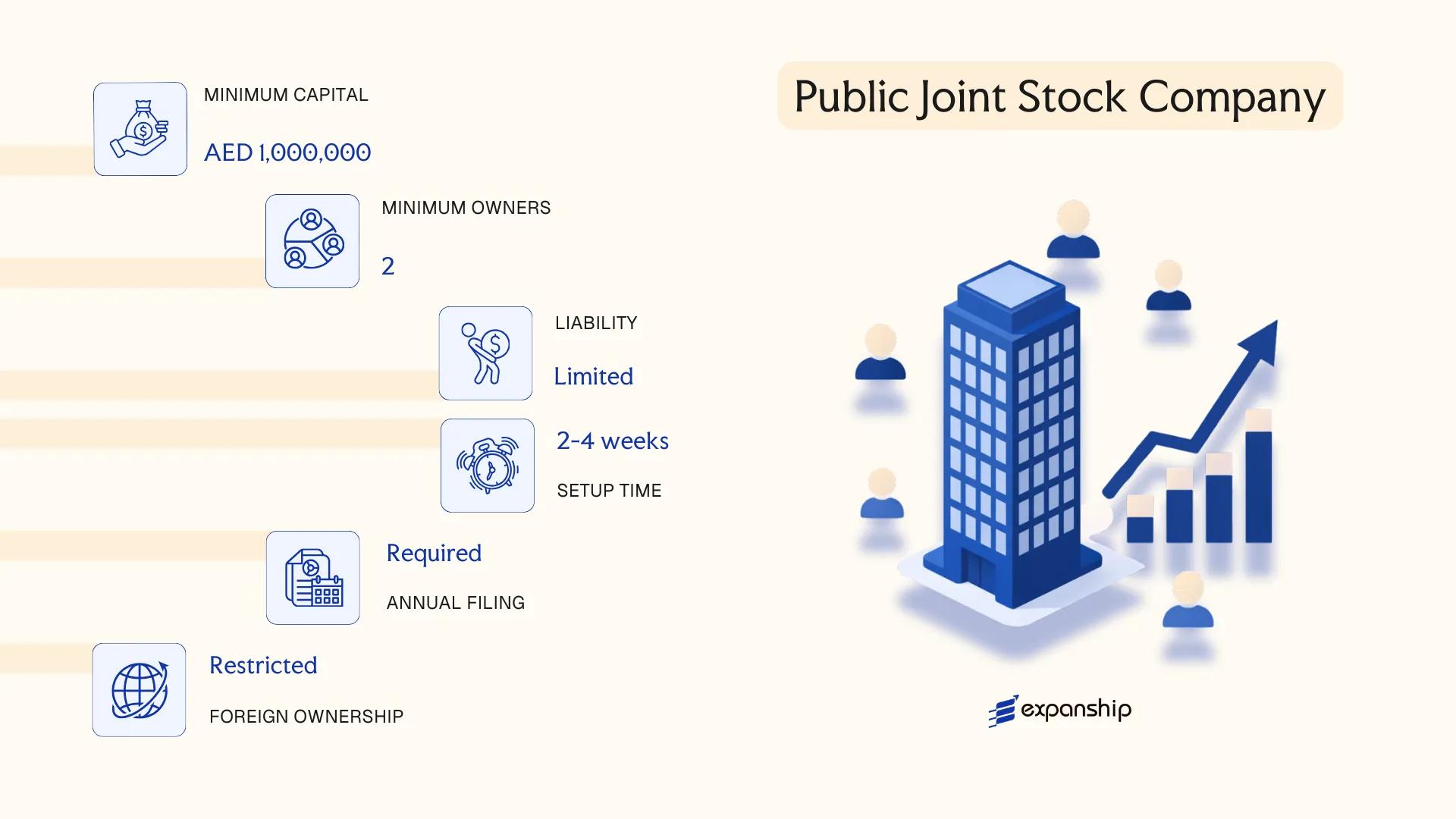

Public Joint Stock Company (PJSC)

A public joint stock company UAE PJSC is governed primarily by Federal Decree-Law No. 32 of 2021 on Commercial Companies, which replaced the earlier Companies Law No. 2 of 2015. The entity carries a separate legal personality, meaning its obligations are distinct from those of its shareholders.

Shares in a PJSC are offered to the public and listed on a recognised exchange such as the Abu Dhabi Securities Exchange (ADX) or the Dubai Financial Market (DFM). This listing requirement distinguishes it from its private counterpart and makes it the appropriate structure for large-scale capital mobilisation.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Joint Stock Company (PJSC) | Separate legal personality; limited liability for shareholders |

| Members | Shareholders; minimum 5 founders at incorporation | No prescribed maximum; shares freely transferable on exchange |

| Governing Body | Board of Directors; minimum 3, maximum 15 members | At least one UAE national required on the board |

| Local Presence | Registered office within the UAE required | Must maintain a physical address; registered agent not mandatory |

| Share Capital | Minimum AED 30 million for non-banking entities | Higher minimums apply for banks and insurance companies under sector regulators |

| Privacy | Shareholder register is publicly accessible | Financial statements must be published; limited confidentiality |

Focus Points

- Taxation: Subject to UAE corporate tax at 9% on taxable income exceeding AED 375,000; VAT at 5% applies to taxable supplies; no withholding tax on dividends or interest; no stamp duty on share transfers.

- Regulatory oversight: PJSCs are supervised by the Securities and Commodities Authority (SCA) in addition to the standard corporate registry; ongoing disclosure and prospectus obligations apply.

- Annual compliance: Mandatory audited financial statements, annual general meetings, and periodic filings with the SCA and relevant emirate authority.

- Economic substance: Activities falling under UAE Economic Substance Regulations may trigger annual notification and reporting requirements.

- Conversion: A private joint stock company may convert to a PJSC subject to SCA approval and fulfilment of the minimum capital and shareholder thresholds.

Closing

A PJSC suits large enterprises seeking public capital, including financial institutions, utilities, and real estate developers. The structure provides access to equity markets but carries significant ongoing regulatory and disclosure obligations that increase administrative burden considerably.

Established large-scale businesses or joint ventures planning a public listing on the ADX or DFM, where raising capital from the public is a core operational objective.

Company Incorporation in the UAE

Expanship assists with end-to-end incorporation of UAE entities, including Public Joint Stock Companies, across mainland and free zone jurisdictions.

Private Joint Stock Company (PrJSC)

A private joint stock company UAE PrJSC structure is governed by Federal Decree-Law No. 32 of 2021 on Commercial Companies, which replaced the earlier Companies Law No. 2 of 2015. The entity carries a separate legal personality distinct from its shareholders, with liability confined to each shareholder's capital contribution.

Unlike its publicly listed counterpart, a PrJSC cannot offer shares to the general public or list on a UAE stock exchange. This makes it a hybrid vehicle — structured with the corporate formality of a joint stock company while remaining privately held.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private Joint Stock Company (PrJSC) | Separate legal personality; governed by Federal Decree-Law No. 32 of 2021 |

| Members | Shareholders; Board of Directors (minimum 3 directors) | Minimum 3 shareholders; no maximum cap specified under the law |

| Local Presence | Registered address within UAE; must appoint a UAE-licensed auditor | Physical or flexi-desk office accepted depending on emirate |

| Capital | AED 5,000,000 minimum share capital | Must be fully subscribed at incorporation; shares are not publicly tradeable |

| Ownership | Up to 100% foreign ownership permitted in most sectors post-2021 reforms | Certain regulated sectors retain local ownership requirements |

| Privacy | Shareholder register not publicly disclosed | Financial statements are not publicly filed |

Focus Points

- Taxation: Subject to UAE corporate tax at 9% on taxable income exceeding AED 375,000 (effective June 2023); VAT applies at 5% where applicable; no withholding tax or stamp duty currently applies.

- Economic Substance: May be subject to Economic Substance Regulations if conducting a Relevant Activity as defined under Cabinet Resolution No. 57 of 2020.

- Annual Compliance: Mandatory audited financial statements, annual general meeting, and trade licence renewal required each year.

- Treaty Access: Qualifies as a UAE tax resident entity, potentially eligible for benefits under UAE's double tax treaty network subject to substance requirements.

- Share Transfer Restrictions: Share transfers require board or shareholder approval per the company's articles of association; no open-market mechanism exists.

Closing

A PrJSC suits businesses seeking a formally structured corporate vehicle for large-scale private operations, group holding arrangements, or pre-IPO structuring, though the AED 5,000,000 minimum capital requirement makes it less accessible for smaller ventures.

Best suited for established businesses or investor groups requiring a scalable, formally governed entity without immediate public listing obligations.

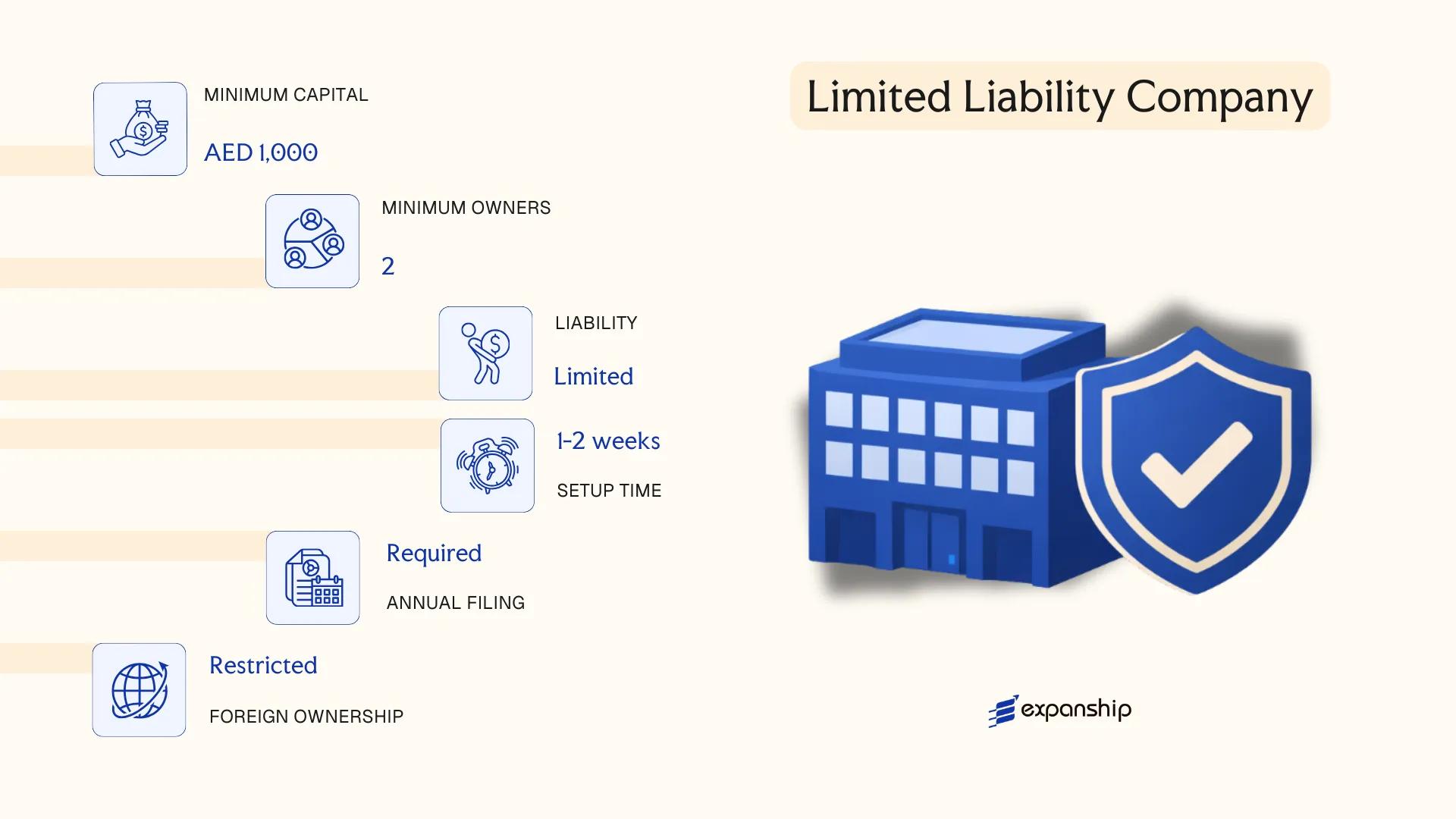

Limited Liability Company (LLC)

Governed by Federal Decree-Law No. 32 of 2021 on Commercial Companies, the LLC is the most widely used onshore structure for LLC company formation in UAE. It carries a separate legal personality distinct from its members, and shareholder liability is confined to their respective capital contributions.

The entity functions as a hybrid structure — combining corporate characteristics with contractual flexibility in how it is internally managed. A Memorandum of Association, attested by a notary and filed with the Department of Economy (DED) in the relevant emirate, formally constitutes the entity.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Company (LLC) | Separate legal personality; governed by Federal Decree-Law No. 32 of 2021 |

| Members | 1–50 shareholders | Single-member LLCs are permitted following 2021 reforms |

| Management | One or more managers (need not be shareholders) | Managers appointed via MoA or separate resolution |

| Local Presence | Registered office address in the emirate of incorporation | Physical or flexi-desk address accepted in most emirates |

| Capital | No statutory minimum capital under the 2021 law | Some regulated activities and specific emirates may impose their own minimums |

| Ownership | 100% foreign ownership permitted for most activities | Certain strategic sectors retain restrictions under Cabinet Resolution No. 55 of 2021 |

| Privacy | Shareholder details filed with DED; not publicly searchable in a centralised registry | Beneficial ownership is reported to the Registrar under Cabinet Decision No. 58 of 2020 |

Focus Points

- Taxation: Subject to federal Corporate Tax at 9% on taxable income exceeding AED 375,000 (effective June 2023); VAT at 5% applies if turnover exceeds the registration threshold; no withholding tax or stamp duty on share transfers.

- Economic Substance: LLCs conducting relevant activities as defined under Cabinet Resolution No. 57 of 2020 must satisfy economic substance requirements and file annual notifications.

- Annual Compliance: Annual financial statements are required; audit obligations depend on the emirate and activity type; trade licence renewal is mandatory each year with the relevant DED.

- Restricted Activities: Certain sectors — including oil and gas, utilities, and defence — are reserved for Emirati ownership or government entities regardless of the 2021 liberalisation.

- Conversion: An LLC may be converted to a Private or Public Joint Stock Company through a formal restructuring process subject to DED approval and shareholder resolution.

Closing

An LLC suits trading, services, consulting, and light manufacturing activities where onshore market access is required. The structure offers full legal standing to contract directly with government entities, though activities in restricted sectors remain subject to Emirati ownership requirements that cannot be waived.

Mid-to-large foreign businesses seeking direct onshore commercial operations across the UAE mainland with broad activity flexibility.

Civil Company

A civil company UAE setup is governed by Federal Law No. 5 of 1985 (the UAE Civil Code), as amended, rather than by the Commercial Companies Law that applies to most other business structures. This entity form is specifically reserved for licensed professionals and does not carry out commercial activities in the conventional sense.

Unlike commercial entities, a civil company does not acquire a separate legal personality distinct from its partners. Partners bear joint and unlimited liability for the firm's obligations, making this structure closer in nature to a professional partnership than a corporate vehicle.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Civil Company | Governed by UAE Civil Code, not Commercial Companies Law |

| Members | Partners (minimum 2, no statutory maximum) | All partners must hold relevant professional qualifications |

| Ownership | Up to 100% foreign ownership permitted in some free zones; mainland requires a UAE national service agent for certain licensed activities | Service agent holds no equity stake |

| Registered Office | Physical address required in the licensing emirate | Department of Economic Development or relevant emirate authority issues the licence |

| Capital | No statutory minimum capital requirement | Partners' contributions documented in the partnership agreement |

| Liability | Unlimited, joint and several | Partners are personally liable for firm debts |

Focus Points

- Taxation: Subject to 9% UAE corporate tax where applicable thresholds are met; VAT registration required if annual turnover exceeds AED 375,000; no withholding tax or stamp duty applies.

- Permitted Activities: Restricted to professional and consultancy services (medical, legal, engineering, accounting); commercial trading is not permitted under this licence type.

- Annual Compliance: Licence renewal required annually with the relevant emirate authority; partners must maintain valid professional licences throughout.

- Economic Substance: Generally not subject to Economic Substance Regulations unless the firm conducts a relevant activity as defined under Cabinet Resolution No. 57 of 2020.

- Conversion: Converting a civil company to a commercial entity requires re-licensing and restructuring; the process is not automatic and involves regulatory approvals.

Closing Paragraph

A civil company suits licensed professionals — doctors, lawyers, engineers, and consultants — who wish to practise jointly under a shared structure while retaining direct accountability to clients. The absence of a minimum capital requirement lowers the entry barrier, though unlimited personal liability remains a significant exposure for each partner.

Licensed professionals in UAE seeking a joint practice structure without the capital and governance requirements of a commercial company.

Partnerships [General Partnership, Limited Partnership]

Governed by Federal Decree-Law No. 32 of 2021 on Commercial Companies, the general and limited partnership UAE structures are among the older and less commonly adopted commercial forms available to businesses. Both carry unlimited liability exposure for at least one category of partner, which distinguishes them sharply from capital-based entities.

Under UAE law, partnerships do not carry a separate legal personality independent of their partners in the same way a joint stock or limited liability company does. Registration is handled through the Department of Economic Development (DED) in the relevant emirate, and the firm's name must include the name of at least one partner.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Partnership (General / Limited) | Governed by Federal Decree-Law No. 32 of 2021 |

| Members | General partners (min. 2); limited partners (min. 1 in limited partnership) | All general partners bear unlimited personal liability |

| Nationality Requirement | At least one UAE national partner required for mainland registration | Applies to both general and limited structures |

| Local Presence | Registered office address in the emirate of incorporation | No registered agent requirement, but DED registration is mandatory |

| Capital | No statutory minimum capital prescribed | Capital terms typically defined in the partnership agreement |

| Privacy | Partner names appear in the trade name and commercial register | Low privacy; publicly identifiable |

Focus Points

- Taxation: Subject to UAE corporate tax at 9% on taxable income exceeding AED 375,000; VAT registration required if taxable supplies exceed AED 375,000 annually; no withholding tax or stamp duty applies.

- Economic Substance: Relevant activities may trigger Economic Substance Regulations (ESR) obligations, requiring adequate local substance and annual reporting.

- Annual Compliance: Annual licence renewal with the DED, financial record maintenance, and corporate tax return filing with the Federal Tax Authority (FTA) are required.

- Treaty Access: Mainland partnerships may access UAE double tax treaties, subject to residency qualification under each treaty's provisions.

- Restrictions: Foreign nationals cannot hold general partner status on the mainland; business activities are restricted to those listed on the commercial licence.

Sub-Types

General Partnership

All partners hold equal managerial authority and bear unlimited joint liability for the firm's obligations. This structure is used primarily by UAE nationals operating family-run or professional businesses where shared control is intentional.

Limited Partnership

At least one general partner assumes unlimited liability, while limited partners contribute capital and remain liable only up to their contributed amount. Limited partners cannot participate in management without risking reclassification as general partners under the law.

Closing

Partnerships suit closely-held businesses where two or more founders prefer a contractually defined profit-sharing arrangement over a corporate structure, though unlimited liability for general partners remains a significant structural drawback for most commercial purposes.

This structure works best for UAE national partners operating family businesses or professional practices where shared management and personal accountability are acceptable outcomes.

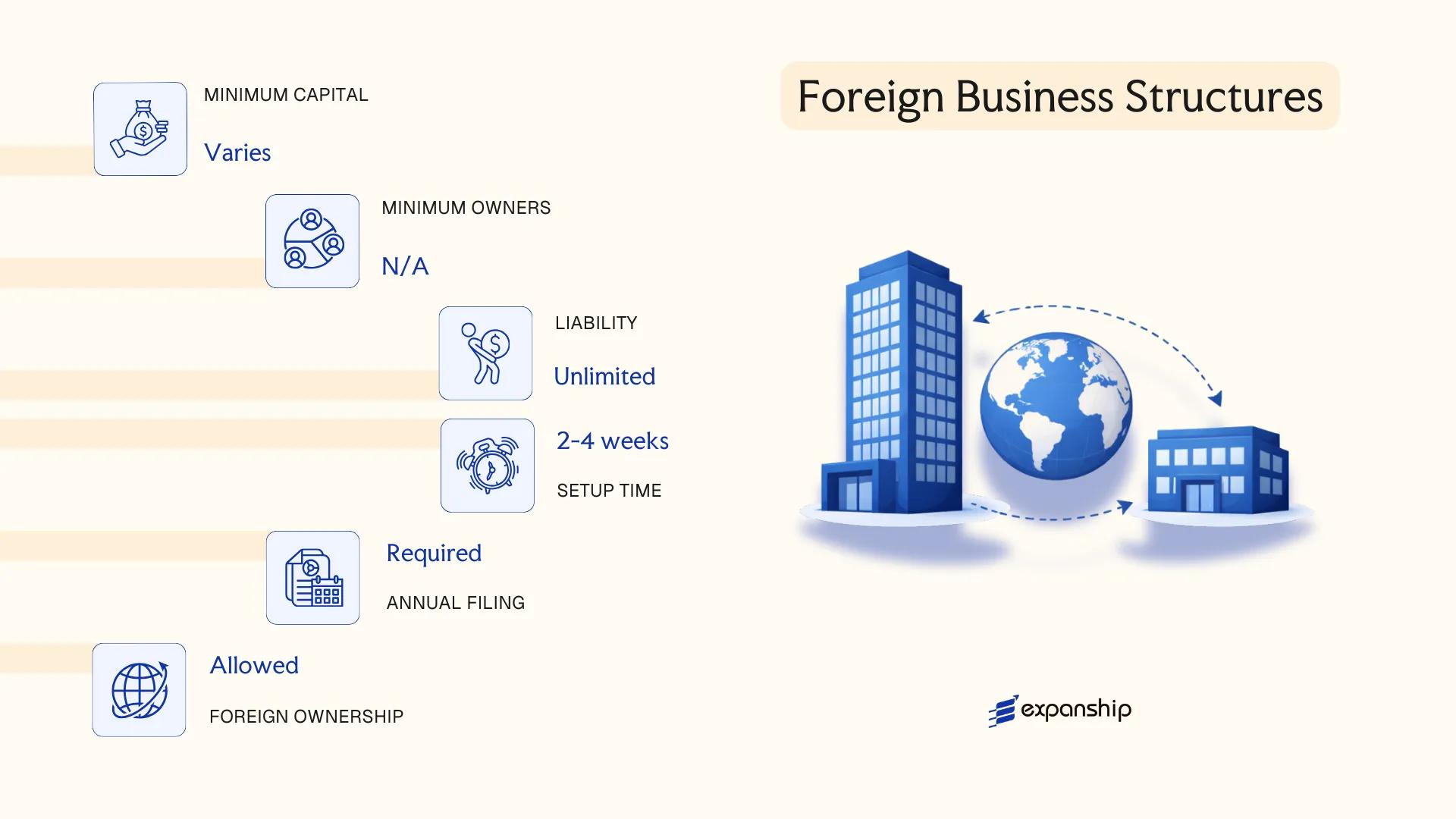

Foreign Business Structures [Branch Office, Representative Office]

A foreign company branch office in UAE operates as an extension of its parent entity rather than a distinct legal person — meaning the parent company bears full liability for all obligations incurred by the branch. Registration is governed primarily by Federal Decree-Law No. 32 of 2021 on Commercial Companies, along with sector-specific licensing requirements administered by the Ministry of Economy and the relevant emirate-level Department of Economic Development.

Both structures require appointment of a licensed local service agent — a UAE national or wholly UAE-national-owned company — though this agent holds no ownership stake and performs an administrative liaison function.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Personality | None (extension of parent) | None (extension of parent) |

| Commercial Activity | Permitted (within licensed scope) | Not permitted; promotional activities only |

| Local Service Agent | Required (UAE national) | Required (UAE national) |

| Minimum Capital | None mandated federally | None mandated federally |

| Ownership | 100% foreign parent | 100% foreign parent |

| Privacy | Parent financials may be referenced in filings | Parent financials may be referenced in filings |

Focus Points

- Taxation: Subject to UAE corporate tax (9% on taxable income above AED 375,000 from June 2023); VAT registration required if taxable supplies exceed the AED 375,000 threshold; no withholding tax or stamp duty.

- Economic Substance: Branch offices conducting relevant activities must satisfy Economic Substance Regulations (Cabinet Resolution No. 57 of 2020).

- Annual Compliance: Annual licence renewal, audited financial statements, and Ministry of Economy filing required for branch offices.

- Treaty Access: Access to UAE double tax treaties depends on the parent's jurisdiction and treaty provisions; professional advice is warranted before assuming treaty benefits apply.

- Restrictions: Representative offices cannot generate revenue, sign contracts commercially, or import goods for resale.

Sub-Types

Branch Office

A branch office can conduct the same business activities as its parent company within the scope of its UAE trade licence. It is commonly used by foreign firms seeking direct market operations — including trading, service delivery, or project execution — without incorporating a separate local entity.

Representative Office

A representative office is limited to market research, promotion, and liaison activities on behalf of the parent. No invoicing or revenue generation is permitted from UAE operations, making this structure suited to firms assessing the market before committing to full establishment.

Closing

Both structures suit foreign firms that require a UAE presence without relinquishing group-level ownership, though the parent's unlimited liability exposure is a material constraint for higher-risk operations.

Established foreign companies seeking operational presence or market entry in the UAE without forming a new local entity — particularly in professional services, contracting, or pre-investment market assessment.

Free Zone Entities [Free Zone LLC (FZ-LLC), Free Zone Company (FZC), Free Zone Establishment (FZE)]

Each free zone in the UAE operates under its own enabling legislation and authority — for example, the Dubai International Financial Centre is governed by DIFC Law No. 5 of 2018, while the Abu Dhabi Global Market follows ADGM Companies Regulations 2020. Free zone entities carry separate legal personality and benefit from limited liability, though the precise structural rules vary by free zone authority.

Across most free zones, UAE free zone company types FZE FZC and FZ-LLC share a common framework: 100% foreign ownership, no requirement for a local sponsor, and operations confined to the free zone or international markets unless a mainland distribution arrangement is in place.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited liability entity with separate legal personality | Exact designation varies by free zone authority |

| Members | Shareholders (FZE: 1; FZC: 2–5; FZ-LLC: 1–50, varies by authority) | FZE is single-shareholder; FZC suits small groups; FZ-LLC allows broader ownership |

| Management | Directors and/or managers as prescribed by each authority | Some free zones require a resident manager |

| Local Presence | Registered office within the free zone; physical or flexi-desk options available | Virtual offices permitted in select free zones |

| Share Capital | Varies by authority and entity type; no universal federal minimum | Some authorities require capital deposit before licence issuance |

| Privacy | Beneficial ownership disclosed to the free zone authority; not on public register in most zones | DIFC and ADGM maintain public registries |

Focus Points

- Taxation: Corporate tax at 9% applies to taxable income above AED 375,000 from June 2023 under Federal Decree-Law No. 47 of 2022; qualifying free zone persons may benefit from a 0% rate on qualifying income subject to meeting substance and other conditions. VAT at 5% applies where applicable; no withholding tax or stamp duty.

- Economic Substance: Entities conducting relevant activities must satisfy UAE Economic Substance Regulations under Cabinet Resolution No. 57 of 2020.

- Annual Compliance: Licence renewal, audited financial statements (required by most authorities), and Ultimate Beneficial Owner register filings are standard obligations.

- Treaty Access: Free zone entities are generally eligible for UAE double tax treaty benefits, subject to meeting residency and substance requirements.

- Restrictions: Direct trading on the UAE mainland requires a separate mainland licence or a locally registered distributor arrangement.

Sub-Types

Free Zone Establishment (FZE)

An FZE has a single shareholder, which may be an individual or a corporate entity. It is commonly used for sole-owner ventures or as a wholly owned subsidiary of a parent company seeking a free zone presence.

Free Zone Company (FZC)

An FZC accommodates between two and five shareholders, depending on the authority. This structure suits joint ventures or small partnerships where multiple parties require shared ownership within a free zone.

Free Zone LLC (FZ-LLC)

The FZ-LLC permits a broader shareholder base, with some authorities allowing up to fifty shareholders. It is structurally closer to a mainland LLC and is used where scalability or eventual conversion to a mainland entity is anticipated.

Closing

Free zone entities are well-suited to trading, holding, IP ownership, and international service businesses that do not require direct mainland retail access. The primary structural advantage is unconditional 100% foreign ownership without a local sponsor; the principal limitation is the restriction on direct mainland commercial activity without additional licensing.

Foreign investors and multinationals seeking a wholly owned UAE presence for international trading, holding structures, or regional headquarters, without the need for a local partner.

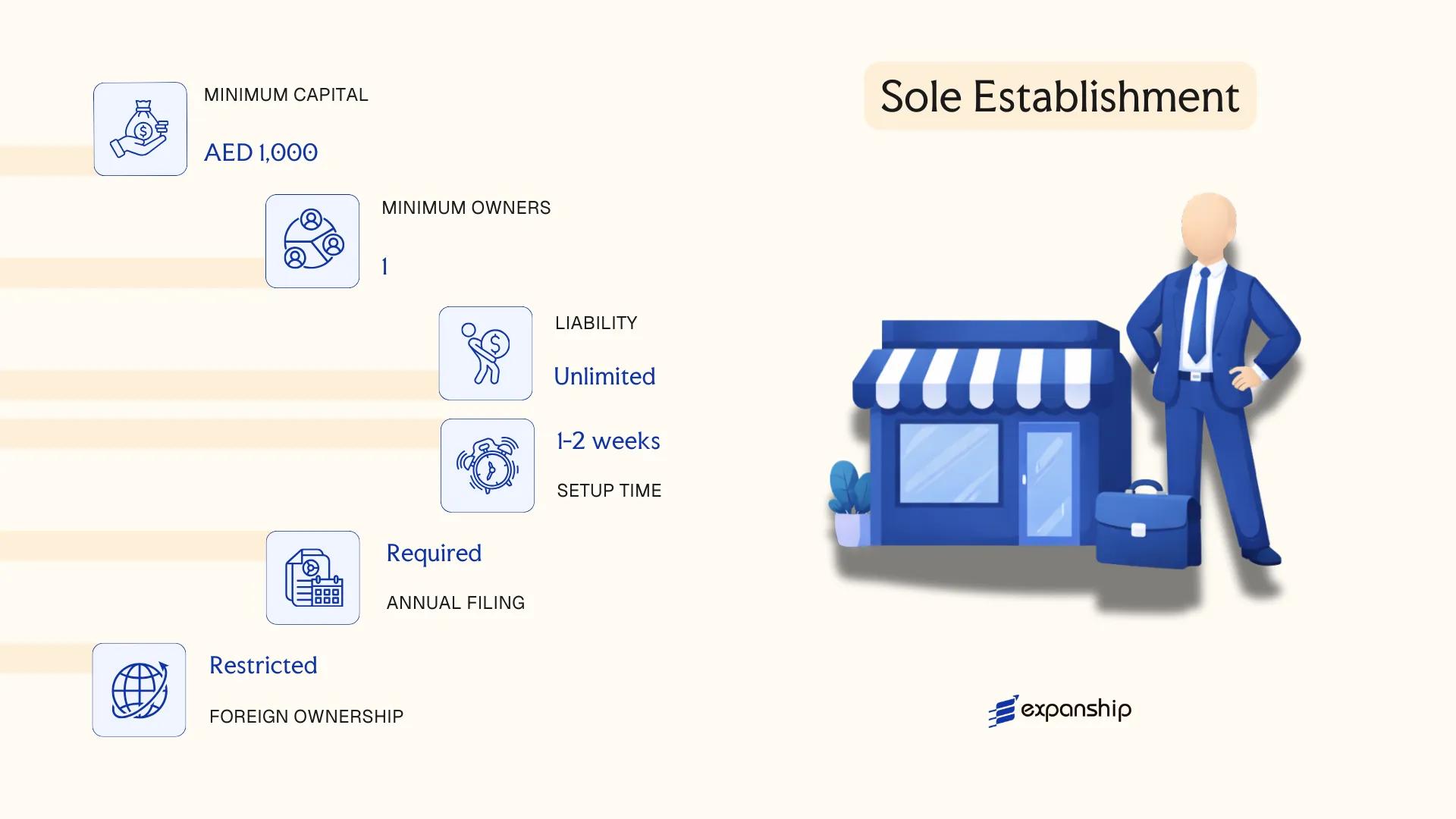

Sole Establishment

Sole establishment UAE registration is governed by Federal Law No. 37 of 1992 and, more recently, shaped by subsequent Commercial Companies Law amendments and individual emirate-level licensing regulations administered through the Department of Economic Development (DED) in each emirate. Unlike a limited liability company, a sole establishment carries no separate legal personality — the business and its owner are treated as a single legal unit.

This structure is the UAE equivalent of a sole proprietorship. The owner bears unlimited personal liability for all debts and obligations of the business, meaning personal assets are exposed in the event of a claim or insolvency.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated sole proprietorship | No separate legal personality from the owner |

| Members | Single proprietor only | UAE nationals or GCC nationals for most commercial activities; expatriates permitted for professional service licences |

| Local Presence | Physical office or flexi-desk required | Registered with emirate-level DED; address must be verifiable |

| Capital | No statutory minimum | Capital declaration may be required on the trade licence application |

| Liability | Unlimited personal liability | Owner's personal assets are fully exposed to business obligations |

| Privacy | Owner's name appears on trade licence | Limited confidentiality; publicly associated with the business |

Focus Points

- Taxation: Subject to the UAE's 9% corporate tax (effective June 2023) on taxable income above AED 375,000; VAT registration required if annual turnover exceeds AED 375,000; no withholding tax or stamp duty applies.

- Licensing restrictions: Expatriate owners are generally restricted to professional activity licences; commercial and industrial licences require UAE or GCC nationality.

- Annual compliance: Trade licence renewal required annually through the relevant emirate's DED; no mandatory audit for most sole establishments.

- Conversion: Can be converted to an LLC or other licensed structure, but the process requires a new incorporation rather than a structural amendment.

- Economic substance: Not typically subject to Economic Substance Regulations unless conducting a relevant activity as defined under Cabinet Resolution No. 57 of 2020.

Closing Paragraph

A sole establishment suits individual professionals — consultants, freelancers, and service providers — who operate independently and do not require a multi-shareholder structure. The primary advantage is administrative simplicity and low setup cost; the significant drawback is unlimited personal liability, which creates meaningful financial risk as the business scales.

UAE or GCC nationals running small commercial operations, or expatriate professionals seeking a straightforward licence for single-discipline service activities.

How to Choose the Right Entity Type in United Arab Emirates

Selecting the wrong entity structure carries direct legal and financial consequences, not theoretical ones.

Why Your Entity Choice Matters

Understanding how to choose the right business structure UAE requires confronting what goes wrong when the decision is poorly made:

- Registering a free zone entity and then conducting business with UAE mainland customers without the appropriate licensing puts the firm in breach of the relevant free zone authority's operating conditions and Federal Decree-Law No. 32 of 2021, exposing it to penalties or cancellation.

- Choosing a free zone entity solely for tax exemption may disqualify your business from accessing the UAE's double tax treaty network, as treaty eligibility depends on the entity's tax residency status and substance.

- Selecting a structure without adequate substance capacity when Economic Substance Regulations apply under Cabinet Resolution No. 57 of 2020 triggers reporting failures and administrative penalties.

- Forming an LLC when the underlying need is asset protection or succession planning creates ongoing shareholder obligations that a foundation established under applicable emirate-level legislation would not impose.

Key Factors to Consider

- Business Activity: Active trading, regulated sectors such as banking or insurance, and passive asset-holding each require distinct structures under UAE commercial law.

- Mainland vs. Free Zone Operations: Transacting directly with UAE-resident clients requires a mainland licence; free zone entities are restricted to operating within their designated zone or internationally.

- Ownership Structure: A sole founder points toward an FZE or Sole Establishment, while multi-party ventures require an LLC, partnership, or joint stock company.

- Tax Position: Your need for corporate tax exemption, treaty access, or qualification under the UAE's 9% corporate tax regime introduced by Federal Decree-Law No. 47 of 2022 should drive structure selection.

- Substance Capacity: If you cannot maintain genuine employees and decision-making activity in the jurisdiction, confirm whether your chosen entity type falls within a lower-threshold category under the Economic Substance Regulations.

- Exit and Conversion: Not all UAE structures permit redomiciliation or conversion; confirm the permitted exit mechanisms under Federal Decree-Law No. 32 of 2021 before committing to a form.

Corporate Compliance Services in the UAE

Maintain your UAE entity's good standing with accurate filings, regulatory reporting, and substance documentation.

Conclusion

Selecting the right structure is the central decision in any UAE company formation summary guide, and the options span a wide spectrum. The LLC suits most onshore trading and service businesses due to its flexibility on ownership and liability. PJSCs and PrJSCs serve companies with capital-intensive operations or plans for public fundraising. General and limited partnerships fit professional firms with defined partner arrangements. Civil companies remain the default for licensed professionals such as lawyers and accountants operating under UAE law. The Sole Establishment works for individual entrepreneurs requiring direct operational control. Free zone entities, particularly the FZE and FZ-LLC, attract non-resident investors and export-oriented businesses through their ownership and repatriation terms.

The LLC is consistently the most registered onshore entity type across the UAE. On the regulatory side, the country continues to expand its double tax treaty network and refine its corporate tax framework under Federal Decree-Law No. 47 of 2022, signalling a sustained shift toward international alignment. Expanship's advisory services are structured to support each stage of this process.

How Expanship Can Assist You

Expanship's UAE company incorporation services cover the full range of entities discussed in this blog — from mainland LLCs and civil companies registered with the Ministry of Economy to free zone structures governed by authorities such as ADGM, DIFC, or JAFZA. Your specific goals, ownership preferences, and operational requirements shape which entity makes sense, and Expanship's corporate services work around that assessment from day one.

Across each engagement, the scope of support includes:

- Document preparation, attestation, and legalization

- Registered agent and registered office provision

- Government filing and liaison with the relevant licensing authority

- Post-incorporation compliance management, including annual renewals

- Banking introduction assistance

Get in touch with Expanship UAE to discuss your specific incorporation requirements.

Frequently Asked Questions (FAQ)

The Limited Liability Company (LLC) is the most frequently registered onshore entity, governed by Federal Decree-Law No. 32 of 2021 on Commercial Companies. Its broad permissible activity range and ability to trade directly with UAE residents make it the default choice for most commercial operations.

A Free Zone LLC can be 100% foreign-owned and is exempt from federal corporate tax on qualifying income earned within the free zone, but it cannot trade directly in the UAE mainland without a local distributor or additional licensing. A mainland LLC is subject to the standard 9% corporate tax rate on taxable income exceeding AED 375,000, yet it holds unrestricted access to local markets.

Free Zone Establishments (FZEs) and Free Zone Companies (FZCs) registered in certain jurisdictions — such as RAKEZ or DMCC — offer a comparatively higher degree of ownership privacy, as beneficial ownership information is not always publicly accessible. Nominee arrangements are available through registered agents in select free zones, subject to the relevant free zone authority's rules.

A sole establishment requires exactly one natural person as owner and does not create a separate legal entity. An FZE is the free zone equivalent for single-person companies and does carry separate legal personality. Partnerships, by contrast, require a minimum of two partners under Federal Decree-Law No. 32 of 2021, making sole registration impossible for those structures.

Foreigners can establish FZEs, FZCs, and Free Zone LLCs with 100% ownership across the UAE's 40-plus free zones without a local partner. On the mainland, Federal Decree-Law No. 32 of 2021 removed the mandatory 51% Emirati ownership requirement for most activities, allowing full foreign ownership of LLCs in many sectors — though certain strategic activities remain restricted.

Conversion is permitted in defined circumstances. An LLC can be converted into a Public Joint Stock Company (PJSC) following the procedures outlined in Federal Decree-Law No. 32 of 2021, including minimum capital requirements and Securities and Commodities Authority approval. Converting a free zone entity to a mainland structure typically requires re-incorporation rather than a direct conversion.

No. A sole establishment has no legal personality distinct from its owner, meaning personal liability is unlimited. All other structures — including LLCs, PJSCs, PrJSCs, FZEs, and FZCs — carry separate legal personality under applicable federal or free zone legislation, which limits owner liability to their respective capital contributions.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.